Risk Based Margin Considerations

| LLC Risk Based (i.e. Portfolio Margin) | Non-LLC Risk Based Margin | |

| $110,000 initial value requirement | Yes | N/A |

| Minimum equity to operate on margin | USD 100,000 | IB-HK: USD 2,000 IB-AU: AUD 2,000 IB-LUX, IB-IE and IB-CE: EUR 2,000 IB-SG: SGD 2,000 |

| Full options trading approval | Yes | N/A |

| PDT | Yes | N/A |

| Stress testing | Yes | Yes |

| Dynamic House Scanning Charges (TOMS) ¹ | Yes | Yes |

| Shifts in option Implied Volatility (IV) | Yes | Yes |

| A $0.375 multiplied by the index per contract minimum is computed (Only applied to Portfolio Margin eligble products) | Yes | Yes |

| Initial margin will be 110% of Maintenance Margin (US securities only) | Yes | Yes |

| Initial margin will be 125% of Maintenance Margin (Non-US securities) | Yes | Yes |

| Extreme Price Scans | Yes | Yes |

| Large Position Charge (A position which is 1% or more of shares outstanding) | Yes | Yes |

| Days to Liquidate (A large position in relation to the average daily trading volume, which may result in higher initial margin requirements) | Yes | Yes |

| Global Concentration Charge (2 riskiest position stressed +/-30% remaining assets +/-5%) | Yes | Yes |

| Singleton Margin Method for Small Cap Stocks (Stress Test which simulates a price change reflective of a $500 million USD in market capitalization)² | Yes | Yes |

| Singleton Margin Method for stocks domiciled in China (Stress Test which simulates a price change reflective of a $1.5 billion USD in market capitalization)² | Yes | Yes |

| Default Singleton Margin Method (Stress Test which simulates a price change +30% and down -25%)² | Yes | Yes |

| Singleton Margin Method for HK Real Estate Stocks (Stress test +/-50%)² | Yes | Yes |

1 Dynamic House Scanning Charges are available only on select exchanges (Asian Exchanges and MEXDER)

2 IBKR will calculate the potential loss for each stock and its derivates by subjecting them to a stress test. The requirement for the stock (and its derivatives) which projects the greatest loss in the above scenario will be compared to what would otherwise be the aggregate portfolio margin requirement, and the greater of the two will be the margin requirement for the portfolio

Навигатор риска – калькулятор альтернативной маржи

Overview:

IB регулярно анализирует уровень маржи и вводит изменения, которые увеличивают требования выше минимума, установленного законодательством, в соответствии с условиями рынка. Чтобы помочь клиентам оценить последствия таких изменений для своего портфеля, в "Навигатор риска" добавлена функция "Калькулятор альтернативной маржи". Ниже приведены шаги по созданию портфеля "что, если", который позволяет определить, к чему могут привести такие изменения маржи.

Шаг 1. Откройте новый портфель "что, если"

На экране торговой платформы Classic TWS выберите Аналитические инструменты, Навигатор риска и затем Открыть новый "что, если" (Рис. 1: Analytical Tools -> Risk Navigator -> Open New What-If).

Рис. 1

.png)

При работе в Mosaic TWS выберите Новое окно, Навигатор риска и затем Открыть новый "что, если".

Шаг 2. Настройте исходный портфель

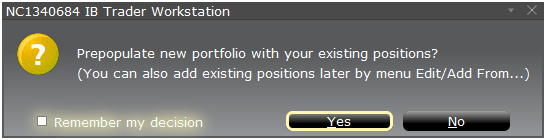

Появится всплывающее окно (Рис. 2), где Вам предложат создать гипотетический портфель на основе своего текущего портфеля или создать новый. Если нажать "Да", в новый портфель "что, если" будут загружены Ваши текущие позиции.

Рис. 2

Если нажать "Нет", откроется новый портфель "что, если" без позиций.

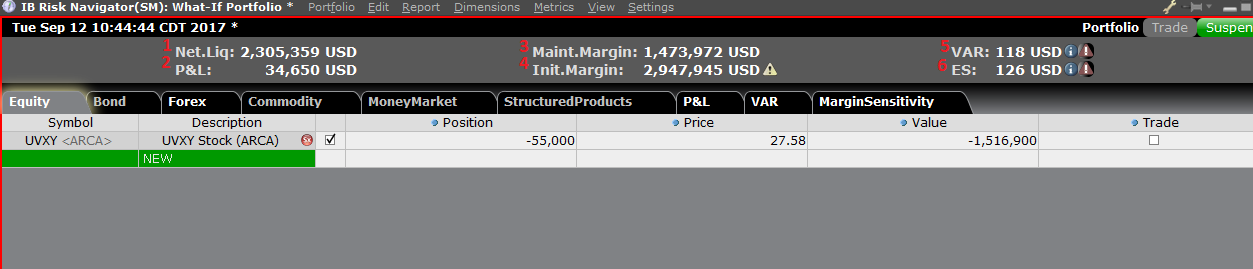

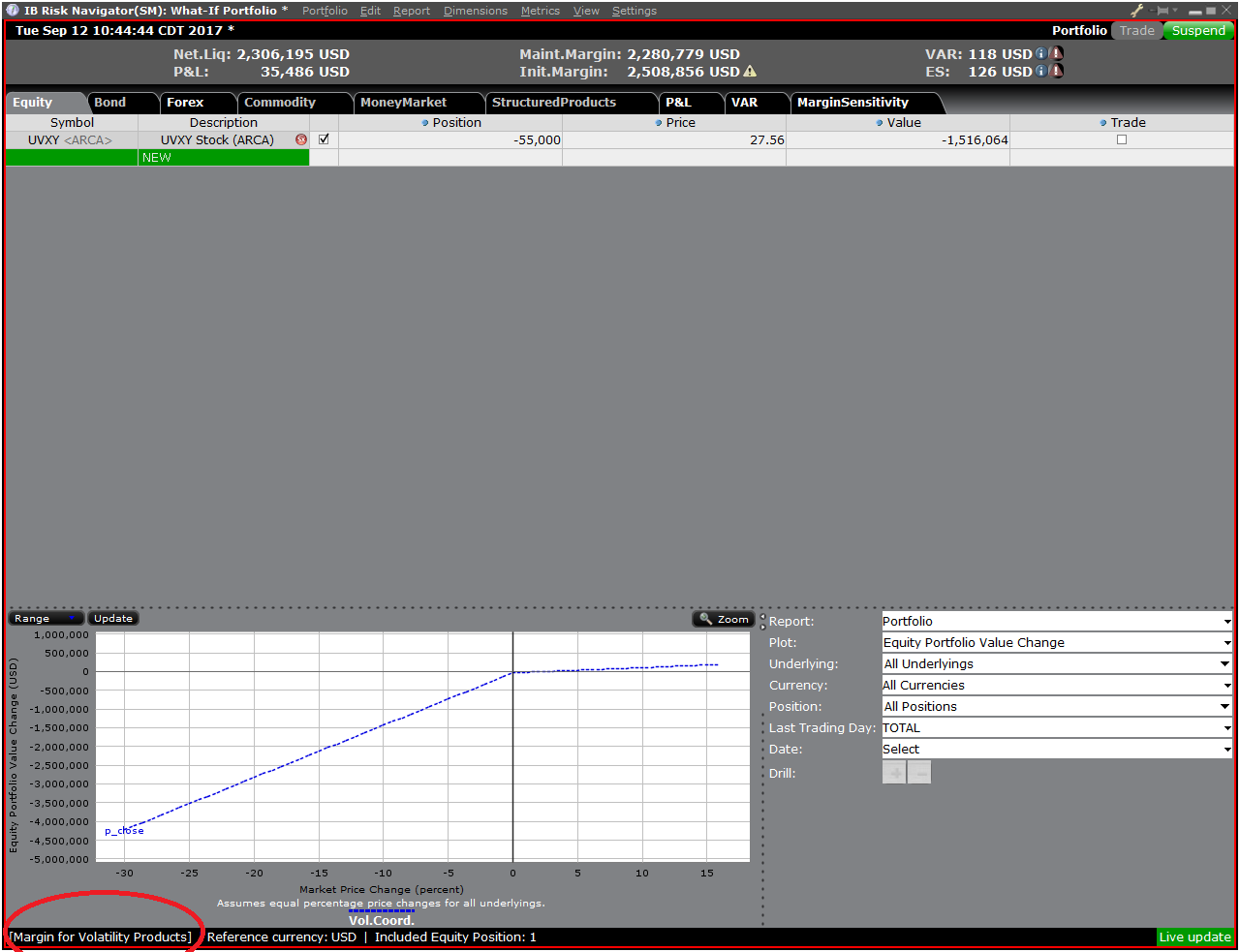

Панель управления рисками

Панель управления рисками находится над вкладками с продуктами и доступна для работы с портфелями "что, если" и активными портфелями. Для портфелей "что, если" значения рассчитываются по запросу. На панели отображается основная информация счета, в том числе:

1) Чистая ликвидационная стоимость – общая чистая ликвидационная стоимость счета

2) ПиУ – общие дневные ПиУ для всего портфеля

3) Минимальная маржа – текущие требования общей минимальной маржи

4) Начальная маржа – общие требования начальной маржи

5) VAR – стоимость под риском (Value at risk) всего портфеля

6) ES – ожидаемый дефицит (Expected Shortfall), т.е. средняя стоимость под риском – ожидаемая доходность портфеля в худшем случае

Калькулятор альтернативной маржи

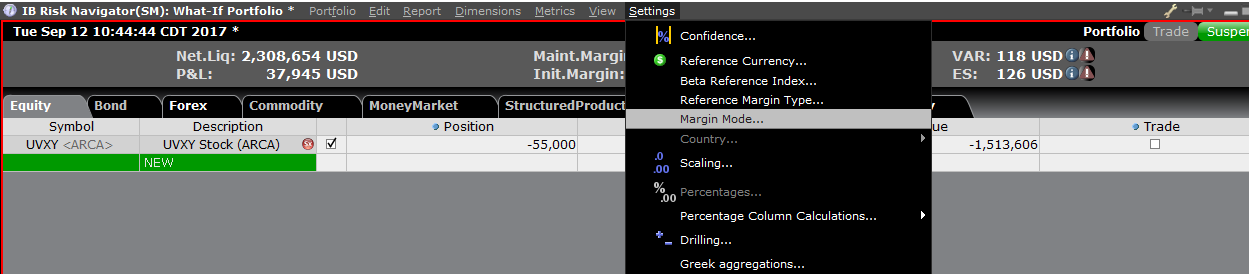

Чтобы открыть "Калькулятор альтернативной маржи", в меню "Настройки" выберите "Режим маржи" (Рис. 3: Settings -> Margin Mode). Калькулятор отображает, как изменения маржи повлияют на общие маржинальные требования после вступления в силу.

Рис. 3

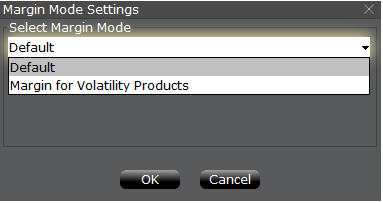

Шаг 3. Настройте режим маржи

Появится всплывающее окно (Рис. 4) с заголовком "Настройки режима маржи" (Margin Mode Settings). С помощью выпадающего меню на экране Вы можете изменить расчет маржи с опции по умолчанию (нынешниие регуляции) на новые настройки маржи (т.е. новые правила маржи). Выберите желаемый вариант и нажмите "ОК".

Рис. 4

После изменения режима маржи панель "Навигатора риска" автоматически обновится. Вы можете переключать и сравнивать режимы маржи. Выбранный режим маржи будет указан в левом нижнем углу "Навигатора риска" (Рис. 5).

Рис. 5

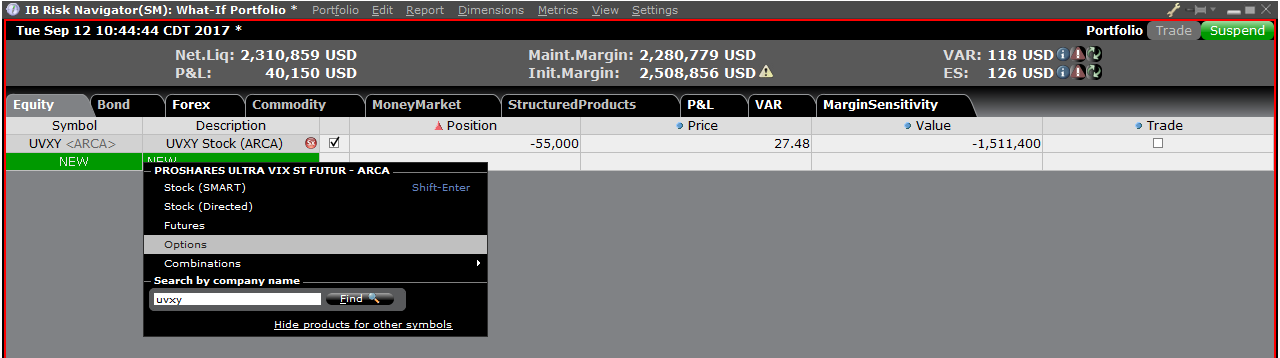

Шаг 4. Добавьте позиции

Чтобы добавить позиции в портфель "что, если", нажмите на зеленую строку с названием "Новый" и введите символ андерлаинга (Рис. 6), укажите тип продукта (Рис. 7) и введите размер позиции (Рис. 8)

Рис. 6

Рис. 7

Рис. 8

Вы можете изменить позиции и посмотреть, как это влияет на маржу. Измените позиции и нажмите на иконку пересчета (![]() ) справа от значений маржи, чтобы их обновить. Если рядом со значением маржи отображена эта иконка, значит величина не отражает актуальные данные портфеля "что, если".

) справа от значений маржи, чтобы их обновить. Если рядом со значением маржи отображена эта иконка, значит величина не отражает актуальные данные портфеля "что, если".

Увеличение маржи в связи с выборами в США (2020 год)

Ввиду волатильности рынка, связанной с предстоящими президентскими выборами в США, Interactive Brokers повысит маржинальные требования всех американских индексных фьючерсов и деривативов, а также фьючерсов Dow Jones, котируемых на бирже OSE.JPN.

Клиенты, имеющие позиции по индексным фьючерсам США и их деривативам и/или фьючерсам Down Jones на бирже OSE.JPN, должны быть готовы к тому, что текущие маржинальные требования вырастут примерно на 35%. Процесс займет 20 календарных дней: постепенное повышение начальной маржи начнется 28 сентября 2020 года, а минимальной маржи – 5 октября 2020 года.

Таблица ниже содержит примеры прогнозируемого роста маржи для некоторых распространенных продуктов:

| Символ фьючерса |

Описание | Биржа | Торговый класс |

Текущая ставка (диапазон сканирования цены)* | Прогнозируемая ставка (диапазон сканирования цены) |

| ES | E-mini S&P 500 | GLOBEX | ES | 7.13 | 9.63 |

| YM | MINI DJIA | ECBOT | YM | 6.14 | 8.29 |

| RTY | Russell 2000 | GLOBEX | RTY | 6.79 | 9.17 |

| NQ | NASDAQ E-MINI | GLOBEX | NQ | 6.57 | 8.87 |

| DJIA | OSE Dow Jones Industrial Average | OSE.JPN | DJIA | 5.14 | 6.94 |

*по состоянию на открытие торговли 02/10/2020.

ПРИМЕЧАНИЕ: "Навигатор риска" IBKR поможет Вам оценить влияние новых маржинальных требований на Ваш текущий портфель или на любой гипотетический портфель. Подробнее о функции расчета альтернативной маржи можно узнать в статье KB2957: Навигатор риска - калькулятор альтернативной маржи (режим "Выборы в США").

U.S. 2020 Election Margin Increase

In light of the potential market volatility associated with the upcoming United States presidential election, Interactive Brokers will implement an increase in the margin requirement for all U.S. traded equity index futures and derivatives and Dow Jones Futures listed on the OSE.JPN exchange.

Clients holding a position in a U.S. equity index future and their derivatives and/or Down Jones Futures listed on the OSE.JPN exchange should expect the margin requirement to increase by approximately 35% above the normal margin requirement. The increase is scheduled to be implemented gradually over a 20-calendar day period with the maintenance margin increase starting on October 5, 2020 through October 30, 2020.

The table below provides examples of the margin increases projected for some of the more widely held products

| Future Symbol |

Description | Listing Exchange | Trading Class | Current Rate (Price scan range)* | Projected Rate (Price scan range) |

| ES | E-mini S&P 500 | CME | ES | 7.13 | 9.63 |

| YM | MINI DJIA | CBOT | YM | 6.14 | 8.29 |

| RTY | Russell 2000 | CME | RTY | 6.79 | 9.17 |

| NQ | NASDAQ E-MINI | CME | NQ | 6.57 | 8.87 |

| DJIA | OSE Dow Jones Industrial Average | OSE.JPN | DJIA | 5.14 | 6.94 |

*As of 10/2/20 open.

NOTE: IBKR's Risk Navigator can help you determine the impact the new maintenance margin requirements will have on your current portfolio or any other portfolio you would like to construct or test. For more information about the Alternative Margin Calculator feature, please see KB Article 2957: Risk Navigator: Alternative Margin Calculator and from the margin mode setting in Risk Navigator, select " US Election Margin".

Overview of Central Bank of Ireland CFD Rules Implementation for Retail Clients at IBIE

Overview:

|

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 61% of retail investor accounts lose money when trading CFDs with IBKR. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. |

The Central Bank of Ireland (CBI) enacted new rules applicable to retail clients trading CFDs, effective 1st August 2019. Professional clients are unaffected.

The rules consist of: 1) leverage limits; 2) a margin close out rule on a per account basis; 3) negative balance protection on a per account basis; 4) a restriction on the incentives offered to trade CFDs; and 5) a standardized risk warning.

Most clients (excepting regulated entities) are initially categorised as Retail Clients. IBKR may in certain circumstances agree to reclassify a Retail Client as a Professional Client, or a Professional Client as a Retail Client. Please see MiFID Categorisation for further detail.

The following sections detail how IBKR has implemented the CBI Decision.

1 Leverage Limits

1.1 Margins

Leverage limits were set by CBI at different levels depending on the underlying:

- 3.33% for major currency pairs; Major currency pairs are any combination of USD; CAD; EUR; GBP; CHF; JPY

- 5% for:

- Non-major currency pairs are any combination that includes a currency not listed above, e.g., USD.CNH

- Major indices are IBUS500; IBUS30; IBUST100; IBGB100; IBDE40; IBEU50; IBFR40; IBJP225; IBAU200

- Gold

- 10% for non-major equity indices; IBES35; IBCH20; IBNL25; IBHK50

- 20% for individual equities

1.2 Applied Margins - Standard Requirement

In addition to the CBI Margins, IBKR establishes its own margin requirements (IB Margins) based on the historical volatility of the underlying, and other factors. We will apply the IB Margins if they are higher than those prescribed by CBI .

Details of applicable IB and CBI margins can be found here.

1.2.1 Applied Margins - Concentration Minimum

A concentration charge is applied if your portfolio consists of a small number of CFD and/or Stock positions, or if the three largest positions have a dominant weight. We stress the portfolio by applying a 30% adverse move on the three largest positions and a 5% adverse move on the remaining positions. The total loss is applied as the maintenance margin requirement if it is greater than the standard requirement for the combined Stock and CFD positions. Note that the concentration charge is the only instance where CFD and Stock positions are margined together.

1.3 Funding of Initial Margin Requirements

You can only use cash to post initial margin to open a CFD position.

Initially all cash used to fund the account is available for CFD trading. Any initial margin requirements for other instruments and cash used to purchase cash stock reduce the available cash. If your cash stock purchases have created a margin loan, no funds are available for CFD trades even if your account has significant equity. We cannot increase a margin loan to fund CFD margin under the CBI rules.

Realized CFD profits are included in cash and are available immediately; the cash does not have to settle first. Unrealized profits however cannot be used to meet initial margin requirements.

2 Margin Close Out Rule

2.1 Maintenance Margin Calculations & Liquidations

The CBI requires IBKR to liquidate CFD positions latest when qualifying equity falls below 50% of the initial margin posted to open the positions. IBKR may close out positions sooner if our risk view is more conservative. Qualifying equity for this purpose includes CFD cash and unrealized CFD P&L (positive and negative). Note that CFD cash excludes cash supporting margin requirements for other instruments.

The basis for the calculation is the initial margin posted at the time of opening a CFD position. In other words, and unlike margin calculations applicable to non-CFD positions, the initial margin amount does not change when the value of the open position changes.

2.1.1 Example

You have EUR 2000 cash in your account and no open positions. You want to buy 100 CFDs of XYZ at a limit price of EUR 100. You are first filled 50 CFDs and then the remaining 50. Your available cash reduces as your trades are filled:

|

|

Cash |

Equity* |

Position |

Price |

Value |

Unrealized P&L |

IM |

MM |

Available Cash |

MM Violation |

|

Pre Trade |

2000 |

2000 |

|

|

|

|

|

|

2000 |

|

|

Post Trade 1 |

2000 |

2000 |

50 |

100 |

5000 |

0 |

1000 |

500 |

1000 |

No |

|

Post Trade 2 |

2000 |

2000 |

100 |

100 |

10000 |

0 |

2000 |

1000 |

0 |

No |

*Equity equals Cash plus Unrealized P&L

The price increases to 110. Your equity is now 3000, but you cannot open additional positions because your available cash is still 0, and under the CBI rules IM and MM remain unchanged:

|

|

Cash |

Equity |

Position |

Price |

Value |

Unrealized P&L |

IM |

MM |

Available Cash |

MM Violation |

|

Change |

2000 |

3000 |

100 |

110 |

11000 |

1000 |

2000 |

1000 |

0 |

No |

The price then drops to 95. Your equity declines to 1500 but there is no margin violation since it is still greater than the 1000 requirement:

|

|

Cash |

Equity |

Position |

Price |

Value |

Unrealized P&L |

IM |

MM |

Available Cash |

MM Violation |

|

Change |

2000 |

1500 |

100 |

95 |

9500 |

(500) |

2000 |

1000 |

0 |

No |

The price falls further to 85, causing a margin violation and triggering a liquidation:

|

|

Cash |

Equity |

Position |

Price |

Value |

Unrealized P&L |

IM |

MM |

Available Cash |

MM Violation |

|

Change |

2000 |

500 |

100 |

85 |

8500 |

(1500) |

2000 |

1000 |

0 |

Yes |

3 Negative Equity Protection

The CBI Decision limits your CFD-related liability to the funds dedicated to CFD-trading. Other financial instruments (e.g., shares or futures) cannot be liquidated to satisfy a CFD margin-deficit.*

Therefore, non-CFD assets are not part of your capital at risk for CFD trading.

Should you lose more than the cash dedicated to CFD trading, IB must write off the loss.

As Negative Equity Protection represents additional risk to IBKR, we will charge retail investors an additional financing spread of 1% for CFD positions held overnight. You can find detailed CFD financing rates here.

*Although we cannot liquidate non-CFD positions to cover a CFD deficit, we can liquidate CFD positions to cover a non-CFD deficit.

Margin Considerations for Intramarket Futures Spreads

Background

Clients who simultaneously hold both long and short positions of a given futures contract having different delivery months are often provided a spread margin rate that is less than the margin requirement for each position if considered separately. However, as the settlement prices of each contract may deviate significantly as the front month contract approaches its close out date, IBKR will reduce the benefit of the spread margin rate to reflect the risk of this price deviation.

Spread Margin Adjustment

This reduction is accomplished by effectively decoupling or breaking the spread in phases on each of the 3 business days preceding the close out date of the front contract month, as follows:

- On the 3rd business day prior to close out, the initial and maintenance margin requirements will be equal to 10% of their respective requirements on each contract month as if there was no spread, plus 90% of the spread requirement;

- On the 2nd business day prior to close out, the initial and maintenance margin requirements will be equal to 20% of their respective requirements on each contract month as if there was no spread, plus 80% of the spread requirement;

- On the business day prior to close out, the initial and maintenance margin requirements will be equal to 30% of their respective requirements on each contract month as if there was no spread, plus 70% of the spread requirement.

Working Example

Assume a hypothetical futures contract XYZ with the margin requirements as outlined in the table below:

| XYZ | Front Month - 1 Short Contract (Uncovered) | Back Month - 1 Long Contract (Uncovered) | Spread - 1 Short Front Month vs. 1 Long Back Month |

| Initial Margin | $1,250 | $1,500 | $500 |

| Maintenance Margin | $1,000 | $1,200 | $400 |

Further assume a position consisting of 1 short front month contract and 1 long back month contract with the front month contract close out date = T. using this hypothetical example, the initial margin requirement over the 3 business day period preceding close out date is outlined in the table below:

| Day | Initial Margin Requirement | Calculation Details |

| T-4 | $500 | Unadjusted |

| T-3 | $725 | .1($1,250 + $1,500) + .9($500) |

| T-2 | $950 | .2($1,250 + $1,500) + .8($500) |

| T-1 | $1,175 | .3($1,250 + $1,500) + .7($500) |

| T | $1,175 | Positions not in compliance with close out requirements are subject to liquidation. |

Concentrated Positions in Low Cap Stocks

The margin requirement for accounts holding concentrated positions in low cap stocks is as follows:

- An alternative stress test will be considered following the margin calculation currently in place. Here, each stock and its derivatives will be subject to a stress test which simulates a price change reflective of a $500 million decrease in capitalization (e.g., 25% in the case of a stock with a market capitalization of $2 billion; 30% for a stock with a market capitalization of $1.5 billion; etc.). Stocks with a market capitalization of $500 million or below will be subject to a stress test as if the price has fallen to $0.

- For the stock which projects the greatest loss assuming a $500 million decrease in capitalization, that loss will be compared to the initial margin as determined under the preceding calculation for the aggregate portfolio and, if greater, will become the initial margin requirement.

- If the initial margin requirement is increased, the maintenance margin for that same stock and its derivatives will increase to approximately 90% of the initial requirement for the aggregate portfolio.

Что такое SMA и как он устроен?

Overview:

SMA – это "Специальный гарантийный счет" (Special Memorandum Account), представляющий собой не капитал или наличные средства, а скорее кредитную линию, создаваемую при увеличении рыночной стоимости ценных бумаг маржевого счета Reg. T. Цель такого счета состоит в сохранении покупательской способности, обеспечиваемой нереализованной прибылью, для дальнейших покупок, которая в противном случае может быть гарантирована только путем вывода избытка капитала и последующим внесением его на счет в момент совершения покупки. Таким образом SMA помогает поддерживать постоянный остаток на счете и избегать излишних переводов.

SMA увеличивается вместе с ростом ценной бумаги, однако не уменьшается при падении ее стоимости. Стоимость SMA снижается только при покупке ценных бумаг или выводе наличных средств, и единственное ограничение по его использованию состоит в том, что остаток на нем не должен опускаться ниже минимальных маржинальных требований в результате упомянутых операций. Транзакции, которые способствуют увеличению SMA, включают: денежные депозиты, доход от процентов или дивиденды (в отношении "доллар в доллар") или продажа ценных бумаг (50% чистой прибыли). Обращаем Ваше внимание, что остаток по счету SMA отражает совокупность всех влияющих на него бухгалтерских записей с момента открытия счета. Учитывая типично охватываемый временной период и объем записей, сверка текущего уровня остатка SMA с ежедневными выписками по операциям, хотя и осуществима, представляется нецелесообразной.

Чтобы понять, как работает SMA, представим, что владелец счета вносит $5,000 и покупает $10,000 ценных бумаг с кредитом в размере 50% от стоимости (или маржинальными требованиями, равными 1 – сумма кредита, или 50%). Тогда показатели счета до и после выглядят следующим образом:

|

Строка

|

Описание

|

Событие 1 –

исходный депозит

|

Событие 2 –

покупка акций

|

|

A.

|

Наличные

|

$5,000

|

($5,000)

|

|

B.

|

Рыночная стоимость длинных акций

|

$0

|

$10,000

|

|

C.

|

Чистая ликвидационная стоимость/EWL* (A + B)

|

$5,000

|

$5,000

|

|

D.

|

Начальные маржинальные требования (B * 50%)

|

$0

|

$5,000

|

|

E

|

Доступные средства (C - D)

|

$5,000

|

$0

|

|

F.

|

SMA

|

$5,000

|

$0

|

|

G.

|

Покупательская способность

|

$10,000

|

$0

|

Далее представим, что стоимость длинных акций увеличилась до $12,000. Этот рост рыночной стоимости на $2,000 приведет к созданию счета SMA размером в $1,000, что позволит владельцу счета: 1) дополнительно приобрести ценные бумаги стоимостью в $2,000 без необходимости вкладывать дополнительные средства и выплаты 50%-ой ставки маржи; или 2) вывести $1,000 наличными, которые можно финансировать путем увеличения дебетового остатка, если на счете нет наличных денежных средств. См. ниже:

|

Строка

|

Описание

|

Событие 2 –

покупка акций

|

Событие 3 –

рост акций

|

|

A.

|

Наличные

|

($5,000)

|

($5,000)

|

|

B.

|

Рыночная стоимость длинных акций

|

$10,000

|

$12,000

|

|

C.

|

Чистая ликвидационная стоимость/EWL* (A + B)

|

$5,000

|

$7,000

|

|

D.

|

Начальные маржинальные требования (B * 50%)

|

$5,000

|

$6,000

|

|

E

|

Доступные средства (C - D)

|

$0

|

$1,000

|

|

F.

|

SMA

|

$0

|

$1,000

|

|

G.

|

Покупательская способность

|

$0

|

$2,000

|

*EWL отражает стоимость капитала с кредитом, которая в данном примере равна чистой ликвидационной стоимости.

В заключение, также обратите внимание, что SMA является понятием Reg. T, которое используется для оценки соответствия счетов ценных бумаг, хранящихся в IB LLC, суточным начальным маржинальным требованиям, но не внутридневным или суточным минимальным требованиям. Оно также не используется для определения того, удовлетворяют ли маржинальным требованиям счета биржевых товаров. Аналогичным образом, счета с отрицательным SMA в момент вступления в силу суточных или начальных маржинальных требований Reg.T (15:50 ET) подвергаются ликвидации позиций для восстановления соответствия требованиям маржи.

Реализация правил ESMA в отношении CFD в IBKR – розничные клиенты

Overview:

|

CFD – это сложные инструменты, которые сопряжены с высоким риском убытков из-за использования кредитного плеча.

63,7% счетов розничных инвесторов терпят убытки при торговле CFD через IBKR.

Убедитесь, что Вы понимаете принцип работы CFD и в состоянии принять на себя высокий риск убытков. |

Европейская служба по ценным бумагам и рынкам (ESMA) ввела новые правила по CFD для розничных клиентов, вступившие в силу 1 августа 2018 года. Они не распространяются на профессиональных клиентов.

В правила входят: 1) ограничения кредитного плеча; 2) правило ликвидации согласно марже конкретного счета; 3) защита счета от отрицательного баланса; 4) ограничение поощрительных программ по торговле CFD; и 5) стандартное предупреждение о рисках.

Большинство клиентов (за исключением регулируемых юр. лиц) изначально классифицируются как розничные. В некоторых случаях IBKR может согласиться изменить статус розничного клиента на профессиональный или наоборот. Подробнее можно узнать в статье "Классификация MiFID".

В следующих разделах описывается, как решение ESMA реализуется в IBKR (UK).

1. Ограничения кредитного плеча

1.1. Маржа ESMA.

ESMA установила ограничения кредитного плеча, которые зависят от базисного актива:

- 3,33% для основных валютных пар. Основные валютные пары – это любые комбинации USD; CAD; EUR; GBP; CHF; JPY.

- 5% для прочих валютных пар и основных индексов;

- Прочие (не основные) валютные пары – это комбинации, в которые входит валюта, не указанная выше (например, USD.CNH)

- Основные индексы: IBUS500; IBUS30; IBUST100; IBGB100; IBDE40; IBEU50; IBFR40; IBJP225; IBAU200

- 10% для прочих фондовых индексов: IBES35; IBCH20; IBNL25; IBHK50

- 20% для отдельных акций

1.2. Применяемая маржа – стандартные требования.

Вдобавок к марже ESMA компания IBKR (UK) устанавливает свои собственные минимальные маржинальные требования ("Маржа IB") согласно исторической волатильности андерлаинга и прочим факторам, описанным ниже.Маржа IB применяется, если она выше предписанной ESMA.

Подробнее о действующих маржинальных требованиях IB и ESMA можно узнать здесь.

1.2.1. Применяемая маржа – минимальный уровень концентрации.

С портфеля взимается плата за концентрацию, если он состоит из малого числа позиций с CFD или его основной вес приходится на две крупнейшие позиции. Мы проводим тест для портфеля, моделируя неблагоприятный сдвиг в 30% для двух крупнейших позиций и в 5% – для остальных. Если общий убыток превышает стандартную маржу, то он устанавливается в качестве минимального маржинального требования.

1.3. Средства, доступные для начальной маржи.

Выполнение начальных маржинальных требований при открытии позиции по CFD возможно только за счет денежных средств. Реализованная прибыль по CFD включается в денежный остаток и становится доступна сразу – расчета ждать не нужно. В то же время нереализованная прибыль не может использоваться для покрытия начальной маржи.

1.4. Автоматическое финансирование начальных маржинальных требований (сегменты с приставкой "F").

IBKR (UK) автоматически переводит средства с Вашего основного счета на сегмент с приставкой "F", чтобы покрыть начальные маржинальные требования по CFD.

Обращаем внимание, что для удовлетворения дальнейших минимальных требований по CFD мы не совершаем таких переводов. Поэтому, если на этом сегменте недостаточно необходимых средств для покрытия маржи (см. ниже), то позиции будут ликвидированы независимо от того, достаточно ли средств на Вашем основном счете. Во избежание ликвидации Вам необходимо самостоятельно перевести дополнительные средства на F-сегмент на "Портале клиентов".

2. Правило ликвидации

2.1. Расчет минимальной маржи и ликвидация.

Согласно правилам ESMA, IBKR обязана ликвидировать CFD-позиции до того, как доступный остаток на счете опустится ниже 50% от начальной маржи, внесенной при открытии этих позиций. IBKR может закрыть позиции раньше, если внутренние правила в отношении риска являются более строгими. В рассматриваемый для этих целей остаток входят денежные средства на сегменте счета с приставкой "F" (средства на любых других сегментах не включаются) и нереализованная ПиУ по CFD-контрактам (положительная и отрицательная).

Основой расчета служат начальные маржинальные требования, действовавшие при открытии позиции по CFD. Другими словами, в отличие от расчетов маржи других продуктов, сумма начальной маржи для СFD не меняется при росте/снижении стоимости соответствующих открытых позиций.

2.1.1. Пример.

Денежный остаток на Вашем счете с CFD составляет 2000 EUR . Вы хотите купить 100 CFD на XYZ по лимитной цене в 100 EUR. Сначала выполняется покупка первых 50 CFD, а затем оставшихся 50. Сумма Ваших доступных средств уменьшается по мере исполнения:

| Наличные средства | Капитал* | Позиция | Цена | Стоимость | Нереализ. ПиУ | НМ | ММ | Доступные средства | Нарушение ММ | |

| Перед сделкой | 2000 | 2000 | 2000 | |||||||

| После сделки 1 | 2000 | 2000 | 50 | 100 | 5000 | 0 | 1000 | 500 | 1000 | Нет |

| После сделки 2 | 2000 | 2000 | 100 | 100 | 10000 | 0 | 2000 | 1000 | 0 | Нет |

*Капитал – это денежный остаток (наличные) плюс нереализованная ПиУ.

Цена вырастает до 110. Теперь Ваш капитал равен 3000, но Вы не можете открывать дополнительные позиции, поскольку Ваши доступные денежные средства все еще составляют 0, и, согласно правилам ESMA, начальная и минимальная маржа не меняются.

| Наличные средства | Капитал | Позиция | Цена | Стоимость | Нереализ. ПиУ | НМ | ММ | Доступные средства | Нарушение ММ | |

| Изменение | 2000 | 3000 | 100 | 110 | 11000 | 1000 | 2000 | 1000 | 0 | Нет |

Затем цена опускается до 95. Ваш капитал снижается до 1500, что не нарушает требования маржи, поскольку он все еще превышает 1000:

| Наличные средства | Капитал | Позиция | Цена | Стоимость | Нереализ. ПиУ | НМ | ММ | Доступные средства | Нарушение ММ | |

| Изменение | 2000 | 1500 | 100 | 95 | 9500 | (500) | 2000 | 1000 | 0 | Нет |

Цена снова снижается до 85, что приводит к нарушению маржинальных требований и ликвидации:

| Наличные средства | Капитал | Позиция | Цена | Стоимость | Нереализ. ПиУ | НМ | ММ | Доступные средства | Нарушение ММ | |

| Изменение | 2000 | 500 | 100 | 85 | 8500 | (1500) | 2000 | 1000 | 0 | Да |

3. Защита от отрицательного капитала

Решение ESMA ограничивает Вашу ответственность по контрактам CFD до суммы, выделенной на сделки с ними. Для устранения дефицита маржи CFD не могут быть ликвидированы другие финансовые инструменты (например, акции или фьючерсы)*.

Поэтому активы на сегментах ценных бумаг и товаров Вашего основного счета, а также активы на сегменте "F", не относящиеся к CFD, не подвергаются риску при торговле CFD. Однако все денежные средства на сегменте "F" могут использоваться для покрытия убытков, возникших в результате операций с CFD.

Поскольку защита от отрицательного капитала представляет дополнительный риск для IBKR, с розничных инвесторов будет взиматься дополнительная надбавка в 1% за позиции с CFD, переносимые на следующий день. Подробные ставки финансирования CFD можно найти здесь.

Хотя для покрытия недостающей маржи по CFD нельзя ликвидировать позиции с другими активами, позиции с CFD могут быть ликвидированы для устранения дефицита маржи других инструментов.

4. Поощрительные программы по CFD

ESMA запрещает денежные и некоторые другие формы вознаграждений, связанные с торговлей CFD. IBKR не предлагает никакие бонусные или другие поощрительные программы по CFD.

Overview of ESMA CFD Rules Implementation at IBKR (UK) - Retail Investors Only

Overview:

|

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage.

61% of retail investor accounts lose money when trading CFDs with IBKR.

You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. |

The European Securities and Markets Authority (ESMA) enacted new rules applicable to retail clients trading CFDs, effective 1st August 2018. Professional clients are unaffected.

The rules consist of: 1) leverage limits; 2) a margin close out rule on a per account basis; 3) negative balance protection on a per account basis; 4) a restriction on the incentives offered to trade CFDs; and 5) a standardized risk warning.

Most clients (excepting regulated entities) are initially categorised as Retail Clients. IBKR may in certain circumstances agree to reclassify a Retail Client as a Professional Client, or a Professional Client as a Retail Client. Please see MiFID Categorisation for further detail.

The following sections detail how IBKR (UK) has implemented the ESMA Decision.

1 Leverage Limits

1.1 ESMA Margins

Leverage limits were set by ESMA at different levels depending on the underlying:

- 3.33% for major currency pairs; Major currency pairs are any combination of USD; CAD; EUR; GBP; CHF; JPY

- 5% for non-major currency pairs and major indices;

- Non-major currency pairs are any combination that includes a currency not listed above, e.g. USD.CNH

- Major indices are IBUS500; IBUS30; IBUST100; IBGB100; IBDE40; IBEU50; IBFR40; IBJP225; IBAU200

- 10% for non-major equity indices; IBES35; IBCH20; IBNL25; IBHK50

- 20% for individual equities

1.2 Applied Margins - Standard Requirement

In addition to the ESMA Margins, IBKR (UK) establishes its own margin requirements (IB Margins) based on the historical volatility of the underlying, and other factors. We will apply the IB Margins if they are higher than those prescribed by ESMA.

Details of applicable IB and ESMA margins can be found here.

1.2.1 Applied Margins - Concentration Minimum

A concentration charge is applied if your portfolio consists of a small number of CFD positions, or if the three largest positions have a dominant weight. We stress the portfolio by applying a 30% adverse move on the three largest positions and a 5% adverse move on the remaining positions. The total loss is applied as the maintenance margin requirement if it is greater than the standard requirement.

1.3 Funds Available for Initial Margin

You can only use cash to post initial margin to open a CFD position. Realized CFD profits are included in cash and are available immediately; the cash does not have to settle first. Unrealized profits however cannot be used to meet initial margin requirements.

1.4 Automatic Funding of Initial Margin Requirements (F-segments)

IBKR (UK) automatically transfers funds from your main account to the F-segment of your account to fund initial margin requirements for CFDs.

Note however that no transfers are made to satisfy CFD maintenance margin requirements. Therefore if qualifying equity (defined below) becomes insufficient to meet margin requirements, a liquidation will occur even if you have ample funds in your main account. If you wish to avoid a liquidation you must transfer additional funds to the F-segment in Account Management.

2 Margin Close Out Rule

2.1 Maintenance Margin Calculations & Liquidations

ESMA requires IBKR to liquidate CFD positions latest when qualifying equity falls below 50% of the initial margin posted to open the positions. IBKR may close out positions sooner if our risk view is more conservative. Qualifying equity for this purpose includes cash in the F-segment (excluding cash in any other account segment) and unrealized CFD P&L (positive and negative).

The basis for the calculation is the initial margin posted at the time of opening a CFD position. In other words, and unlike margin calculations applicable to non-CFD positions, the initial margin amount does not change when the value of the open position changes.

2.1.1 Example

You have EUR 2000 cash in your CFD account. You want to buy 100 CFDs of XYZ at a limit price of EUR 100. You are first filled 50 CFDs and then the remaining 50. Your available cash reduces as your trades are filled:

| Cash | Equity* | Position | Price | Value | Unrealized P&L | IM | MM | Available Cash | MM Violation | |

| Pre Trade | 2000 | 2000 | 2000 | |||||||

| Post Trade 1 | 2000 | 2000 | 50 | 100 | 5000 | 0 | 1000 | 500 | 1000 | No |

| Post Trade 2 | 2000 | 2000 | 100 | 100 | 10000 | 0 | 2000 | 1000 | 0 | No |

*Equity equals Cash plus Unrealized P&L

The price increases to 110. Your equity is now 3000, but you cannot open additional positions because your available cash is still 0, and under the ESMA rules IM and MM remain unchanged:

| Cash | Equity | Position | Price | Value | Unrealized P&L | IM | MM | Available Cash | MM Violation | |

| Change | 2000 | 3000 | 100 | 110 | 11000 | 1000 | 2000 | 1000 | 0 | No |

The price then drops to 95. Your equity declines to 1500 but there is no margin violation since it is still greater than the 1000 requirement:

| Cash | Equity | Position | Price | Value | Unrealized P&L | IM | MM | Available Cash | MM Violation | |

| Change | 2000 | 1500 | 100 | 95 | 9500 | (500) | 2000 | 1000 | 0 | No |

The price falls further to 85, causing a margin violation and triggering a liquidation:

| Cash | Equity | Position | Price | Value | Unrealized P&L | IM | MM | Available Cash | MM Violation | |

| Change | 2000 | 500 | 100 | 85 | 8500 | (1500) | 2000 | 1000 | 0 | Yes |

3 Negative Equity Protection

The ESMA Decision limits your CFD-related liability to the funds dedicated to CFD-trading. Other financial instruments (e.g. shares or futures) cannot be liquidated to satisfy a CFD margin-deficit.*

Therefore assets in the security and commodity segments of your main account, and non-CFD assets held in the F-segment, are not part of your capital at risk for CFD trading. However, all cash in the F-segment can be used to cover losses arising from CFD trading.

As Negative Equity Protection represents additional risk to IBKR, we will charge retail investors an additional financing spread of 1% for CFD positions held overnight. You can find detailed CFD financing rates here.

*Although we cannot liquidate non-CFD positions to cover a CFD deficit, we can liquidate CFD positions to cover a non-CFD deficit.

4 Incentives Offered to trade CFDs

The ESMA Decision imposes a ban on monetary and certain types of non-monetary benefits related to CFD trading. IBKR does not offer any bonus or other incentives to trade CFDs.