Présentation des méthodologies de calcul de marge

Présentation

La méthodologie utilisée pour calculer l'exigence de marge pour une position donnée est largement déterminée par les trois facteurs suivants :

1. Le type de produit ;

2. Le règlement de la bourse sur laquelle le produit est listé et/ou le régulateur principal du courtier ;

3. Les exigences internes d'IBKR.

Bien qu’il existe un certain nombre de méthodologies, elles ont tendance à être classées dans l’une des deux approches suivantes : basée sur les règles ou basée sur le risque. Les méthodes basées sur des règles supposent généralement des taux de marge uniformes sur des produits similaires, n’offrent aucune compensation inter-produits et prennent en considération les instruments dérivés d’une manière similaire à celle de leur sous-jacent. En ce sens, ils offrent une facilité de calcul mais font souvent des hypothèses qui, bien que simples à exécuter, peuvent surestimer ou sous-estimer le risque d’un instrument par rapport à sa performance historique. Un exemple courant de méthodologie basée sur des règles est l'exigence Reg. T.

En revanche, les méthodologies basées sur le risque cherchent souvent à appliquer une couverture de marge reflétant les performances passées du produit, à reconnaître certaines compensations inter-produits et à modéliser le risque non linéaire des produits dérivés à l’aide de modèles de tarification mathématiques. Ces méthodologies, bien qu’intuitives, impliquent des calculs qui peuvent ne pas être facilement reproductibles par le client. De plus, dans la mesure où leurs apports reposent sur le comportement observé sur le marché, cela peut entraîner des exigences sujettes à des fluctuations rapides et importantes. TIMS et SPAN sont des exemples de méthodologies basées sur le risque.

Que la méthodologie soit basée sur des règles ou sur le risque, la plupart des courtiers appliqueront des exigences de marge internes qui servent à augmenter l’exigence légale ou de base dans des cas ciblés où l’opinion du courtier sur l’exposition est supérieure à celle qui serait satisfaite uniquement en respectant cette exigence de base. Un aperçu des méthodologies basées sur les risques et les règles les plus courantes est fourni ci-dessous.

Présentation de la méthodologie

Basée sur le risque

a. Portfolio Margin (TIMS) – Le Theoretical Intermarket Margin System, ou TIMS, est une méthodologie basée sur le risque créée par l’Options Clearing Corporation (OCC) qui calcule la valeur du portefeuille en fonction d’une série de scénarios de marché hypothétiques où les changements de prix sont supposés et les positions réévaluées. La méthodologie utilise un modèle d’évaluation des options pour réévaluer les options et les scénarios OCC sont complétés par un certain nombre de scénarios internes qui servent à capturer des risques supplémentaires tels que les mouvements extrêmes du marché, les positions concentrées et les changements dans les volatilités implicites des options. De plus, il existe certains titres (par exemple, Pink Sheet, OTCBB et low cap) pour lesquels la marge peut ne pas être étendue. Une fois que les valeurs prévues du portefeuille sont déterminées à chaque scénario, celui qui prévoit la plus grande perte est l’exigence de marge.

Les positions auxquelles la méthodologie TIMS peut être appliquée comprennent les actions américaines, les ETF, les options, les SSF et les actions et options non américaines qui répondent au test ready market de la SEC.

Comme cette méthodologie utilise un ensemble de calculs beaucoup plus complexe qu’un ensemble basé sur des règles, elle a tendance à modéliser plus précisément le risque et offre généralement un effet de levier plus important. Compte tenu de sa capacité à offrir un effet de levier accru et du fait que les exigences fluctuent et peuvent réagir rapidement aux conditions changeantes du marché, il est destiné aux personnes averties et nécessite un capital minimum de 110 000 $ pour commencer et de 100 000 $ pour maintenir. Les exigences pour les actions selon cette méthodologie varient généralement de 15 % à 30 %, l’exigence la plus favorable étant appliquée aux portefeuilles qui constituent un groupe d’actions hautement diversifié qui ont historiquement affiché une faible volatilité et qui ont tendance à utiliser des couvertures d’options.

b. SPAN – Standard Portfolio Analysis of Risk, ou SPAN, est une méthodologie de marge basée sur le risque créée par le Chicago Mercantile Exchange (CME) qui est conçue pour les contrats à terme et les options sur contrat à terme. D’une façon similaire à TIMS, SPAN détermine une exigence de marge en calculant la valeur du portefeuille compte tenu d’un ensemble de scénarios de marché hypothétiques où les changements de prix sous-jacents et les volatilités implicites des options sont supposés changer. Encore une fois, IBKR inclura dans ces hypothèses des scénarios internes qui représente les mouvements extrêmes de prix ainsi que l’impact particulier que ces mouvements peuvent avoir sur les options profondément hors du cours. Le scénario qui projette la plus grande perte devient l’exigence de marge. Un aperçu détaillé du système de marge SPAN est fourni dans KB563.

Basée sur les règles

a. Reg. T – La banque centrale américaine, le Federal Reserve Board, a la responsabilité de maintenir la stabilité du système financier et de contenir le risque systémique pouvant survenir sur les marchés financiers. Pour ce faire, elle régit en partie le montant du crédit que les courtiers peuvent accorder aux clients qui empruntent de l’argent pour acheter des titres sur marge.

Ceci est accompli par Regulation T, or Reg. T comme on l’appelle communément, qui prévoit la constitution d’un compte sur marge et qui impose l’exigence de marge initiale et des règles de paiement sur certaines opérations sur titres. Par exemple, sur les achats d’actions, Reg. Par exemple, sur les achats d’actions, Reg. T exige actuellement un dépôt initial de marge par le client égal à 50 % de la valeur d’achat, permettant au courtier d’étendre le crédit ou de financer les 50 % restants. Par exemple, un détenteur de compte qui achète pour 1 000 $ de titres est tenu de déposer 500 $ et autorisé à emprunter 500 $ pour détenir ces titres.

Reg. T établit uniquement l’exigence de marge initiale et l’exigence de maintien, le montant nécessaire pour continuer à détenir la position une fois initiée, est fixée par la règle de Bourse (25 % pour les actions). Reg. T n’établit pas non plus d’exigences de marge pour les options car cela relève de la compétence des règles de la bourse de cotation qui sont soumises à l’approbation de la SEC. Les options détenues dans un compte Reg. T sont également soumises à une méthodologie basée sur des règles dans laquelle les positions à découvert sont traitées comme un équivalent d’actions et un allègement de marge est prévu pour les transactions de spread. Enfin, les positions détenues dans un Portfolio Margin éligible sont exemptées des exigences de Reg. T.

Pour en apprendre plus

Définitions importantes concernant la marge

Outils fournis pour surveiller et gérer la marge

Comment déterminer si vous emprunter des fonds à IBKR

Pourquoi IBKR calcule et signale une exigence de marge quand je n'emprunte pas de fonds ?

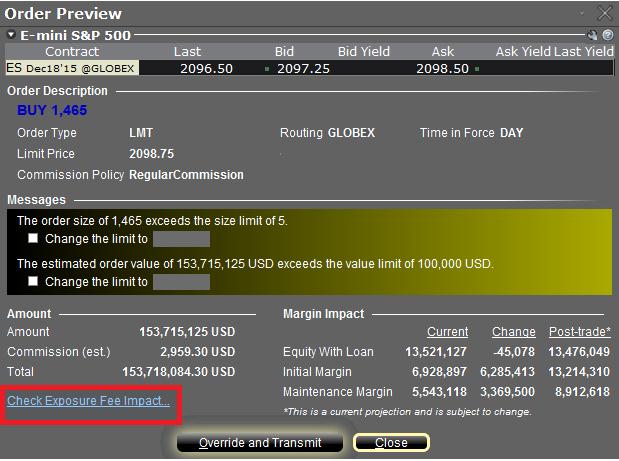

Order Preview - Check Exposure Fee Impact

IB provides a feature which allows account holders to check what impact, if any, an order will have upon the projected Exposure Fee. The feature is intended to be used prior to submitting the order to provide advance notice as to the fee and allow for changes to be made to the order prior to submission in order to minimize or eliminate the fee.

The feature is enabled by right-clicking on the order line at which point the Order Preview window will open. This window will contain a link titled "Check Exposure Fee Impact" (see red highlighted box in Exhibit I below).

Exhibit I

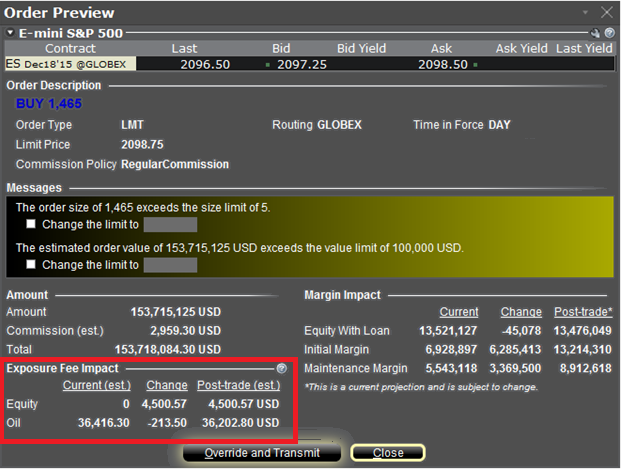

Clicking the link will expand the window and display the Exposure fee, if any, associated with the current positions, the change in the fee were the order to be executed, and the total resultant fee upon order execution (see red highlighted box in Exhibit II below). These balances are further broken down by the product classification to which the fee applies (e.g. Equity, Oil). Account holders may simply close the window without transmitting the order if the fee impact is determined to be excessive.

Exhibit II

Please see KB2275 for information regarding the use of IB's Risk Navigator for managing and projecting the Exposure Fee and KB2344 for monitoring fees through the Account Window

Important Notes

1. The Estimated Next Exposure Fee is a projection based upon readily available information. As the fee calculation is based upon information (e.g., prices and implied volatility factors) available only after the close, the actual fee may differ from that of the projection.

2. The Check Exposure Fee Impact is only available for accounts that have been charged an exposure fee in the last 30 days

Using Risk Navigator to Project Exposure Fees

Overview:

IB's Risk Navigator provides a custom scenario feature which allows one to determine what effect, if any, changes to their portfolio will have to the Exposure fee. Outlined below are the steps for creating a “what-if” portfolio through assumed changes to an existing portfolio or through an entirely new proposed portfolio along with determining the resultant fee. Note that this feature is available through TWS build 971.0i and above.

Step 1: Open a new “What-if” portfolio

From the Classic TWS trading platform, select the Analytical Tools, Risk Navigator, and then Open New What-If menu options (Exhibit 1).

Exhibit 1

.png)

From the Mosaic TWS trading platform, select the New Window, Select Risk Navigator, and then Open New What-If menu options.

Step 2: Define starting portfolio

A pop-up window will appear (Exhibit 2) from which you will be prompted to define whether you would like to create a hypothetical portfolio starting from your current portfolio or a newly created portfolio. Clicking on the "yes" button will serve to download existing positions to the new “What-If” portfolio.

Exhibit 2

.png)

Clicking on the "No" button will open up the “What-If” Portfolio with no positions.

Step 3: Add Positions

To add a position to the “what-if” portfolio, click on the green row titled "New" and then enter the underlying symbol (Exhibit 3), define the product type (Exhibit 4) and enter position quantity (Exhibit 5).

Exhibit 3

.png)

Exhibit 4

.png)

Exhibit 5

.png)

You can modify the positions to see how that changes the margin. After you altered your positions you will need to click on the recalculate icon ( ) to the right of the margin numbers in order to have them update. Whenever that icon is present the margin numbers are not up-to-date with the content of the “what-if” Portfolio.

) to the right of the margin numbers in order to have them update. Whenever that icon is present the margin numbers are not up-to-date with the content of the “what-if” Portfolio.

Step 4: Determine Exposure Fee

To view the projected correlated exposure fee based upon your “what-if” portfolio, click on the Report and then Exposure Fee menu options (Exhibit 6). Once selected, a new Exposure Fee tab will be added, which will display the projected exposure fee broken down by primary risk factors (Exhibit 7).

Exhibit 6

.png)

Exhibit 7

.png)

You can modify the positions to see how that changes the Exposure Fee. After you altered your positions you will need to click on the refresh button to the right of the Last Calculation Time. Whenever the warning icon ( ) is present the Exposure Fee Calculations numbers are not up-to-date with the content of the “what-if” Portfolio.

) is present the Exposure Fee Calculations numbers are not up-to-date with the content of the “what-if” Portfolio.

Please see KB2344 for information on monitoring the Exposure fee through the Account Window and KB2276 for verifying exposure fee through the Order Preview screen.

Important Note

1. The on-demand Exposure Fee check represents a projection based upon readily available information. As the fee calculation is based upon information (e.g., prices and implied volatility factors) available only after the close, the actual fee may differ from that of the projection.

Overview of Margin Methodologies

Introduction

The methodology used to calculate the margin requirement for a given position is largely determined by the following three factors:

1. The product type;

2. The rules of the exchange on which the product is listed and/or the primary regulator of the carrying broker;

3. IBKR’s “house” requirements.

While a number of methodologies exist, they tend to be categorized into one of two approaches: rules based or risk based. Rules based methods generally assume uniform margin rates across like products, offer no inter-product offsets and consider derivative instruments in a manner similar to that of their underlying. In this sense, they offer ease of computation but oftentimes make assumptions which, while simple to execute, may overstate or understate the risk of an instrument relative to its historic performance. A common example of a rules based methodology is the U.S. based Reg. T requirement.

In contrast, risk based methodologies often seek to apply margin coverage reflective of the product’s past performance, recognize some inter-product offsets and seek to model the non-linear risk of derivative products using mathematical pricing models. These methodologies, while intuitive, involve computations which may not be easily replicable by the client. Moreover, to the extent that their inputs rely upon observed market behavior, may result in requirements that are subject to rapid and sizable fluctuation. Examples of risk based methodologies include TIMS and SPAN.

Regardless of whether the methodology is rules or risk based, most brokers will apply “house” margin requirements which serve to increase the statutory, or base, requirement in targeted instances where the broker’s view of exposure is greater than that which would satisfied solely by meeting that base requirement. An overview of the most common risk and rules based methodologies is provided below.

Methodology Overview

Risk Based

a. Portfolio Margin (TIMS) – The Theoretical Intermarket Margin System, or TIMS, is a risk based methodology created by the Options Clearing Corporation (OCC) which computes the value of the portfolio given a series of hypothetical market scenarios where price changes are assumed and positions revalued. The methodology uses an option pricing model to revalue options and the OCC scenarios are augmented by a number of house scenarios which serve to capture additional risks such as extreme market moves, concentrated positions and shifts in option implied volatilities. In addition, there are certain securities (e.g., Pink Sheet, OTCBB and low cap) for which margin may not be extended. Once the projected portfolio values are determined at each scenario, the one which projects the greatest loss is the margin requirement.

Positions to which the TIMS methodology is eligible to be applied include U.S. stocks, ETFs, options, single stock futures and Non U.S. stocks and options which meet the SEC’s ready market test.

As this methodology uses a much more complex set of computations than one that is rules based, it tends to more accurately model risk and generally offers greater leverage. Given its ability to offer enhanced leverage and that the requirements fluctuate and may react quickly to changing market conditions, it is intended for sophisticated individuals and requires minimum equity of $110,000 to initiate and $100,000 to maintain. Requirements for stocks under this methodology generally range from 15% to 30% with the more favorable requirement applied to portfolios which contain a highly diversified group of stocks which have historically exhibited low volatility and which tend to employ option hedges.

b. SPAN – Standard Portfolio Analysis of Risk, or SPAN, is a risk-based margin methodology created by the Chicago Mercantile Exchange (CME) that is designed for futures and future options. Similar to TIMS, SPAN determines a margin requirement by calculating the value of the portfolio given a set of hypothetical market scenarios where underlying price changes and option implied volatilities are assumed to change. Again, IBKR will include in these assumptions house scenarios which account for extreme price moves along with the particular impact such moves may have upon deep out-of-the-money options. The scenario which projects the greatest loss becomes the margin requirement. A detailed overview of the SPAN margining system is provided in KB563.

Rules Based

a. Reg. T – The U.S. central bank, the Federal Reserve Board, holds responsibility for maintaining the stability of the financial system and containing systemic risk that may arise in financial markets. It does this, in part, by governing the amount of credit that broker dealers may extend to customers who borrow money to buy securities on margin.

This is accomplished through Regulation T, or Reg. T as it is commonly referred, which provides for establishment of a margin account and which imposes the initial margin requirement and payment rules on certain securities transactions. For example, on stock purchases, Reg. T currently requires an initial margin deposit by the client equal to 50% of the purchase value, allowing the broker to extend credit or finance the remaining 50%. For example, an account holder purchasing $1,000 worth of securities is required to deposit $500 and allowed to borrow $500 to hold those securities.

Reg. T only establishes the initial margin requirement and the maintenance requirement, the amount necessary to continue holding the position once initiated, is set by exchange rule (25% for stocks). Reg. T also does not establish margin requirements for securities options as this falls under the jurisdiction of the listing exchange’s rules which are subject to SEC approval. Options held in a Reg.T account are also subject to a rules based methodology where short positions are treated like a stock equivalent and margin relief is provided for spread transactions. Finally, positions held in a qualifying portfolio margin account are exempt from the requirements of Reg. T.

Where to Learn More

Tools provided to monitor and manage margin

How to determine if you are borrowing funds from IBKR

Why does IBKR calculate and report a margin requirement when I am not borrowing funds?

Margin Requirement on Leveraged ETF Products

Leveraged Exchange Traded Funds (ETFs) are a subset of general ETFs and are intended to generate performance in multiples of that of the underlying index or benchmark (e.g. 200%, 300% or greater). In addition, some of these ETFs seek to generate performance which is not only a multiple of, but also the inverse of the underlying index or benchmark (e.g., a short ETF). To accomplish this, these leveraged funds typically include among their holdings derivative instruments such as options, futures or swaps which are intended to provide the desired leverage and/or inverse performance.

Exchange margin rules seek to recognize the additional leverage and risk associated with these instruments by establishing a margin rate which is commensurate with that level of leverage (but not to exceed 100% of the ETF value). Thus, for example, whereas the base strategy-based maintenance margin requirement for a non-leveraged long ETF is set at 25% and a short non-leveraged ETF at 30%, examples of the maintenance margin change for leveraged ETFs are as follows:

1. Long an ETF having a 200% leverage factor: 50% (= 2 x 25%)

2. Short an ETF having a 300% leverage factor: 90% (= 3 x 30%)

A similar scaling in margin is also in effect for options. For example, the Reg. T maintenance margin requirement for a non-leveraged, short broad based ETF index option is 100% of the option premium plus 15% of the ETF market value, less any out-of-the-money amount (to a minimum of 10% of ETF market value in the case of calls and 10% of the option strike price in the case of puts). In the case where the option underlying is a leveraged ETF, however, the 15% rate is increased by the leverage factor of the ETF.

In the case of portfolio margin accounts, the effect is similar, with the scan ranges by which the leveraged ETF positions are stress tested increasing by the ETF leverage factor. See NASD Rule 2520 and NYSE Rule 431 for further details.

What happens if the net liquidating equity in my Portfolio Margining account falls below USD 100,000?

Overview:

Portfolio Margining accounts reporting net liquidating equity below USD 100,000 are limited to entering trades which serve solely to reduce the margin requirement until such time as either: 1) the equity increases to above 100,000 or 2) the account holder requests a downgrade to Reg T style margining through Client Portal (select the Settings, Account Settings, Configure and Account Type menu options).

If a Portfolio Margining eligible account reporting net liquidating equity below USD 100,000 enters an order which, if executed, would serve to increase the margin requirement, the following TWS message will be displayed: "Your order is not accepted, margin requirement increase not allowed. Equity with loan value is less than 100,000.00 USD."

IMPORTANT NOTICE

Please note that requests to downgrade to Reg. T will become effective the following business day if submitted prior to 4:00 ET. Also note that as the Reg. T margining methodology generally affords less leverage than does Portfolio Margining, requesting a downgrade may lead to the automatic liquidation of positions in your account in order to comply with Reg. T. You will receive a warning message if that is the case at the time you request the downgrade.

-->

What positions are eligible for Portfolio Margining?

Overview:

Portfolio Margining is eligible for US securities positions including stocks, ETFs, stock and index options and single stock futures. It does not apply to US futures or futures options positions or non-US stocks, which may already be margined using an exchange approved risk based margining methodology.

Are there any qualification requirements in order to receive Portfolio Margining treatment on US securities positions and how does one request this form of margin?

Overview:

In order to enabled for portfolio margining an account must be approved for option trading and must have at least USD 110,000 in net liquidating equity (USD 100,000 to maintain, once enabled). Account holders will also be required to acknowledge and sign the Portfolio Margin Risk Disclosure document and be bound by its terms.

Portfolio margining may be requested through the on-line application phase (in the Account Configuration step) or after the account has been approved. To apply once the account has already been approved, log into Client Portal and select the Settings and Account Settings menu options. In the Configuration section, click the gear icon next to the words "Account Type". There you may choose the portfolio margin treatment which will initiate the approval process. Please note that requests are subject to review (generally a 1-2 day process) and may be declined for various reasons including a projected increase in margin upon upgrade from Reg T to Portfolio Margining.