Order Preview - Check Exposure Fee Impact

IB provides a feature which allows account holders to check what impact, if any, an order will have upon the projected Exposure Fee. The feature is intended to be used prior to submitting the order to provide advance notice as to the fee and allow for changes to be made to the order prior to submission in order to minimize or eliminate the fee.

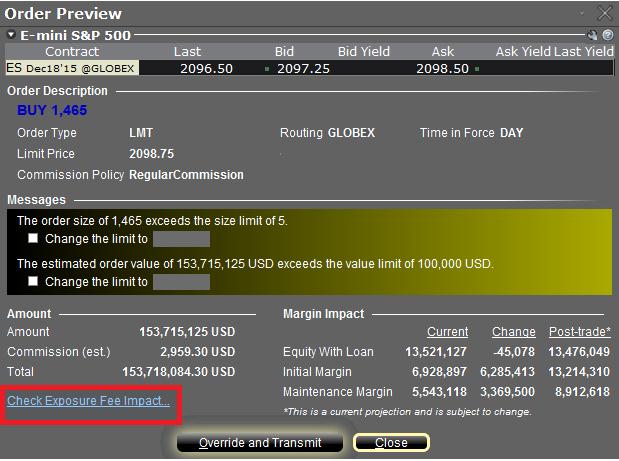

The feature is enabled by right-clicking on the order line at which point the Order Preview window will open. This window will contain a link titled "Check Exposure Fee Impact" (see red highlighted box in Exhibit I below).

Exhibit I

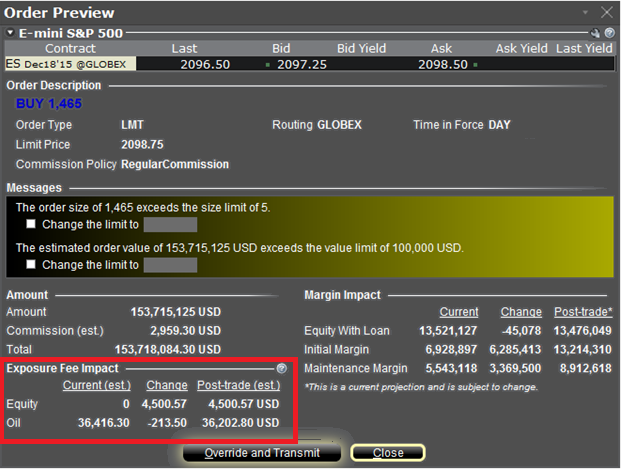

Clicking the link will expand the window and display the Exposure fee, if any, associated with the current positions, the change in the fee were the order to be executed, and the total resultant fee upon order execution (see red highlighted box in Exhibit II below). These balances are further broken down by the product classification to which the fee applies (e.g. Equity, Oil). Account holders may simply close the window without transmitting the order if the fee impact is determined to be excessive.

Exhibit II

Please see KB2275 for information regarding the use of IB's Risk Navigator for managing and projecting the Exposure Fee and KB2344 for monitoring fees through the Account Window

Important Notes

1. The Estimated Next Exposure Fee is a projection based upon readily available information. As the fee calculation is based upon information (e.g., prices and implied volatility factors) available only after the close, the actual fee may differ from that of the projection.

2. The Check Exposure Fee Impact is only available for accounts that have been charged an exposure fee in the last 30 days

Tools Provided to Monitor and Manage Margin

IB provides a variety of tools and information intended to provide account holders with real-time details as to their state of margin compliance so as to avoid forced liquidations. These include the following:

a. Account Window – The account window is available for real-time account activity monitoring. This window will display key values that update with every price change in the portfolio. Included are account balances (cash, Net Liquidation Value, Equity with Loan Value), margin requirements (current, look ahead, overnight and post expiration), and balances available for trading (Available Funds and Excess Equity).

b. Preview Order/Check Margin – Prior to transmitting an order it can be previewed including the impact upon the margin requirement were the order to be executed. Additional information may be found in KB644.

c. Communications – IB will act to send out communications via TWS bulletin and/or email when the margin cushion in an account reaches 10% and a margin deficiency is therefore approaching. Account holders may also create their own margin alerts based upon the margin cushion which, when triggered, may generate email or text message alerts, TWS pop-up messages and flashing rows, and sound alarms.

d. Reports – A Daily Margin Report is made available with Account Management which reflects key margin balances and for portfolio margin accounts, requirements broken down by security class.

In addition, IB provides a Last to Liquidate feature within the TWS Account window that allows customers to specify the positions they would prefer IB liquidate last in the event of a margin deficit. While IB will attempt on a best efforts basis to adhere to such requests, account positions and market conditions may make doing so impractical and IB therefore reserves the right to liquidate in the sequence it deems most optimal.

Trading on margin in an IRA account

IRA accounts, by definition, may not use borrowed funds to purchase securities and must pay for all long stock purchases in full, may not carry short stock positions and may not hold a debit cash balance (in any currency). IRA accounts are eligible to carry futures and option contracts. In addition, IB offers a specific form of IRA account referred to as a “Margin IRA” that allows the account holder to trade with unsettled funds, carry American style option spreads and maintain long balances in multiple currency denominations.

For additional information regarding trading permissions in an IRA account, refer to KB188.

How to determine if you are borrowing funds from IBKR

If the aggregate cash balance in a given account is a debit, or negative, then funds are being borrowed and the loan is subject to interest charges. A loan may still exist, however, even if the aggregate cash balance is a credit, or positive, as a result of balance netting or timing differences. The most common examples of this are as follows:

1. Long vs. Short Currency Balances – accounts holders may borrow cash denominated in one currency if it can be secured by a credit balance in another. Take, for example, a USD base currency account holding a long USD settled cash balance of 10,000, a short EUR settled cash balance of 5,000, with a EUR.USD exchange rate of 1.38:1. Here, for statement reporting and interest computation purposes, the overall cash balance is a USD credit of 3,088 (10,000 – (5,000 * 1.38)). As each currency is subject to a unique funding and reinvestment arrangement, the short balance would be subject to financing costs based upon its benchmark rate and tier. This cost may be offset by any interest earned on the long balance based upon its benchmark rate and tier.

2. Gross Balances by Segment – IBKR’s Universal Account contains multiple sub accounts or segments, each of which holds positions and collateral which, for regulatory and customer protection purposes, may not be commingled. This separation does not allow for netting of balances across segments and a credit in one segment may therefore not offset a debit in another. Take, for example, an IBLLC account holding both securities and commodities positions with the securities segment maintaining a debit cash balance of USD 3,000 and the commodities segment a credit cash balance of USD 8,000. While the account holds an overall net credit balance of USD 5,000, the short balance would be subject to an interest charge which may be partially offset by any interest earned on the long balance.

3. Short Sales – a short sale is a margin transaction in which the account holder is borrowing stock rather than cash. While the proceeds from the short sale are credited to the cash balance of the account, these funds must be posted with the lender of the shares as collateral to secure their return. As a result, and in recognition of the fact that the loan transaction is subject to its own financing terms, the cash collateralizing the loan is excluded for the purpose of determining whether a margin loan exists.

As example, consider an account reporting net liquidating equity (all balances in USD) of 9,000 comprised of a credit cash balance of 4,000, long stock valued at 10,000 and short stock valued at 5,000. In order to determine whether funds are being borrowed to finance the long stock position, the 5,000 portion of the cash pledged as collateral to the lender of the shares is deducted from the overall 4,000 cash balance, resulting in a 1,000 debit. This debit is subject to interest charges and the cash underlying the stock borrow either an interest charge in the case of hard to borrow shares or a short stock rebate if the shares are easy to borrow and reinvestment rates sufficiently high.

4. Unsettled Funds - borrowings are determined based upon settled funds and the time frame by which payment is due or received for a given transaction is product specific (e.g., stocks generally settle in 3 business days, spot currencies 2 and derivatives 1). For statement and trading platform purposes, cash balances are reported on a trade date rather than settlement date basis, as if settlement has completed.

As a result, an account reporting a credit cash balance may, in fact, still be carrying a margin loan if that balance includes proceeds from the sale of stock purchased with borrowed funds awaiting settlement. Similarly, an account may report a trade date based debit balance, but not yet incurring a margin loan and interest charges, as the trade has not yet settled.

For additional information regarding interest calculations, please refer to How Interest is Calculated.

Overview of Margin Methodologies

Introduction

The methodology used to calculate the margin requirement for a given position is largely determined by the following three factors:

1. The product type;

2. The rules of the exchange on which the product is listed and/or the primary regulator of the carrying broker;

3. IBKR’s “house” requirements.

While a number of methodologies exist, they tend to be categorized into one of two approaches: rules based or risk based. Rules based methods generally assume uniform margin rates across like products, offer no inter-product offsets and consider derivative instruments in a manner similar to that of their underlying. In this sense, they offer ease of computation but oftentimes make assumptions which, while simple to execute, may overstate or understate the risk of an instrument relative to its historic performance. A common example of a rules based methodology is the U.S. based Reg. T requirement.

In contrast, risk based methodologies often seek to apply margin coverage reflective of the product’s past performance, recognize some inter-product offsets and seek to model the non-linear risk of derivative products using mathematical pricing models. These methodologies, while intuitive, involve computations which may not be easily replicable by the client. Moreover, to the extent that their inputs rely upon observed market behavior, may result in requirements that are subject to rapid and sizable fluctuation. Examples of risk based methodologies include TIMS and SPAN.

Regardless of whether the methodology is rules or risk based, most brokers will apply “house” margin requirements which serve to increase the statutory, or base, requirement in targeted instances where the broker’s view of exposure is greater than that which would satisfied solely by meeting that base requirement. An overview of the most common risk and rules based methodologies is provided below.

Methodology Overview

Risk Based

a. Portfolio Margin (TIMS) – The Theoretical Intermarket Margin System, or TIMS, is a risk based methodology created by the Options Clearing Corporation (OCC) which computes the value of the portfolio given a series of hypothetical market scenarios where price changes are assumed and positions revalued. The methodology uses an option pricing model to revalue options and the OCC scenarios are augmented by a number of house scenarios which serve to capture additional risks such as extreme market moves, concentrated positions and shifts in option implied volatilities. In addition, there are certain securities (e.g., Pink Sheet, OTCBB and low cap) for which margin may not be extended. Once the projected portfolio values are determined at each scenario, the one which projects the greatest loss is the margin requirement.

Positions to which the TIMS methodology is eligible to be applied include U.S. stocks, ETFs, options, single stock futures and Non U.S. stocks and options which meet the SEC’s ready market test.

As this methodology uses a much more complex set of computations than one that is rules based, it tends to more accurately model risk and generally offers greater leverage. Given its ability to offer enhanced leverage and that the requirements fluctuate and may react quickly to changing market conditions, it is intended for sophisticated individuals and requires minimum equity of $110,000 to initiate and $100,000 to maintain. Requirements for stocks under this methodology generally range from 15% to 30% with the more favorable requirement applied to portfolios which contain a highly diversified group of stocks which have historically exhibited low volatility and which tend to employ option hedges.

b. SPAN – Standard Portfolio Analysis of Risk, or SPAN, is a risk-based margin methodology created by the Chicago Mercantile Exchange (CME) that is designed for futures and future options. Similar to TIMS, SPAN determines a margin requirement by calculating the value of the portfolio given a set of hypothetical market scenarios where underlying price changes and option implied volatilities are assumed to change. Again, IBKR will include in these assumptions house scenarios which account for extreme price moves along with the particular impact such moves may have upon deep out-of-the-money options. The scenario which projects the greatest loss becomes the margin requirement. A detailed overview of the SPAN margining system is provided in KB563.

Rules Based

a. Reg. T – The U.S. central bank, the Federal Reserve Board, holds responsibility for maintaining the stability of the financial system and containing systemic risk that may arise in financial markets. It does this, in part, by governing the amount of credit that broker dealers may extend to customers who borrow money to buy securities on margin.

This is accomplished through Regulation T, or Reg. T as it is commonly referred, which provides for establishment of a margin account and which imposes the initial margin requirement and payment rules on certain securities transactions. For example, on stock purchases, Reg. T currently requires an initial margin deposit by the client equal to 50% of the purchase value, allowing the broker to extend credit or finance the remaining 50%. For example, an account holder purchasing $1,000 worth of securities is required to deposit $500 and allowed to borrow $500 to hold those securities.

Reg. T only establishes the initial margin requirement and the maintenance requirement, the amount necessary to continue holding the position once initiated, is set by exchange rule (25% for stocks). Reg. T also does not establish margin requirements for securities options as this falls under the jurisdiction of the listing exchange’s rules which are subject to SEC approval. Options held in a Reg.T account are also subject to a rules based methodology where short positions are treated like a stock equivalent and margin relief is provided for spread transactions. Finally, positions held in a qualifying portfolio margin account are exempt from the requirements of Reg. T.

Where to Learn More

Tools provided to monitor and manage margin

How to determine if you are borrowing funds from IBKR

Why does IBKR calculate and report a margin requirement when I am not borrowing funds?

Determining Buying Power

Buying power serves as a measurement of the dollar value of securities that one may purchase in a securities account without depositing additional funds. In the case of a cash account where, by definition, securities may not be purchased using funds borrowed from the broker and must be paid for in full, buying power is equal to the amount of settled cash on hand. Here, for example, an account holding $10,000 in cash may purchase up to $10,000 in stock.

In a margin account, buying power is increased through the use of leverage provided by the broker using cash as well as the value of stocks already held in the account as collateral. The amount of leverage depends upon whether the account is approved for Reg. T margin or Portfolio Margin. Here, a Reg. T account holding $10,000 in cash may purchase and hold overnight $20,000 in securities as Reg. T imposes an initial margin requirement of 50%, which translates to buying power of 2:1 (i.e., 1/.50). Similarly, a Reg. T account holding $10,000 in cash may purchase and hold on an intra-day basis $40,000 in securities given IB’s default intra-day maintenance margin requirement of 25%, which translates to buying power of 4:1 (i.e., 1/.25).

In the case of a Portfolio Margin account, greater leverage is available although, as the name suggests, the amount is highly dependent upon the make-up of the portfolio. Here, the requirement on individual stocks (initial = maintenance) generally ranges from 15% - 30%, translating to buying power of between 6.67 – 3.33:1. As the margin rate under this methodology can change daily as it considers risk factors such as the observed volatility of each stock and concentration, portfolios comprised of low-volatility stocks and which are diversified in nature tend to receive the most favorable margin treatment (e.g., higher buying power).

In addition to the cash examples above, buying power may be provided to securities held in the margin account, with the leverage dependent upon the loan value of the securities and the amount of funds, if any, borrowed to purchase them. Take, for example, an account which holds $10,000 in securities which are fully paid (i.e., no margin loan). Using the Reg. T initial margin requirement of 50%, these securities would have a loan value of $5,000 (= $10,000 * (1 - 0.50)) which, using that same initial requirement providing buying power of 2:1, could be applied to purchase and hold overnight an additional $10,000 of securities. Similarly, an account holding $10,000 in securities and a $1,000 margin loan (i.e., net liquidating equity of $9,000), has a remaining equity loan value of $4,000 which could be applied to purchase and hold overnight an additional $8,000 of securities. The same principles would hold true in a Portfolio Margin account, albeit with a potentially different level of buying power.

Finally, while the concept of buying power applies to the purchase of assets such as stocks, bonds, funds and forex, it does not translate in the same manner to derivatives. Most securities derivatives (e.g., short options and single stock futures) are not assets but rather contingent liabilities and long options, while an asset, are short-term in nature, considered a wasting asset and therefore generally have no loan value. The margin requirement on short options, therefore, is not based upon a percentage of the option premium value, but rather determined on the underlying stock as if the option were assigned (under Reg. T) or by estimating the cost to repurchase the option given adverse market changes (under Portfolio Margining).

Margin Treatment for Foreign Stocks Carried by a U.S. Broker

As a U.S. broker-dealer registered with the Securities & Exchange Commission (SEC) for the purpose of facilitating customer securities transactions, IB LLC is subject to various regulations relating to the extension of credit and margining of those transactions. In the case of foreign equity securities (i.e., non-U.S. issuer), Reg T. allows a U.S. broker to extend margin credit to those which either appear on the Federal Reserve Board's periodically published List of Foreign Margin Stocks, or are deemed to have a have a "ready market" under SEC Rule 15c3-1 or SEC no-action letter.

Prior to November 2012, "ready market" was deemed to include equity securities of a foreign issuer that are listed on what is now known as the FTSE World Index. This definition was based upon a 1993 SEC no-action letter and was premised upon the fact that, while there may not have been a ready market for such securities within the U.S., the securities could be readily resold in the applicable foreign market. In November of 2012, the SEC issued a follow-up no-action letter (www.sec.gov/divisions/marketreg/mr-noaction/2012/finra-112812.pdf) which expanded the population of foreign equity securities deemed to have a ready market to also include those not listed on the FTSE World Index provided that the following four conditions are met:

1. The security is listed on a foreign exchange located within a FTSE World Index recognized country, where the security has been trading on the exchange for at least 90 days;

2. Daily bid, ask and last quotations for the security as provided by the foreign listing exchange are made continuously available to the U.S. broker through an electronic quote system;

3. The median daily trading volume calculated over the preceding 20 business day period of the security on its listing exchange is either at least 100,000 shares or $500,000 (excluding shares purchased by the computing broker);

4. The aggregate unrestricted market capitalization in shares of the security exceed $500 million over each of the preceding 10 business days.

Note: if a security previously meeting the above conditions no longer does so, the broker is provided with a 5 business day window after which time the security will no longer be deemed readily marketable and must be treated as non-marginable.

Foreign equity securities which do not meet the above conditions, will be treated as non-marginable and will therefore have no loan value. Note that for purposes of this no-action letter foreign equity securities do not include options.

Low Capitalization Stocks

| Symbol | Description |

| CQC | CUESTA COAL LTD |

| UNS | UNILIFE CORP-CDI |

| GHC | GENERATION HEALTHCARE REIT D |

| CDG | CLEVELAND MINING CO LTD |

| THR | THOR MINING PLC-CDI |

| CXX | CRADLE RESOURCES LTD |

| MGN | MAGELLAN PETROLEUM CORP-CDI |

| MXQ | MAX TRUST |

| PXS | PHARMAXIS LTD |

| EGG | ENERO GROUP LTD |

| AFR | AFRICAN ENERGY RESOURCES-CDI |

| TTI | TRAFFIC TECHNOLOGIES LTD |

| GID | GI DYNAMICS INC-CDI |

| MLX | METALS X LTD |

| IRI | INTEGRATED RESEARCH LIMITED |

| RCU | REAL ESTATE CAPITAL PARTNERS |

| PAA | PHARMAUST LTD |

| AVQ | AXIOM MINING LTD |

| SUM | SUMATRA COPPER & GOLD-CDI |

| SHC | SUNSHINE HEART INC-CDI |

| MNZ | MNEMON LTD |

| FRC | FORTE CONSOLIDATED LTD |

| RVA | REVA MEDICAL INC - CDI |

| SCD | SCANTECH LIMITED |

| PGI | PANTERRA GOLD LTD |

| AKP | AUDIO PIXELS HOLDINGS LTD |

| KPR | KUPANG RESOURCES LTD |

| WCB | WARRNAMBOOL CHEESE & BUTTER |

| 307 | UP ENERGY DEVELOPMENT GROUP |

| 8096 | RUIFENG PETROLEUM CHEMICAL |

| 3777 | CHINA FIBER OPTIC NETWORK SY |

| 396 | HING LEE HK HOLDINGS LTD |

| 8372 | RUIFENG PETROLEUM CHEMICAL |

| 8376 | GLOBAL ENERGY RESOURCES INT |

| 702 | SINO OIL AND GAS HOLDINGS LT |

| 8286 | SHANXI CHANGCHENG MICROLIG-H |

| 3300 | CHINA GLASS HOLDINGS LTD |

| 355 | CENTURY CITY INTL |

| 399 | UNITED GENE HIGH-TECH GROUP |

| STRTECH | STERLITE TECHNOLOGIES LTD |

| INGERRAND | INGERSOLL-RAND INDIA LTD |

| KALPATPOW | KALPATARU POWER TRANSMISSION |

| IBSEC | INDIABULLS SECURITIES LTD |

| RELMEDIA | RELIANCE MEDIAWORKS LTD |

| KENNAMET | KENNAMETAL INDIA LIMITED |

| TBZ | TRIBHOVANDAS BHIMJI ZAVERI L |

| MAHINDFOR | MAHINDRA FORGINGS LTD |

| IVRCLINFR | IVRCL LTD |

| GOLDLEG | GOLDEN LEGAND LEASING & FIN |

| 8068 | RYOYO ELECTRO CORP |

| 2749 | JP-HOLDINGS INC |

| 2169 | CDS CO LTD |

| 3278 | KENEDIX RESIDENTIAL INVESTME |

| 1934 | YURTEC CORP |

| 3433 | TOCALO CO LTD |

| 4109 | STELLA CHEMIFA CORP |

| 1720 | TOKYU CONSTRUCTION CO LTD |

| 4775 | SOGO MEDICAL CO LTD |

| 6801 | TOKO INC |

Low Capitalization Stocks

| SYMBOL | DESCRIPTION |

| AFAB.B | ACANDO AB |

| ALPA | ALPCOT AGRO AB |

| AOILSDBPR | ALLIANCE OIL CO LTD-PREF |

| ARCM | ARCAM AB |

| EOS | EOS RUSSIA |

| GDWN | GOODWIN PLC |

| IMS1 | IMMSI SPA |

| KDEV | KAROLINSKA DEVELOPMENT-B |

| MSAB.B | MICRO SYSTEMATION AB-B |

| NETI.B | NET INSIGHT AB-B |

| NOMI | NORDIC MINES AB |

| PARE | PA RESOURCES AB. |

| PGD | PATAGONIA GOLD PLC |

| REG | RARE EARTHS GLOBAL LTD |

| RPO | RUSPETRO PLC |

| SHELB | SHELTON PETROLEUM AB |

| SWOL.B | SWEDOL AB-B |

| TAGR | TRIGON AGRI A/S |

| VPP | VALIANT PETROLEUM PLC |

Low Capitalization Stocks

Overview:

Please be advised that IB has increased the initial margin rates to 100% on low capitalization stocks (currently defined as companies with less than$250 million in market capitalization). The maintenance margin increases will occur in stages starting with an increase to 50% beginning after the EU market close on Friday, January 25th, 2013 and will be implemented as follows:

Monday January 28th, 2013: Maintenance Margin - 50%

Thursday January 31st,2013: Maintenance Margin - 75%

Tuesday February 2nd, 2013: Maintenance Margin - 100%

The list of stocks which are subject to this margin increase can be found on the following page:

Upon implementation, any of the incremental margin increases may result in a margin deficit in the account. A margin deficit implies that an account becomes subject to automated liquidation. Please carefully review the current positions within your account and adjust the portfolio accordingly.

Interactive Brokers Customer Service

| SYMBOL | DESCRIPTION |

| 02P | PEARL GOLD AG |

| 1PL | POWERLAND AG |

| 5MC | MOTRICITY INC |

| A2O | ALTONA MINING LTD |

| AAH3 | AHLERS AG PFD |

| ABL | ABLON GROUP |

| ABO | ABO INVEST AG |

| ACAN | ACANTHE DEVELOPPEMENT SA |

| ACD | ACENCIA DEBT STRATEGIES LTD |

| ADD | ADLER MODEMARKTE AG |

| ADI | AUDIKA GROUPE |

| AGX | AGENNIX AG |

| AJAX | AFC AJAX |

| ALC | A123 SYSTEMS INC |

| ALGLD | GOLD BY GOLD |

| ALS30 | SOLUTIONS 30 |

| AMC | AMUR MINERALS CORP |

| AMS | ADVANCED MEDICAL SOLUTIONS |

| APEF | ABERDEEN PRIVATE EQUITY FUND |

| AQU | GIGASET AG |

| ARG | ARGAN |

| ARN | ALERION CLEANPOWER |

| ATEB | ATENOR GROUP |

| AV.A | AVIVA PLC 8.75% PFD |

| BABE | BLUECREST ALLBLUE FUND LTD |

| BBN | BELLEVUE GROUP AG |

| BCRA | BACCARAT |

| BHGLE | BH GLOBAL LTD-EURO SHRS |

| BHUE | BLACKROCK HEDGE-UK EMERGING |

| BMP | BMP PHARMA TRADING AG |

| BMS | BRAEMAR SHIPPING SERVICES PL |

| BPC | BAHAMAS PETROLEUM CO PLC |

| BWB | BAADER BANK AG |

| CAMK | CAMKIDS GROUP PLC |

| CAML | CENTRAL ASIA METALS PLC |

| CARDG | LIFEWATCH AG-REG |

| CBAV | CLINICA BAVIERA SA |

| CEN | GROUPE CRIT |

| CGD | CEGID GROUP |

| CIB | TECNOCOM TELECOM Y ENERGIA |

| CIC | CONYGAR INVESTMENT CO PLC |

| CIRC | CIRCLE HOLDINGS LTD |

| CLIG | CITY OF LONDON INVESTMENT GR |

| CMBT | ATEVIA AG |

| CN9 | CIRCLE OIL PLC |

| CNP1 | CONAFI PRESTITO SPA |

| CRM | CARRS MILLING INDUSTRIES PL |

| CTH | CARETECH HOLDINGS PLC |

| CTN | CENTROTHERM PHOTOVOLTAICS AG |

| CU21 | CERUS CORP |

| DECB | DECEUNINCK NV |

| DES | DESIRE PETROLEUM PLC |

| DEVO | DEVOTEAM SA |

| DPT | S.T. DUPONT |

| DTL | DEXION TRADING LTD |

| EN6 | ECHELON CORP |

| ETG | ENVITEC BIOGAS AG |

| ETV | CONSTANTIN MEDIEN AG |

| EUCA | EUROMICRON AG |

| EXC1 | EXCEET GROUP SE |

| F2P | GLU MOBILE INC |

| FFY | FYFFES PLC |

| FFY | FYFFES PLC |

| FLO | GROUPE FLO |

| FM | FIERA MILANO SPA |

| FORE | LA FORESTIERE EQUATORIALE |

| FTON | FEINTOOL INTL HOLDING-REG |

| G6S | GENCO SHIPPING & TRADING LTD |

| GAL1S | 3W POWER SA |

| GBMN | GOLDBACH GROUP AG |

| GBO | GLOBO PLC |

| GDL | GREKA DRILLING LTD-DI |

| GDMS | GRANDS MOULINS DE STRASBOURG |

| GDWN | GOODWIN PLC |

| GEM | GEMFIELDS PLC |

| GFI | GFI INFORMATIQUE |

| GMC | GLOBAL MARKET GROUP LTD |

| GPX | GULFSANDS PETROLEUM PLC |

| GUR | GURIT HOLDING AG-BR |

| GYQ | FIRST DERIVATIVES PLC |

| HAMO | HAMON SA |

| HAT | H&T GROUP PLC |

| HEAD | HEAD N.V. |

| HIM | HI-MEDIA SA |

| HINS | HENDERSON INTERNATIONAL INCO |

| HNT | HUNTSWORTH PLC |

| HUE | HUEGLI HOLDING AG-BR |

| IBAB | ION BEAM APPLICATIONS |

| IBG | IBERPAPEL GESTION SA |

| ICLL | INTERCELL AG |

| IDH | IMMUNODIAGNOSTIC SYSTEMS HLD |

| IDIP | IDI |

| IFD | SCHRODER REAL ESTATE INVESTM |

| IFL | INTERNATIONAL FERRO METALS |

| IML | AFFINE |

| IMMO | IMMOBEL |

| IN0 | INPHI CORP |

| INM | INDEPENDENT NEWS & MEDIA PLC |

| INSD | INSIDE SECURE SA |

| IPEL | IMPELLAM GROUP PLC |

| ITMR | ITALMOBILIARE SPA-RSP |

| IUR | KAP-BETEILIGUNGS-AG |

| IX4 | IRIDEX CORP |

| JWB | JK WOHNBAU AG |

| KA | KAS BANK NV -CVA |

| KARN | KARDEX AG-REG |

| KMU | KLEMURS |

| LAC | LACIE SA |

| LBR | CUSTODIA HOLDING AG |

| LD | LOCINDUS |

| LKI | SEDO HOLDING AG |

| LLPE | LLOYDS BANKING GROUP PLC 6.475% NON-CUM |

| LN4 | LINEDATA SERVICES |

| LNA | LE NOBLE AGE |

| LSS | LECTRA |

| M5Z | MANZ AG |

| MBH3 | MASCH BERTHOLD HERMLE AG-VOR |

| MEO3 | METRO AG-VORZ |

| MF6 | MAGFORCE AG |

| MIRL | MINERA IRL LTD |

| MJT | MAJESTIC GOLD CORP. |

| MKEA | MAUNA KEA TECHNOLOGIES |

| MLD | MIRLAND DEVELOPMENT CORP |

| MOL | GRUPPO MUTUIONLINE SPA |

| MRB | MR BRICOLAGE |

| MSZN | COLTENE HOLDING AG-REG |

| MUB | MUEHLBAUER HOLDING AG & CO |

| MYRN | MYRIAD GROUP AG |

| NOP | NORTHERN PETROLEUM PLC |

| OFN | ORELL FUESSLI HOLDING AG-REG |

| ORANW | ORANJEWOUD NV |

| ORDN | ORDINA NV |

| OVXA | OVOCA GOLD PLC |

| PARP | GROUPE PARTOUCHE |

| PLAZ | PLAZA CENTERS NV |

| PMO | PRIME OFFICE REIT-AG |

| PNX | PHOENIX IT GROUP LTD |

| POL | POLO RESOURCES LTD |

| PRA | PRAKTIKER AG |

| PRS | PRELIOS SPA |

| PRT | ESPRINET SPA |

| PRW | PROMETHEAN WORLD PLC |

| PYT | POLYTEC HOLDING AG |

| RE. | R.E.A. HOLDINGS PLC |

| REA | REALDOLMEN |

| RECT | RECTICEL |

| REP | REPOWER AG-PC |

| RM. | RM PLC |

| RPT | REGAL PETROLEUM PLC |

| RSAB | RSA INSURANCE GROUP PLC 7 3/8% CUM IRRD PRF #1 |

| RSL1 | R STAHL AG |

| RWA | ROBERT WALTERS PLC |

| SAB | SABAF SPA |

| SBLM | SABLE MINING AFRICA LTD |

| SEPU | SEPURA LTD |

| SESL | STORE ELECTRONIC |

| SEY | STERLING ENERGY PLC |

| SFR | SEVERFIELD-ROWEN PLC |

| SHPN | SHAPE CAPITAL AG-REG |

| SII | SOCIETE POUR L'INFORMATIQUE |

| SIOE | SIOEN INDUSTRIES NV |

| SIV | ST.IVES PLC |

| SK1 | SKW STAHL-METALLURGIE HOLDIN |

| SMH | SUESS MICROTEC AG |

| SNBN | SCHWEIZERISCH NATIONALBA-REG |

| SNC3 | SANACORP PHARMAHOLDING-PFD |

| SNG | SINGULUS TECHNOLOGIES |

| SPI1 | SPIR COMMUNICATION |

| STAC | STANDARD CHARTERED PLC 8.25% NON-CUM PREF |

| STNT | STENTYS |

| STRN | STERN GROEP NV |

| SW1 | SHW AG |

| SWP | SWORD GROUP |

| TAM | ETAM DEVELOPPEMENT SA |

| TAN | TANFIELD GROUP PLC |

| TGH | LOGWIN AG |

| TGT | TELEGATE AG |

| TPET | TANGIERS PETROLEUM LTD |

| TPL | TETHYS PETROLEUM LTD |

| TPOE | THIRD POINT OFFSHORE INVESTM |

| TPOG | THIRD POINT OFFSHORE INVESTM |

| TPT | TOPPS TILES PLC |

| TRB | TRIBAL GROUP PLC |

| TV0 | TRAVEL VIVA AG |

| U6Z | URANIUM ENERGY CORP |

| UCC1 | URANIUM RESOURCES INC |

| UPL | ADVEO GROUP INTERNATIONAL SA |

| UTV | UTV MEDIA PLC |

| VBK | VERBIO AG |

| VCH | CHARLES VOEGELE HOLDING A-BR |

| VGAS | VOLGA GAS PLC |

| VIZ | VI[Z]RT LTD |

| VLS | VIVALIS SA |

| WFT | WENG FINE ART AG |

| WIMO | WITTE MOLEN NV |

| WMF3 | WMF- WUERTTEMBERG METAL- PRF |

| WSU | WASHTEC AG |

| ZAM | ZAMBEEF PRODUCTS PLC |