Fees for Trading Warrants and Structured Products on Euronext

Overview:

Euronext's fee thresholds on structured products and how it impacts clients' trading, for both fixed and tiered commission models

Background:

Clients that place orders and trade for more than EUR 6'000 in Warrants and Structured Products will be charged a 2.5 basis points fee with a maximum of EUR 20.

The table below displays the exchange fees for warrants and structured products when trading on Euronext:

|

Product Group |

Fee |

Minimum per Trade |

Maximum per Trade |

|

Warrants & Structured Products – trade value up to EUR 6’000 |

0.00 |

N/A |

N/A |

|

Warrants & Structured Products – trade value more than EUR 6’000 |

2.50 bps |

N/A |

EUR 20 per Trade |

Calculations:

For Cost Plus (Tiered) Clients:

Example: Client wishes to trade structured products on Euronext for a total trade value of EUR 10’000.

Scenario A:

Trade value = EUR 10’000

Fee = 2.5 Bps

As the trade value is above EUR 6’000, the fee of 2.50 bps applies and therefore an additional EUR 2.50 will have to be paid for the trade.

Scenario B:

Order 1:

Trade Value = EUR 5’000

Fee = 0.00

Order 2:

Trade Value = EUR 5’000

Fee = 0.00

As the trade value of each trade is below EUR 6’000, no additional fees apply.

Note: This calculation does not impact clients on the Fixed commission schedule.

Дополнительная информация об использовании стоп-ордеров

На рынках США могут возникать периоды чрезвычайно высокой волатильности и смещения цен. Такие периоды могут быть как кратковременными, так и продолжительными. Стоп-ордера могут способствовать снижению цены и волатильности на рынке, а также могут приводить к исполнению по цене, которая сильно отличается от цены-триггера.

Инвесторы могут использовать стоп-ордера на продажу, чтобы защитить прибыль на случай снижения цены акции или ограничить убытки. Кроме того, если у Вас есть короткие позиции, то ограничить убытки на случай повышения цены можно с помощью стоп-ордера на покупку. Однако, поскольку после срабатывания стоп-ордер становится рыночным ордером, то в этом случае инвесторы сразу же подвергаются рискам обычных рыночных ордеров. В частности, в условиях волатильного рынка цена исполнения может быть значительно ниже или выше ожидаемой.

Хотя стоп-ордера являются полезным инструментом для отслеживания цены позиции, они также сопряжены с некоторыми рисками. Если Вы хотите размещать стоп-ордера, Вам следует учитывать следующие факторы:

· Стоп-цена не является гарантированной ценой исполнения. Когда цена на рынке достигает заданную стоп-цену, стоп-ордер становится рыночным ордером и должен быть исполнен быстро и в полном объеме по текущей рыночной цене. Поэтому итоговая цена исполнения может значительно отличаться от стоп-цены, заданной инвестором. Соответственно, хотя стоп-ордер, став рыночным, может быть исполнен быстро, в условиях волатильности цена исполнения и стоп-цена могут сильно расходиться.

· Стоп-ордера могут сработать из-за кратковременного резкого изменения цены. В периоды волатильности цена акции может значительно и резко измениться, вызвав срабатывание стоп-ордера (а позже цена может вернуться на прежний уровень). Инвесторы должны понимать, что если стоп-ордер срабатывает при данных условиях, то он может быть исполнен по нежелательной цене, и цена может стабилизироваться в течение того же дня.

· В периоды высокой волатильности стоп-ордера на продажу могут усилить падение цены. Активация стоп-ордеров на продажу может усилить тенденцию в сторону понижения цены. Если стоп-ордер на продажу сработал при резком падении цены, то он с большей вероятностью также будет исполнен по цене намного ниже стоповой.

· Снизить такие риски можно, установив для стоп-ордера "лимитную" цену. Когда цена на рынке достигает заданную стоп-цену, стоп-ордер с лимитной ценой ("стоп-лимит") становится лимитным. Лимитный ордер – это ордер на покупку или продажу ценной бумаги по цене не хуже, чем заданная (т.е. лимитная). Используя стоп-лимитный ордер вместо обычного стоп-ордера, инвестор получает дополнительную гарантию цены исполнения. Однако инвесторам также следует учитывать, что поскольку ордер на продажу не может быть исполнен по цене ниже (а в случае ордера на покупку – по цене выше), чем заданная лимитная цена, то существует вероятность, что ордер не будет исполнен. Лимитные ордера лучше использовать в случаях, когда цена исполнения важнее, чем скорость.

· Риски, связанные со стоп-ордерами, возрастают в периоды неликвидности на рынке или при открытии и закрытии биржи, когда рынки более волатильны. Этот фактор может быть особенно важен для неликвидных акций, т.к. их может быть еще сложнее продать при текущей цене на этот момент, и при высокой волатильности их цена может еще сильнее колебаться по сравнению с рынком. Клиентам рекомендуется ограничивать время, в течение которого может сработать стоп-ордер, чтобы предотвратить активацию ордера в период отсутствия ликвидности или близко к открытию или закрытию, когда рынки более волатильны. Также рекомендуется использовать в такие периоды другие типы ордеров.

· Поскольку стоп-ордера сопряжены с неотъемлемым риском, инвесторам рекомендуется сначала рассмотреть возможность достижения своих торговых целей с помощью других типов ордеров.

Исполнение рыночных ордеров

Клиентам рекомендуется при возможности использовать лимитные ордера вместо рыночных, т.к. рыночные ордера могут быть исполнены по более низким/высоким ценам, чем отображаемый на момент отправки ордера бид/аск, особенно в условиях волатильного рынка, в случае отправки крупных ордеров и ордеров с неликвидными инструментами. В целях защиты клиентов и IB от убытков, связанных с резким изменением цен, IB может отправить рыночный ордер клиента как "рыночный ордер с защитой", установив лимит исполнения в рамках спреда между бидом и аском. Хотя данный лимит устанавливается на таком уровне, чтобы найти оптимальное соотношение между гарантированным исполнением и риском, существует небольшая вероятность, что исполнение будет отложено или не произойдет.

Кроме того, в качестве меры защиты некоторые биржи устанавливают собственные ограничения на рыночные ордера на уровнях, которые могут быть более или менее строгими, чем в IB, что также может повлиять на скорость и вероятность исполнения ордера.

Добавление/удаление ликвидности

Overview:

Цель данной статьи - разъяснить биржевые сборы, а также плату за добавление/удаление ликвидности при раздельных комиссиях.

Принцип добавления или удаления ликвидности применим как к акциям, так и к опционам на акции/индексы. Влияние ордера на ликвидность зависит от того, является ли он реализуемым или нереализуемым.

Реализуемые ордера УСТРАНЯЮТ ликвидность.

Реализуемые ордера - это либо рыночные ордера, либо лимитные ордера на продажу/покупку с предельной ценой на уровне или выше/ниже рыночной.

1. Лимитная цена реализуемого ордера покупки находится на уровне аска или выше него.

2. Предельная цена реализуемого лимитного ордера продажи находится на уровне бида или ниже него.

Пример:

Текущий размер/цена АСКА (предложения) XYZ составляет 400 акций по 46.00. Вы вводите лимитный ордер на покупку 100 акций XYZ по 46.01. Этот ордер будет считаться реализуемым, поскольку он немедленно исполнится. Если на бирже установлен сбор за понижение ликвидности, то клиент должен будет его оплатить.

Нереализуемые ордера ДОБАВЛЯЮТ ликвидность.

Нереализуемые ордера являются лимитными ордерами на покупку/продажу с предельной ценой ниже/выше рыночной.

1. Предельная цена нереализуемого лимитного ордера покупки находится ниже аска.

2. Предельная цена нереализуемого лимитного ордера продажи находится выше бида.

Пример:

Текущий размер/цена АСКА (предложения) XYZ составляет 400 акций по 46.00. Вы вводите лимитный ордер на покупку 100 акций XYZ по 45.99. Данный ордер будет считаться нереализуемым, поскольку он разместится на рынке как лучший бид вместо того, чтобы сразу же исполниться.

Если кто-то отправит ордер, на основе которого ваш лимитный ордер покупки исполнится, и если будет доступен бонус за добавление ликвидности, то вы получите рибейт (ретроспективный вычет).

ПРИМЕЧАНИЯ:

1. На все счета, торгующие опционами, распространяются биржевые сборы или бонусы за устранение/добавление ликвидности.

2. Только отрицательные значения в графе устранения/добавления ликвидности на сайте IB являются рибейтами (возвратными бонусами).

https://www.interactivebrokers.com/ru/index.php?f=5492

Нереализуемые ордера являются лимитными ордерами на покупку/продажу с предельной ценой ниже/выше рыночной.

1. Предельная цена нереализуемого лимитного ордера покупки находится ниже аска.

2. Предельная цена нереализуемого лимитного ордера продажи находится выше бида.

Пример:

Текущий размер/цена АСКА (предложения) XYZ составляет 400 акций по 46.00. Вы вводите лимитный ордер на покупку 100 акций XYZ по 45.99. Данный ордер будет считаться нереализуемым, поскольку он разместится на рынке как лучший бид вместо того, чтобы сразу же исполниться.

Если кто-то отправит ордер, на основе которого ваш лимитный ордер покупки исполнится, и если будет доступен бонус за добавление ликвидности, то вы получите рибейт (ретроспективный вычет).

ПРИМЕЧАНИЯ:

1. На все счета, торгующие опционами, распространяются биржевые сборы или бонусы за устранение/добавление ликвидности.

2. Только отрицательные значения в графе устранения/добавления ликвидности на сайте IB являются рибейтами (возвратными бонусами).

https://www.interactivebrokers.com/ru/index.php?f=5492

Справка о комиссиях/сборах, действующих для акций и опционов, доступна по ссылке выше

IEX Discretionary Peg Order

Background:

IEX offers a Discretionary Peg™ (D-Peg™) order type which is a non-displayed order that is priced at either the National Best Bid (NBB for buys) or National Best Offer (NBO for sells). D-Peg™ orders passively rest on the book while seeking to access liquidity at a more aggressive price up to Midpoint of the NBBO, except when IEX determines that the quote is transitioning to less aggressive price

D-Peg™ combines elements of Midpoint Peg, Primary Peg, and traditional discretionary order types.

Information about slow and predictable changes in the NBBO are detected in IEX's Crumbling Quote Indicator and provides D-Peg™ orders with an instruction to stop seeking access to liquidity at a more aggressive price until the quote returns to a stable state.

How to Place a D-Peg Order

Please note, the IEX D-Peg order type is only available via the TWS version 961 and above. Instructions for entering this order type are outlined below:

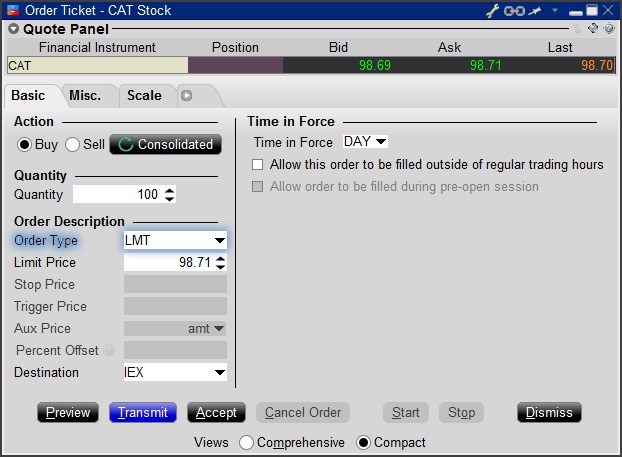

Step 1

Enter a symbol and choose a directed quote, selecting IEX as the destination. Right click on the data line and select Trade followed by Order Ticket to open the Order Ticket window.

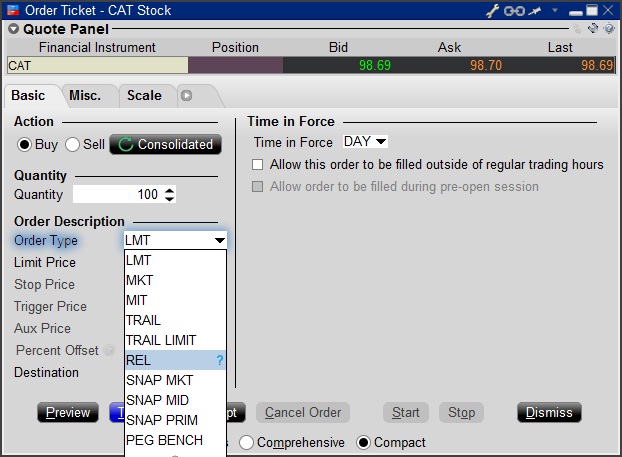

Step 2

Select the REL order type from the Order Type drop down menu.

Step 3

Click on the Miscellaneous tab (Misc.) and at the bottom there will be a checkbox for "Discretionary up to limit". Check this box. The price that you set in the Limit Price field will be used at the discretionary price on the order.

.jpg)

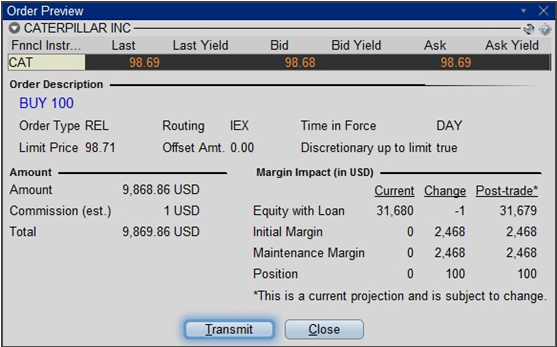

Step 4

Hit Preview to view the Order Preview window.

For additional information concerning this order type, please review the following exchange website link: https://www.iextrading.com/trading/dpeg/

Additional Information Regarding the Use of Stop Orders

U.S. equity markets occasionally experience periods of extraordinary volatility and price dislocation. Sometimes these occurrences are prolonged and at other times they are of very short duration. Stop orders may play a role in contributing to downward price pressure and market volatility and may result in executions at prices very far from the trigger price.

Investors may use stop sell orders to help protect a profit position in the event the price of a stock declines or to limit a loss. In addition, investors with a short position may use stop buy orders to help limit losses in the event of price increases. However, because stop orders, once triggered, become market orders, investors immediately face the same risks inherent with market orders – particularly during volatile market conditions when orders may be executed at prices materially above or below expected prices.

While stop orders may be a useful tool for investors to help monitor the price of their positions, stop orders are not without potential risks. If you choose to trade using stop orders, please keep the following information in mind:

· Stop prices are not guaranteed execution prices. A “stop order” becomes a “market order” when the “stop price” is reached and the resulting order is required to be executed fully and promptly at the current market price. Therefore, the price at which a stop order ultimately is executed may be very different from the investor’s “stop price.” Accordingly, while a customer may receive a prompt execution of a stop order that becomes a market order, during volatile market conditions, the execution price may be significantly different from the stop price, if the market is moving rapidly.

· Stop orders may be triggered by a short-lived, dramatic price change. During periods of volatile market conditions, the price of a stock can move significantly in a short period of time and trigger an execution of a stop order (and the stock may later resume trading at its prior price level). Investors should understand that if their stop order is triggered under these circumstances, their order may be filled at an undesirable price, and the price may subsequently stabilize during the same trading day.

· Sell stop orders may exacerbate price declines during times of extreme volatility. The activation of sell stop orders may add downward price pressure on a security. If triggered during a precipitous price decline, a sell stop order also is more likely to result in an execution well below the stop price.

· Placing a “limit price” on a stop order may help manage some of these risks. A stop order with a “limit price” (a “stop limit” order) becomes a “limit order” when the stock reaches or exceeds the “stop price.” A “limit order” is an order to buy or sell a security for an amount no worse than a specific price (i.e., the “limit price”). By using a stop limit order instead of a regular stop order, a customer will receive additional certainty with respect to the price the customer receives for the stock. However, investors also should be aware that, because a sell order cannot be filled at a price that is lower (or a buy order for a price that is higher) than the limit price selected, there is the possibility that the order will not be filled at all. Customers should consider using limit orders in cases where they prioritize achieving a desired target price more than receiving an immediate execution irrespective of price.

· The risks inherent in stop orders may be higher during illiquid market hours or around the open and close when markets may be more volatile. This may be of heightened importance for illiquid stocks, which may become even harder to sell at the then current price level and may experience added price dislocation during times of extraordinary market volatility. Customers should consider restricting the time of day during which a stop order may be triggered to prevent stop orders from activating during illiquid market hours or around the open and close when markets may be more volatile, and consider using other order types during these periods.

· In light of the risks inherent in using stop orders, customers should carefully consider using other order types that may also be consistent with their trading needs.

Hong Kong - China Stock Connect

Hong Kong – China Stock Connect (“China Connect”) is a mutual market access program through which Hong Kong and international investors can trade shares listed on the Shanghai Stock Exchange (SSE) and Shenzhen Stock Exchange (SZSE) via the Stock Exchange of Hong Kong (SEHK) and their existing clearinghouse. As a member of SEHK, IBKR provides you with direct access to trade with eligible listed products on the Shanghai and Shenzhen Stock Exchange. IBKR clients with China Connect trading permissions will be eligible to trade SSE/SZSE securities through Shanghai and Shenzhen - Stock Connect.

Among the different types of SSE/SZSE-listed securities, only A shares (shares in mainland China-based companies that trade on Chinese stock exchange) are included in the Shanghai and Shenzhen Stock Connect.

Shanghai Connect includes all the constituent stocks of the SSE 180 Index, SSE 380 Index and all the SSE-listed A shares that have corresponding H shares listed on the SEHK.

Product List and Stock Codes for SSE

Shenzhen Connect includes all the constituent stocks of the SZSE Component Index, the SZSE Small/Mid Cap Innovation Index that have a market capitalization of not less than RMB 6 billion and all the SZSE-listed A shares that have corresponding H shares listed on SEHK.

Product List and Stock Codes for SZSE

IBKR Commission for Trading SSE/SZSE Securities

Same as trading Hong Kong stocks, IBKR charges only 0.08% of trade value as a commission with a minimum CNH 15 per order. Detailed fee rates can be found in the Hong Kong – China Stock Connect Northbound fee table.

Daily Quota

Trading under Shanghai Connect and Shenzhen Connect is subject to a Daily Quota. The Daily Quota is applied on a “net buy” basis. The Daily Quota limits the maximum net buy value of cross-boundary trades under Shanghai Connect and Shenzhen Connect each day.

If the Northbound Daily Quota Balance drops to zero or the Daily Quota is exceeded during the opening call auction session, new buy orders will be rejected. Or if it happens during a continuous auction session or closing call auction session, no further buy orders will be accepted for the remainder of the day. SEHK will resume the Northbound buying service on the following trading day.

SEHK will also publish the remaining balance of the Aggregate Quota and Daily Quota.

For details, please refer to HKEX Stock Connect FAQ or HKEX Stock Connect Rule 1407

Trading Information of Shanghai and Shenzhen Connect

|

Trading currency |

RMB |

|

Order Type |

IBKR offers various order types but will stimulate the order into limit order for execution. More information can be referred to our website.

|

|

Tick Size / Spread |

Uniform at RMB 0.01 |

|

Board Lot |

100 shares (applicable for buyers only) |

|

Odd Lot |

Sell orders only (odd lot should be made in one single order) |

|

Max Order Size |

1 million shares |

|

Price Limit |

±10% on previous closing price (±5% for stocks under special treatment under risk alert, i.e. ST and *ST stocks) |

|

Day (Turnaround) Trading |

Not allowed |

|

Block Trade |

Not available |

|

Manual Trade |

Not available |

|

Order Modification |

IBKR will cancel and replace the order for any order modification |

|

Settlement cycle |

Securities: Settlement on T day Cash from China Connect trades: Settlement on T+1 day Forex*: Settlement on T+2 day |

*Due to the unsynchronized settlement cycle, clients who exchange CNH themselves should execute the Forex trade one day prior to the stock trade (T-1) to avoid the extra day’s interest payment (considering normal settlement without involving holidays).

Trading Hours

|

SSE/SZSE Trading Sessions |

SSE/SZSE Trading Hours |

|

Opening Call Auction |

09:15 - 09:25 |

|

Continuous Auction (Morning) |

09:30 – 11:30 |

|

Continuous Auction (Afternoon) |

13:00 – 14:57 |

|

Closing Call Auction |

14:57 – 15:00 |

Half-day Trading

If a Northbound trading day is a half-trading day in the Hong Kong market, it will continue until respective Connect Market is closed. Refer to the exchange website for holiday trading arrangements and additional information.

Disclosure Obligation

If client holds or controls up to 5% of the issued shares of China Connect, the client is required to report in writing to the China Securities Regulatory Commission (“CSRC”) and the relevant exchange, and inform the Mainland listed company within three working days of reaching 5%.

The client is not allowed to continue purchasing or selling shares in that Mainland listed company during the three days notification period. Visit the IBKR Knowledge Base for more information.

Shareholding Restriction

A single foreign investor’s shareholding in a Mainland listed company is not allowed to exceed 10% of the company’s total issued shares, while all foreign investors’ shareholding in the A shares of the listed company is not allowed to exceed 30% of its total issued shares. Visit the IBKR Knowledge Base for more information.

Forced-sale Arrangement

Each IBKR client is not allowed to hold more than a specific percentage of the China Connect listing company's total issued shares. HKEX requires the client to follow the forced-sell requirements if the shares exceed the limit:

|

Situation |

Shareholding (in a listed company) |

|

A single foreign investor |

> = 10% of the company’s total issued shares |

|

All foreign investors |

> = 30% of the company’s total issued shares |

Margin Financing

Margin trading in China Connect securities will subject to restrictions and only certain A shares will be eligible for margin trading. Eligible Securities, as determined by SSE and SZSE from time to time, are listed on the HKEX website.

According to the relevant rules of SSE and SZSE, either market may suspend margin trading activities in specific A shares when the volume of margin trading activities for a specific A share exceeds the prescribed threshold. The market will resume margin trading activities in the affected A share when its volume drops below a prescribed threshold.

Stock Borrowing and Lending (SBL)

SBL in China Stock Connect Securities is subject to restrictions set by the SSE or SZSE and stated in the Rules of the Exchange.

IBHK does not offer this service at the moment.

Eligible Short Selling Securities

SBL for the purpose of short selling will be limited to those China Stock Connect Securities that are eligible for both buy orders and sell orders through Shanghai and Shenzhen Connect (i.e., excluding Connect Securities that are only eligible for sell orders).

IBHK does not offer this service at the moment.

Trading Shenzhen ChiNext and Shanghai Star shares

Trading Shenzhen ChiNext and Shanghai Star shares are limited to institutional professional investors.

Holidays

Clients will only be allowed to trade China Connect on days where Hong Kong and Mainland markets are both open for trading and banking services are available in both Hong Kong and Mainland markets on the corresponding settlement days. This arrangement is essential in ensuring that investors and brokers will have the necessary banking support on the relevant settlement days when they will be required to make payments.

The following table illustrates the holiday arrangement of Northbound trading of SSE/SZSE Securities:

|

|

Mainland |

Hong Kong |

Open for Northbound Trading |

|

Day 1 |

Business Day |

Business Day |

Yes |

|

Day 2 |

Business Day |

Business Day |

No, HK market closes on money settlement day |

|

Day 3 |

Business Day |

Public Holiday |

No, HK market closes on trading day |

|

Day 4 |

Public Holiday |

Business Day |

No, Mainland market closes |

Severe Weather Conditions

Information on the trading arrangement available under severe weather conditions can found on the HKEx website.

Where to Learn More?

Please refer to the following exchange website links for additional information regarding Hong Kong China Stock Connect:

If you have any questions regarding Hong Kong-China Stock Connect, please contact IBKR Client Services for further information.

IPO Considerations

An Initial Public Offering, or IPO, is defined as the first sale of stock by a company to the public. As IB generally does not operate as an underwriter or selling agent of IPO shares, the first opportunity customers have to transact in such shares does not take place until the issue begins trading in the secondary market. Outlined below are key issues which customers should consider when transacting in shares on their first day of listing:

1. Margin

As IPOs are inherently subject to a high degree of uncertainty as to price and liquidity once secondary market trading begins, each new issue is subject to a review to determine whether initial and maintenance margin requirements above the minimum which is required by regulation is warranted. Current margin information is made available through the "Check Margin" feature on the trading platform. Customers should also note that IB reserves the right to change margin on an intraday basis and without advance notice when warranted.

2. Order Entry

IB monitors for upcoming IPOs and makes every effort to provide customers the ability to enter orders in advance of the day at which trading begins in the secondary market. In certain circumstances, either IB and/or the exchange may impose restrictions on the type of orders which may be accepted as well as the time in force conditions associated with such orders. It should also be noted that orders not direct-routed to the primary exchange may be subject to special auction handling and therefore may receive a different opening print from that of the primary exchange. In addition, as the price at which the issue trades once available in the secondary market may differ significantly from the IPO price, customers are strongly encouraged to use limit orders when.

3. Short Availability

Customers should assume that IPO issues will not be available for shorting immediately upon trading in the secondary market. This limitation is a function of regulations which require the broker to locate and make a good faith determination that shares are available to borrow at settlement coupled with the likelihood that such shares will not be available (due to underwriter lending restrictions and the fact that secondary market transactions have not yet settled).

How to Place a CFD Trade on the Trader Workstation

How to place trades in U.K. CFDs on the Trader Workstation