現金劃轉

背景

IB全能賬戶由兩個獨立的子賬戶或賬戶段組成,一個用于持有證券倉位和餘額,受美國證券交易委員會(SEC)客戶保護規則約束,另一個用于持有商品倉位和餘額,受美國商品期貨交易委員會(CFTC)客戶保護規則約束。這種全能賬戶的設計旨在盡可能地降低客戶維護兩個不同賬戶(例如,賬戶之間轉帳現金、兩個賬戶登錄和提交委托單、多份報表等)可能面臨的行政管理開銷,同時又維持法規要求的分隔措施。

該等法規還要求所有證券交易和相關保證金交易均在全能賬戶的證券賬戶段進行,而商品交易則在商品賬戶段進行。1 雖然法規允許將全額支付的證券持倉以保證金抵押品的形成存放在商品賬戶段進行托管,但IB幷不允許這種操作,從而對抵押權應用了更爲嚴格的SEC限制性規則。鑒于相關法規和政策已對持倉應歸于哪個賬戶段作出了規定,現金是唯一可由客戶自行决定在兩個賬戶段之間來回轉帳的資産。

下方爲現金劃轉選項、選擇步驟和注意事項相關的說明。

現金劃轉選項

客戶有三種劃轉選項,說明如下:

1. 不劃轉剩餘資金 – 根據這個選項,如非必要,剩餘現金不會在兩者之間進行轉移:

a. 解决/緩解另一賬戶段保證金不足的問題;

b. 盡可能地降低指定賬戶段的借方現金餘額,從而减少相關的利息費用。 請注意,對于只擁有證券或商品交易許可中一項許可的賬戶持有人來說,這是默認選項,也是唯一的選項。

2. 將剩餘資金劃轉至我的IB證券賬戶 – 只在商品賬戶段中留下能滿足當前商品保證金要求的現金餘額。 任何由于現金增加(例如,有利的變化和/或與交易相關)或保證金要求降低(例如,SPAN風險陣列和/或與交易相關的變化)而産生的超出保證金要求的現金,都將自動從商品賬戶段轉移到證券賬戶段。請注意,賬戶持有人必須具備證券交易許可才能選擇此選項。

3. 將剩餘資金劃轉至我的IB商品賬戶 – 只在證券賬戶段中留下能滿足當前證券保證金要求的現金餘額(加上含有貸款價值的其它證券倉位)。請注意,賬戶持有人必須具備商品交易許可才能選擇此選項。

其它注意事項:

- 由于全能賬戶允許以不同幣種持有現金餘額,因此存在一個層次結構,以决定當多種貨幣出現多頭餘額時,首先轉移哪種貨幣。在這類情况下,首先會轉移以基礎貨幣計價的餘額,然後是美元,然後剩下的多頭餘額再按金額從高到低的順序轉移。

- 爲了盡可能地降低一個賬戶段在把剩餘現金劃轉至另一個賬戶段後出現保證金不足的可能性,剩餘資金不會全部轉移,而是會留下相當于維持保證金要求5%的資金作爲緩衝。 同樣,爲了盡可能地降低轉移名義餘額的運營開銷,只有在扣除5%的保證金緩衝後,剩餘金額(如有)仍不低于賬戶淨資産的1%或200美元時,才會轉移餘額。

- 在執行交易前信用核查以確定賬戶是否擁有足够的淨資産來支持新的委托單時,一個賬戶段內進行的交易也會將另一個賬戶段內的剩餘現金納入考慮(但在交易執行之前不會進行劃轉,幷且也只有在爲了滿足保證金要求而有必要時才會進行劃轉)。 被標記爲典型日內交易者以及需要進行交易前信用核查(會考慮前一日和當日淨資産)的賬戶應特別留意下方選擇注意事項。

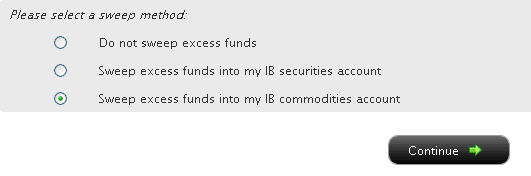

選擇劃轉的選項

如果您的賬戶管理版本在左側有一系列菜單選項,請選擇賬戶行政,然後選擇 剩餘資金劃轉菜單選項。 如果您的版本是頂部有菜單選項,請選擇管理賬戶/設置,然後選擇 配置賬戶/剩餘資金劃轉菜單選項。無論您的版本如何,您都將看到以下界面:

然後,您可點擊您想要的劃轉方式對應的單選按鈕,然後選擇〝繼續〞按鈕。您的選擇將從下一個工作日起生效,幷將一直有效,直到選擇其它選項爲止。請注意,只要滿足上文中提到的交易許可設置,您可隨時更改劃轉方式,沒有次數限制。

選擇注意事項

雖然選擇將剩餘現金存放在哪個賬戶段可能涉及每位客戶獨特的主觀决策和偏好(例如,客戶將大部份資産集中存放在其中一個賬戶段),但下述有幾個因素值得注意:

1. 典型日內交易淨資産 - 根據相關法規被標記爲典型日內交易者的賬戶(即在5個工作日內進行4次或以上日內交易),其證券購買力將被限制爲證券賬戶段當日或前一日收盤淨資産中的較低者。根據這個計算方式,如選擇將剩餘資金劃轉至商品賬戶段,則該筆資金將無法納入計算,從而可能對下達新委托單的造成一定限制。要最大程度地利用淨資産來擴大購買力下達證券委托單,客戶需選擇將剩餘資金劃轉至證券賬戶段。 請注意,選擇證券賬戶段幷不會限制下達商品委托單的能力,因爲典型日內交易規則不適用于此類賬戶。

2. 保險 – 美國證券投資者保護公司(SIPC)的保障範圍覆蓋證券賬戶段的資産,而商品賬戶段則沒有相應的保障計劃。不過,超過SIPC的$250,000現金分項給付限額(勞合社現金分項給付限額爲$900,000,如適用)的餘額不在承保範圍內。 IB加拿大和IB英國的客戶也分別受加拿大投資者保護基金(CIPF)和英國金融服務補償計劃(FSCS)規定的承保規則約束。

3.利息收入 – 在所有其它條件相同的情况下,從未將多頭現金餘額在證券和商品賬戶段中分開存放的客戶,可望獲得最高的利息收入,這是因爲兩者不會匯總以計算貸方利息(它們受不同的隔離池和再投資規則的約束)。 在選擇現金劃轉時,除了上述的因素外,也應該要考慮到貸款需要維持最低現金餘額,幷且餘額高一些,利率也會優惠一些。2

脚注:

1由于OneChicago個股期貨是由SEC和CFTC共同監管的混合産品,因此可在任何一種賬戶類型中進行買賣。不過,IB選擇在全能賬戶的證券賬戶段進行此類交易,因爲只有在這情况下,才能向單一股票期貨和任何合資格股票或期權持倉提供保證金减免。

2例如,某賬戶在證券和商品賬戶段各持有$9,000的多頭美元餘額。根據基準聯邦基金有效利率,如果兩個餘額存放在同一賬戶段,該賬戶有$8,000 ($18,000 - $10,000)可以獲得利息。但由于分別放在兩個賬戶段中的現金餘額均低于$10,000,都無法獲得利息,如不選擇現金劃轉,將無法賺取任何利息。同樣,如進行現金劃轉後,某賬戶段的多頭美元現金餘額超過$100,000,則賬戶持有人將能够賺取更高一檔的利息。有關利息計算的其它信息,包括當前基準利率的鏈接,請參閱KB39。

“信用限制期”內的存款是否可以獲得利息?

Overview:

答案取决于存款方式。 對于通過ACH進行的存款,利息從存款到達當日起便開始計算,資金記入賬戶前爲期四個工作日的信用限制期都會持續計息。對于銀行支票以外的支票存款,在信用限制期內不産生利息。銀行支票和電匯會在收到後立即記入賬戶,因此不受任何信用限制期的影響。

您收到的利息因市况而异。 有關當前向貸方餘額支付利息的信息,請參閱 www.interactivebrokers.com/interest

活動報表上的應計利息轉回項目代表什麼?

Overview:

IBKR每日都會在活動報表的應計利息部分,對報表期間預期或應計賺取或將支付的利息進行計算和報告。大約在每個月的第一周,上個月的應計利息會被〝返還〞或轉回,而當月的實際利息會在現金報告板塊發佈。應計利息的轉回操作每月進行一次,調整後應接近實際利息,但它們可能並不總是完全相同,因為應計額是對實際利息的預測。

賬戶持有人還應注意,報告期內的應計利息需超過1美元(正數或負數)才會顯示出來。低於1 美元的餘額會作保存,當加上未來應計利息後金額超過 1美元時將予顯示。

賣空股票收入的貸方利息

Overview:

如何確定與股票借入倉位相關的貸方利息或費用

Background:

賬戶持有人賣空股票時,IBKR會代賬戶持有人借入相應數量的股票,以履行向買方交付股票的義務。根據借入股票的股票借貸協議,IBKR需向股票出借方提供現金抵押品。現金抵押品的金額基于股票價值的行業標準計算,稱爲抵押品標記。

股票出借方就現金抵押品向IBKR提供利息,利率通常會低于現金抵押存款的現行市場利率(通常與美元計價現金存款的聯邦基金有效利率挂鈎),其中的差額即作爲出借方提供此服務收取的費用。對于難以借入的股票,出借方所收取的費用會相應提高,可能會導致淨利率變爲負,IBKR反而被倒扣費用。

許多經紀商只會向機構客戶提供部分利息返還,但所有IBKR客戶其賣空股票收入超出10萬美元或等值其它貨幣的部分都可以獲得利息。當某證券可供借用的供應量高于借用需求時,賬戶持有人可就其賣空股票餘額獲得的利息利率相當于基準利率(例如,美元餘額采用聯邦基金有效隔夜利率)减去一個利差(目前介于1.25%(10萬美元檔的餘額)至0.25%(300萬美元以上的餘額)之間)。利率可能會在無事先通知的情况下發生變化。

當某特定證券的供求不平衡導致其難以借入時,借出方提供的利息返還將會减少,甚至可能導致向賬戶倒扣費用。該等利息返還或倒扣費用會以更高的借券費用的形式轉嫁給賬戶持有人,這可能會超過賣空收入所得的利息,導致賬戶最終算下來還付出了費用。由于利率因證券和日期而异,IBKR建議客戶通過客戶端/賬戶管理中的支持部分,訪問〝可供賣空股票〞工具,查看賣空的指示性利率。請注意,該等工具中反映的指示性利率對應的是IBKR向第三等級餘額支付的賣空收入利息,即賣空收入爲300萬美元或以上。對于較低的餘額,其利率將根據餘額等級和交易貨幣對應的基準利率進行調整。可使用“對賣空收益現金餘額向您支付的利息”計算器計算適用的利率。

請參閱證券融資(融券)頁面的更多範例和計算機。

重要提示

“可供賣空股票”工具和TWS中關于可供借用股票和指示性利率的信息,是在盡最大努力的基礎上提供,不保證其準確性或有效性。 “可供賣空股票”包括來自第三方的信息,不會實時更新。利率信息僅爲指示性質。在當前交易時段執行的交易通常在2個工作日內結算,實際供應和借入成本在結算日確定。交易者應注意,在交易和結算日之間,利率和供應可能會發生重大變化,尤其是交易稀少的股票、小盤股和即將發生公司行動(包括股息)的股票。詳情請參閱賣空的操作風險(Operational Risks of Short Selling) 。

有關向淨現金餘額為正的賬戶收取利息的說明

在以下情况下,儘管賬戶保持整體淨多頭或貸方現金餘額,但仍需支付利息:

1. 該賬戶持有特定幣種的空頭或借方餘額。

例如,某賬戶有相當于5,000美元的淨現金貸方餘額,這其中包括8,000美元的多頭餘額和相當于3,000美元的歐元空頭餘額,需要對歐元空頭餘額支付利息。 由于賬戶所持有的多頭美元餘額低于10,000美元的第一階梯水平,不會獲得利息,因此無法沖抵要支付的利息。

賬戶持有人應注意,如其買入的證券是以賬戶未持有的貨幣計價,則IBKR會創建相應幣種的貸款,以便與清算所結算交易。如希望避免此類貸款和相關利息費用,客戶需在進行交易前存入以該特定貨幣計價的資金,或通過Ideal Pro(餘額25,000美元或以上)或散股(餘額低于25,000美元)交易場所兌換現有的現金餘額。

2. 貸方餘額主要來自于賣空證券所得。

例如,某賬戶的淨現金餘額爲12,000美元,其中包括證券子賬戶中的6,000美元借方餘額(减去空頭股票持倉的市場價值)和18,000美元的股票空倉價值。賬戶需就第一階梯借記餘額6,000美元支付利息,同時,由于空頭股票貸記低于100,000美元的第一階梯水平,不會從空頭股票貸記中獲得利息。

3. 貸方餘額包含未結算的資金。

IBKR僅根據已結算資金决定要收取和支付利息。正如賬戶持有人在買入交易結算之前,無需對用來買入證券的借款支付利息一樣,在賣出交易結算之前(而清算所已向IBKR存入資金),賬戶持有人也不會就賣出證券所得資金獲得利息或借方餘額沖抵。

FAQs – Irish Income Withholding Tax

Overview:

As an Irish company, Interactive Brokers Ireland Limited (IBIE) is generally required to collect withholding tax (WHT) at a rate of 20% on interest paid to certain clients.

This requirement is set out in section 246 of the Irish Taxes Consolidation Act 1997 and generally applies to interest paid to clients that are:

(i) natural persons resident in Ireland,

(ii) natural persons resident outside Ireland unless the client has successfully applied for an exemption or a reduction in the WHT rate under a Double Tax Treaty (DTT) between Ireland and the person’s country of residence.

(iii) Irish companies

(iv) Companies established in countries with which Ireland has NOT concluded a DTT.

Background:

The purpose of this document is to set out our responses to some frequently asked questions (FAQs) on the WHT.

This document is for information purposes only and does not constitute tax, regulatory or any other kind of advice. If you are unsure of your tax obligations please consult the Irish Revenue Commissioners, your local tax authority or an appropriate tax professional.

FAQs

What type of interest does Irish WHT apply to?

Does Irish WHT apply to interest I earn through the Stock Yield Enhancement Program?

If I earn interest through Bond Coupons, am I required to pay Irish WHT?

I do not trade Irish stocks, do I still have to pay Irish WHT?

What is the standard Irish WHT Rate?

When is the 20% WHT applied to my account?

What currency is used for Irish WHT?

I am resident in Ireland. Do I have to pay Irish WHT?

I am not resident in Ireland. Does Irish WHT apply to me?

Does WHT apply to clients who are companies?

How do I apply for an exemption from WHT or a reduced WHT rate?

What do joint account holders need to submit to obtain a WHT exemption/reduction?

Where should I send my completed Form 8-3-6?

How do I submit Form 8-3-6 and supporting documentation to IBIE?

Do I need to apply for an exemption from WHT or a reduction in the WHT rate by a certain deadline?

How do I apply to reclaim WHT applied to my account?

How long does a completed Form 8-3-6 remain valid for?

Do I have to complete a Form 8-3-6? Can I still trade if I don’t complete it?

Where can I see information relating to Irish WHT on my account statement?

How do I know what WHT rate has been agreed between my country of residence and Ireland?

WHT is a set amount of income tax that is withheld at the time income is paid to a person.

Under Irish law, interest payments are considered income. This means that IBIE is legally required to deduct WHT from credit interests on uninvested cash balances in our clients’ securities accounts.

What type of interest does Irish WHT apply to?

Irish WHT applies to credit interest paid to long settled uninvested cash balances as well as short credit interest where you have borrowed stock from IBIE.

Does Irish WHT apply to interest I earn through the Stock Yield Enhancement Program?

No. The interest you earn under the Stock Yield Enhancement Program is not within scope for Irish WHT obligations. Irish WHT only applies to credit interest paid on uninvested cash balances in your account.

If I earn interest through Bond Coupons, am I required to pay Irish WHT?

No. Interest that you earn on Bond Coupons is not within scope for Irish WHT obligations. Irish WHT applies only to credit interest paid on uninvested cash balances in your account.

I do not trade Irish stocks, do I still have to pay Irish WHT?

Yes. If your account is held by IBIE, your account is in scope for Irish WHT on credit interest payments. It is irrelevant whether or not you trade in Irish stocks.

What is the standard Irish WHT Rate?

The standard rate of WHT is 20%. You can find further information on credit interest rates on our webpage.

When is the 20% WHT applied to my account?

If IBIE is required to apply WHT to your interest payments, we will do so at the same time any credit interest is paid to your account.

IBIE pays interest due on the uninvested cash balance in your account on the third business day of the month following the month in which the interest accrued. For example, interest accrued in January will be paid on the third business day in February.

What currency is used for Irish WHT?

Irish WHT is charged in the same currency as the credit interest paid on the uninvested cash balances in your account.

I am resident in Ireland. Do I have to pay Irish WHT?

Yes. Under Irish tax law, all Irish resident individuals and partnerships are subject to 20% WHT on credit interest payments. Irish companies are also subject to WHT, although some limited exemptions may apply.

I am not resident in Ireland. Does Irish WHT apply to me?

Yes, generally Irish WHT applies to natural persons whether or not they reside in Ireland.

However, if Ireland has entered a Double Taxation Treaty (DTT) with your country of residence, that DTA may allow you to apply for an exemption from or reduction in WHT, depending on its terms. Please see further below.

You can find information about Ireland’s DTTs on the Irish Revenue website https://www.revenue.ie/en/tax-professionals/tax-agreements/rates/index.aspx

Does WHT apply to clients who are companies?

WHT does not apply to companies resident in countries that have a DTT with Ireland.

In general, WHT applies to Irish resident companies with a few exceptions, including;

(a) an investment undertaking within the meaning of section 739B of the Taxes Consolidation Act 1997,

(b) interest paid in the State to a qualifying company (within the meaning of section 110).

For a full list of exemptions, please refer to Section 246(3) of the Taxes Consolidation Act.

There is no standard exemption form for corporate clients. In order to avail of these exemptions, clients will have to provide proof of their corporate status requested by IBIE.

How do I apply for an exemption from WHT or a reduced WHT rate?

If you wish to apply for a WHT exemption or reduction under the terms of a DTT, you should complete Form 8-3-6, and return that Form to IBIE.

The following is a summary of the information you must provide when completing Form 8-3-6:

1. Your name (please ensure this matches the name on your IBKR account)

2. Your address

3. Your tax reference number in country of residence

4. The country in which you are tax resident

5. The WHT rate agreed between your country of tax residence and Ireland (see FAQ on this topic).

6. Signature.

7. Date.

You must request your local Tax Authority to sign and stamp Form 8-3-6 before returning it to us.

For more detailed information on how to complete Form 8-3-6, please refer to the Irish Revenue Commissioners’ website here https://www.revenue.ie/en/companies-and-charities/financial-services/withholding-tax-interest-payments/index.aspx

If you have asked your local tax authority to sign Form 8-3-6 and they have refused, you can instead submit a Tax Residency Certificate (TRC) from your local Tax Authority, with a completed Form 8-3-6 that has not been signed and stamped by your local tax authority. Revenue introduced this possibility in January 2023, after being informed by IBIE of the difficulties clients were experiencing in completing the Form.

To be acceptable, the TRC must explicitly state that you are tax resident in your country of residence in accordance with the relevant provision of the double taxation treaty between Ireland and your country of residence.

Please note that a TRC will only be accepted where you have first requested your local tax authority to sign and stamp Form 8-3-6 and it has refused to do so or has failed to do so within a reasonable time.

Form 8-3-6 and information about completing the Form 8-3-6 is available on the website of the Irish Revenue Commissioners.

To assist you, IBIE has also prepared a number of versions of Form 8-3-6 with certain information pre-filled, depending on your jurisdiction of tax residency. You can select the most appropriate form from the list below.

Form 8-3-6 has been translated into French, German, Spanish, Italian and Dutch*

1. EEA countries with 0% Withholding Tax.

2. EEA countries with rates above 0% Withholding Tax.

|

|

3. Other countries with a DTA with Ireland (* denotes where there is 0% withholding tax in all situations).

|

Georgia |

Moldova |

Singapore |

|

|

Armenia |

Ghana |

Montenegro |

South Africa* |

|

Australia |

Hong Kong |

Morocco |

South Korea* |

|

Bahrain* |

India |

New Zealand |

Switzerland* |

|

Belarus |

Israel |

North Macedonia* |

Thailand |

|

Bosnia & Herzegovina* |

Japan |

Norway |

Turkey |

|

Botswana |

Kazakhstan |

Pakistan |

Ukraine |

|

Canada |

Kenya |

Panama |

United Arab Emirates* |

|

Chile |

Kosovo |

Qatar* |

United Kingdom* |

|

China |

Kuwait* |

Russian Federation* |

United States of America* |

|

Egypt |

Malaysia |

Saudi Arabia* |

Uzbekistan |

|

Ethiopia |

Mexico |

Serbia |

Vietnam |

|

|

|

|

Zambia* |

What do joint account holders need to submit to obtain a WHT exemption/reduction?

Each account holder in a joint account needs to complete their own documentation. This means that a separate Form 8-3-6 must be completed by each account holder and (if relevant) a separate TRC must be provided by each account holder.

Where should I send my completed Form 8-3-6?

You should send your completed Form to IBIE. You should NOT send the Form to Irish Revenue.

How do I submit Form 8-3-6 and supporting documentation to IBIE?

You should email a PDF or JPEG copy of the signed form to tax-withholding@interactivebrokers.com. If you have not been able to obtain a stamp from your local tax authority, please ensure that you also email your Tax Residency Certificate (TRC) to this same email address.

Alternatively, you can upload your signed Form 8-3-6 to your Client Portal through the ‘Document Submission Task’ tab. However, if you are submitting a TRC with your Form you will still need to send this separately to the above email address.

Please put your IBIE account number in the email subject line in all email correspondence. A failure to do so may delay or prevent the processing of your application,

If your submitted documentation is in order, IBIE will send you a confirmation email stating that your Form has been received and processed.

If your submitted documentation is not in order, we will send you an email setting out the additional information or documentation we require to process your application.

Please follow up with IBIE if you have not heard from us within four weeks.

Do I need to apply for an exemption from WHT or a reduction in the WHT rate by a certain deadline?

There is no deadline. However, for applications made in 2023, a WHT exemption or rate reduction will only apply to interest payments made after IBIE has received a complete application.

If we have not processed your Form 8-3-6 by the time the next interest payment is made to your account we will refund any WHT deducted after the date we received your application. Refunds will be visible in the Withholding Tax section of a statement.

Yes, if you are not subject to WHT, or are subject to a reduced WHT rate by virtue of a Double Taxation Treaty between Ireland and your country of residence, you will be entitled to reclaim WHT paid in excess of the WHT rate set out in the DTT.

How do I apply to reclaim WHT applied to my account?

Generally, the application process (i) to apply for an exemption from WHT or a reduction in the WHT rate going forward and (ii) to reclaim WHT already charged, are two separate processes. IBIE is awaiting full details from the Irish Revenue Authority on how clients can make reclaims on WHT and will make these details available once provided.

However, for 2022, Revenue has agreed to allow a completed Form 8-3-6 (signed and stamped by the relevant Tax Authority) received by IBIE before 31 December 2022, to be used to reclaim WHT applied in 2022. This means that if IBIE received a completed form from you on or before 31 December 2022 and WHT was applied to your account from January – December 2022, IBIE will refund all or part of that WHT, depending on Ireland’s arrangements with your tax jurisdiction.

If you did not provide a Form 8-3-6 before 31 December 2022 or, if you provided a Form 8-3-6 but it was incomplete (for example by not being stamped by your local tax authority), you must separately apply for a full or partial reclaim of WHT paid in 2022 and 2023. Further details on the reclaim process may be found in an article titled Irish Tax Withholding Reclaim Process. For your convenience, the full article may be viewed here.

How long does a completed Form 8-3-6 remain valid for?

A fully completed Form 8-3-6 remains valid for 5 years unless there is a material change in your facts and circumstances. This also applies if you have provided IBIE with a TRC in lieu of having your Form 8-3-6 stamped by your local tax authority. If there is a material change to your circumstances from a tax perspective, you must advise IBIE immediately and provide an updated Form 8-3-6 where appropriate. For example, if you move tax residency from one country to another, you should advise IBIE and provide IBIE with a Form 8-3-6, signed and stamped by your local tax authority from your new country of residence.

Do I have to complete a Form 8-3-6? Can I still trade if I don’t complete it?

You do not have to complete Form 8-3-6 and you will still be able to trade if you do not complete the form.

However, if you do not complete Form 8-3-6 IBIE must continue to deduct WHT at a rate of 20% from the credit interest earned on cash balances in your account.

Where can I see information relating to Irish WHT on my account statement?

You can review information relating to Irish WHT in the ‘Withholding Tax’ section of your monthly account activity statement.

You can also view this information in your daily statement on the 3rd business day of the month (when credit interest is paid).

Please see the IBIE website here for more information: https://www.interactivebrokers.ie/en/index.php?f=46788

How do I know what WHT rate has been agreed between my country of residence and Ireland?

This information is available from the Irish Revenue Commissioners and/or your own local tax authority. However, in order to assist you, IBIE has also prepared a list of Irish WHT information by jurisdiction below.

By clicking on the country below, it will bring you to the relevant Form 8-3-6.

*Form 8-3-6 has been translated into French, German, Spanish, Italian and Dutch*

1. EEA countries with 0% Withholding Tax.

2. EEA countries with rates above 0% Withholding Tax.

|

|

3. Other countries with a DTA with Ireland (* denotes where there is 0% withholding tax in all situations).

|

Georgia |

Moldova |

Singapore |

|

|

Armenia |

Ghana |

Montenegro |

South Africa* |

|

Australia |

Hong Kong |

Morocco |

South Korea* |

|

Bahrain* |

India |

New Zealand |

Switzerland* |

|

Belarus |

Israel |

North Macedonia* |

Thailand |

|

Bosnia & Herzegovina* |

Japan |

Norway |

Turkey |

|

Botswana |

Kazakhstan |

Pakistan |

Ukraine |

|

Canada |

Kenya |

Panama |

United Arab Emirates* |

|

Chile |

Kosovo |

Qatar* |

United Kingdom* |

|

China |

Kuwait* |

Russian Federation* |

United States of America* |

|

Egypt |

Malaysia |

Saudi Arabia* |

Uzbekistan |

|

Ethiopia |

Mexico |

Serbia |

Vietnam |

|

|

|

|

Zambia* |

為什麼難以借到的股票其“價格”與收盤價不一致?

在確定借用股票頭寸所需存入的現金抵押金額時,通用的行業慣例是用股票前一個交易日**的收盤價乘以102%,向上取整到最近的美元,然後再乘以所借股數。由於借股費用根據現金抵押金額確定,這一慣例直接影響到維持空頭頭寸的成本,尤其是對那些股價不高但難以借到的股票。注意,不是以美元計價的股票,計算會有所不同。下表為各個幣種對應的行業慣例:

| 幣種 | 計算方法 |

| USD | 102%;向上取整到最近的元 |

| CAD | 102%;向上取整到最近的元 |

| EUR | 105%;向上取整到最近的分 |

| CHF | 105%;向上取整到最近的生丁 |

| GBP | 105%;向上取整到最近的便士 |

| HKD | 105%;向上取整到最近的分 |

賬戶持有人可在每日賬戶報表的“非直接難以借用股票詳情(Non-Direct Hard to Borrow Details)”部分查看借股價格。下方通過舉例說明了現金抵押金額的計算及其對借股費用的影響。

例 1

以$1.50美元的價格賣空100,000股ABC

賣空所得 = $150,000.00美元

假設ABC股價跌至$0.25美元,股票借貸費率為50%

賣空股票抵押金額計算

價格 = 0.25 x 102% = 0.255; 向上取整至$1.00美元

總金額 = 100,000股 x $1.00 = $100,000.00美元

借股費用 = $100,000 x 50% / 360天 = $138.89美元/天

假設賬戶持有人的現金餘額中沒有任何其它賣空交易所得,由於餘額沒有超過可以開始計息的最低門檻要求$100,000美元,將不會有任何賣空收益的利息收入可用於沖抵此借股費用。

例 2(以歐元計價的股票)

以1.50歐元的價格賣空100,000股ABC

假設前一個交易日收盤價為1.55歐元,股票借貸費率為50%

賣空股票抵押金額計算

價格 = 1.55歐元 x 105% = 1.6275; 向上取整至1.63歐元

總金額 = 100,000股 x 1.63 = 163,000.00歐元

借股費用 = 163,000歐元 x 50% / 360天 = 226.38歐元/天

** 請注意,週六和周天與週五一樣將採用週四的收盤價計算抵押金額。

股票收益提升計劃(SYEP)常見問題

股票收益提升計劃推出的目的是什麽?

股票收益提升計劃可供客戶通過允許IBKR將其賬戶內原本閑置的證券頭寸(即全額支付和超額保證金證券)出借給第三方來賺取額外收益。參與此計劃的客戶會收到用以確保股票在借貸終止時順利歸還的抵押(美國國債或現金)。

什麽是全額支付和超額保證金證券?

全額支付證券是客戶賬戶中全款付清的證券。超額保證金證券是雖然沒有全款付清但本身市場價值已超過保證金貸款餘額的140%的證券。

客戶股票收益提升計劃的借出交易收益如何計算?

客戶借出股票的收益取决于場外證券借貸市場的借貸利率。借出的股票不同,出借的日期不同,都會對借貸利率造成很大差异。通常,IBKR會按自己借出股票所得金額的大約50%向參與計劃的客戶支付利息。

借貸交易的抵押金額如何確定?

證券借貸的抵押(美國國債或現金)金額採用行業慣例確定,即用股票的收盤價乘以特定百分比(通常爲102-105%),然後向上取整到最近的美元/分。每個幣種的行業慣例不同。例如,借出100股收盤價爲$59.24美元的美元計價股票,現金抵押應爲$6,100 ($59.24 * 1.02 = $60.4248;取整到$61,再乘以100)。下表爲各個幣種的行業慣例:

| 美元 | 102%;向上取整到最近的元 |

| 加元 | 102%;向上取整到最近的元 |

| 歐元 | 105%;向上取整到最近的分 |

| 瑞士法郎 | 105%;向上取整到最近的生丁 |

| 英鎊 | 105%;向上取整到最近的便士 |

| 港幣 | 105%;向上取整到最近的分 |

更多信息,請參見KB1146。

股票收益提升計劃下的抵押如何保管以及保管在何處?

對於IBLLC的客戶,抵押將採用現金或美國國債的形式,並將轉入IBLLC的聯營公司IBKR Securities Services LLC (“IBKRSS”)進行保管。您在該計劃下借出股票的抵押會由IBKRSS以您爲受益人保管在一個賬戶中,您將享有第一優先級擔保權益。如果IBLLC違約,您將可以直接從IBKRSS取得抵押,無需經過IBLLC。請參見 此處的《證券賬戶控制協議》瞭解更多信息。對于非IBLLC的客戶,抵押將由賬戶所在實體保管。例如,IBIE的賬戶其抵押將由IBIE保管。

退出IBKR股票收益提升計劃或賣出/轉帳通過此計劃借出的股票會對利息造成什麽影響?

交易日的下一個工作日(T+1)停止計息。對於轉帳或退出計劃,利息也會在發起轉帳或退出計劃的下一個工作日停止計算。

參加IBKR股票收益提升計劃有什麽資格要求?

| 可參加股票收益提升計劃的實體* |

| 盈透證券有限公司(IB LLC) |

| 盈透證券英國有限公司(IB UK)(SIPP賬戶除外) |

| 盈透證券愛爾蘭有限公司(IB IE) |

| 盈透證券中歐有限公司(IB CE) |

| 盈透證券香港有限公司(IB HK) |

| 盈透證券加拿大有限公司(IB Canada)(RRSP/TFSA賬戶除外) |

| 盈透證券新加坡有限公司(IB Singapore) |

| 可參加股票收益提升計劃的賬戶類型 |

| 現金帳戶(申請參加時賬戶資産超過$50,000美元) |

| 保證金賬戶 |

| 財務顧問客戶賬戶* |

| 介紹經紀商客戶賬戶:全披露和非披露* |

| 介紹經紀商綜合賬戶 |

| 獨立交易限制賬戶(STL) |

*參加的賬戶必須是保證金賬戶或滿足上述現金帳戶最低資産要求的現金帳戶。

盈透證券日本、盈透證券盧森堡、盈透證券澳大利亞和盈透證券印度公司的客戶不能參加此計劃。賬戶開在IB LLC下的日本和印度客戶可以參加。

此外,滿足上方條件的財務顧問客戶賬戶、全披露介紹經紀商客戶和綜合經紀商可以參加此計劃。如果是財務顧問和全披露介紹經紀商,必須由客戶自己簽署協議。綜合經紀商由經紀商簽署協議。

IRA賬戶可以參加股票收益提升計劃嗎?

可以。

IRA賬戶由盈透證券資産管理公司(Interactive Brokers Asset Management)管理的賬戶分區可以參加股票收益提升計劃嗎??

不是。

英國SIPP賬戶可以參加股票收益提升計劃嗎?

不是。

如果參加計劃的現金帳戶資産跌破最低資産要求$50,000美元會怎麽樣?

現金帳戶只有在申請參加計劃當時必須滿足這一最低資産要求。之後資産跌破此要求並不會對現有借貸造成任何影響,也不影響您繼續借出股票。

如何申請參加IBKR股票收益提升計劃?

要參加股票收益提升計劃,請登錄客戶端。登錄後,點擊 使用者菜單(右上角的小人圖標),然後點擊設置。然後,在賬戶設置內,尋找交易板塊並點擊股票收益提升計劃 以申請參加。您將會看到參加該計劃所需填寫的表格和披露。閱讀並簽署表格後,您的申請便會提交處理。可能需要24到48小時才能完成激活。

如何終止股票收益提升計劃?

要退出股票收益提升計劃,請登錄客戶端。登錄後,點擊使用者菜單 (右上角的小人圖標),然後點擊 設置。在賬戶 設置板塊內會找到交易,然後點擊股票 收益 提升 計劃,然後依照所需步驟。您的申請便會提交處理。 中止參加的請求通常會在當日結束時進行處理。

如果一個賬戶參加了計劃然後又退出,那麽該賬戶多久可以重新參加計劃?

退出計劃後,賬戶需要等待90天才能重新參加。

哪些證券頭寸可以出借?

| 美國市場 | 歐洲市場 | 香港市場 | 加拿大市場 |

| 普通股(交易所掛牌、粉單和OTCBB) | 普通股(交易所掛牌) | 普通股(交易所掛牌) | 普通股(交易所掛牌) |

| ETF | ETF | ETF | ETF |

| 優先股 | 優先股 | 優先股 | 優先股 |

| 公司債券* |

*市政債券不適用。

借出IPO後在二級市場交易的股票有什麽限制嗎?

沒有,只要賬戶本身沒有就相應的證券受到限制就可以。

IBKR如何確定可以借出的股票數量?

第一步是確定IBKR有保證金扣押權從而可以在沒有客戶參與的情况下通過股票收益提升計劃借出的證券的價值(如有)。根據規定,通過保證金貸款借錢給客戶購買證券的經紀商可以將該客戶的證券借出或用作抵押,金額最高不超過貸款金額的140%。例如,如果客戶現金餘額爲$50,000美元,買入市場價值爲$100,000美元的證券,則貸款金額爲$50,000美元,那麽經紀商對$70,000美元($50,000的140%)的證券享有扣押權。客戶持有的證券超出這一金額的部分被稱爲超額保證金證券(此例子中爲$30,000),需要記在隔離賬戶,除非客戶授權IBKR通過股票收益提升計劃將其借出。

計算貸款金額首先要將所有非美元計價的現金餘額轉換成美元,然後减去股票賣空所得(轉換成美元)。如果結果爲負數,則我們最高可抵押此數目的140%。此外,商品賬戶段中持有的現金餘額和現貨金屬和差價合約相關現金不納入考慮範圍。 詳細說明請參見此處。

例1: 客戶在基礎貨幣爲美元的賬戶內持有100,000歐元,歐元兌美元匯率爲1.40。客戶買入價值$112,000美元(相當於80,000歐元)的美元計價股票。由於轉換成美元後現金餘額爲正數,所有證券被視爲全額支付。

| 項目 | 歐元 | 美元 | 基礎貨幣(美元) |

| 現金 | 100,000 | (112,000) | $28,000 |

| 多頭股票 | $112,000 | $112,000 | |

| 淨清算價值 | $140,000 |

例2: 客戶持有80,000美元、多頭持有價值$100,000美元的美元計價股票並且做空了價值$100,000美元的美元計價股票。總計$28,000美元的多頭證券被視爲保證金證券,剩餘的$72,000美元爲超額保證金證券。計算方法是用現金餘額减去賣空所得($80,000 - $100,000),所得貸款金額再乘以140% ($20,000 * 1.4 = $28,000)

| 項目 | 基礎貨幣(美元) |

| 現金 | $80,000 |

| 多頭股票 | $100,000 |

| 空頭股票 | ($100,000) |

| 淨清算價值 | $80,000 |

IBKR會把所有符合條件的股票都借出去嗎?

不保證賬戶內所有符合條件的股票都能通過股票收益提升計劃借出去,因爲某些證券可能沒有利率有利的市場,或者IBKR無法接入有意願的借用方所在的市場,也有可能IBKR不想借出您的股票。

通過股票收益提升計劃借出股票是否都要以100爲單位?

不是。只要是整股都可以,但是借給第三方的時候我們只以100爲倍數借出。這樣,如果有第三方需要借用100股,就可能發生我們從一個客戶那裏借出75股、從另一個客戶那裏借出25股的情况。

如果可供借出的股票超過借用需求,如何在多個客戶之間分配借出份額?

如果我們股票收益提升計劃的參與者可用以借出的股票數量大於借用需求,則借出份額將按比例分配。例如,可供借出XYZ數量爲20,000股,而對於XYZ的需求只有10,000股的情况下,每個客戶可以借出其所持股數的一半。

股票是只借給其它IBKR客戶還是也會借給其它第三方?

股票可以借給IBKR客戶和第三方。

股票收益提升計劃的參與者可以自行决定哪些股票IBKR可以借出嗎?

不是。此計劃完全由IBKR管理,IBKR在確定了自己因保證金貸款扣押權可以借出的證券後,可自行决定哪些全額支付或超額保證金證券可以借出,並發起借貸。

通過股票收益提升計劃借出去的證券其賣出是否會受到限制?

借出去的股票可隨時賣出,沒有任何限制。賣出交易的結算並不需要股票及時歸還,賣出收益會按正常結算日記入客戶的賬戶。此外,借貸會於證券賣出的下一個工作日開盤終止。

客戶就通過股票收益提升計劃借出去的股票沽出持保看張期權還能享受持保看漲期權保證金待遇嗎?

可以。由於借出去的股票其盈虧風險仍然在借出方身上,借出股票不會對相關保證金要求造成任何影響。

借出去的股票由於看漲期權被行權或看跌期權行權被交付會怎麽樣?

借貸將於平倉或减倉操作(交易、被行權、行權)的T+1日終止。

借出去的股票被暫停交易會怎麽樣?

暫停交易對股票借出沒有直接影響,只要IBKR能繼續借出該等股票,則無論股票是否被暫停交易,借貸都可以繼續進行。

借貸股票的抵押可以劃至商品賬戶段沖抵保證金和/或應付行情變化嗎?

不是。股票借貸的抵押不會對保證金或融資造成任何影響。

計劃參與者發起保證金貸款或提高現有貸款金額會怎麽樣?

如果客戶有全額支付的證券通過股票收益提升計劃借出,之後又發起保證金貸款,則不屬於超額保證金證券的部分將被終止借貸。同樣,如果客戶有超額保證金證券通過此計劃借出,之後又要增加現有保證金貸款,則不屬於超額保證金證券的部分也將被終止借貸。

什麽情况下股票借貸會被終止?

發生以下情况(但不限于以下情况),股票借貸將被自動終止:

- 客戶選擇退出計劃

- 轉帳股票

- 以股票作抵押借款

- 賣出股票

- 看漲期權被行權/看跌期權行權

- 賬戶關閉

股票收益提升計劃的參與者是否會收到被借出股票的股息?

通過股票收益提升計劃借出的股票通常會在除息日前召回以獲取股息、避免股息替代支付。但是仍然有可能獲得股息替代支付。

股票收益提升計劃的參與者是否對被借出的股票保有投票權?

不是。如果登記日或投票、給予同意或採取其它行動的截止日期在貸款期內,則證券的借用者有權就證券相關事項進行投票或决斷。

股票收益提升計劃的參與者是否能就被借出的股票獲得權利、權證和分拆股份?

可以。被借出股票分配的任何權利、權證和分拆股份都將屬於證券的借出方。

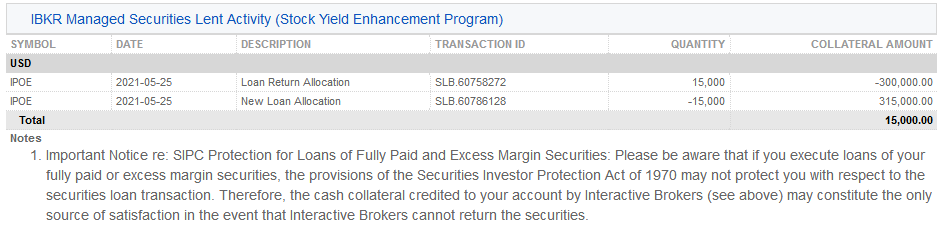

股票借貸在活動報表中如何呈現?

借貸抵押、借出在外的股數、活動和收益在以下6個報表區域中反映:

1. 現金詳情 – 詳細列出了期初抵押(美國國債或現金)餘額、借貸活動導致的淨變化(如果發起新的借貸則爲正;如果股票歸還則爲負)和期末現金抵押餘額。

2. 淨股票頭寸總結 – 按股票詳細列出了在IBKR持有的總股數、借入的股數、借出的股數和淨股數(=在IBKR持有的總股數 + 借入的股數 - 借出的股數)。

3. 借出的IBKR管理證券(股票收益提升計劃) – 對通過股票收益提升計劃借出的股票按股票列出了借出的股數以及利率(%)。

3a. 在IBSS保管的IBKR管理證券的抵押(股票收益提升計劃) – IBLLC的客戶會看到其報表中多出來一欄,顯示作爲抵押的美國國債以及抵押的數量、價格和總價值。

4. IBKR管理證券借出活動 (股票收益提升計劃)– 詳細列出了各證券的借貸活動,包括歸還份額分配(即終止的借貸);新借出份額分配(即新發起的借貸);股數;淨利率(%);客戶抵押金額及其利率(%)。

5. IBKR管理的證券借出活動利息詳情 (股票收益提升計劃)– 按每筆借出活動詳細列出了IBKR賺取的利率(%);IBKR賺取的收益(爲IBKR從該筆借出活動賺取的總收益,等于{抵押金額 * 利率}/360);客戶抵押的利率(爲IBKR從該筆借出活動賺取的收益的一半)以及支付給客戶的利息(爲客戶的現金抵押賺取的利息收入)

注:此部分只有在報表期內客戶賺取的應計利息超過1美元的情况下才會顯示。

6. 應計利息 – 此處利息收入列爲應計利息,與任何其它應計利息一樣處理(累積計算,但只有超過$1美元才會顯示並按月過帳到現金)。年末申報時,該筆利息收入將上報表格1099(美國納稅人)。

確定利率的方法

背景

在確定賬戶持有人正現金餘額可以獲得的利息和負現金餘額需要支付的利息時,每種貨幣均有一個IBKR參考基準利率。IBKR參考基準利率根據短期市場利率確定,但會圍繞市場普遍使用的外部參考利率或銀行存款利率設置偏離的上限。本文解釋了IBKR參考基準利率是如何確定的。

參考利率

參考利率分三步確定。其偏離傳統外部參考利率的幅度不得超過一定限制。 對于外匯掉期市場定價幷不會對我們的利率造成影響的幣種和IBKR聯營公司,確定最終利率時會省略第一步。

1. 市場隱含利率

對于市場定價,我們參考的是短期外匯掉期市場。由于大部分交易都涉及美元,我們會抽取一個預定義時間段內各貨幣相對于美元的外匯掉期價格,其中定義的時間段被稱爲“定價時間窗口”,反映流動交易時間和主要成交量。特定的互換期限及定價窗口視貨幣而不同。隱含的非美元短期利率將根據多達12家最大的外匯做市銀行的最佳買賣價格計算得出(通常爲隔夜(T/T+1),Tom Next (T+1/T+2)或Spot Next (T+2/T+3))。定價時間窗口結束後,將這些結果排序,剔除最高及最低的價格,然後對剩餘的結果做平均,從而得出市場隱含的參考利率。

2. 傳統外部基準參考利率

對于傳統基準,我們采用的是已公布的參考利率和銀行存款利率。該等利率通常是根據銀行調研或實際交易情况確定的。比如香港銀行同業拆借利率(HIBOR)就是根據對一組銀行的調研得出的,調研會詢問銀行在每天的某個特定時間能够以什麽樣的利率從其它銀行借到資金。與此相反,美元聯邦基金利率則是聯邦基金市場上銀行間拆借利率的加權平均值。

由20國集團國家于2013年發起幷由監管機構以及公共和私營部門工作小組實施推行的利率基準改革(IBOR改革)正在逐漸用由新交易驅動的參考利率取代銀行調研利率。

3. IBKR參考基準利率

最後,我們會使用1中的市場隱含利率,然後在2中的傳統基準利率的基礎上應用一定比例的偏離上限,從而得出最終的IBKR參考基準利率。 對于不受外匯掉期市場定價影響的幣種和IBKR聯營公司,最終的IBKR參考基準利率采用傳統基準或銀行存款利率確定,幷設置前面提到的偏離上限。上限可在沒有事先明示通知的情况下隨時更改,幷在下方表格中列出。一幷列出的還有相關貨幣和基準參考利率。

舉例

a. 假設英鎊的市場隱含隔夜利率爲0.55%。英鎊隔夜銀行同業拆借平均利率(SONIA)爲0.65%。則實際利率等于0.55%的市場隱含利率,因爲該利率仍在SONIA參考利率(0.65%)加减1.00%的範圍內。

b. 如果假設離岸人民幣的市場隱含利率爲4.5%,但同期的隔夜參考利率爲1.0%,則實際利率的上限將被設置在參考利率加2%,即3% (1.0%參考利率 + 2.0%偏離上限)。

|

貨幣

|

基準利率描述

|

向下偏離上限1

|

向上偏離上限1

|

|

USD

|

聯邦基金有效利率(隔夜利率)

|

0.00%

|

0.00%

|

|

AUD

|

澳洲聯儲(RBA)每日目標隔夜拆借利率

|

1.00%

|

1.00%

|

| AED | 阿聯酋銀行同業拆借利率(EIBOR) | 3.00% | 3.00% |

|

CAD

|

加拿大銀行隔夜借貸利率

|

1.00%

|

1.00%

|

|

CHF

|

瑞士平均隔夜利率(SARON)

|

1.00%

|

1.00%

|

|

CNY/CNH

|

離岸人民幣固定香港銀行同業隔夜拆借利率(TMA)

|

2.00%

|

2.00%

|

|

CZK

|

布拉格Prague ON銀行間同業拆借利率

|

1.00%

|

1.00%

|

|

DKK

|

丹麥Tom/Next指數

|

1.00%

|

1.00%

|

|

EUR

|

歐元短期利率(€STR)

|

1.00%

|

1.00%

|

|

GBP

|

英鎊隔夜銀行同業拆借平均利率(SONIA)

|

1.00%

|

1.00%

|

|

HKD

|

港幣香港銀行同業拆借利率(隔夜利率)

|

1.00%

|

1.00%

|

|

HUF

|

布達佩斯銀行同業拆借利率

|

1.00%

|

1.00%

|

|

ILS

|

特拉維夫銀行同業拆借利率

|

1.00%

|

1.00%

|

|

INR

|

印度中央銀行基準利率

|

0.00%

|

0.00%

|

|

JPY

|

東京隔夜平均利率(TONAR)

|

1.00%

|

1.00%

|

|

KRW

|

韓元KORIBOR(1周)

|

0.00%

|

0.00%

|

|

MXN

|

墨西哥銀行間TIIE利率(28天利率)

|

3.00%

|

3.00%

|

|

NOK

|

挪威隔夜加權平均

|

1.00%

|

1.00%

|

|

NZD

|

新西蘭元官方每日現金利率

|

1.00%

|

1.00%

|

|

PLN

|

華沙銀行間隔夜拆借利率(WIBOR)

|

1.00%

|

1.00%

|

| SAR | 沙特阿拉伯銀行同業拆借利率(SAIBOR) | 3.00% | 3.00% |

|

SEK

|

SEK STIBOR(隔夜利率)

|

1.00%

|

1.00%

|

|

SGD

|

新加坡元SOR(互換隔夜)利率

|

1.00%

|

1.00%

|

|

TRY

|

土耳其里拉隔夜銀行同業拆借利率(TRLIBOR)

|

無上限

|

無上限

|

|

ZAR

|

南非存款基準隔夜利率(Sabor)

|

3.00%

|

3.00%

|

1實際利率偏離基準利率的上限可在無事先明示通知的情况下隨時變動。

Benchmark Interest Calculation – Reference Rate Descriptions

|

Currency

|

Reference rate

|

Description

|

|

USD

|

Fed Funds Effective

|

Volume weighted average of the transactions processed through the Federal Reserve between member banks. It is intended to reflect the best estimate of interbank financing activity for Reserve Bank members and is the reference for many short-term money market transactions in the broader market.

|

| AED | EIBOR | Is the daily reference rate at which the Panel Banks are able and willing to access UAE Dirham funding, just prior to 11:00 local time. The Contributor Banks use a waterfall in order to contribute their Contributions. For Level 1 of the waterfall, volume weighted average prices of all eligible unsecured Saudi Riyal transactions are used. |

|

AUD

|

RBA Daily Cash Target

|

Refers to a 1-day rate set by the Reserve Bank of Australia to influence short term interest rates.

|

| BGN | LEONIA Plus (Lev Overnight Index Average Plus) | Is a weighted reference rate of concluded and effected overnight deposit transactions on the interbank market. |

|

BRL

|

Brazil CETIP DI Interbank Deposit Rate

|

Brazil’s Interbank Deposit Rate is the daily average annualized rate calculated by the number of business days in the month, of the one-day interbank deposit rates.

|

|

CAD

|

Bank of Canada Overnight Lending Rate

|

Refers to a 1-day rate set by Bank of Canada to influence short term interest rates.

|

|

CHF

|

SARON

|

Stands for Swiss Average Rate Overnight and represents the overnight interest rate of the secured funding market for the Swiss Franc. SARON is administered by SIX.

|

|

CNH

|

CNH HIBOR

|

Stands for Hong Kong Interbank Offered Rate and is the offered rate at which deposits in CNH are being quoted to prime banks in the Hong Kong interbank market.

|

|

CZK

|

PRIBOR

|

Average interest rate at which term deposits are offered between prime banks.

|

|

DKK

|

Denmark Tomorrow/Next

|

The interest rate at which a bank is prepared to lend Danish kroner to a prime bank on an uncollateralized basis day to day.

|

|

EUR

|

€STR

|

Stands for Euro Short-Term Rate and is the rate which reflects the wholesale euro unsecured overnight borrowing costs of euro area banks. The rate is published by the ECB and is based on transactions conducted and settled on the previous day and which are deemed to be executed at arm’s length and thereby reflect market rates in an unbiased way.

|

|

GBP

|

SONIA

|

Stands for Sterling Overnight Index Average and is the effective overnight interest rate paid by banks for unsecured transactions in the British sterling market. SONIA is administered by the Bank of England.

|

|

HKD

|

HKD HIBOR

|

Stands for Hong Kong Interbank Offered Rate and is the offered rate at which deposits in HKD are being quoted to prime banks in the Hong Kong interbank market.

|

|

HUF

|

BUBOR

|

Stands for Budapest Interbank Offered Rates and is the average interest rate at which term deposits are offered between prime banks.

|

| HUF | Hungary 3 Month Treasury Bill | Is an annualized yield on Hungarian 3 month Treasury bills. |

|

ILS

|

TELBOR

|

Stands for Tel Aviv Inter-Bank Offered Rate and is based on interest rate quotes by a number of contributors in the inter-bank market.

|

|

INR

|

Indian Rupee Overnight Interest Rate Fixing

|

A rate based on overnight call money trade data from the NDS-Call system within the first hour of trading.

|

|

JPY

|

TONAR

|

Stands for Tokyo Overnight Average Rate and is a measure of the cost of borrowing in the Japanese yen unsecured overnight money market for Japanese Yen. TONAR is administered by the Bank of Japan.

|

|

KRW

|

KORIBOR

|

Average of the leading interest rates for KRW as determined by a group of large Korean banks. The benchmark utilizes the KORIBOR with 1 week maturity.

|

|

MXN

|

TIIE

|

The interbank "equilibrium" rate based on the quotes provided by money center banks as calculated by the Mexican Central Bank. The benchmark TIIE is based on 28-day deposits so is atypical as a measure for short term funds (most currencies have an overnight or similar short-term benchmark).

|

|

NOK

|

Norwegian Overnight Weighted Average

|

The interest rate on unsecured overnight interbank loans between banks that are active in the Norwegian overnight market.

|

|

NZD

|

NZD Daily Cash Target

|

Refers to a 1-day rate set by the Reserve Bank of New Zealand to influence short term interest rates.

|

|

PLN

|

WIBOR

|

Stands for Warsaw Interbank Offered Rates and is a measure of unsecured deposits concluded between market participants.

|

| RON | ROBOR (Romanian Overnight Interbank Offered Rate) | Calculated daily as a trimmed arithmetic average of the quotations by main banks on the interbank market. |

| SAR | SAIBOR | Is a daily benchmark using contributions from a panel of Contributor Banks. The Contributor Banks use a waterfall in order to contribute their Contributions. For Level 1 of the waterfall, volume weighted average prices of all eligible unsecured Saudi Riyal transactions are used. |

|

SEK

|

STIBOR

|

Daily fixing based on a group of large Swedish banks.

|

|

SGD

|

SOR

|

Stands for the SGD Swap Offer Rate and represents the cost of borrowing SGD synthetically by borrowing USD for the same maturity and swapping USD in return for SGD.

|

|

TRY

|

TLREF

|

The Turkish Lira Overnight Rate (TLREF) is calculated as the volume-weighted mean rate, based on the central 70% of the the volume-weighted distribution of overnight repo rate transactions. |

|

ZAR

|

SABOR

|

Stands for South African Benchmark Overnight Rate and is calculated based on interbank funding.

|

|

|

|

|

|

|

|

|

|

|

Overnight

|

(O/N) rate is the most widely used short term benchmark and represents the rate for balances held from today until the next business day.

|

|

|

Spot-Next

|

(S/N) refers to the rate on balances from the next business day to the business day thereafter. Due to time zone and other criteria, Spot-Next rates are sometimes used as the short-term reference.

|

|

|

Day-Count conventions:

|

IBKR conforms to the international standards for day-counting wherein deposits rates for most currencies are expressed in terms of a 360-day year, while for other currencies (ex: GBP) the convention is a 365-day year.

|