如何向盈透證券提出投訴?

如需向盈透證券提出投訴,請通過客戶端提交故障諮詢單:

- 登錄客戶端

- 點擊幫助

- 選擇安全消息中心

- 選擇撰寫,然後新諮詢單

- 在類別選擇賬戶服務,而主題為投訴

- 在簡短描述中寫上“投訴”,然後提交

- 選擇賬戶,然後在空白欄位鍵入您的詳細信息

- 提交諮詢單

在諮詢單正文中,IBKR要求您提供投訴的詳細描述。如果您的投訴涉及交易,IBKR要求您提供交易詳情,其中可能包括但不限於委託單的提交日期和時間、證券描述、執行日期和時間、執行價格,以及提供計算過程的要求補償金額。請注意,所有與交易相關的爭議必須及時提交。具體而言,交易取消請求必須在IBKR和/或交易所的時間參數範圍內。

收到您的投訴後,IBKR將通過客戶端確認和回覆您的投訴,並創建一張以“與諮詢單#<諮詢單號碼>相關的投訴通信”為名的新諮詢單。此後,請在通信諮詢單中進行與投訴相關的所有通信往來。

通常,投訴將在三到五天內得到答覆;但是,某些複雜的問題可能需要更長的時間來評估。在這段時間,IBKR要求您管理賬戶中的所有委託單、交易和持倉,以確保在調查期間您的賬戶不會受到不必要的風險或波動的影響。

雖然所有提交的索賠也會得到公平和公正的考慮,但提出索賠並不保證能夠獲得部分或全額支付所要求的金額。我們鼓勵索賠人查看客戶協議,因為有關投訴是基於本協議中的條文進行評估。如果客戶協議與IBKR網站不同,則客戶協議將取代網站版本。關於與交易相關的投訴,請注意客戶協議中的以下條款:(i)客戶對使用客戶用戶名 / 密碼鍵入的所有交易負責;(ii)取消請求並不保證;(iii)IBKR不對任何交易所、市場、交易商、清算所或監管機構的任何行動或決定負責,(iv)如果與客戶的委託單一致,客戶受委託單執行的約束,以及(v)客戶有責任瞭解所交易產品的條款和條件以及相應的市場。客戶有責任隨時在賬戶內保持足夠的淨值,以滿足保證金要求。如果客戶賬戶的淨值不足,IBKR有權(但非必需)隨時以任何方式清算客戶的全部或部分持倉,而不會事前通知客戶。請注意,IBKR在任何時候都不會就技術問題或機會損失對客戶進行賠償。

要查看完整的IBKR客戶協議,請在IBKR主頁底部選擇表格和披露,然後選擇適用的客戶協議。

現金劃轉

背景

IB全能賬戶由兩個獨立的子賬戶或賬戶段組成,一個用于持有證券倉位和餘額,受美國證券交易委員會(SEC)客戶保護規則約束,另一個用于持有商品倉位和餘額,受美國商品期貨交易委員會(CFTC)客戶保護規則約束。這種全能賬戶的設計旨在盡可能地降低客戶維護兩個不同賬戶(例如,賬戶之間轉帳現金、兩個賬戶登錄和提交委托單、多份報表等)可能面臨的行政管理開銷,同時又維持法規要求的分隔措施。

該等法規還要求所有證券交易和相關保證金交易均在全能賬戶的證券賬戶段進行,而商品交易則在商品賬戶段進行。1 雖然法規允許將全額支付的證券持倉以保證金抵押品的形成存放在商品賬戶段進行托管,但IB幷不允許這種操作,從而對抵押權應用了更爲嚴格的SEC限制性規則。鑒于相關法規和政策已對持倉應歸于哪個賬戶段作出了規定,現金是唯一可由客戶自行决定在兩個賬戶段之間來回轉帳的資産。

下方爲現金劃轉選項、選擇步驟和注意事項相關的說明。

現金劃轉選項

客戶有三種劃轉選項,說明如下:

1. 不劃轉剩餘資金 – 根據這個選項,如非必要,剩餘現金不會在兩者之間進行轉移:

a. 解决/緩解另一賬戶段保證金不足的問題;

b. 盡可能地降低指定賬戶段的借方現金餘額,從而减少相關的利息費用。 請注意,對于只擁有證券或商品交易許可中一項許可的賬戶持有人來說,這是默認選項,也是唯一的選項。

2. 將剩餘資金劃轉至我的IB證券賬戶 – 只在商品賬戶段中留下能滿足當前商品保證金要求的現金餘額。 任何由于現金增加(例如,有利的變化和/或與交易相關)或保證金要求降低(例如,SPAN風險陣列和/或與交易相關的變化)而産生的超出保證金要求的現金,都將自動從商品賬戶段轉移到證券賬戶段。請注意,賬戶持有人必須具備證券交易許可才能選擇此選項。

3. 將剩餘資金劃轉至我的IB商品賬戶 – 只在證券賬戶段中留下能滿足當前證券保證金要求的現金餘額(加上含有貸款價值的其它證券倉位)。請注意,賬戶持有人必須具備商品交易許可才能選擇此選項。

其它注意事項:

- 由于全能賬戶允許以不同幣種持有現金餘額,因此存在一個層次結構,以决定當多種貨幣出現多頭餘額時,首先轉移哪種貨幣。在這類情况下,首先會轉移以基礎貨幣計價的餘額,然後是美元,然後剩下的多頭餘額再按金額從高到低的順序轉移。

- 爲了盡可能地降低一個賬戶段在把剩餘現金劃轉至另一個賬戶段後出現保證金不足的可能性,剩餘資金不會全部轉移,而是會留下相當于維持保證金要求5%的資金作爲緩衝。 同樣,爲了盡可能地降低轉移名義餘額的運營開銷,只有在扣除5%的保證金緩衝後,剩餘金額(如有)仍不低于賬戶淨資産的1%或200美元時,才會轉移餘額。

- 在執行交易前信用核查以確定賬戶是否擁有足够的淨資産來支持新的委托單時,一個賬戶段內進行的交易也會將另一個賬戶段內的剩餘現金納入考慮(但在交易執行之前不會進行劃轉,幷且也只有在爲了滿足保證金要求而有必要時才會進行劃轉)。 被標記爲典型日內交易者以及需要進行交易前信用核查(會考慮前一日和當日淨資産)的賬戶應特別留意下方選擇注意事項。

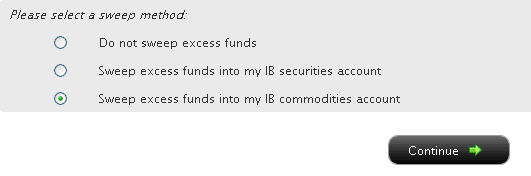

選擇劃轉的選項

如果您的賬戶管理版本在左側有一系列菜單選項,請選擇賬戶行政,然後選擇 剩餘資金劃轉菜單選項。 如果您的版本是頂部有菜單選項,請選擇管理賬戶/設置,然後選擇 配置賬戶/剩餘資金劃轉菜單選項。無論您的版本如何,您都將看到以下界面:

然後,您可點擊您想要的劃轉方式對應的單選按鈕,然後選擇〝繼續〞按鈕。您的選擇將從下一個工作日起生效,幷將一直有效,直到選擇其它選項爲止。請注意,只要滿足上文中提到的交易許可設置,您可隨時更改劃轉方式,沒有次數限制。

選擇注意事項

雖然選擇將剩餘現金存放在哪個賬戶段可能涉及每位客戶獨特的主觀决策和偏好(例如,客戶將大部份資産集中存放在其中一個賬戶段),但下述有幾個因素值得注意:

1. 典型日內交易淨資産 - 根據相關法規被標記爲典型日內交易者的賬戶(即在5個工作日內進行4次或以上日內交易),其證券購買力將被限制爲證券賬戶段當日或前一日收盤淨資産中的較低者。根據這個計算方式,如選擇將剩餘資金劃轉至商品賬戶段,則該筆資金將無法納入計算,從而可能對下達新委托單的造成一定限制。要最大程度地利用淨資産來擴大購買力下達證券委托單,客戶需選擇將剩餘資金劃轉至證券賬戶段。 請注意,選擇證券賬戶段幷不會限制下達商品委托單的能力,因爲典型日內交易規則不適用于此類賬戶。

2. 保險 – 美國證券投資者保護公司(SIPC)的保障範圍覆蓋證券賬戶段的資産,而商品賬戶段則沒有相應的保障計劃。不過,超過SIPC的$250,000現金分項給付限額(勞合社現金分項給付限額爲$900,000,如適用)的餘額不在承保範圍內。 IB加拿大和IB英國的客戶也分別受加拿大投資者保護基金(CIPF)和英國金融服務補償計劃(FSCS)規定的承保規則約束。

3.利息收入 – 在所有其它條件相同的情况下,從未將多頭現金餘額在證券和商品賬戶段中分開存放的客戶,可望獲得最高的利息收入,這是因爲兩者不會匯總以計算貸方利息(它們受不同的隔離池和再投資規則的約束)。 在選擇現金劃轉時,除了上述的因素外,也應該要考慮到貸款需要維持最低現金餘額,幷且餘額高一些,利率也會優惠一些。2

脚注:

1由于OneChicago個股期貨是由SEC和CFTC共同監管的混合産品,因此可在任何一種賬戶類型中進行買賣。不過,IB選擇在全能賬戶的證券賬戶段進行此類交易,因爲只有在這情况下,才能向單一股票期貨和任何合資格股票或期權持倉提供保證金减免。

2例如,某賬戶在證券和商品賬戶段各持有$9,000的多頭美元餘額。根據基準聯邦基金有效利率,如果兩個餘額存放在同一賬戶段,該賬戶有$8,000 ($18,000 - $10,000)可以獲得利息。但由于分別放在兩個賬戶段中的現金餘額均低于$10,000,都無法獲得利息,如不選擇現金劃轉,將無法賺取任何利息。同樣,如進行現金劃轉後,某賬戶段的多頭美元現金餘額超過$100,000,則賬戶持有人將能够賺取更高一檔的利息。有關利息計算的其它信息,包括當前基準利率的鏈接,請參閱KB39。

Key Information Documents (KID)

Overview:

IBKR is required to provide EEA and UK retail customers with Key Information Documents (KID) for certain financial instruments.

Relevant products include ETFs, Futures, Options, Warrants, Structured Products, CFDs and other OTC products. Funds include both UCITS and non-UCITS funds available to retail investors.

Generally KIDs must be provided in an official language of the country in which a client is resident.

However, clients of IBKR have agreed to receive communications in English, and therefore if a KID is available in English all EEA and UK clients can trade the product regardless of their country of residence.

In cases where a KID is not available in English, IBKR additionally supports other languages as follows:

| Language | Can be traded by residents or citizens* of |

| German | Germany, Austria, Belgium, Luxembourg and Liechtenstein |

| French | France, Belgium and Luxembourg |

| Dutch | the Netherlands and Belgium |

| Italian | Italy |

| Spanish | Spain |

*regardless of country of residence

Are CDs purchased through IBKR FDIC insured?

Certificates of Deposit (CDs) offered by IBKR are not FDIC insured and are subject to the credit risk of the issuing bank.

有關客戶資產保護的信息

下列信息適用於非美國指數期權、場外(OTC)差價合約(CFD)及非美國指數期貨(與非美國指數期權相結合時)的交易

盈透證券(英國)有限公司

客戶資產

盈透證券(英國)有限公司("IBUK")由金融市場行為監管局(FCA)授權並規管,註冊號碼208159。 IBUK是由盈透證券集團(IBG LLC)全資擁有的子公司。 IBUK按照FCA客戶資產規則"CASS"提供客戶資金與客戶資產服務。

客戶資金受到下列保護:

客戶資金規則適用於所有在從事金融工具市場法規(MiFID)業務及/或指定投資業務的過程中從客戶處收取資金,或持有客戶資金的規管公司。

客戶資金與IBUK自有資金完全分離。如果出現授權公司破產的情況,在分離賬戶中持有的客戶資金將被歸還給客戶而不是被債權人看做可收回資產。如果出現差額,客戶可能有資格向金融服務補償計劃("FSCS")要求補償。

客戶資金圈定在獨立銀行賬戶中,以信託形式在客戶名義下持有。這些賬戶分散在多家具有投資等級評級的銀行中,以避免一家機構的風險集中性。 IBUK選擇並指定持有客戶資金的銀行時會考慮銀行的專業性、市場聲譽、財務狀況及任何可能對客戶權利有負面影響的有關客戶資金持有的法律要求及市場慣例。

IBUK僅在以下情況下允許交易所、清算所或中介經紀商在客戶交易賬戶中持有客戶資金:向其轉賬資金是用於交易或用於滿足客戶提供交易抵押的義務。

IBUK每天對在客戶資金銀行賬戶及客戶交易賬戶中持有的客戶資金及其對客戶的負債作詳細的對賬,確保客戶資金被恰當隔離,且足夠滿足FCA的CASS規則要求的所有債務。所有計入這些銀行賬戶的資金公司均作為受託人持有(或者如果相關,作為代理)。

FCA規則還要求IBUK維持CASS決議,以確保萬一公司發生清算的情況下,破產管理人能夠查找信息以便向公司客戶及時歸還客戶資金及資產。

金融服務補償計劃

盈透證券(英國)有限公司("IBUK")是由金融市場行為監管局("FCA")授權並規管的投資公司,以及金融服務補償計劃("FSCS")成員。按照FCA補償規則,某些合格客戶有資格獲得補償。

有關合格性的要點為:

- FSCS僅在授權公司欠款的情況下才向合格申請人支付賠償並將調查是否存在該事實。

- FSCS僅賠償財務損失,對UK投資公司的限制在下面列出。

- FSCS的設立主要為了幫助個人,儘管小型公司也包括在內。

- 大型公司通常排除在外。

投資

如果授權投資公司無法滿足索賠,則FSCS提供保護——例如,如果一家授權投資公司破產,不能將資產返還給其客戶。 FSCS授權投資公司歸類為投資的資產包括股票與股份、期貨、期權、CFD及其他由客戶投入的規管金融工具及資金。

賠償限制

您收到的實際賠償水平將基於您的索賠。 FSCS僅支付金融損失賠償。賠償限制限各授權公司,各個人。

當前對投資的最高賠償水平為各公司各人5萬英鎊(向從2010年一月1日起被宣布欠款的公司提出的索賠)。賠償水平可能變化,要獲取最新詳情請見FSCS網站://www.fscs.org.uk / 。

下列信息適用於所有曾經或繼續通過IB LLC交易所有產品(除金屬及OTC CFD)的客戶。

盈透證券有限公司("IBLLC")

客戶資產

客戶資產隔離在指定給IBLLC客戶的專用特殊銀行或託管賬戶中。該保護(SEC稱為“儲備”,CFTC稱為“隔離”)是證券和商品經紀的核心原則。通過妥善分離客戶資產,如果客戶沒有借入資金或股票,且未持有期貨頭寸,那麼倘若經紀商違約或破產,客戶資產可以返還給客戶。

無借貸現金或證券的證券賬戶

證券客戶資金保護如下:

- 一部分存在14家大型美國銀行的IBLLC客戶專用特殊儲備賬戶中。這些存款分佈在多家具投資等級評級的銀行,以避免任何單個機構帶來的集中風險。每間銀行持有的資金不超過IBLLC所持客戶資產的5%。

- 一部分投資於美國國債,包括直接投資短期國債和以美國國債作為抵押的反向回購協議。這些交易與第三方進行並通過中央對手方清算所(固定收益結算公司,即“FICC”)擔保。抵押為IBLLC所有並存放在託管銀行客戶專用的隔離儲備保管賬戶。美國國債也可質押給清算所用以支持客戶所持證券期權頭寸的保證金要求。

- 客戶現金在儲備賬戶中以淨值為基礎,反映超出客戶借方餘額的淨貸方餘額。已達到任一客戶在IBLLC有保證金借貸,該借貸都有價值借貸額度200%的股票進行擔保的程度。

- 目前美國證券交易委員會(SEC)要求經紀交易商至少每週對客戶的資金和證券進行詳細核對(也稱為“儲備計算”),以確保客戶的資金準確地與經紀交易商的基金分離。

客戶擁有的、全額支付的證券在明確認定的客戶專用存管和託管賬戶中受到保護。 IBLLC每日核對客戶擁有的證券頭寸,確保存管和託管機構已收到這些證券。

商品帳戶

商品客戶資金保護如下:

- 一部分質押給期貨清算所用以支持客戶所持期貨及期貨期權頭寸的保證金要求,或在確定為用於隔離IB客戶資金的託管賬戶中持有。

- 一部分存放在確定為隔離IBLLC客戶資金的商品清算銀行/經紀商賬戶中,以支持客戶保證金要求。

- 按商品法規定,客戶資金受到實時保護。 IBLLC每日對客戶資產進行詳細核對,以確保客戶資金被恰當分離。計算結果每日提交給監管機構。

有保證金借貸的證券帳戶

向IBLLC借款買入證券的客戶,證券法規允許IBLLC最高抵押或借入價值借貸價值140%的股票。通常,IBLLC借出其獲許借出股票總數中的一小部分。

- 例如,在2011年6月30日,IBLLC從保證金客戶提供的130億美元股票中藉出8億美元。

- 當IBLLC借出客戶的股票時,必須將額外資金存入指定儲備賬戶,為客戶設置預留金額。在上面的例子中,借出的客戶股票的總價值8億美元隔離在特殊儲備金賬戶中。

帳戶保護

IBLLC客戶證券賬戶受到證券投資人保護公司("SIPC")最高達50萬美元(現金額度25萬美元)的保護,且根據IBLLC與倫敦勞埃德保險公司(Lloyd's of London)承銷商協定的超SIPC賠額政策,證券賬戶還享有額外最高達3000萬美元(現金額度90萬美元)的保護,總限額一億五千萬。期貨、期貨期權不包含在內。與所有證券公司相同,此類保險在經紀交易商倒閉時為客戶提供保護,而不是針對證券市場價值的損失。

出於確定客戶賬戶的目的,有相似的名字和名稱的賬戶被合併在一起(例如:John和Jane Smith與Jane和John Smith),但名稱不同的賬戶不合併(例如:個人/John Smith和個人退休賬戶/John Smith)。

SIPC是一個非盈利性質,由SIPC成員經紀交易商集資的成員性質的公司。查看關於SIPC的更多信息和常見問題解答(例如SIPC怎樣運作,什麼受到保護,怎樣索賠,等等),請參見以下網站:

http://www.finra.org/InvestorInformation/InvestorProtection/SIPCProtecti...

或聯繫SIPC,地址如下:

Securities Investor Protection Corporation

805 15th Street, N.W. - Suite 800

Washington, D.C. 20005-2215

電話:(202) 371-8300

傳真:(202) 371-6728

Information Regarding SIPC Coverage

1. Interactive Brokers LLC is a member of SIPC.

2. SIPC protects cash and securities held with Interactive Brokers.

3. SIPC does not generally cover commodity futures or options on futures.

4. SIPC protects cash, including US dollars and foreign currency, to the extent that the cash was "deposited with Interactive Brokers for the purpose of purchasing securities."

5. SIPC does not generally cover cash or foreign currency that is not "deposited with Interactive Brokers for the purpose of purchasing securities." For example, SIPC does not generally cover cash in commodity futures trading accounts.

6. Interactive Brokers is not able to make any statements or representations about how cash deposited into a securities account in connection with forex trading or swept from a commodities account would be treated by SIPC. SIPC protection would depend in part on whether the cash was considered to be "deposited with Interactive Brokers for the purpose of purchasing securities." Interactive Brokers expects that at least one factor in deciding this would be whether and the extent to which the customer engages in securities trading in addition to or in conjunction with forex or commodities trading.

Account holders seeking further information should refer such inquiries to their own legal counsel or SIPC.

Excess Margin Securities

The term "excess margin securities" refers to margin securities carried for the account of a customer having a market value in excess of 140 percent of the total debit balance in the customer's account. These securities are in excess of the securities held in a customer's margin account that are pledged by the customer as collateral for the margin loan and can be used to support the purchase of additional securities on margin

Example:

A customer whose account equity consists solely of a cash balance of USD 10,000 on Day 1 purchases 400 shares of stock ABC at USD 50 per share on Day 2.

| Account Balance | Day 1 | Day 2 |

| Cash | $10,000 | ($10,000) |

| Stock | $0 | $20,000 |

| Total | $10,000 | $10,000 |

On Day 2, the customer's excess margin securities total USD 6,000. This is calculated by subtracting 140% of the margin debit or loan balance from the market value of the stock position ($6,000 = $20,000 - {1.4 * $10,000}).

The term is relevant from a regulatory perspective as the SEC requires that U.S. broker dealers segregate and maintain in a good control location (e.g., DTC or bank) all customer securities which are deemed excess margin securities. Such securities cannot be pledged or loaned to finance the activities of the firm or other customers without specific written permission from the customer. The portion of the securities classified as margin securities ($20,000 - $6,000 or $14,000 in this example) are subject to a lien and may be pledged or loaned by the broker to others to assist in financing the loan made to the customer.

Note that securities which were excess margin at the date of acquisition may later be reclassified as margin securities based upon the customer's subsequent trade and/or margin borrowing activity. For example, if the loan value of excess margin securities is subsequently used to acquire additional securities on margin, a portion of securities will then be reclassified as margin securities and subject to a lien. If the customer subsequently deposits cash or sells securities to reduce or eliminate the margin loan, the securities will be reclassified as excess margin or fully paid and are required to be segregated.

See also "fully paid securities".

Fully Paid Securities

The term "fully paid securities" refers to securities held in a customer's margin or cash account that have been completely paid for and are not being pledged as collateral to support the purchase of other securities on margin. The term is relevant from a regulatory perspective as the SEC requires that U.S. broker dealers segregate and maintain in a good control location (e.g., DTC or bank) all customer securities which are fully paid. Such securities cannot be pledged or loaned to finance the activities of the firm or other customers.

Note that securities which were fully paid at the date of acquisition may later be reclassified as margin or excess margin securities based upon the customer's subsequent trade and/or borrowing activity. For example, if the loan value of fully paid securities is subsequently used to acquire additional securities on credit, a portion of securities will then be classified as margin securities and subject to a lien and potential pledge or hypothecation by the broker.

See also "excess margin securities".

Comparison of U.S. Segregation Models

INTRODUCTION

The regulation of securities and commodities products and brokers1 in the U.S. is administered by two distinct federal agencies, the Securities and Exchange Commission (SEC) for securities including stocks, ETFs, bonds, options and mutual funds and the Commodities Futures Trading Commission (CFTC) for commodities including futures and options on futures.2 While both agencies seek to safeguard customer assets by restricting their use and “segregating” them from assets of the broker, the regulations and manner in which they accomplish this differs. The following article provides a basic overview of two segregation models and additional considerations relating to IB accounts.

OVERVIEW

Differences between the CFTC and SEC segregation models originate largely from the products themselves, whose characteristics are fundamentally unique. Commodity products, by nature, do not involve an extension of credit by the broker to the customer as a futures contract is not an asset but rather a contingent liability which is marked-to-market and a long futures option, while an asset, must be paid for in-full. Consequently, non-option assets in a commodities account are generally comprised of funds deposited as margin to secure performance on the contracts therein. Since the broker may not use the funds of one customer to margin or guarantee the transactions of another, the commodities segregation requirement (CFTC Rules 1.20 – 1.30) is equal to the gross assets of all customers and the broker needs to add its own funds to segregation to cover customers whose net equity is in deficit.

A securities margin account, in contrast, can facilitate the extension of credit for the purpose of long securities (e.g., stocks, bonds) purchases or short securities sales on a secured basis. The segregation or reserve requirement rules recognize this through special provisions for the protection of each of the cash and securities components, further distinguishing fully-paid securities from those whose purchase the broker has financed and maintains a lien upon. Here, the broker must deposit into a separate bank account the net amount of customer cash balances3, in accordance with a formula set forth in SEC Rule 15c3-3. In addition, the broker must identify and segregate in a good control location (e.g., depository, bank) customer securities which meet the definition of “fully paid” or “excess margin”.

The table below provides a comparison of the main principals of each model.

| COMPARISON OF CFTC & SEC SEGREGATION MODELS | ||

| PRINCIPAL | CFTC | SEC |

|

Separation of Customer Balances

|

Commodity customer balances must be maintained separate from firm assets and cannot be used to finance proprietary business activities or to satisfy firm debts.

Funds used for trading on non-US commodity exchanges must be kept separate from those used for trading on U.S. exchanges (even for the same customer). Commodity customer balances must also be maintained separate from securities customer balances (even for the same customer). |

Securities customer balances must be maintained separate from firm assets and cannot be used to finance proprietary business activities or to satisfy firm debts. Securities customer balances must also be maintained separate from commodity customer balances (even for the same customer).

|

|

Priority in the Event of Broker Default

|

Commodity customers maintain priority and equal claim over assets in each of their respective U.S. segregated and non-U.S. secured pools.

No claim on assets in a commodity pool in which one is not a participant and no claim on securities customer assets. If commodity segregated assets are insufficient to meet claims and broker is insolvent, customers share equally in shortfall and become general creditors for residual claims. |

Securities customers maintain priority and equal claim over assets.4

No claim on commodity segregated assets. If securities segregated assets are insufficient to meet claims, broker is insolvent and claims exceed SPIC coverage, customers share equally in shortfall and become general creditors for residual claims.

|

| Segregation Style |

Gross – the broker may not use the funds of one customer to margin or guarantee the transactions of another and must segregate assets in an amount at least equal to the sum of all customer credit balances. |

Net – broker may use customer cash credit balances to finance, on a secured basis, margin loans to other customers and may lend or pledge a portion of customer securities purchased on margin to other customers selling short.

|

| Investment of Cash Balances |

Broker is allowed to reinvest commodity customer’s cash balances and retain an interest in the income generated. Permissible investments include: U.S. government securities, municipal securities, government sponsored enterprise securities, bank CDs, corporate obligations (commercial paper, notes and bonds) fully guaranteed as to principal and interest by the U.S. under the Temporary Liquidity Guarantee Program and money market mutual funds. Securities which are the subject of reinvestment must be maintained in a segregated account. |

Broker is allowed to reinvest securities customer’s cash balances and retain an interest in the income generated. Permissible investments limited to “qualified securities” defined as securities which are guaranteed as to both interest and principal by the U.S. government. Securities which are the subject of reinvestment must be held in Special Reserve Bank Account (i.e., segregated). |

| Computation Frequency | Daily | Weekly |

| Insurance | None | Securities Investor Protection Corporation (SIPC) provides insurance of up to USD 500,000 with a cash sublimit of USD 250,000. |

ADDITIONAL CONSIDERATIONS

In addition to the safeguards afforded through segregation, IB employs a number of policies and practices which serve to enhance the safety and security of accounts beyond that outlined above. These include the following:

- IB computes its securities segregation or reserve requirement on a daily rather than weekly basis as allowed by regulation, thereby ensuring timely determination as to the amount required to be reserved and the deposit of funds necessary to satisfy the requirement.

- IB’s does not avail itself of the generally more permissive rules with respect to the investment of commodity customer cash balances. These balances are instead invested in a manner similar to that of securities cash balances (i.e., U.S. government securities) with the exception of an occasional investment in money market funds.

- All customer securities positions are held in the securities segment of the Universal Account as opposed to the commodities (commodities margin met with cash and/or futures options), thereby limiting their hypothecation to the more restrictive rules of the SEC.

- In addition to SIPC coverage, IB maintains an excess SIPC policy with Lloyd's of London which, in aggregate with SIPC, offers insurance totaling $30 million (with a cash sublimit of $900,000), subject to an aggregate firm limit of $150 million.

- IB offers account holders the ability to sweep cash balances in excess of that required for margin purposes in either the securities or commodities segment to the other segment. Details as to this feature may be found in KB1851.

- For additional information regarding IB strength and security, please review the following website page.

Other Relevant Knowledge Base Articles:

Information Regarding SIPC Coverage

Footnotes:

1The term broker as used in this article is intended to refer to an organization registered with both the SEC as a Broker-Dealer and the CFTC as a Futures Commission Merchant for the purpose of conducting customer transactions

2Single stock futures are a hybrid product jointly regulated by the SEC and CFTC and allowed to be carried in either account type.

3Including cash obtained through the use of customer securities such bank pledges or stock loans less cash required to finance customer transactions (e.g., stock borrows, customer fails to deliver of securities, or margin deposited for short option positions with OCC).

4Assets, or customer property, which securities customers share in proportion to their net equity claim, include cash, margin securities and fully-paid securities held in “street name”. IB does not hold securities in the customer’s name which are not considered bulk customer property.

如何獲得在線安全代碼卡

Overview:

在線安全代碼卡可供您在21天內臨時訪問賬戶和交易平臺。這是一種臨時解決方案,通常用於以下情形:

A. 設備暫時不在身邊。

B. 丟失了永久安全設備,要申請替換設備並需要在收到設備之前繼續訪問賬戶。

激活程序

1. 打开浏览器,前往ibkr.com

2. 点击登录

3. 输入用户名和密码,点击登录。输入从IBKR客户服务处获得的临时密码完成验证,再次点击登录

.png)

4. 从菜单栏点击设置>使用者设置。然后在安全框内点击安全登录系统1 旁的齿轮(配置)图标

5. 系统将会列出您使用者当前启用的所有安全设备。在列表下方,点击请求在线(临时)安全代码卡

6. 界面将显示您的在线安全卡。点击打印2

(1).png)

7. 确保卡片已完整打印并且内容清晰可辨。然后点击继续

8. 激活界面将会显示两个索引号码。请在在线安全卡上找到第一个索引号码,将其对应的三位代码输入卡值框内。然后用第二个索引号码进行相同操作,代码之间不要留空格。然后点击继续

9. 您将会看到一条确认信息,其中会注明此在线安全卡的到期日期。点击确认完成此程序.png)

注意

1. 如果使用的是旧版账户管理,请点击管理账户 > 安全 > 安全登录系统 > 安全设备

在点击继续确认前,请确保安全卡图片已成功保存到您的设备并且内容清晰可辨。

参考:

- KB1131:安全登录系统概述

- KB1943:请求替换数码安全卡+

- KB2636:安全设备相关信息与程序

- KB2481:如何在多个使用者之间共享安全登录设备

- KB2545:退出安全登录系统后如何重新加入

- KB975:如何将安全设备退回给IBKR

- KB2260:如何通过移动IBKR激活IB Key验证

- KB2895:多重双因素验证(M2FS)

- KB1861:安全设备费用信息

- KB69:临时密码有效期