How to Complete CFTC Form 40

Clients maintaining a U.S. futures or futures option position at a quantity exceeding the CFTC's reportable thresholds may be contacted directly by the CFTC file with a request that they complete a Form 40. Contact will generally be made via email and clients are encouraged to respond to such requests in a timely manner to avoid trading restrictions and/or fines imposed by CFTC upon their account at the FCM.

Completion of the Form requires the following steps:

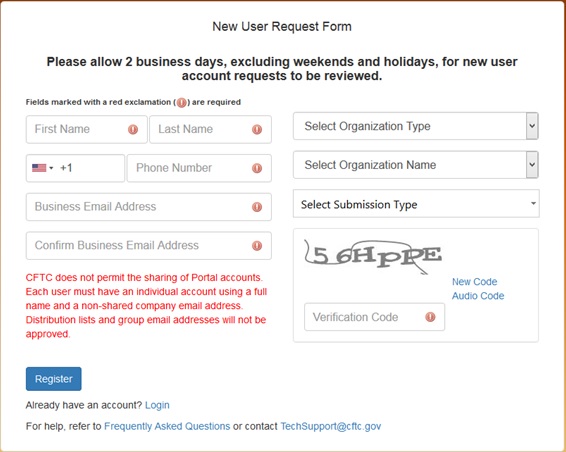

- Register for a CFTC Portal Account - performed online at: https://portal.cftc.gov/Account/Register.aspx Registration will require entry of the 9-digit code that the CFTC provided to you within the email requesting that you register. If you cannot locate your code or receive an invalid entry message, contact TechSupport@cftc.gov. When entering "Organization Type" from the drop-down selector, choose "LTR (Large Traders)".

2. Complete Form 40 - You will receive an email notification from the CFTC once your Portal Account has been approved. Note that this approval may take up to 2 business days from the date you complete the New User Request Form. The email will contain a link to the Portal where you will be prompted to log in: https://portal.cftc.gov/

Instructions for completing the form are available at: https://www.ecfr.gov/cgi-bin/text-idx?node=ap17.1.18_106.a

Note that Portal provides the opportunity to save a copy of your submission in XML format, a recommended step, as this allows for uploading the file to the Portal should you need to make modifications at a later date. This will eliminate the need to renter the form in its entirety.

The CFTC will send a confirmation email upon successful completion of your Form 40.

3. Confirm with IBKR - forward your confirmation email, or other evidence that you have submitted the Form 40 to cftc_form40_filing@interactivebrokers.com. This will assist to ensure that your account is not subject to CFTC directed restrictions or fines.

Overview of CFTC Form 40

The CFTC, the primary regulator of U.S. commodity futures markets and Futures Commission Merchants (FCMs), operates a comprehensive system of collecting information on market participants as part of its market surveillance and large trader reporting program.

IBKR, as a registered FCM providing clients with access to those markets, is obligated to report to the CFTC information on clients who hold a position in a quantity that exceeds defined thresholds (i.e., a "reportable position"). In order to report this information, IBKR requires clients trading U.S. futures or futures options to complete an online CFTC Ownership and Control Reporting form at the point the client requests futures trading permissions.

Once a client holds a "reportable position", the CFTC may then contact that client directly and require them to file more detailed information via CFTC Form 40. The information required of this report includes the following:

- Trader's name and address

- Principal business

- Form of ownership (e.g., individual, joint, partnership, corporation, trust, etc.)

- Whether the reporting trader is registered under the Commodity Exchange Act

- Whether the reporting trader controls trading for others

- Whether any other person controls the trading of the reportable trader

- Name and location of all firms through which the reportable trader carries accounts

- Name and location of other persons providing a trading guarantee or having a financial interest in account of 10% or greater

- Name of accounts not in the reporting trader's name in which the trader provides a guarantee or has a financial interest of 10% or more.

Clients who fail to complete this Form in a timely manner may be subject to trading restrictions and/or fines imposed by CFTC upon their account at the FCM. It is therefore imperative that clients immediately respond to these CFTC requests.

To complete the CFTC Form 40, clients must first register for a CFTC Portal Account, an online process which is subject to a review period of 2 business days from the point of initial registration to acknowledgement of approval by the CFTC. For information regarding this registration process and completing the Form 40, see KB3149.

MiFIR下EEA投资公司委托交易报告及其增强版

全新的2014/65/EC号指引(“MiFID II”)和(欧盟)600/2014 号法规(“MiFIR”)为报告由EEA投资公司执行的MiFID II下金融产品交易提出了新要求。(“MiFIR交易报告”)

谁受MiFIR交易报告要求约束?

所有欧洲经济区(“EEA”)投资公司均受新规约束,须在MiFIR覆盖的金融产品交易执行的一个工作日内报告所有交易。

盈透证券(英国)有限公司(“IBUK”)将向所有符合EEA投资公司定义的盈透证券集团(“IB”)客户提供协助,使其遵守新规要求。

除了使用IB平台的综合经纪商(其所有下属客户的头寸都保有在一个或多个综合账户中)外,所有作为EEA投资公司的IB客户都可选择要求IBUK代其履行报告义务。IBUK将通过法规要求的两种不同的报告机制代客户报告,即增强版交易报告和委托交易报告。

增强版交易报告

根据委员会委托监管条款(欧盟)2017/590第4条的规定,若IBUK将EEA投资公司(“定单传递公司”)提交的定单之详情纳入了其自己的交易报告,则定单传递公司可免于报告此类交易。

增强版交易报告仅适用于EEA投资公司代表其客户就IBUK提供服务的金融产品提交执行指令的交易(比如,财务顾问、基金经理或介绍经纪商账户为其客户子账户提交定单)。

委托交易报告

委托交易报告是IBUK向EEA投资公司提供的服务,帮助后者报告其提交的所有其他交易。

这包括投资公司通过其自营账户下达的交易、根据客户给出的全权委托指令提交的交易、以及IBUK不作为服务经纪商的金融产品之交易(即,由另一家IB关联公司担任服务经纪商的金融产品交易)。当交易是由投资公司的客户直接提交时,委托交易报告不适用。

此类报告将被提交给账户“法定住所”的国家主管部门(“NCA”),其中“法定住所”在启用了委托交易报告功能的账户的法律实体识别信息下记录(如,若投资公司的法定住所是荷兰,则交易将被报告给金融市场管理局(AFM))。

客户只需与IBUK签署一份协议即可同时覆盖增强版交易报告和委托交易报告。

如何使用增强版和委托交易报告服务

EEA投资公司(非披露介绍经纪商和综合介绍经纪商除外)将被要求在账户管理中完成一份电子表格,届时投资公司可选择使用IB的增强版或委托交易报告服务。

鉴于IB可能没有非披露介绍经纪商下属客户的完整身份信息,作为非披露介绍经纪商的投资公司不会收到以上电子表格,除非他们主动联系IB的客户服务部门,请求使用IBUK的增强版交易报告或委托交易报告服务并提供相应的信息。

IB平台上作为综合介绍经纪商的EEA投资公司无法使用增强版交易报告和委托交易报告服务。

使用IB的增强版和委托交易报告服务的EEA投资公司需签署相关法律协议并提供以下信息:

- 法律实体识别信息(“LEI”)。没有法律实体标识的客户可通过IBUK申请一个标识;

- 相关国家客户识别要求规定的每个经授权交易者的公民身份及更多信息;

- 投资公司内负责做投资决策的个人或算法;

- 之前被选为公司内部的投资决策者的活跃个人交易者。只允许是被授权作为账户交易者的个人;

- 公司可能用来做投资决策的算法的识别信息。客户有义务根据法规要求确定并提供算法识别信息。

新规将如何影响IB账户管理和定单输入系统

提交交易报告所需的某些信息可能视单个定单而不同,也可能要求提交交易的人提供信息。因此,IB已升级了IB账户管理系统及定单输入系统,使交易者得以提供所需的信息。

想要使用IB增强版和委托交易报告服务的账户应指定经授权的交易者,并提供做投资决策的算法的ID列表。

账户管理中列出的交易者和算法会在提交定单时于交易者工作站新增的下拉列表中显示。该区域会显示账户管理中选择的默认值。客户可在下拉列表中选择其他值。

IB交易者工作站将允许启用了增强版和委托交易报告功能的账户下经授权交易者就提交的特定定单选择公司内负责做投资决策的个人或算法。

注:常见MiFIR定义和条款列表,请见KB2980

本信息仅用于指导使用盈透证券清算服务的投资公司。本信息不适用于仅使用执行服务的账户。

注意:以上信息不作为全面穷尽式指南,也不是对法规的权威性解释,而是对MiFIR交易报告义务的总结。

MiFIR定义和条款

欧洲经济区(EEA) - 截至2017年10月,EEA由以下国家组成:奥地利、比利时、保加利亚、克罗地亚、塞浦路斯共和国、捷克共和国、丹麦、爱沙尼亚、芬兰、法国、德国、希腊、匈牙利、冰岛、爱尔兰、意大利、拉脱维亚、列支敦士登、立陶宛、卢森堡、马耳他、荷兰、挪威、波兰、葡萄牙、罗马尼亚、斯洛伐克、斯洛文尼亚、西班牙、瑞典和英国。

投资公司 - MiFID II第4 (1) (1)条将投资公司定义为以向第三方提供一项或多项投资服务为常规职能或业务的法人,及/或以专业的方式开展一项或多项投资活动的法人。该框架涉及的投资服务和活动在MiFID II附录I的第A部分列出。

执行的交易 - 就MiFIR交易报告而言,“交易”指完成买卖MiFIR覆盖的金融产品。当一笔交易是由于投资公司完成以下活动而产生时,该笔交易视为被执行:

- 接收或传递与一种或多种金融产品有关的定单(委员会委托监管条款(欧盟)2017/590号第4条规定的特例除外);

- 代表客户执行定单;

- 用自有账户交易;

- 根据客户给出的投资指令做投资决策;

- 向账户中转入或从账户中转出金融产品。

[参考:委员会委托监管条款(欧盟)2017/590号第2条和第3条]

IB经纪商 - 交易由以下盈透证券集团实体(“IB经纪商”)接收和/或传递之金融产品的账户:

- 盈透证券(英国)有限公司

- 盈透证券(中欧)有限公司

- 盈透证券(爱尔兰)有限公司

MiFIR覆盖的金融产品 - (欧盟)法规第600/2014号第26 (2)条(MiFIR)规定了与以下金融产品交易有关的交易报告义务,不论此类交易是否在交易场所进行:

- 在交易场所交易、获准在交易场所交易或已提交申请、希望获准在交易场所交易的金融产;

- 底层证券是在交易场所交易的金融产品的金融产品;以及

- 底层证券是由在交易场所交易的金融产品构成的指数或篮子的金融产品。

该法规覆盖的金融产品在MiFID II的C部分作了法律上的列举:

(1) 可转让证券;

(2) 货币市场产品;

(3) 集合投资活动的单位;

(4) 与证券、货币、利率或回报率、排放配额或其它衍生产品、金融指数或金融指标有关的,且可用实物或现金结算的期权、期货、互换、远期利率协议及任意其它衍生品合约;

(5) 与大宗商品有关的,且必须以现金结算或在未发生违约或其它终止事件的情况下可由交易的一方选择以现金结算的期权、期货、互换、远期及任意其它衍生品合约;

(6) 与大宗商品有关、且可用实物结算的期权、期货、互换及任意其它衍生品合约,前提是此类合约在受监管的市场、多边交易设施(MTF)或有组织交易设施(OTF)上交易,但在OTF上交易且必须以实物结算的批发能源产品除外;

(7) 可用实物结算但未在本段第6点中提及的与大宗商品有关的期权、期货、互换、远期及任意其它衍生品合约,此类合约不用于商业用途,而具有其它衍生金融产品的特点;

(8) 用于转移信用风险的衍生品;

(9) 金融差价合约;

(10) 与气候变量、运费率、通货膨胀率或其它官方经济指标有关的,且必须以现金结算或在未发生违约或其它终止事件的情况下可由交易的一方选择以现金结算的期权、期货、互换、远期利率协议及任意其它衍生品合约,以及与资产、权利、义务、指数及本部分未提及的指标有关、且在某些方面(包括但不限于是否在受监管的市场、OTF或MTF上交易)具有其它衍生金融产品的特征的任意其它衍生品合约;

(11) 由2003/87/EC号法令(排放交易机制)承认的任意单位构成的排放配额。

国民身份识别信息 - 在MiFIR下,自然人必须根据特定国民识别信息的优先级要求报告该识别信息,其中优先级取决于MiFIR认可的国籍。身份识别信息可为护照、身份证、税务代码、个人代码或全名和生日的串联(“串联”)。IB经纪商只要求客户提供IBUK尚未获得的国民身份识别信息。

法律实体标识(“LEI”)= 一个基于ISO 17442的由20字符构成的独特识别信息,用于在全球范围内识别参与金融交易的法律实体。

能以客观可衡量的方式降低风险的大宗商品衍生品交易- 在报告大宗商品衍生品交易时,IB经纪商须说明该交易根据2014/65/EU号指引第57条(第57条)是否能以客观可衡量的方式降低风险。 仅当此类交易是来自非金融实体持有的账户,且根据第57条,此类实体通过该账户交易大宗商品衍生品的目的是客观降低与其业务活动直接有关的风险时,IB经纪商才会允许此类交易。(如生产小麦的公司交易此类衍生品以对冲业务活动的风险)。(如生产小麦的公司交易此类衍生品以对冲业务活动的风险)。

在账户管理的交易权限部分作出以上声明的账户持有人同意,该账户执行的所有大宗商品衍生品交易的目的都是第57条规定的降低风险,且IB经纪商会相应地报告相关交易。

在有报告义务的公司负责做投资决策的个人或算法 - 在MiFIR下,投资公司有义务在交易报告中列明公司内负责就买/卖金融产品做投资决策的主要负责人或算法。只有单个个人或算法可被认定为是某笔交易的负责人,而投资公司必须根据委员会委托监管条款(欧盟)2017/590号第8条的规定报告此类个人或算法。

考虑到此类报告要求,IB经纪商已在账户管理和IB交易者工作站中推出了新的板块和新功能,帮助通过IB经纪商报告交易的投资公司按新法规的要求报告相关个人和算法。

在有报告义务的公司负责执行交易的个人 - 委员会委托监管条款(欧盟)2017/590号第9条要求投资公司报告决定接入哪个交易场所[…]、向哪家公司传递委托单或与委托单执行有关的任意其它条件的个人或算法。对于大多数交易报告,本要求仅适用于IB经纪商,但由于IB经纪商通常是执行交易的实体,当一家通过委托交易报告计划委托IB经纪商报告交易的投资公司提交委托单时,提交委托单的特定用户将被作为负责执行交易的个人进行报告。

委员会委托监管条款(欧盟)2017/590号第4条 - 委托单传递

1. 仅当以下条件被满足后,根据(欧盟)第600/2014号法规第26(4)条传递定单的投资公司(定单传递公司)才被视为传递了该委托单:

(a) 委托单来自其客户或源于其根据一位或多位客户向其提供的全权委托指令购入或处置特定金融产品的决定;

(b) 委托单传递公司已将第2段中提及的定单详情传递给了另一家投资公司(定单接收公司);

(c) 委托单接收公司受(欧盟)第600/2014号法规第26(1)条之约束,且同意报告该定单的交易或根据本条款将委托单详情传递给另一家投资公司。

就上述第一子段第(c)点而言,协议应明确委托单传递公司向委托单接收公司提供委托单详情的时间限制,并规定委托单接收公司应核实其收到的定单详情是否包含明显的错误或遗漏,然后方可提交交易报告或根据本条款传递委托单。

2. 就某个给定的委托单而言,应根据第1段传递以下委托单详情:

(a) 金融产品的识别码;

(b) 委托单的目的是收购还是处置金融产品;

(c) 委托单中列明的价格和数量;

(d) 委托单传递公司的客户就定单而言的标识和详细信息;

(e) 当投资决策是根据代理权做出时,应表明客户的决策者的标识和详情;

(f) 识别做空交易的标识;

(g) 识别在委托单传递公司内负责做投资决策的的个人或算法的指示;

(h) 投资公司内负责监督做投资决策的个人的分支所在的国家,及从客户处收到委托单或根据客户的全权委托指令代表客户做投资决策的分支所在的国家;

(i) 对于大宗商品衍生品委托单,表明该交易根据2014/65/EU号指引第57条是否旨在以客观可衡量的方式降低风险;

(j) 委托单传递公司的识别码。

就第一子段第(d)点而言,当客户为自然人时,应根据第6条标识客户。就第一子段第(j)点而言,当传递的委托单是接收自未按本条款的要求传递委托单的前一家公司,识别码应为识别委托单传递公司的代码。当传递的委托单是接收自按本条款的要求传递委托单的前一家传递公司,则第一子段第(j)点中的代码应为识别前一家传递公司的代码。

3. 当某个委托单涉及一家以上传递公司时,第2段第一子段(d)到(i)点中所指的委托单详情应针对第一家传递公司的客户。

4. 当委托单包含多个客户时,第2段所指的信息应针对单个客户传递。

更多信息请见:

无报告义务的账户持有人需提供的MiFIR信息

MiFIR交易报告体系要求诸如您的IB经纪商的投资公司在其交易报告中包括特定的客户识别信息。

交易由以下盈透证券集团实体(“IB经纪商”)接收和/或传递之金融产品的账户需使用特定的识别信息在IB经纪商的报告中标识自己的身份,IB经纪商目前可能已知此类识别信息,也可能未知。

- 盈透证券(英国)有限公司

- 盈透证券(中欧)有限公司

- 盈透证券(爱尔兰)有限公司

同样地,使用IB平台执行客户委托单并选择由IB经纪商处理交易报告的投资公司将需就其客户委托单使用类似的识别信息。如您为此类公司的客户,IB经纪商需向您请求额外的信息以完成交易报告。

需提供的信息

如果还需要其它信息,我们会要求客户在账户管理中填写电子表格来提供信息。

此类账户需提供的信息包括:

- 作为账户持有人或被授权交易者的自然人的国籍;

- 作为账户持有人或被授权交易者的自然人的特定国民身份信息;

- 法律实体需提供法律实体识别号码(LEI)。没有法律实体识别号码的客户可通过其IB经纪商申请。

- 机构账户需表明该法律实体是否为非金融实体且使用该账户进行大宗商品衍生品交易、根据MiFID II第57条以客观可衡量的方式降低风险。

注:常见MiFIR定义和条款列表,请见 KB2980

本信息仅用于指导使用盈透证券清算服务的客户。本信息不适用于仅使用执行服务的账户。

注意:以上信息不作为全面穷尽式指南,也不是对法规的权威性解释,而是对MiFIR交易报告义务的总结。

MIFIR交易报告概况

背景

2018年1月3日起,全新的2014/65/EC号指引(“MiFID II”)和(欧盟)600/2014 号法规(“MiFIR”)将生效,届时将为2007年通过金融工具市场指引(“MiFID I”)创建的交易报告(“MiFIR交易报告”)框架带来重大变革。

盈透证券推出了一套全新的交易报告体系,以帮助在新法规下有直接报告义务的客户遵守新的MiFIR要求。

MiFIR交易报告义务的范围

MiFIR交易报告适用于欧洲经济区(“EEA”)和英国的投资公司,也适用于使用盈透证券集团内的经纪商执行委托单的投资公司。如您是投资公司的客户且使用的是IB平台,则您将被要求提供额外的信息以便申报交易报告。

投资公司有义务在交易执行的次日收市前向相关国家主管机构(“NCA”)报告MiFIR覆盖的金融产品的交易之完整及准确细节。

MiFIR拓展了需报告的金融产品范围,覆盖了在EEA/英国监管的交易所、多边交易设施(“MTFs”)及有组织交易设施(“OTFs”)内交易的产品。除了在EEA/英国交易所执行的交易外,MiFIR还覆盖场外(“OTC”)交易及在非EEA/英国交易场所执行的EEA/英国上市金融产品交易,如在伦敦证交所(LSE)上市、但在纽交所(NYSE)交易的股票。(详见MiFIR覆盖的金融产品)。

面向EEA投资公司的MiFIR交易报告解决方案:增强版委托交易报告

确认自身为有MiFIR交易报告义务的投资公司的IB客户可选择将其报告义务委托给相关IB经纪商。

IB经纪商将根据“增强版报告”义务报告某些由此类投资公司执行的交易。对于此类交易,IB经纪商会在其自身的报告中增加有关投资公司的详细信息,以满足投资公司的报告义务。其它交易将仅以委托的形式代表投资公司报告,即在IB经纪商自身报告外以独立报告的形式呈现。客户只需与IB经纪商签署一份协议即可覆盖这两种报告形式。

需报告的信息

需报告的项目已从MiFID I体系下的23项增长至MIFIR下的65项。新增的信息要求包括:

- 每笔交易买卖双方的详细信息。具体地,法规要求法律实体提供法律实体标识(“LEI”)、自然人提供国民身份识别信息(基于国籍)。

- 当由第三方行使自由裁量权时,需明确买卖双方的决策者:

- 对于个人或联名账户,指账户持有人以外的个人或第三方实体。

- 对于机构账户,指账户授权交易者(如为客户子账户交易的财务顾问)以外的第三方。

当账户持有人为自己交易或被授权的交易者是为其自己的机构交易时,不要求提供本信息。

- 有报告义务的公司负责做投资决策或负责执行交易的个人或算法。使用我们的报告服务的EEA投资公司须提供该信息。

- 对于大宗商品衍生品交易,表明此类大宗商品衍生品交易根据MiFID II第57条是否能以客观可衡量的方式降低风险;当账户持有人为非金融实体时,本规则仅适用于机构账户。

新信息要求会以不同的方式影响盈透证券的客户,其影响取决于客户是EEA投资公司,还是投资公司以外的机构或个人,还取决于被交易的金融产品是由其IB经纪商还是其它盈透证券集团的关联公司接收和/或传递。

对无MiFIR交易报告义务的IB客户的影响

为履行IBUK自身的报告义务,IB经纪商须识别并报告每笔由其执行的直接客户。该报告必须包含法规规定的新的客户识别信息。

因此,每个IB经纪商都需从以下客户处收集识别信息并报告:

- 持有由IB经纪商接收和/或传递之金融产品的账户的IB经纪商直接客户;

- 使用盈透证券报告服务的EEA投资公司客户;

- 使用盈透证券平台及报告服务的EEA投资公司的子账户客户。

有关不直接受MiFIR管辖的账户持有人需要提供哪些信息,详情请见知识库文章 KB2976。

注:常见MiFIR定义和条款列表,请见 KB2980

本信息仅用于指导使用盈透证券清算服务的客户。本信息不适用于仅使用执行服务的账户。

注:以上信息不作为全面穷尽式指南,也不是对法规的权威性解释,而是对MiFIR交易报告义务的总结。

PRIIPs Regulation

The Packaged Retail and Insurance-based Investment Products Regulation - EU No 1286/2014 (“PRIIPs Regulation” or “PRIIPs”) became applicable on 1 January 2018.

A PRIIP is defined as any investment where the amount repayable to the investor is subject to fluctuations because of exposure to reference values. PRIIPs include ETFs, options, futures, CFDs, structured products, etc.

The Regulation requires product manufacturers to create Key Information Documents (KIDs) and persons advising or selling PRIIPs to provide retail investors based in the European Economic Area (EEA) with KIDs to enable those investors to better understand and compare products. The UK Financial Conduct Authority (FCA) has equivalent requirements for UK residents.

As a broker, IBKR is required to block trading in a PRIIP if a KID is not available.

The objectives of the PRIIPs Regulation.

Since the financial crisis of 2008, one of the main objectives of the European Commission has been to increase consumer protection and rebuild confidence in financial markets.

The Regulation specifies that the Key Information Document (KID) must be prepared in a standardised format.

By defining a standard format and content for the KID, the Regulation aims to:

- Ensure that the information provided is complete and comparable between similar products in order to help investors make informed investment decisions.

- Improve transparency and increase confidence in the retail investment market.

What is a KID?

The KID is a 3-page document that contains important details of the product including general description, cost, risk reward profile and possible performance scenarios.

Who is the regulation applicable to?

The Regulation applies to both PRIIPs manufacturers and distributors. The responsibility to create and maintain the document falls to the product manufacturer. However, any distributor or financial intermediary that sells or provides advice about PRIIPs to a retail investor, or receives a buy order for a PRIIP from a retail investor, must provide the investor with a KID. This also applies to execution-only, online environments.

Who should receive a KID?

Retail investors domiciled in the EEA and the UK should receive a KID prior to investing in a PRIIP. If no KID is available from the manufacturer, the PRIIP will be restricted from trading for EEA and UK retail clients.

Generally KIDs must be provided in an official language of the country in which a client is resident.

However, clients of IBKR have agreed to receive communications in English, and therefore if a KID is available in English all EEA and UK clients can trade the product regardless of their country of residence.

If a KID is not available in English, but one is available in another language, German for example, the PRIIP can only be traded by retail clients who are citizens of, or resident in countries where that language is an official language, in this example Germany, Austria, Belgium, Luxembourg or Liechtenstein.

Special Case – US ETFs

U.S. clients are not impacted by PRIIPs, so the issuers of U.S. listed ETFs do not as a rule create KIDs. This means that EEA and UK Retail clients may not purchase the product. Clients nevertheless have several options:

- Many US ETF issuers have equivalent ETFs issued by their European entities. European-issued ETFs have KIDs and are therefore freely tradable.

- Clients can trade most large US ETFs as CFDs. The CFDs are issued by IBKRs European entities and as such meet all KID requirements.

- Clients may be eligible for re-classification as a professional client, for whom KIDs are not required.

CLIENT CATEGORISATION

We categorize all individual clients as “Retail” by default as this affords clients the broadest level of protection afforded by MiFID. Client who are categorised as “Professional” do not receive the same level of protection as “Retail” but are not subject to the KIDs requirement. As defined under MiFID II rules, “Professional” clients include regulated entities, large clients and individuals who have asked to be re-categorised as “elective professional clients” and meet the MiFID II requirements based on their knowledge, experience and financial capability.

We provide an online step-by-step process that allows “Retail” to request that their categorisation be changed to “Professional". The qualifications for re-categorisation along with the steps for requesting that one’s categorisation be considered are outlined here or, to directly apply for a change in categorisation, the questionnaire is available in the Client Portal/Account Management.

Implications for Interactive Brokers:

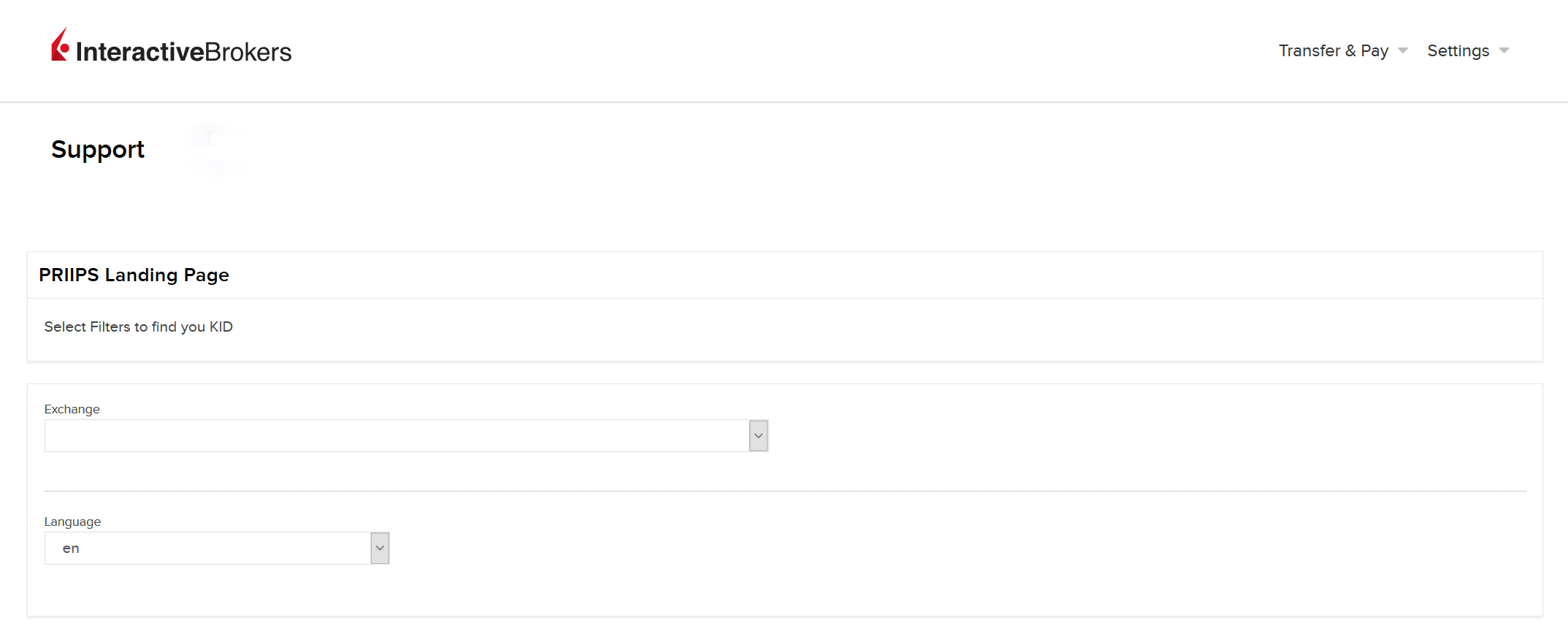

In order to meet the PRIIPs Regulation, where required, IB UK will provide KIDs electronically by means of a website (“PRIIPs KID Landing Page”).

Where can I find the PRIIPs KID Landing Page?

The KIDs can be accessed from our designated PRIIPs KID Landing Page. There are three different ways you can find the KIDs. They are available through the IBKR Trader Workstation (“TWS”), the IBKR website and Client Portal.

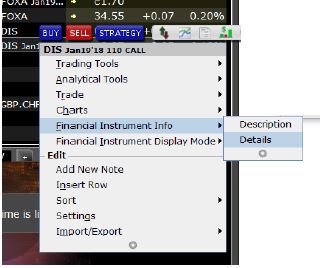

1. Find KIDs through TWS:

- Log into TWS

- Right click on the symbol of the product for which you want the KID.

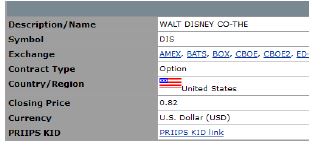

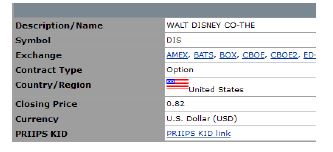

- Under Financial Instrument Info select Details.

- From the Contract Details page, you can select the PRIIPs KID link. This will take you to our PRIIPs KID Landing Page in Client Portal.

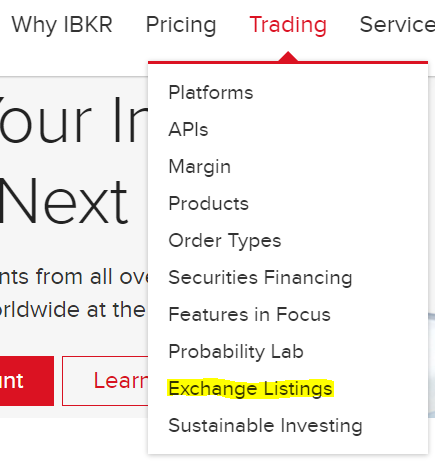

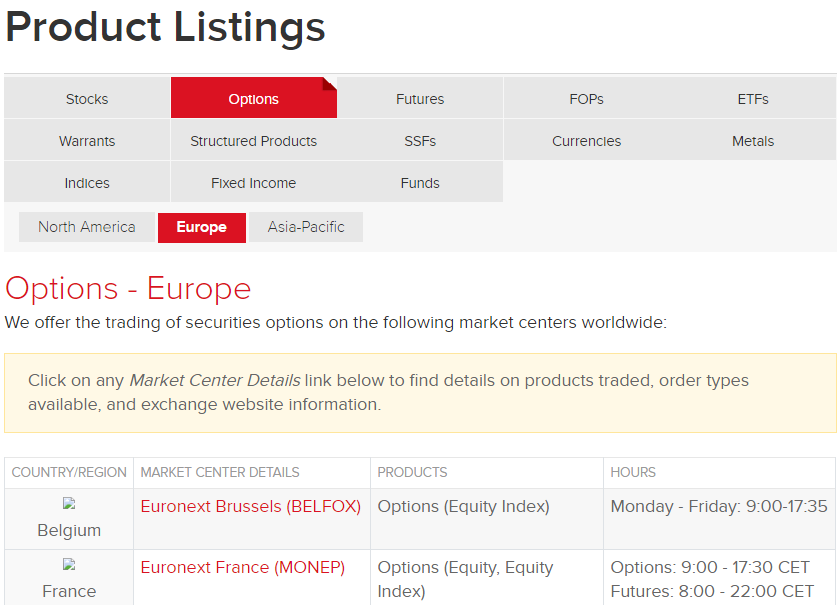

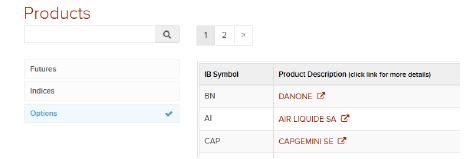

2. Find KIDs through the IBKR website:

- Open the Trading tab and select Exchange Listings.

- From there, select Product Listings. Select the derivative type, region and exchange of the product for which you would like to find the contract information.

- Select the product you would like to see the KID of, which will take you to the Contract Details page.

- From the Contract Details page, as above, you can select the PRIIPs KID link, which will take you to our PRIIPs KID Landing Page in Client Portal.

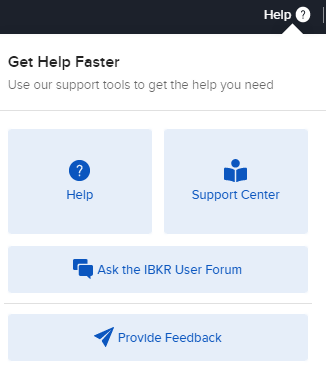

3. Find KIDs through Client Portal:

- Log into Client Portal.

- Click the Help (?) icon followed by Support Center.

- In the Information & Tools section, select PRIIPs Kid, which will take you to our PRIIPs KID Landing Page.

Can I potentially get exposure to a US ETF/other PRIIPs restricted product through a CFD?

An investor could potentially get exposure to a U.S. ETF or other PRIIPs restricted product when trading a CFD (Contract for Difference) as some CFDs are designed to track the performance of underlying assets, including ETFs and other PRIIPs products.

If an investor trades a CFD that is designed to track the performance of a U.S. ETF or other PRIIPs product, the investor may be indirectly investing in that underlying asset. This is because the CFD's value is based on the value of the underlying asset, and any gains or losses in the value of the underlying asset will be reflected in the value of the CFD.

MiFIR Definitions & Terms

European Economic Area (EEA) - As of October 2017, the EEA consists of the following countries: Austria, Belgium, Bulgaria, Croatia, Republic of Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Latvia, Liechtenstein, Lithuania, Luxembourg, Malta, Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden and the United Kingdom.

Investment Firms - Article 4 (1) (1) of MiFID II defines investment firm as any legal person whose regular occupation or business is the provision of one or more investment services to third parties and/or the performance of one or more investment activities on a professional basis. The investment services and activities covered by the framework are listed in Section A of Annex I of MiFID II.

Transactions Executed - For the purposes of MiFIR Transaction Reporting, a transaction is the conclusion of an acquisition or disposal of one of the financial instruments covered by MiFIR. A transaction is considered to be executed when it resulted from one of the following activities performed by an Investment Firm:

- Reception or transmission of orders in relation to one or more financial instruments (exceptions apply under Article 4 of Commission Delegated Regulation (EU) 2017/590);

- Execution of orders on behalf of clients;

- Dealing on own account;

- Making an investment decision in accordance with a discretionary mandate given by a client;

- Transfer of financial instruments to or from accounts.

[Ref: Articles 2 and 3 of Commission Delegated Regulation (EU) 2017/590]

IB Broker - Accounts that trade financial instruments which are received and/or transmitted by one of the following Interactive Brokers Group entities ("IB Brokers"):

- Interactive Brokers (U.K.) Limited

- Interactive Brokers Central Europe Zrt.

- Interactive Brokers Ireland Limited

Financial Instruments Covered by MiFIR - Article 26 (2) of Regulation (EU) No 600/2014 (MiFIR) lays out the transaction reporting obligation with regard to transactions in financial instruments listed below, irrespective of whether or not such transactions are carried out on the trading venue:

- Financial instruments which are admitted to trading or traded on a trading venue or for which a request for admission to trading has been made;

- Financial instruments where the underlying is a financial instrument traded on a trading venue; and

- Financial instruments where the underlying is an index or a basket composed of financial instruments traded on a trading venue.

The financial instruments covered by this requirement are legally enumerated in Section C of MiFID II:

(1) Transferable securities;

(2) Money-market instruments;

(3) Units in collective investment undertakings;

(4) Options, futures, swaps, forward rate agreements and any other derivative contracts relating to securities, currencies, interest rates or yields, emission allowances or other derivatives instruments, financial indices or financial measures which may be settled physically or in cash;

(5) Options, futures, swaps, forwards and any other derivative contracts relating to commodities that must be settled in cash or may be settled in cash at the option of one of the parties other than by reason of default or other termination event;

(6) Options, futures, swaps, and any other derivative contract relating to commodities that can be physically settled provided that they are traded on a regulated market, a MTF, or an OTF, except for wholesale energy products traded on an OTF that must be physically settled;

(7) Options, futures, swaps, forwards and any other derivative contracts relating to commodities, that can be physically settled not otherwise mentioned in point 6 of this Section and not being for commercial purposes, which have the characteristics of other derivative financial instruments;

(8) Derivative instruments for the transfer of credit risk;

(9) Financial contracts for differences;

(10) Options, futures, swaps, forward rate agreements and any other derivative contracts relating to climatic variables, freight rates or inflation rates or other official economic statistics that must be settled in cash or may be settled in cash at the option of one of the parties other than by reason of default or other termination event, as well as any other derivative contracts relating to assets, rights, obligations, indices and measures not otherwise mentioned in this Section, which have the characteristics of other derivative financial instruments, having regard to whether, inter alia, they are traded on a regulated market, OTF, or an MTF;

(11) Emission allowances consisting of any units recognised for compliance with the requirements of Directive 2003/87/EC (Emissions Trading Scheme).

National Identifiers - Under MiFIR, natural persons must be reported by using specific national identifiers required under a priority order that depends and varies on the Country of citizenship that is identified as relevant under MiFIR. The identifier can be a passport, a national ID card, a tax or personal code or a concatenation of full name and date of birth (“CONCAT”). The IB Broker will only request clients to provide national identifiers that are not already available.

Legal Entity Identifiers (“LEI”) = 20-character unique identifier based on the ISO 17442 for the global identification of legal entities that engage in financial transactions.

Commodity Derivatives Transactions that reduce risk in an objectively measurable way - When reporting transactions in commodity derivatives, the IB Broker will have to specify whether the transaction reduces risk in an objectively measurable way in accordance with Article 57 of Directive 2014/65/EU (“Art 57”). The IB Broker will allow such transactions only from accounts held by entities that are non-financial entities using the account for trades in commodity derivatives that are intended to objectively reduce risk directly relating to their commercial activity in accordance with Art 57. (e.g. company that produces wheat that trades in such derivatives to hedge its commercial activity).

Account holders that make such a declaration in the Trading Permission section of their Account Management, agree that all the transactions executed in commodity derivatives for that account will be executed for reducing the risk under Art 57, and the IB Broker will report the relevant transactions accordingly.

Individual or algorithm responsible at the reporting firm for making the investment decision - Under MiFIR, Investment Firms are required to include in their transaction reports the identification of the individual or algorithm that was primarily responsible for making the investment decision within the firm to acquire or dispose of a financial instrument. Only one individual or algorithm can be identified as responsible with regard to a transaction, and Investment Firms must identify such individual or algorithm as specified in Article 8 of commission delegated regulation (EU) 2017/590.

In accordance with these requirements, your IB Broker has implemented a new section in Account Management and new features in the IB Trader Workstation to allow Investment Firms that report their transactions through an IB Broker to identify individuals and algorithms in compliance with the new obligations.

Individual responsible at the reporting firm for the execution of a transaction - Art 9 of Commission Delegated Regulation (EU) 2017/590 requires Investment Firms to identify individuals or algorithms responsible for determining which trading venue to access […], which firms to transmit orders to or any other condition related to the execution of an order. While this requirement applies only to IB Brokers for the majority of the transactions reports (because the IB Broker is usually the entity that executes the transaction), when an order is submitted by an Investment Firm that transaction reports through an IB Broker via the Delegated Transaction Reporting, the specific user that has submitted the order will be reported as responsible for executing the transaction.

Article 4 of commission delegated regulation (EU) 2017/590 - Transmission of an order

1. An investment firm transmitting an order pursuant to Article 26(4) of Regulation (EU) No 600/2014 (transmitting firm) shall be deemed to have transmitted that order only if the following conditions are met:

(a) the order was received from its client or results from its decision to acquire or dispose of a specific financial instrument in accordance with a discretionary mandate provided to it by one or more clients;

(b) the transmitting firm has transmitted the order details referred to in paragraph 2 to another investment firm (receiving firm);

(c) the receiving firm is subject to Article 26(1) of Regulation (EU) No 600/2014 and agrees either to report the transaction resulting from the order concerned or to transmit the order details in accordance with this Article to another investment firm.

For the purposes of point (c) of the first subparagraph the agreement shall specify the time limit for the provision of the order details by the transmitting firm to the receiving firm and provide that the receiving firm shall verify whether the order details received contain obvious errors or omissions before submitting a transaction report or transmitting the order in accordance with this Article.

2. The following order details shall be transmitted in accordance with paragraph 1, insofar as pertinent to a given order:

(a) the identification code of the financial instrument;

(b) whether the order is for the acquisition or disposal of the financial instrument;

(c) the price and quantity indicated in the order;

(d) the designation and details of the client of the transmitting firm for the purposes of the order;

(e) the designation and details of the decision maker for the client where the investment decision is made under a power of representation;

(f) a designation to identify a short sale;

(g) a designation to identify a person or algorithm responsible for the investment decision within the transmitting firm;

(h) country of the branch of the investment firm supervising the person responsible for the investment decision and country of the investment firm's branch that received the order from the client or made an investment decision for a client in accordance with a discretionary mandate given to it by the client;

(i) for an order in commodity derivatives, an indication whether the transaction is to reduce risk in an objectively measurable way in accordance with Article 57 of Directive 2014/65/EU;

(j) the code identifying the transmitting firm.

For the purposes of point (d) of the first subparagraph, where the client is a natural person, the client shall be designated in accordance with Article 6. For the purposes of point (j) of the first subparagraph, where the order transmitted was received from a prior firm that did not transmit the order in accordance with the conditions set out in this Article, the code shall be the code identifying the transmitting firm. Where the order transmitted was received from a prior transmitting firm in accordance with the conditions set out in this Article, the code provided pursuant to point (j) referred to in the first subparagraph shall be the code identifying the prior transmitting firm.

3. Where there is more than one transmitting firm in relation to a given order, the order details referred to in points (d) to (i) of the first subparagraph of paragraph 2 shall be transmitted in respect of the client of the first transmitting firm.

4. Where the order is aggregated for several clients, information referred to in paragraph 2 shall be transmitted for each client.

Also see:

Overview of MIFIR Transaction Reporting

MiFIR Enriched and Delegated Transaction Reporting for EEA Investment Firms

MiFIR Information Required from Account Holders that do not have Reporting Obligations

MiFIR Information Required from Account Holders that do not have Reporting Obligations

The MiFIR Transaction Reporting regime requires Investment Firms, like your IB Broker, to include specific client identifiers in their transaction reports.

Accounts that trade in financial instruments which are received and/or transmitted by one of the following Interactive Brokers Group entities (“IB Brokers”) will need to be identified in the IB Broker’s reports by using specific identifiers that may or may not be already available to it.

- Interactive Brokers (U.K.) Limited

- Interactive Brokers Central Europe Zrt.

- Interactive Brokers Ireland Limited

Similarly, Investment Firms that use the IB platform for their clients’ orders and have elected to transaction report through their IB Broker will have to use the same identifiers for their client orders. If you are the client of such a firm, your IB Broker may need additional information from you to complete the transaction reports.

Information Required

When additional information is necessary for this purpose, clients will be asked to provide it via the completion of an electronic form available in the Account Management.

The information requested for these accounts is:

- All countries of citizenship for natural persons that are account holders and authorised traders;

- A specific National Identifier for natural persons that are account holders and authorised traders;

- The Legal Entity Identifier for legal entities. Clients that do not have an LEI will be able to apply for one through their IB Broker.

- For organisation accounts, an indication as to whether the Legal Entity is a non-financial entity using the account for trades in Commodity Derivatives Transactions to reduce risk in an objectively measurable way in accordance with Article 57 of MiFID II.

Note: For a listing of common MiFIR definitions and terms, see KB2980

THIS INFORMATION IS GUIDANCE FOR INTERACTIVE BROKERS CLEARED CLIENTS ONLY. THIS GUIDANCE DOES NOT APPLY TO EXECUTION ONLY ACCOUNTS.

NOTE: THE INFORMATION ABOVE IS NOT INTENDED TO BE A COMPREHENSIVE OR EXHAUSTIVE GUIDANCE AND IT IS NOT A DEFINITIVE INTERPRETATION OF THE REGULATION, BUT A SUMMARY OF MiFIR TRANSACTION REPORTING OBLIGATIONS.

MiFIR Enriched and Delegated Transaction Reporting for Investment Firms

Who is Subject to the MiFIR Transaction Reporting Requirements?

All EEA and UK investment firms (collectively, "Investment Firms") are subject to the reporting requirements and will have to report all transactions executed in financial instruments covered by MiFIR within one working day from their execution.

The below entities (“IB Brokers”), will offer assistance to IB clients that are Investment Firms in complying with the new requirements:

- Interactive Brokers (U.K.) Limited

- Interactive Brokers Central Europe Zrt.

- Interactive Brokers Ireland Limited

- Interactive Brokers Luxembourg SARL

With the exception of Omnibus Introducing Brokers, where applicable, that utilise the IB platform (in which all their underlying client positions are held in one or more omnibus accounts), all IB clients that are EEA Investment Firms will be able to elect to have their IB Broker report on their behalf. The IB Broker will report for IB clients based on two distinct reporting mechanisms implemented in accordance with the Regulation: Enriched Transaction Reporting and Delegated Transaction Reporting.

ENRICHED TRANSACTION REPORTING

In compliance with Article 4 of Commission Delegated Regulation (EU) 2017/590, if an IB Broker includes details of orders submitted by clients that are Investment Firms (“the transmitting firm”) in its own transaction reports, the transmitting firm is exempt from reporting these transactions.

Enriched Transaction Reporting will only apply to transactions in financial instruments carried by an IB Broker submitted for execution by an Investment Firm for the benefit of the Investment Firm’s clients (for example, a Financial Advisor, Fund Manager or Introducing Broker Account submitting orders for its clients' subaccounts).

DELEGATED TRANSACTION REPORTING

Delegated Transaction Reporting services are provided by an IB Broker to Investment Firms for all other transactions submitted by the Investment Firm.

This includes transactions entered by the Investment Firm for its own proprietary account, transactions submitted on the basis of discretionary mandates given by their clients and transactions in Financial Instruments for which an IB Broker is not the carrying broker (i.e., any transaction in a financial instrument where another IB affiliate is the carrying broker). Delegated transaction reporting does not apply where the trades are submitted directly by clients of the Investment Firm.

These reports will be submitted to the National Competent Authority (“NCA”) of the Country of legal residence recorded in the Legal Entity Identifier of the account for which the Delegated Transaction Reporting was enabled (e.g., if the Investment Firm’s legal residence is Netherlands, transactions will be reported to the Authority for the Financial Markets (AFM)).

Clients will only need to sign one agreement with an IB Broker to cover both Enriched and Delegated Transaction Reporting.

How to Sign Up for the Enriched and Delegated Transaction Reporting Service

Investment Firms (other than Omnibus Introducing Brokers) will be prompted to complete an electronic form in the Account Management system during which it will be possible to accept to use IB’s Enriched and Delegated Transaction Reporting Service.

Investment Firms that are Omnibus Introducing Brokers on the IB platform will not have the ability to activate the Enriched and Delegated Transaction Reporting.

Investment Firms that utilise IB’s Enriched and Delegated Transaction Reporting Service will need to sign the relevant legal agreement and provide the following information:

- Legal Entity Identifier (“LEI”). Clients that do not have an LEI, will be able to apply for one through an IB Broker;

- The citizenship(s) for each authorised trader and further information as required by the national client identifier requirements for the relevant country;

- Individuals or Algorithms that can be responsible for making the investment decision within the investment firm:

- Individual active traders who have been previously selected as possible investment decision makers within the firm. Only individuals that are authorised as traders on the account will be allowed;

- Algorithm identifiers provided for algorithms that the firm may use for making investment decisions. It is the client’s responsibility to determine and provide algorithm identifiers in compliance with the regulation.

How the New Requirements Will Affect the Account Management and the IB Order Entry System

Some of the information required for the submission of a transaction report may change on an order by order basis, and may require input of the person submitting the trade. Hence, IB has amended IB Account Management and the IB Order Entry System to allow traders to provide the necessary information.

Accounts that want to use IB’s Enriched and Delegated Transaction Reporting Service shall select the authorised traders and list the Algorithm IDs that may be responsible for making an investment decision.

The traders and algorithms listed in Account Management will be displayed in a new dropdown field of the IB Trader Workstation at the time of the order submission. This field will show the default value selected in Account Management of the account. The client will be able to change this by selecting another value present in the dropdown list.

The IB Trader Workstation will allow an authorised trader on the account for which the Enriched and Delegated Transaction Reporting was activated to select one person or algorithm as responsible for the investment decision within the firm with regard to the specific order submitted.

Note: For a listing of common MiFIR definitions and terms, see KB2980

THIS INFORMATION IS GUIDANCE FOR INTERACTIVE BROKERS CLEARED CLIENTS THAT ARE INVESTMENT FIRMS ONLY. THIS GUIDANCE DOES NOT APPLY TO EXECUTION ONLY ACCOUNTS.

NOTE: THE INFORMATION ABOVE IS NOT INTENDED TO BE A COMPREHENSIVE OR EXHAUSTIVE GUIDANCE AND IT IS NOT A DEFINITIVE INTERPRETATION OF THE REGULATION, BUT A SUMMARY OF MiFIR TRANSACTION REPORTING OBLIGATIONS.