Общие сведения о PRIIP

ВВОДНАЯ ИНФОРМАЦИЯ

В 2018 году была введена новая директива ЕС, предназначенная дли защиты клиентов, входящих в категорию розничных, посредством обеспечения их надлежащими уведомлениями при покупке определенных продуктов. Она известна как Закон ЕС об инвестиционных продуктах розничного и страхового бизнеса (MiFID II, Директива 2014/65/ЕС) или PRIIP и охватывает все инвестиции, где выплачиваемая клиенту сумма может колебаться в силу ее зависимости от справочных показателей или динамики активов, не находящихся в прямом владении данного розничного инвестора. Типичные примеры таких продуктов включают опционы, фьючерсы, CFD, ETF, ETN и другие структурированные финансовые инструменты.

Важно заметить, что брокер запретит розничному клиенту покупку продукта, подпадающего под условия PRIIP, если у эмитента будет отсутствовать уведомительный документ, необходимый брокеру для передачи этому клиенту. Речь идет о ключевой информационной документации или KID (англ. Key Information Document) - она содержит такие сведения, как описание продукта, стоимость, соотношение риска и прибыли, а также возможные сценарии производительности. PRIIP не затрагивает клиентов из США, поэтому эмитенты некоторых популярных американских ETF предпочитают не составлять KID. Это значит, что розничные клиенты из Европейской экономической зоны (англ. European Economic Area или EEA) не могут купить такие продукты.

КЛАССИФИКАЦИЯ КЛИЕНТОВ

IBKR классифицирует всех частных клиентов как розничных по умолчанию, поскольку это обеспечивает их самым высоким уровнем защиты в рамках MiFID. Клиенты, относящиеся к категории профессионалов, менее защищены в отличие от розничных, но на них не распространяется требование о документации KID. Согласно определению MiFID II профессионалы - это поднадзорные юридические лица, крупные клиенты, а также индивиды, которые запросили статус "Профессионал по выбору" и отвечают требованиям MiFID II относительно уровня знаний, опыта и финансовых возможностей.

IB предлагает клиентам возможность онлайн-запроса смены категории с "Розничный" на "Профессионал". Требования и пошаговые инструкции приведены в статье KB3298. Для отправки прямого запроса о переклассификации воспользуйтесь соответствующей анкетой в "Портале клиентов" или "Управлении счетом".

PRIIPs Overview

BACKGROUND

In 2018, an EU regulation, intended to protect “Retail” clients by ensuring that they are provided with adequate disclosure when purchasing certain products took effect. This disclosure document is referred to as a Key Information Document, or KID, and it contains information such as product description, cost, risk-reward profile and possible performance scenarios.

This regulation is known as the Packaged Retail and Insurance-based Investment Product Regulation (MiFID II, Directive 2014/65/EU), or PRIIPs, and it covers any investment where the amount payable to the client fluctuates because of exposure to reference values or to the performance of one or more assets not directly purchased by such retail investor. Common examples of such products include options, futures, CFDs, ETFs, ETNs and other structured products.

The UK Financial Conduct Authority (FCA) has equivalent requirements for UK residents.

It’s important to note that a broker cannot allow a Retail client to purchase a product covered by PRIIPs unless the issuer of that product has prepared the required disclosure document for the broker to provide to the client. U.S. clients are not impacted by PRIIPs, so the issuers of U.S. listed ETFs do not as a rule create KIDs. This means that EEA and UK Retail clients may not purchase the product. Clients nevertheless have several options:

- Many US ETF issuers have equivalent ETFs issued by their European entities. European-issued ETFs have KIDs and are therefore freely tradable.

- Clients can trade most large US ETFs as CFDs. The CFDs are issued by IBKRs European entities and as such meet all KID requirements.

- Clients may be eligible for re-classification as a professional client, for whom KIDs are not required.

CLIENT CATEGORISATION

We categorize all individual clients as “Retail” by default as this affords clients the broadest level of protection afforded by MiFID. Client who are categorised as “Professional” do not receive the same level of protection as “Retail” but are not subject to the KIDs requirement. As defined under MiFID II rules, “Professional” clients include regulated entities, large clients and individuals who have asked to be re-categorised as “elective professional clients” and meet the MiFID II requirements based on their knowledge, experience and financial capability.

We provide an online step-by-step process that allows “Retail” to request that their categorisation be changed to “Professional". The qualifications for re-categorisation along with the steps for requesting that one’s categorisation be considered are outlined in KB3298 or, to directly apply for a change in categorisation, the questionnaire is available in the Client Portal/Account Management.

Interactive Brokers (U.K.) Limited – Классификация MiFID

Введение

Законодательный акт Евросоюза под названием Директива о рынках финансовых инструментов (MiFID) с поправками согласно MiFID II требует, чтобы компания Interactive Brokers (U.K.) Limited (IBUK) классифицировала каждого клиента как "Розничный", "Профессиональный" или "Правомочный контрагент" согласно своим данным, знаниям и опыту.

Основываясь на правилах Инспекции по контролю за деятельностью финансовых организаций, IBUK относит большинство клиентов к разряду розничных, обеспечивая их повышенной защитой.

Только клиентам, являющимся поднадзорными юридическими лицами или фондами под управлением регулируемых администраторов, присваивается статус "Заведомо профессиональных клиентов".

К главным различиям в регулятивной защите профессиональных клиентов в отличие от розничных относятся:

1. Описание характера и рисков стандартизированных инвестиций: Фирма, предлагающая инвестиционные услуги в совокупности с другими услугами или продуктами или в качестве одного из условий соглашения с розничным клиентом, должна: (i) проинформировать розничных клиентов о том, могут ли риски, обусловленные данным соглашением, отличаться от рисков, сопряженных с его отдельными составляющими; и (ii) предоставить розничным клиентам надлежащее описание различных составляющих соглашения и того, как меняются риски при их взаимодействии. Вышеназванные требования не применимы к профессиональным клиентам, однако IBUK не будет делать подобного различия за исключением пункта 3 ниже.

2. Меры защиты инвесторов при работе с контрактами на разницу (CFD): Европейская служба по ценным бумагам и рынкам (ESMA) ввела меры вмешательства, касающиеся предоставления CFD-контрактов розничным клиентам. В эти меры входят: (i) ограничения кредитного плеча при открытии позиции, зависящие от волатильности андерлаинга; (ii) правило ликвидации согласно марже конкретного счета, которое стандартизирует процент маржи, обязующий поставщиков к закрытию одного или нескольких CFD-контрактов; (iii) защита счета от отрицательного баланса;

(iv) ограничение поощрительных программ по торговле CFD; и (v) стандартное предупреждение о рисках, включая процент убытков на счетах розничных клиентов у поставщика CFD. Вышеперечисленные требования не применимы к профессиональным клиентам.

3. Связь с клиентами: Фирма должна обеспечивать четкую, беспристрастную и понятную коммуникацию со всеми клиентами. Однако ее подход к общению с профессиональными клиентами (передача информации о компании, услугах, продуктах и вознаграждении) может отличаться от подхода к розничным. Обязанности фирмы касательно уровня детализации, формата и времени предоставления информации зависят от того, является ли клиент розничным или профессиональным. Требование о снабжении клиентов некоторыми документами по конкретным продуктам (например, ключевой информационной документацией (KID) об инвестиционных продуктах розничного и страхового бизнеса (PRIIP) не действует в отношении профессионалов.

4. Отчетность о снижении стоимости: Фирма, хранящая счета розничных клиентов, на которых имеются позиции по финансовым инструментам с кредитным плечом или транзакции с условными обязательствами, должна сообщать розничным клиентам о падении начальной стоимости каждого инструмента на 10 процентов и о последующих снижениях, кратных 10 процентам. Вышеназванные требования не применимы к профессиональным клиентам.

5. Уместность: При оценке уместности неконсультируемых услуг фирма может быть обязана определить, есть ли у клиента достаточные знания и опыт для понимания рисков, связанных с предлагаемым или запрашиваемым продуктом или сервисом. В случае такого требования у фирмы могут иметься основания полагать, что профессиональный клиент обладает необходимым опытом и знаниями, а поэтому понимает риски конкретных инвестиционных услуг и операций или типов транзакций/продуктов, в области которых он является профессионалом. Подобное предположение недопустимо по отношению к розничному клиенту, и оценка его знаний/опыта обязательна.

Компания IBUK предоставляет неконсультируемые услуги и в случае профессиональных клиентов не обязана запрашивать информацию или придерживаться тех же процедур оценки, что и при определении уместности конкретного продукта или сервиса для розничных клиентов. IBUK не должна предупреждать профессиональных клиентов, если ей не удается установить уместность какого-либо продукта или сервиса.

6. Исключение ответственности: По правилам FCA способность фирм сузить или исключить какие-либо обязательства или ответственность более ограничена при работе с розничными клиентами.

7. Служба финансового омбудсмена (FOS): Услуги FOS в Великобритании могут быть недоступны профессиональному клиенту, если он, к примеру, не является потребителем, малым бизнесом или частным лицом, ведущим деятельность вне своей профессиональной, деловой или торговой сферы.

8. Компенсация: Компания IBUK участвует в Программе Великобритании по компенсации в сфере финансовых услуг (FSCS). В случае невыполнения IBUK своих обязательств Вы можете потребовать возмещение в рамках этой программы. Результат будет зависеть от характера Вашей деятельности и обстоятельств предъявленного запроса; компенсация предоставляется только определенным типам заявителей и применительно к конкретным типам бизнеса. Приемлемость компенсации определяется согласно правилам программы.

Смена категории клиента на профессионала

IBUK позволяет розничным клиентам запросить смену их категории на "Профессионал". Ваша классификация указана в "Управлении счетом", раздел Настройки > Настройки счета > Категория клиента MiFID. В этом же окне можно запросить переклассификацию по MiFID.

IBUK рассмотрит возможность смены категории розничного клиента на профессиональную в двух случаях:

1. Клиенты, заведомо являющиеся профессионалами, могут сообщить IBUK, что, по их мнению, должны были быть классифицированы как таковые согласно правилам FCA, поскольку соответствуют как минимум одному из нижеприведенных условий:

(i) имеет полномочия осуществлять операции на финансовых рынках; или

(ii) является крупным предприятием, отвечающим двум из следующих требований размера в рамках одной компании:

(а) общий баланс в EUR 20,000,000 (или эквивалент в другой валюте);

(б) чистый оборот в EUR 40,000,000 ;

(в) собственные средства в EUR 2,000,000;

(iii) институциональный инвестор, чьей основной деятельностью является инвестирование в финансовые инструменты. Это включает юридические структуры, занимающиеся преобразованием активов в ценные бумаги или другими финансовыми транзакциями.

2. IBUK может классифицировать клиента как "Профессионал по выбору", если квалификаций, опыта и знаний клиента будет достаточно, чтобы убедить IBUK, что он способен принимать собственные инвестиционные решения и понимает сопряженные риски ввиду природы рассматриваемых транзакций или услуг. Лица, не отвечающие требованиям вхождения в категорию клиентов, заведомо являющихся профессиональными, могут запросить статус "Профессионал по выбору".

Для подобной переклассификации розничный клиент должен предоставить доказательство того, что он удовлетворяет хотя бы двум (2) следующим критериям:

1. За последние четыре (4) квартала клиент вел торговлю финансовыми инструментами в значительных объемах со средней частотой в десять (10) сделок за квартал.

Определяя, был ли объем значительным, IBUK основывается на следующих факторах:

а. За последние четыре квартала произошло как минимум сорок (40) сделок; и

б. За каждый из последних четырех (4) кварталов была осуществлена хотя бы одна (1) сделка; и

в. Общая номинальная стоимость сорока (40) главных сделок за последние четыре (4) квартала превышает EUR 200,000; и

г. Чистая стоимость активов (NAV) счета превышает EUR 50,000.

В данном расчете не учитываются сделки по спот-FX и "обезличенным" (unallocated) внебиржевым металлам.

2. Клиент владеет портфелем финансовых инструментов (включая деньги), чья стоимость превышает EUR 500,000 (или эквивалент в другой валюте);

3. Клиент является независимым владельцем индивидуального счета или трейдером счета организации, занимавшем или занимающим профессиональную должность в сфере финансов, где необходимы знания о продуктах, которыми он торгует.

Рассмотрев и проверив предоставленные сведения и подтверждающие документы, IBUK переклассифицирует клиента, если все актуальные условия были выполнены.

Розничные клиенты, запрашивающие смену категории на "Профессионал", должны прочесть и понять предупреждение от IBUK, прежде чем смогут отправить запрос.

Смена категории на "Розничный клиент" Профессиональные клиенты могут запросить, чтобы их переклассифицировали как розничных, через вышеописанный раздел "Управления счетом" (Настройки > Настройки счета > Категория клиента MiFID).

За исключением поднадзорных юридических лиц или фондов под управлением регулируемых администраторов, которым присваивается статус "Заведомо профессиональных клиентов", IBUK принимает все такие запросы.

ПРЕДСТАВЛЕННЫЕ СВЕДЕНИЯ ПРЕДНАЗНАЧЕНЫ ИСКЛЮЧИТЕЛЬНО ДЛЯ КЛИЕНТОВ, ОСУЩЕСТВЛЯЮЩИХ КЛИРИНГ В INTERACTIVE BROKERS.

ВНИМАНИЕ! ВЫШЕУКАЗАННАЯ ИНФОРМАЦИЯ НЕ ЯВЛЯЕТСЯ ВСЕОБЪЕМЛЮЩИМ ИЛИ ИСЧЕРПЫВАЮЩИМ ТОЛКОВАНИЕМ УПОМЯНУТЫХ НОРМ, А ПРЕДСТАВЛЯЕТ СОБОЙ ОБЩИЙ ОБЗОР ПОЛИТИКИ IBUK ПО КЛАССИФИКАЦИИ И ПЕРЕКЛАССИФИКАЦИИ КЛИЕНТОВ.

Interactive Brokers (U.K.) Limited – MiFID Categorisation

Introduction

The European Union legislative act known as the Markets in Financial Instruments Directive, or MiFID, as amended by MiFID II, requires Interactive Brokers (U.K.) Limited (IBUK) to classify each Client according to their knowledge, experience and expertise: "Retail", "Professional" or "Eligible Counterparty".

In accordance with the Financial Conduct Authority rules, IBUK categorises most clients as Retail clients, providing them with a higher degree of protection.

Only those clients that are either regulated entities or funds managed by regulated fund managers, are categorised as Per Se Professional Clients.

Professional Clients are entitled to a lower degree of protection under the UK regulatory regimes than Retail Clients. This notice contains, for information purposes only, a summary of the protections that a Retail Client might lose if they are to be treated as a Professional Client.

1. Description of the nature and risks of packaged investments: A firm that offers an investment service with another service or product or as a condition of the same agreement with a Retail Client must: (i) inform Retail Clients if the risks resulting from the agreement are likely to be different from the risks associated with the components when taken separately; and (ii) provide Retail Clients with an adequate description of the different components of the agreement and the way in which its interaction modifies the risks. The above requirements do not apply in respect of Professional Clients. However, IBUK will not make such differentiation apart from the case specified under point 3 below.

2. Retail investor protection measures on the provision of Contracts for Differences (“CFDs”): The regulatory measures include: (i) Leverage limits on the opening of a position, which vary according to the volatility of the underlying; (ii) A margin close out rule on a per account basis that standardises the percentage of margin (at 50%of the minimum required margin) at which providers are required to close out one or more open CFDs; (iii) Negative balance protection on a per account basis;(iv) A restriction on the incentives offered to trade CFDs; and (v) A standardised risk warning, including the percentage of losses on a CFD provider’s Retail investor accounts. These measures do not apply in respect of Professional Clients.

3. Communication with clients, including financial promotions: A firm must ensure that its communications with all clients are, and remain, fair, clear and not misleading. However, the simplicity and frequency in which a firm may communicate with Professional Clients (about itself, its services and products, and its remuneration) may be different to the way in which the firm communicates with Retail Clients. Regulations relating to restrictions on, and the required contents of, direct offer financial promotions do not apply to promotions to Professional Clients and such promotions need not contain sufficient information for Professional Clients to make an informed assessment of the investment to which they relate. A firm’s obligations in respect of the level of details, medium and timing of the provision of information are different depending on whether the client is a Retailor Professional Client. The requirements to deliver certain product-specific documents, such as Key Information Documents (“KIDs”) for Packaged Retail and Insurance-based Investment Products (“PRIIPs”), are not applied to Professional Clients.

4. Depreciation in value reporting to clients: A firm that holds a Retail Client account that includes positions in leveraged financial instruments or contingent liability transactions must inform the Retail Client, where the initial value of each instrument depreciates by 10 per cent and thereafter at multiples of 10 per cent. The above reporting requirements do not apply in respect of Professional Clients (i.e., these reports do not have to be produced for Professional Clients).

5. Appropriateness: For transactions where a firm does not provide the client with investment advice or discretionary management services (such as an execution-only trade), it may be required to assess whether the transaction is appropriate. When assessing appropriateness for non-advised services, a firm may be required to determine whether the client has the necessary experience and knowledge in order to understand the risks involved in relation to the product or service offered or demanded. Where such an appropriateness assessment requirement applies in respect of a Retail Client, there is a specified test for ascertaining whether the client has the requisite investment knowledge and experience to understand the risks associated with the relevant transaction. However, in respect of a Professional Client the firm is entitled to assume that a Professional Client has the necessary level of experience, knowledge and expertise in order to understand the risks involved in relation to those particular investment services or transactions, or types of transaction or product, for which the client is classified as a Professional Client. IBUK provides non-advised services and is not required to request information or adhere to the assessment procedures for a Professional Client when assessing the appropriateness of a given service or product as with a Retail Client, and IBUK may not be required to give warnings to the Professional Client if it cannot determine appropriateness with respect to a given service or product.

6. Information about costs and associated charges: A firm must provide clients with information on costs and associated charges for its services and/or products. The information provided may not be as comprehensive for Professional Clients as it must be for Retail Clients.

7. Dealing: When undertaking transactions for Retail Clients, the total consideration, representing the price of the financial instrument and the costs relating to execution, should be the overriding factor in any execution. For Professional Clients a range of factors may be considered in order to achieve best execution –price is an important factor, but the relative importance of other different factors, such as speed, costs and fees may vary. However, IBUK will not make such differentiation.

8. Difficulty in carrying out orders: In relation to order execution, firms must inform Retail Clients about any material difficulty relevant to the proper carrying out of orders promptly on becoming aware of the difficulty. This is not required in respect of Professional Clients. The timeframe for providing confirmation that an order has been carried out is more rigorous for Retail Clients’ orders than Professional Clients’ orders.

9. Share trading obligation: In respect of shares admitted to trading on a regulated market or traded on a trading venue, the firm may, in relation to the investments of Retail Clients, only arrange for such trades to be carried out on a regulated market, a multilateral trading facility, a systematic internaliser or a third-country trading venue. This is a restriction which may not apply in respect of trading carried out for Professional Clients (i.e., this restriction can be disapplied where trades in such shares are carried out for Professional Clients in certain circumstances).

10. Exclusion of liability: Firms’ ability to exclude or restrict any duty or liability owed to clients is narrower under the FCA rules in the case of Retail Clients than in respect of Professional Clients.

11. The Financial Services Ombudsman: The services of the Financial Ombudsman Service in the UK may not be avail-able to Professional Clients, unless they are, for example, consumers, small businesses or individuals acting outside of their trade, business, craft or profession.

12. Compensation: IBUK is a member of the UK Financial Services Compensation Scheme. You may be entitled to claim compensation from that scheme if IBUK cannot meet its obligations to you. This will depend on the type of business and the circumstances of the claim; compensation is only available for certain types of claimants and claims in respect of certain types of business. Eligibility for compensation from the Financial Services Compensation Scheme is not contingent on your categorisation but on how the firm is constituted. Eligibility for compensation from the scheme is determined under the rules applicable to the scheme (more information is available at https://www.fscs.org.uk/).

13. Transfer of financial collateral arrangements: As a Professional Client, the firm may conclude title transfer financial collateral arrangements with you for the purpose of securing or covering your present or future, actual or contingent or prospective obligations, which would not be possible for Retail Clients.

14. Client money: The requirements under the client money rules in the FCA Handbook (CASS) are more prescriptive and provide more protection in respect of Retail Clients than in respect of Professional Clients.

Re-categorisation as Professional Client

IBUK allows its Retail Clients to request to be re-categorised as Professional Clients. Clients are notified of their Client Category and can check it at any time from Account Management, under Settings> Account Settings> MiFID Client Category. From this same screen, Clients can also request to change their MiFID Category.

IBUK will consider re-categorising Retail Clients to Professional Clients in two instances:

1. Per Se Professional Clients can notify IBUK that they consider that they should have been categorised as Per Se Professionals under the FCA rules, because at least one of the following conditions applies:

(i) authorised or regulated to operate in the financial markets; or

(ii) a large undertaking meeting two of the following size requirements on a company basis:

(a) balance sheet total of EUR 20,000,000;

(b) net turnover of EUR 40,000,000;

(c) own funds of EUR 2,000,000;

(iii) an institutional investor whose main activity is to invest in financial instruments. This includes entities dedicated to the securitisation of assets or other financing transactions.

2. IBUK may treat Clients as Elective Professional Clients if, based on an assessment of the Client’s expertise, experience, and knowledge, IBUK is reasonably assured that, in light of the nature of the transactions or services envisaged, the Client is capable of making its own investment decisions and understand the risks involved. Clients who do not meet the requirements to be categorised as Per Se Professional Clients can still request to be categorised as Elective Professional Clients.

To obtain such re-categorisation, Retail Clients must provide evidence that they satisfy at least two (2) of the following criteria:

1. Over the last four (4) quarters, the Client conducted trades in financial instruments in significant size at an average frequency of ten (10) per quarter.

To determine the significant size IBUK considers the following:

a. During the last four quarters, there were at least forty (40) trades; and

b. During each of the last four (4) quarters, there was at least one (1) trade; and

c. The total notional value of the top forty (40) trades of the last four (4) quarters is greater than EUR 200,000; and

d. The account has a net asset value greater than EUR 50,000.

Trades in Spot FX and Unallocated OTC Metals are not considered for the purpose of this calculation.

2. The Client holds a portfolio of financial instruments (including cash) that exceeds EUR 500,000 (or equivalent);

3. The Client is an individual account holder or a trader of an organisation account who works or has worked in the financial sector for at least one year in a professional position which requires knowledge of products it trades in.

Upon review and verification of the information and supporting evidence provided, IBUK will re-categorise clients if all relevant conditions are met to satisfaction.

Retail Clients requesting to be re-categorised as Professional Accounts must read and understand the warning provided by IBUK before the relevant request is submitted.

Re-categorisation as Retail Client

Professional Clients can request IBUK to be re-categorised as Retail Clients, from the same Account Management page described above (under Settings> Account Settings> MiFID Client Category).

With the sole exception of regulated entities or funds managed by regulated fund managers, which are categorised as Per Se Professional Clients, IBUK accepts all such requests.

THIS INFORMATION IS GUIDANCE FOR INTERACTIVE BROKERS FULLY DISCLOSED CLEARED CUSTOMERS ONLY.

NOTE: THE INFORMATION ABOVE IS NOT INTENDED TO BE A COMPREHENSIVE, EXHAUSTIVE NOR A DEFINITIVE INTERPRETATION OF THE REGULATION, BUT A SUMMARY OF IBUK’S APPROACH TO CLIENT CATEGORISATION AND RE-CATEGORISATION POLICY.

Information Regarding Australian Regulatory Status Under IBKR Australia

Introduction

Australian resident customers maintaining an account with Interactive Brokers Australia Pty Ltd (IBKR

Australia), which holds an Australian Financial Services License, number 453554, are initially

classified as a retail investor, unless they satisfy one or more of the requirements to be classified as a

wholesale or professional investor according to the relevant provisions of the Corporations Act 2001.

This article outlines how this process is handled by IBKR Australia.

Australian Regulatory Status

All new customers of IBKR Australia default to being classified as a retail investor unless they produce to

IBKR Australia the required documentary evidence to allow IBKR Australia to treat them as a wholesale or

professional investor. Investors of IBKR Australia will only have their regulatory status change from

retail investor to either wholesale or professional investor subsequent to the required

documentation being received and approved by IBKR Australia.

What is a Wholesale Investor?

The most common way to be classified as a wholesale investor is to obtain a qualified accountant’s

certificate stating that you have net assets or net worth of at least $2.5 million AUD OR have a gross

annual income of at least $250,000 AUD in each of the last two financial years. The qualified

accountant’s certificate is only valid for two years before it needs to be renewed. We have prepared a

wholesale investor booklet, including a pro forma certificate for your accountant to complete, that

can be downloaded [here].

What is a Professional Investor?

In order to qualify as a professional investor, you must have an AFSL, be a body regulated by APRA, be a superannuation fund (but not a SMSF) and/or have net worth or liquid net worth of at least $10 million AUD. If you meet ONLY the financial criteria (i.e. net worth or liquid net worth of at least $10 million AUD), you will need to complete and submit to IBKR Australia the professional investor declaration contained within the professional investor booklet that we have prepared, which can be downloaded [here]. However, if you meet the criteria by virtue of having an AFSL, being a body regulated by APRA, or as a listed company (but not a SMSF), no booklet needs to be submitted.

What about Self-Managed Super Funds (SMSF’s)?

IBKR Australia have decided to treat all SMSF’s as retail investors, notwithstanding that they may meet the requirements to otherwise be classified as a wholesale or professional investor.

What about trusts?

For a trust to be considered as a wholesale investor, all trustees must be considered a wholesale

investor based on the tests described above.

Similarly, for a trust to be considered as a professional investor, all trustees must be considered a

professional investor based on the tests described above.

As a result, if at least one trustee is considered retail, the trust is considered a retail trust, regardless

of the status of any other trustees (if applicable).

Other

- For a full list of the disclosure documents and legal terms which govern the services IBKR Australia will make available please refer to the IBKR website.

- For further information on IBKR Australia, click on our Financial Services Guide.

- For more information or assistance, please contact IBKR Investor Services.

Запрет акций каннабиса клиринговой палатой

Служба Clearstream Banking и Штутгартская фондовая биржа объявили, что прекратят предоставлять услуги по ценным бумагам, напрямую или косвенно связанным с коноплей и другими наркотическими веществами. В результате операции с этими акциями на фондовых биржах Штутгарта (SWB) или Франкфурта (FWB) станет невозможна. По окончании торговли 19 сентября 2018 компания IBKR предпримет следующие действия:

- Принудительное закрытие сопряженных позиций, оставленных открытыми клиентом и не пригодных для перевода на рынок США; и

- Принудительный перевод сопряженных позиций, оставленных открытыми клиентом и пригодных для такого перевода, на рынок США.

Ниже Вы найдете таблицу затронутых акций согласно объявлению клиринговой службы Clearstream Banking и Штутгартской биржи по состоянию на 7 августа 2018 года. В ней также уточнена их пригодность для перевода на рынок США. Стоит заметить, что клиринговые палаты могут дополнять данный список, и поэтому клиентам рекомендуется сверяться с их сайтами для получения самой последней информации.

| ISIN | НАЗВАНИЕ | БИРЖА | ВОЗМОЖЕН ПЕРЕВОД В США? | СИМВОЛ В США |

| CA00258G1037 |

ABATTIS BIOCEUTICALS CORP |

FWB2 | Да |

ATTBF |

| CA05156X1087 |

AURORA CANNABIS INC |

FWB2, SWB2 | Да |

ACBFF |

| CA37956B1013 |

GLOBAL CANNABIS APPLICATIONS |

FWB2 | Да |

FUAPF |

| US3988451072 |

GROOVE BOTANICALS INC |

FWB | Да |

GRVE |

| US45408X3089 |

INDIA GLOBALIZATION CAPITAL |

FWB2, SWB2 | Да |

ICG |

| CA4576371062 |

INMED PHARMACEUTICALS INC |

FWB2 | Да |

IMLFF |

| CA53224Y1043 |

LIFESTYLE DELIVERY SYSTEMS I |

FWB2, SWB2 | Да |

LDSYF |

| CA56575M1086 |

MARAPHARM VENTURES INC |

FWB2, SWB2 | Да |

MRPHF |

| CA5768081096 |

MATICA ENTERPRISES INC |

FWB2, SWB2 | Да |

MQPXF |

| CA62987D1087 |

NAMASTE TECHNOLOGIES INC |

FWB2, SWB2 | Да |

NXTTF |

| CA63902L1004 |

NATURALLY SPLENDID ENT LTD |

FWB2, SWB2 | Да |

NSPDF |

| CA88166Y1007 |

TETRA BIO-PHARMA INC |

FWB2 | Да |

TBPMF |

| CA92347A1066 |

VERITAS PHARMA INC |

FWB2 | Да |

VRTHF |

| CA1377991023 |

CANNTAB THERAPEUTICS LTD |

FWB2 | Нет | |

| CA74737N1042 |

QUADRON CANNATECH CORP |

FWB2 | Нет | |

| CA84730M1023 |

SPEAKEASY CANNABIS CLUB LTD |

FWB2, SWB2 | Нет | |

| CA86860J1066 |

SUPREME CANNABIS CO INC/THE |

FWB2 | Нет | |

| CA92858L2021 |

VODIS PHARMACEUTICALS INC |

FWB2 | Нет |

ВАЖНО ЗНАТЬ:

- Обращаем внимание, что в США, как правило, ведется внебиржевая (PINK) торговля, и цены выражаются в USD, а не в EUR, что подвергает Вас валютному риску вдобавок к рыночному.

- Владельцам счетов с ценными бумагами типа PINK Sheet необходимо торговое разрешение Соединенные Штаты (мелкие акции) для ввода ордеров на открытие позиций.

- Все пользователи с торговым разрешением Соединенные Штаты (мелкие акции) должны перейти на 2-факторную систему входа в счет.

Clearinghouse Restrictions on Cannabis Securities

Boerse Stuttgart and Clearstream Banking have announced that they will no longer provide services for issues whose main business is connected directly or indirectly to cannabis and other narcotics products. Consequently, those securities will no longer trade on the Stuttgart (SWB) or Frankfurt (FWB) stock exchanges. Effective as of the 19 September 2018 close, IBKR will take the following actions:

- Force close any impacted positions which clients have not acted to close and that are not eligible for transfer to a U.S. listing; and

- Force transfer to a U.S. listing any impacted positions which clients have not acted to close and that are eligible for such transfer.

Outlined in the table below are impacted issues as announced by the Boerse Stuttgart and Clearstream Banking as of 7 August 2018. This table includes a notation as to whether the impacted issue is eligible for transfer to a U.S. listing. Note that the clearinghouses have indicated that this list may not yet be complete and clients are advised to review their respective websites for the most current information.

| ISIN | NAME | EXCHANGE | U.S. TRANSFER ELIGIBLE? | U.S. SYMBOL |

| CA00258G1037 |

ABATTIS BIOCEUTICALS CORP |

FWB2 | YES |

ATTBF |

| CA05156X1087 |

AURORA CANNABIS INC |

FWB2, SWB2 | YES |

ACBFF |

| CA37956B1013 |

GLOBAL CANNABIS APPLICATIONS |

FWB2 | YES |

FUAPF |

| US3988451072 |

GROOVE BOTANICALS INC |

FWB | YES |

GRVE |

| US45408X3089 |

INDIA GLOBALIZATION CAPITAL |

FWB2, SWB2 | YES |

ICG |

| CA4576371062 |

INMED PHARMACEUTICALS INC |

FWB2 | YES |

IMLFF |

| CA53224Y1043 |

LIFESTYLE DELIVERY SYSTEMS I |

FWB2, SWB2 | YES |

LDSYF |

| CA56575M1086 |

MARAPHARM VENTURES INC |

FWB2, SWB2 | YES |

MRPHF |

| CA5768081096 |

MATICA ENTERPRISES INC |

FWB2, SWB2 | YES |

MQPXF |

| CA62987D1087 |

NAMASTE TECHNOLOGIES INC |

FWB2, SWB2 | YES |

NXTTF |

| CA63902L1004 |

NATURALLY SPLENDID ENT LTD |

FWB2, SWB2 | YES |

NSPDF |

| CA88166Y1007 |

TETRA BIO-PHARMA INC |

FWB2 | YES |

TBPMF |

| CA92347A1066 |

VERITAS PHARMA INC |

FWB2 | YES |

VRTHF |

| CA1377991023 |

CANNTAB THERAPEUTICS LTD |

FWB2 | NO | |

| CA74737N1042 |

QUADRON CANNATECH CORP |

FWB2 | NO | |

| CA84730M1023 |

SPEAKEASY CANNABIS CLUB LTD |

FWB2, SWB2 | NO | |

| CA86860J1066 |

SUPREME CANNABIS CO INC/THE |

FWB2 | NO | |

| CA92858L2021 |

VODIS PHARMACEUTICALS INC |

FWB2 | NO |

IMPORTANT NOTES:

- Note that the U.S. listings generally trade over-the-counter (PINK) and are denominated in USD not EUR thereby exposing you to exchange rate risk in addition to market risk.

- Account holders maintaining PINK Sheet securities require United States (Penny Stocks) trading permissions in order to enter opening orders.

- All users on accounts maintaining United States (Penny Stocks) trading permissions are required use 2 Factor login protection when logging into the account.

Закон о розничных и страховых продуктах (PRIIP)

Закон ЕС об инвестиционных продуктах розничного и страхового бизнеса (акт № 1286/2014: Packaged Retail and Insurance-based Investment Products Regulation, сокр. PRIIP) вступил в силу 29 декабря 2014 года, и его положения начали действовать с 1 января 2018 года. Согласно закону, эмитенты обязаны создавать и регулярно обновлять ключевые информационные документы (КИД) о продуктах PRIIP, а продавцы или консультанты по торговле такими продуктами – предоставлять эти документы розничным инвесторам из Европейской экономической зоны (ЕЭЗ), чтобы помочь им в понимании и сравнении характеристик контрактов. Управление финансового надзора (FCA) установило аналогичные требования для проживающих в Великобритании.

Задачи закона о продуктах PRIIP

После финансового кризиса в 2008 году одной из главных задач Европейской комиссии стало повышение защиты клиентов и восстановление их уверенности в финансовых рынках.

Данный закон вводит новый стандартный ключевой информационный документ (КИД), чтобы помочь розничным инвесторам лучше понимать и сравнивать характеристики продуктов PRIIP. Продукт PRIIP – это любая инвестиция, где сумма, выплачиваемая инвестору, подвержена колебаниям, поскольку связана с определенным базовым показателем. Кроме страховых продуктов, к PRIIP также относятся ETF, опционы, фьючерсы, CFD, структурированные продукты и т.д.

Закон предназначен для защиты инвесторов; его главные задачи:

- Обеспечить понимание и удобство сравнения похожих продуктов для упрощения инвестиционных решений.

- Повысить прозрачность и уверенность в розничном инвестиционном рынке.

- Способствовать развитию единого европейского страхового рынка.

Для достижения этих целей закон стремится стандартизировать формат и содержимое ключевых информационных документов.

Что такое КИД?

Ключевой информационный документ, или КИД (англ. Key Information Document) – это 3-страничный документ, содержащий важные характеристики продукта, включая его общее описание, стоимость, профиль риска и возможные сценарии доходности.

На кого распространяется этот закон?

Закон распространяется как на эмитентов и дистрибьюторов продуктов PRIIP. Ответственность за создание и обновление документа лежит на эмитенте. Тем не менее любой дистрибьютор или финансовый посредник, предоставляющий розничному инвестору торговые или консультационные услуги по продуктам PRIIP или получивший от такого инвестора ордер на покупку PRIIP, должен предоставить ему ключевой информационный документ. Это также касается онлайн-площадок, которые осуществляют только исполнение.

Для кого предназначены документы КИД?

КИД должен быть предоставлен любому розничному инвестору, проживающему в ЕЭЗ и Великобритании, перед сделкой с продуктом PRIIP. Если эмитент не предоставил КИД, торговля этим продуктом будет недоступна для розничных клиентов из ЕЭЗ.

Обычно КИД должен быть предоставлен на официальном языке страны, в которой проживает клиент.

Однако клиенты IBKR соглашаются на получение уведомлений на английском языке, и поэтому если КИД доступен на английском, то все клиенты из ЕЭЗ и Великобритании могут торговать данным продуктом вне зависимости от страны проживания.

Если КИД не доступен на английском языке, но доступен на другом языке, например, на немецком, то торговать этим PRIIP могут только розничные клиенты из стран, в которых этот язык является официальным – в данном примере, клиенты из Германии, Австрии, Бельгии, Люксембурга и Лихтенштейна.

Как Interactive Brokers соблюдает этот регламент:

Для выполнения данных норм компания IB UK при необходимости будет предоставлять КИД в электронном виде (на странице PRIIPs KID Landing Page).

Где находится раздел с КИД для PRIIP?

Документы КИД доступны в специальном разделе нашего сайта – на странице PRIIPs KID Landing Page. Перейти на страницу КИД можно тремя способами: в Trader Workstation (TWS), с сайта IBKR или на "Портале клиентов".

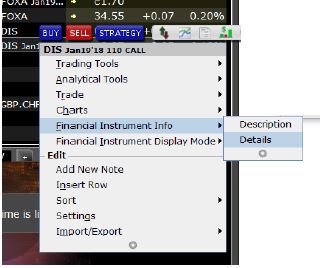

1. Как найти КИД в TWS:

- Авторизуйтесь в TWS.

- Щелкните правой кнопкой мыши по продукту, для которого Вам требуется КИД.

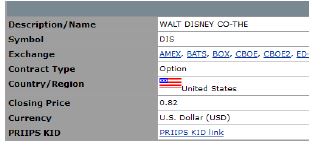

- В разделе "Информация о финансовом инструменте" (Financial Instrument Info) выберите "Детали" (Details).

- В окне данных контакта будет указана ссылка на КИД для этого PRIIP (PRIIPs KID link). Перейдите по ссылке, и откроется раздел документов КИД на "Портале клиентов".

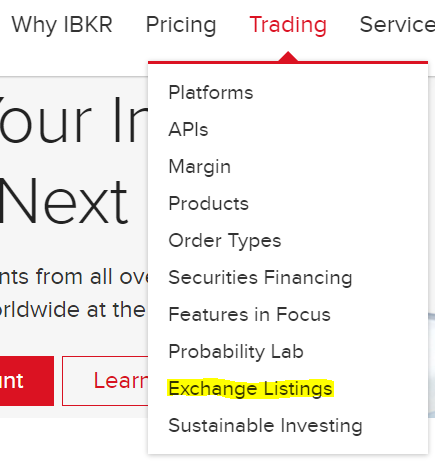

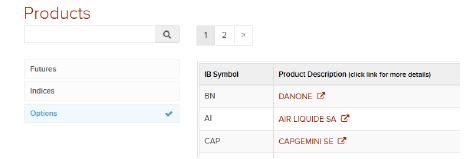

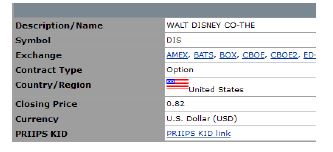

2. Как найти КИД на сайте IBKR:

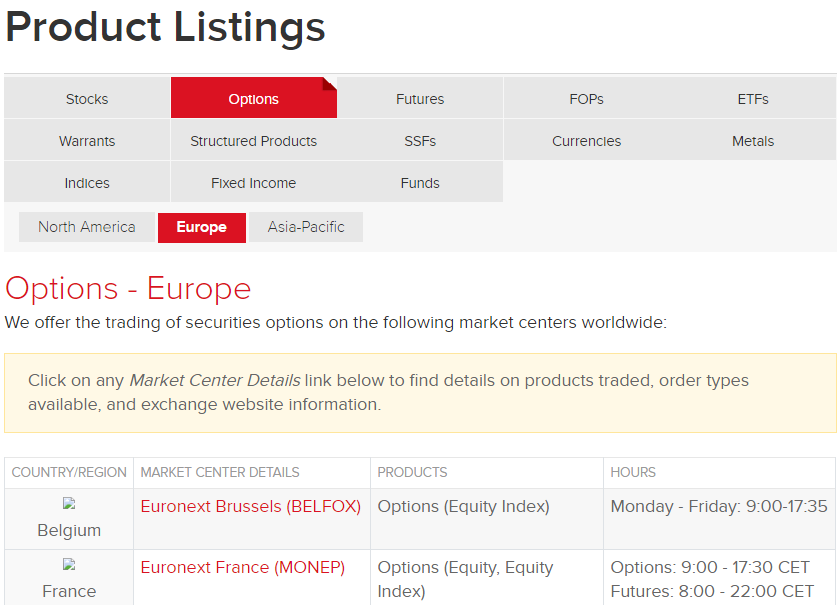

- На вкладке "Торговля" (Trading) и выберите "Список бирж" (Exchange Listings).

- Затем откройте "Список продуктов" (Product Listings). Выберите тип дериватива, а также регион и биржу желаемого продукта.

- Нажмите на нужный продукт, и откроется страница с данными контракта.

- На этой странице нажмите на ссылку на КИД для PRIIP (PRIIPs KID link), откроется раздел с документами КИД на "Портале клиентов".

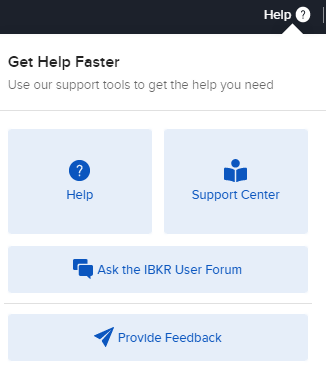

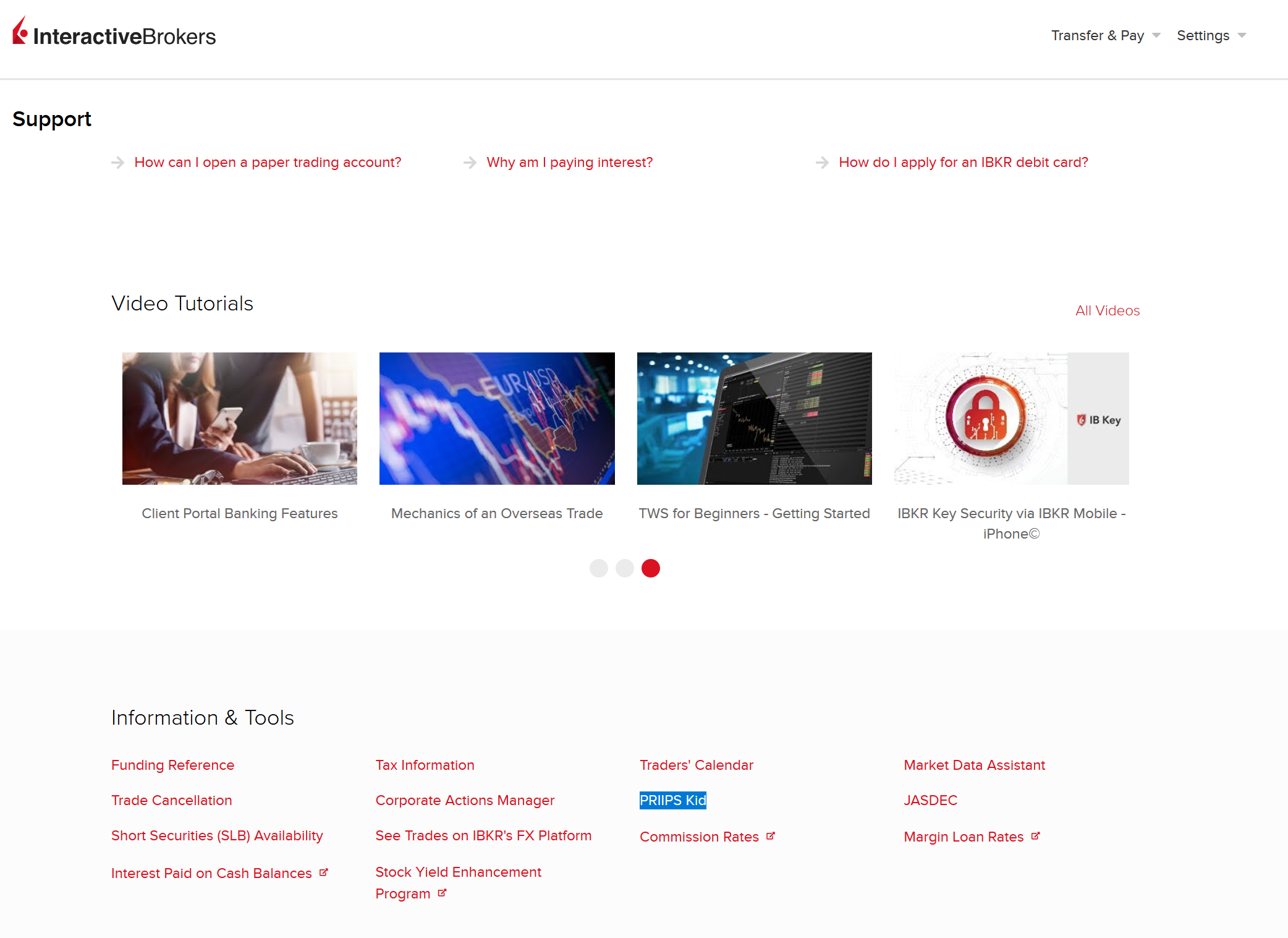

3. Как найти КИД на "Портале клиентов":

- Авторизуйтесь на "Портале клиентов".

- Откройте меню "Справка (?)" (Help) и перейдите в "Центр поддержки" (Support Center).

- В разделе "Информация и инструменты" выберите "PRIIPs KID", откроется раздел документов КИД.

Могу ли я торговать ETF США или другими недоступными PRIIP с помощью CFD?

Инвестор может получить доступ к ETF США или другим PRIIP, используя CFD (контракты на разницу), т.к. некоторые CFD отслеживают доходность базисных активов, включая ETF и другие продукты PRIIP.

Торговля CFD, которые отслеживают доходность ETF США или другого недоступного PRIIP, позволяет инвестору косвенно инвестировать в этот базисный актив. Это обусловлено тем, что стоимость CFD зависит от стоимости базисного актива, и любой рост или падение стоимости андерлаинга отразится на стоимости этого CFD.

Legal Entity Identifier Overview

BACKGROUND

The Legal Entity Identifier (LEI) is a 20-digit reference code that uniquely identifies legally distinct entities engaging in financial transactions globally, and across markets and jurisdictions. The LEI system was developed by the G-20 in accordance with ISO standards and the issuers of LEIs, referred to as Local Operating Units (LOU), supply registration and renewal services. Providing a unique identifier for each legal entity (along with key reference information associated with the entity) participating in financial transactions is intended to promote transparency.

DTC, in collaboration with SWIFT, operate as the local (U.S.) source provider of LEIs and maintains a website for the assignment of new and search of existing LEIs. See: http://www.gmeiutility.org/

SITUATIONS REQUIRING A LEI

In certain instances, brokers are required by regulation to report information regarding a client and include in that information a client identifier. For entities such as trusts and organizations, that identifier is referred to an a LEI. Examples of these reporting instances include the following:

CFTC Ownership and Control Reporting

MiFIR Transaction Reporting

China Stock Connect

EMIR reporting to trade repository

OBTAINING THE LEI

A LEI can be obtained by contacting an authorized LEI issuer, also referred to as a Local Operating Unit (LOU). The DTC, in collaboration with SWIFT, operates as a U.S. LOU and maintains a website for purposes of LEI registration and renewal. Note that LEI applicants can use the services of any accredited LOU and are not limited to using an LEI issuer in their own country.

In addition, as a service to its clients, IBKR will send an invite via Account Management to those who are required to obtain a LEI for trading or other regulatory reporting functions. Through this invite, the client can authorize IBKR to request an LEI through DTC on an accelerated basis (24 hours) and debit the client's account for the application fee and the annual renewal fee thereafter.

PRIIP Order Reject Translations

Clients entering opening orders for products covered by the PRIIPs Regulation where the issuer has not provided the required disclosure documents or Key Information Documents (KIDS) will have their order rejected and will receive the following reject message:

English

This product is currently unavailable to clients classified as 'retail clients'.

Note: Individual clients and entities that are not large institutions generally are classified as 'retail' clients.

There may be other products with similar economic characteristics that are available for you to trade.

French

Ce produit n’est pas actuellement disponible pour les clients considérés comme des clients “Particuliers/de détail”. Remarque : les clients particuliers et entreprises de détail qui ne sont pas de larges établissements sont classifiés comme des clients “de détail”.

D’autres produits aux caractéristiques similaires peuvent exister mais ne vous sont pas proposés au trading.

German

Dieses Produkt ist derzeit für Kunden, die als „Retail-Kunden” eingestuft werden, nicht verfügbar. Hinweis: Einzelkunden und Körperschaften, bei denen es sich nicht um große Institutionen handelt, werden grundsätzlich als „Retail”-Kunden bezeichnet.

Es ist möglich, dass Ihnen andere Produkte mit ähnlichen wirtschaftlichen Merkmalen zum Handel zur Verfügung stehen.

Italian

Questo prodotto al momento non è disponibile per i clienti “retail”. Nota: i clienti privati e le organizzazioni di non grandi dimensioni sono in genere classificati come clienti “retail”.

Potrebbero esserci altri prodotti con simili caratteristiche disponibili per le negoziazioni.

Spanish

Este producto no está actualmente disponible para clientes clasificados como “clientes minoristas”. Nota: los clientes individuales y las entidades que no sean grandes instituciones son clasificados, generalmente, como clientes “minoristas”.

Podría haber otros productos con características económicas similares que estén disponibles para que usted opere en ellos.

Russian

На данный момент этот продукт недоступен для розничных клиентов. Примечание: Частные лица и юридические структуры, не являющиеся крупными предприятиями, как правило, относятся к числу розничных клиентов.

Вам могут быть доступны другие продукты с похожими экономическими характеристиками.

Japanese

こちらの商品は現在「リテール・クライアント」として分類されるお客様にはご利用いただけません。注意:大きな機関ではない個人のお客様および事業体のお客様は、通常「リテール」クライアントとして分類されます。

似た経済特性を持つその他の商品で、お客様にお取引いただくことのできる商品がある可能性があります。

Chinese Simplified

该产品目前不适用于"零售客户"。 请注意:个人用户和非大型机构实体通常均被划分为"零售"客户。

可能有其他具有类似经济特征的产品适用于您的交易。

Chinese Traditional

該產品目前不適用於"零售客戶"。請注意: 個人用戶和非大型機構實體通常均被劃分為"零售"客戶。

可能有其他具有類似經濟特徵的產品適用於您的交易。

Please note, it is possible to be reclassified from Retail to Professional once certain qualitative, quantitative and procedural requirements are met. For more information on requirements, please see: How can I update my MiFID client category?