¿Un depósito sujeto a "retención de crédito" acumula interés durante el periodo de retención?

Overview:

La respuesta depende del método de depósito. En caso de depósitos realizados mediante ACH, cualquier interés se acumula desde la fecha en que el depósito llegue y durante el periodo de retención, tras lo cual se acredita en la cuenta. En caso de depósitos por cheque que no sean cheques bancarios, no se acumula ningún interés durante el periodo de retención. Los cheques bancarios y las transferencias por giro se acreditan en la cuenta de forma efectiva tras el recibo y, por lo tanto, no están sujetos a ninguna retención de crédito.

El interés que se le pague variará según las condiciones del mercado. Para más información sobre la cantidad de interés pagado actualmente en saldos de crédito, consulte www.interactivebrokers.com/interest.

How to determine if you are borrowing funds from IBKR

If the aggregate cash balance in a given account is a debit, or negative, then funds are being borrowed and the loan is subject to interest charges. A loan may still exist, however, even if the aggregate cash balance is a credit, or positive, as a result of balance netting or timing differences. The most common examples of this are as follows:

1. Long vs. Short Currency Balances – accounts holders may borrow cash denominated in one currency if it can be secured by a credit balance in another. Take, for example, a USD base currency account holding a long USD settled cash balance of 10,000, a short EUR settled cash balance of 5,000, with a EUR.USD exchange rate of 1.38:1. Here, for statement reporting and interest computation purposes, the overall cash balance is a USD credit of 3,088 (10,000 – (5,000 * 1.38)). As each currency is subject to a unique funding and reinvestment arrangement, the short balance would be subject to financing costs based upon its benchmark rate and tier. This cost may be offset by any interest earned on the long balance based upon its benchmark rate and tier.

2. Gross Balances by Segment – IBKR’s Universal Account contains multiple sub accounts or segments, each of which holds positions and collateral which, for regulatory and customer protection purposes, may not be commingled. This separation does not allow for netting of balances across segments and a credit in one segment may therefore not offset a debit in another. Take, for example, an IBLLC account holding both securities and commodities positions with the securities segment maintaining a debit cash balance of USD 3,000 and the commodities segment a credit cash balance of USD 8,000. While the account holds an overall net credit balance of USD 5,000, the short balance would be subject to an interest charge which may be partially offset by any interest earned on the long balance.

3. Short Sales – a short sale is a margin transaction in which the account holder is borrowing stock rather than cash. While the proceeds from the short sale are credited to the cash balance of the account, these funds must be posted with the lender of the shares as collateral to secure their return. As a result, and in recognition of the fact that the loan transaction is subject to its own financing terms, the cash collateralizing the loan is excluded for the purpose of determining whether a margin loan exists.

As example, consider an account reporting net liquidating equity (all balances in USD) of 9,000 comprised of a credit cash balance of 4,000, long stock valued at 10,000 and short stock valued at 5,000. In order to determine whether funds are being borrowed to finance the long stock position, the 5,000 portion of the cash pledged as collateral to the lender of the shares is deducted from the overall 4,000 cash balance, resulting in a 1,000 debit. This debit is subject to interest charges and the cash underlying the stock borrow either an interest charge in the case of hard to borrow shares or a short stock rebate if the shares are easy to borrow and reinvestment rates sufficiently high.

4. Unsettled Funds - borrowings are determined based upon settled funds and the time frame by which payment is due or received for a given transaction is product specific (e.g., stocks generally settle in 3 business days, spot currencies 2 and derivatives 1). For statement and trading platform purposes, cash balances are reported on a trade date rather than settlement date basis, as if settlement has completed.

As a result, an account reporting a credit cash balance may, in fact, still be carrying a margin loan if that balance includes proceeds from the sale of stock purchased with borrowed funds awaiting settlement. Similarly, an account may report a trade date based debit balance, but not yet incurring a margin loan and interest charges, as the trade has not yet settled.

For additional information regarding interest calculations, please refer to How Interest is Calculated.

Overview of IBKR issued Share CFDs

The following article is intended to provide a general introduction to share-based Contracts for Differences (CFDs) issued by IBKR.

For Information on IBKR Index CFDs click here. For Forex CFDs click here. For Precious Metals click here.

Topics covered are as follows:

I. CFD Definition

II. Comparison Between CFDs and Underlying Shares

III. CFD Tax and Margin Advantage

IV. US ETFs

V. CFD Resources

VI. Frequently Asked Questions

Risk Warning

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage.

61% of retail investor accounts lose money when trading CFDs with IBKR.

You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

ESMA Rules for CFDs (Retail Clients of IBKRs European entities, including so-called F segments)

The European Securities and Markets Authority (ESMA) has enacted new CFD rules effective 1st August 2018.

The rules include: 1) leverage limits on the opening of a CFD position; 2) a margin close out rule on a per account basis; and 3) negative balance protection on a per account basis.

The ESMA Decision is only applicable to retail clients. Professional clients are unaffected.

Please refer to the following articles for more detail:

ESMA CFD Rules Implementation at IBKR (UK) and IBKR LLC

ESMA CFD Rules Implementation at IBIE and IBCE

I. Overview

IBKR CFDs are OTC contracts which deliver the return of the underlying stock, including dividends and corporate actions (read more about CFD corporate actions).

Said differently, it is an agreement between the buyer (you) and IBKR to exchange the difference in the current value of a share, and its value at a future time. If you hold a long position and the difference is positive, IBKR pays you. If it is negative, you pay IBKR.

Our Share CFDs offer Direct Market Access (DMA). Our Share CFD quotes are identical to the Smart-routed quotes for shares that you can observe in the Trader Workstation. Similar to shares, your non-marketable (i.e. limit) orders have the underlying hedge directly represented on the deep book of those exchanges at which it trades. This also means that you can place orders to buy the CFD at the underlying bid and sell at the offer.

To compare IBKR’s transparent CFD model to others available in the market please see our Overview of CFD Market Models.

We currently offer approximately 8500 Share CFDs covering the principal markets in the US, Europe and Asia. Eligible shares have minimum market capitalization of USD 500 million and median daily trading value of at least USD 600 thousand. Please see CFD Product Listings for more detail.

Most order types are available for CFDs, including auction orders and IBKR Algos.

CFDs on US share can also be traded during extended exchange hours and overnight. Other CFDs are traded during regular hours.

II. Comparison Between CFDs and Underlying Shares

Depending on your trading objectives and trading style, CFDs offer a number of advantages compared to stocks, but also some disadvantages:

| BENEFITS of IBKR CFDs | DRAWBACKS of IBKR CFDs |

|---|---|

| No stamp duty or financial transaction tax (UK, France, Belgium, Spain) | No ownership rights |

| Generally lower margin rates than shares* | Complex corporate actions may not always be exactly replicable |

| Tax treaty rates for dividends without need for reclaim | Taxation of gains may differ from shares (please consult your tax advisor) |

| Exemption from day trading rules | |

| US ETFs tradable as CFDs** |

*IB LLC and IB-UK accounts.

**EEA area clients cannot trade US ETFs directly, as they do not publish KIDs.

III. CFD Tax and Margin Advantage

Where stamp duty or financial transaction tax is applied, currently in the UK (0.5%), France (0.3%), Belgium (0.35%) and Spain (0.2%), it has a substantially detrimental impact on returns, particular in an active trading strategy. The taxes are levied on buy-trades, so each time you open a long, or close a short position, you will incur tax at the rates described above.

The amount of available leverage also significantly impacts returns. For European IBKR entities, margin requirements are risk-based for both stocks and CFDs, and therefore generally the same. IB-UK and IB LLC accounts however are subject to Reg T requirements, which limit available leverage to 2:1 for positions held overnight.

To illustrate, let's assume that you have 20,000 to invest and wish to leverage your investment fully. Let's also assume that you hold your positions overnight and that you trade in and out of positions 5 times in a month.

Let's finally assume that your strategy is successful and that you have earned a 5% return on your gross (fully leveraged) investment.

The table below shows the calculation in detail for a UK security. The calculations for France, Belgium and Spain are identical, except for the tax rates applied.

| UK CFD | UK Stock | UK Stock | |

|---|---|---|---|

| All Entities |

EU Account

|

IB LLC or IBUK Acct

|

|

| Tax Rate | 0% | 0.50% | 0.50% |

| Tax Basis | N/A | Buy Orders | Buy Orders |

| # of Round trips | 5 | 5 | 5 |

| Commission rate | 0.05% | 0.05% | 0.05% |

| Overnight Margin | 20% | 20% | 50% |

| Financing Rate | 1.508% | 1.508% | 1.508% |

| Days Held | 30 | 30 | 30 |

| Gross Rate of Return | 5% | 5% | 5% |

| Investment | 100,000 | 100,000 | 40,000 |

| Amount Financed | 100,000 | 80,000 | 20,000 |

| Own Capital | 20,000 | 20,000 | 20,000 |

| Tax on Purchase | 0.00 | 2,500.00 | 1,000.00 |

| Round-trip Commissions | 500.00 | 500.00 | 200.00 |

| Financing | 123.95 | 99.16 | 24.79 |

| Total Costs | 623.95 | 3099.16 | 1224.79 |

| Gross Return | 5,000 | 5,000 | 2,000 |

| Return after Costs | 4,376.05 | 1,900.84 | 775.21 |

| Difference | -57% | -82% |

The following table summarizes the reduction in return for a stock investment, by country where tax is applied, compared to a CFD investment, given the above assumptions.

| Stock Return vs cfD | Tax Rate | EU Account | IB LLC or IBUK Acct |

|---|---|---|---|

| UK | 0.50% | -57% | -82% |

| France | 0.30% | -34% | -73% |

| Belgium | 0.35% | -39% | -75% |

| Spain | 0.20% | -22% | -69% |

IV. US ETFs

EEA area residents who are retail investors must be provided with a key information document (KID) for all investment products. US ETF issuers do not generally provide KIDs, and US ETFs are therefore not available to EEA retail investors.

CFDs on such ETFs are permitted however, as they are derivatives for which KIDs are available.

Like for all share CFDs, the reference price for CFDs on ETFs is the exchange-quoted, SMART-routed price of the underlying ETF, ensuring economics that are identical to trading the underlying ETF.

V. Extended and Overnight Hours

US CFDs can be traded from 04:00 to 20:00EST, and the again overnight from 20:00 to 03:30 the following day. Trades in the overnight session are attributed to the day when the session ends, even if a trade is entered before midnight the previous day. This has implications for corporate actions and financing.

Trades entered before midnight on the day before ex-date will not have a dividend entitlement. Trades before midnight will settle as if they had been traded the following day, delaying the start of financing.

VI. CFD Resources

Below are some useful links with more detailed information on IBKR’s CFD offering:

The following video tutorial is also available:

How to Place a CFD Trade on the Trader Workstation

VII. Frequently Asked Questions

What Stocks are available as CFDs?

Large and Mid-Cap stocks in the US, Western Europe, Nordic and Japan. Liquid Small Cap stocks are also available in many markets. Please see CFD Product Listings for more detail. More countries will be added in the near future.

Do you have CFDs on other asset classes?

Yes. Please see IBKR Index CFDs - Facts and Q&A, Forex CFDs - Facts and Q&A and Metals CFDs - Facts and Q&A.

How do you determine your Share CFD quotes?

IBKR CFD quotes are identical to the Smart routed quotes for the underlying share. IBKR does not widen the spread or hold positions against you. To learn more please go to Overview of CFD Market Models.

Can I see my limit orders reflected on the exchange?

Yes. IBKR offers Direct market Access (DMA) whereby your non-marketable (i.e. limit) orders have the underlying hedges directly represented on the deep books of the exchanges on which they trade. This also means that you can place orders to buy the CFD at the underlying bid and sell at the offer. In addition, you may also receive price improvement if another client's order crosses yours at a better price than is available on public markets.

How do you determine margins for Share CFDs?

IBKR establishes risk-based margin requirements based on the historical volatility of each underlying share. The minimum margin is 10%, making CFDs more margin-efficient than trading the underlying share in many cases. Retail investors are subject to additional margin requirements mandated by the European regulators. There are no portfolio off-sets between individual CFD positions or between CFDs and exposures to the underlying share. Concentrated positions and very large positions may be subject to additional margin. Please refer to CFD Margin Requirements for more detail.

Are short Share CFDs subject to forced buy-in?

Yes. In the event the underlying stock becomes difficult or impossible to borrow, the holder of the short CFD position may become subject to buy-in.

How do you handle dividends and corporate actions?

IBKR will generally reflect the economic effect of the corporate action for CFD holders as if they had been holding the underlying security. Dividends are reflected as cash adjustments, while other actions may be reflected through either cash or position adjustments, or both. For example, where the corporate action results in a change of the number of shares (e.g. stock-split, reverse stock split), the number of CFDs will be adjusted accordingly. Where the action results in a new entity with listed shares, and IBKR decides to offer these as CFDs, then new long or short positions will be created in the appropriate amount. For an overview please CFD Corporate Actions.

*Please note that in some cases it may not be possible to accurately adjust the CFD for a complex corporate action such as some mergers. In these cases IBKR may terminate the CFD prior to the ex-date.

Can anyone trade IBKR CFDs?

All clients can trade IBKR CFDs, except residents of the USA, Canada, Hong Kong, New Zealand and Israel. There are no exemptions based on investor type to the residency based exclusions.

What do I need to do to start trading CFDs with IBKR?

You need to set up trading permission for CFDs in Client Portal, and agree to the relevant disclosures. If your account is with IBKR (UK) or with IBKR LLC, IBKR will then set up a new account segment (identified with your existing account number plus the suffix “F”). Once the set-up is confirmed you can begin to trade. You do not need to fund the F-account separately, funds will be automatically transferred to meet CFD initial margin requirements from your main account.

If your account is with another IBKR entity, only the permission is required; an additional account segment is not necessary.

Are there any market data requirements?

The market data for IBKR Share CFDs is the market data for the underlying shares. It is therefore necessary to have market data permissions for the relevant exchanges. If you already have market data permissions for an exchange for trading the shares, you do not need to do anything. If you want to trade CFDs on an exchange for which you do not currently have market data permissions, you can set up the permissions in the same way as you would if you planned to trade the underlying shares.

How are my CFD trades and positions reflected in my statements?

If you are a client of IBKR (U.K.) or IBKR LLC, your CFD positions are held in a separate account segment identified by your primary account number with the suffix “F”. You can choose to view Activity Statements for the F-segment either separately or consolidated with your main account. You can make the choice in the statement window in Client Portal.

If you are a client of other IBKR entities, there is no separate segment. You can view your positions normally alongside your non-CFD positions.

Can I transfer in CFD positions from another broker?

IBKR does not facilitate the transfer of CFD positions at this time.

Are charts available for Share CFDs?

Yes.

In what type of IBKR accounts can I trade CFDs e.g., Individual, Friends and Family, Institutional, etc.?

All margin and cash accounts are eligible for CFD trading.

What are the maximum a positions I can have in a specific CFD?

There is no pre-set limit. Bear in mind however that very large positions may be subject to increased margin requirements. Please refer to CFD Margin Requirements for more detail.

Can I trade CFDs over the phone?

No. In exceptional cases we may agree to process closing orders over the phone, but never opening orders.

Cash Sweeps

Background

Underlying the IB Universal account are two separate sub-accounts or segments, one for the securities positions and balances which are subject to the customer protection rules of the SEC and another for the commodities positions and balances which are subject to the customer protection rules of the CFTC. This Universal account structure is designed to minimize the administrative overhead that customers would otherwise be exposed to were they to maintain two distinct accounts (e.g., transferring of cash between accounts, login and order submission through separate accounts, multiple statements, etc.) while preserving the separation required by regulation.

These regulations further require that all securities transactions be effected and margined in the securities segment of the Universal account and commodities transactions in the commodities segment.1 While the regulations allow for the custody of fully-paid securities positions in the commodities segment as margin collateral, IB does not do so, thereby limiting their hypothecation to the more restrictive rules of the SEC. Given the regulations and policies which direct the decision to hold positions in one segment vs. the other, cash remains the only asset eligible to be transferred between the two and for which customer discretion is provided.

Outlined below is a discussion as to the cash sweep options offered, the process for selecting an option as well as selection considerations.

Cash Sweep Options

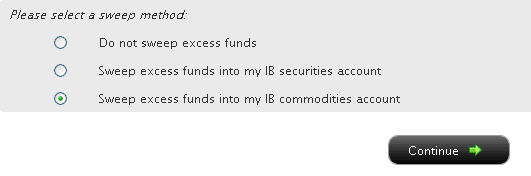

Customers are provided with 3 sweep options, descriptions for which are provided below:

1. Do not sweep excess funds – under this election, excess cash does not move from one segment to another unless necessary to:

a. Eliminate/reduce a margin deficiency in the other segment;

b. Minimize a cash debit balance and therefore interest charges in a given segment. Note that this is the default option and sole option for account holders having only one of securities or commodities trading permissions.

2. Sweep excess funds into my IB securities account – here, cash balances are only held in the commodities segment to the extent necessary to satisfy the current commodities margin requirement. Any cash in excess of the margin requirement, generated as a result of either an increase in cash (e.g., favorable variation and/or transaction related) or decrease in the margin requirement (e.g., changes in the SPAN risk arrays and/or transaction related) will be automatically transferred from the commodities segment to the securities segment. Note that the account holder must have permissions to trade securities in order to select this option.

3. Sweep excess funds into my IB commodities account – here, cash balances are only held in the securities segment to the extent that they, along with any other securities positions having loan value, are needed to satisfy the current securities margin requirement. Note that the account holder must have permissions to trade commodities in order to select this option.

Other items of note:

- As the Universal account allows for cash balances to be held in a variety of denominations, a hierarchy exists for the purpose of determining which particular currency to transfer first when long balances in multiple currencies exist. In these situations the procedure is to first transfer balances denominated in the Base Currency, then USD and then the remaining long currency balances in order of highest to lowest.

- To minimize the likelihood of one segment incurring a margin deficiency following the sweep of excess cash to the other, the full excess will not be transferred and a buffer equal to 5% of the maintenance margin requirement will be retained. Similarly, to minimize the operational overhead of transferring nominal balances, balances will only be transferred if, after giving effect to the 5% margin cushion, the excess, if any, is not less than 1% of account equity or $200.

- When performing the pre-trade credit check to determine whether an account maintains sufficient equity to support a new order, excess cash maintained in one segment will be considered for trades conducted in the other (although a sweep will not occur until the trade has executed and only if it then remains necessary for margin compliance). Accounts which are designated as a Pattern Day Trader and which are subject pre-trade credit check that takes into account the prior as well as current day's equity should pay particular attention to the Selection Considerations section below.

Selecting a Sweep Option

If your Account Management version contains a series of menu options on the left-hand side, select the Account Administration and then Excess Funds Sweep menu options. If your version has menu options across the top, select the Manage Account/Settings and then the Configure Account/Excess Funds Sweep menu options. Regardless of your version, you will be presented with a screen which appears as follows:

You may then select the radio button alongside the option of your choice and select the Continue button. Your choice will take effect as of the next business day and will remain in effect until a different option has been selected. Note that subject to the trading permission settings noted above, there is no restriction upon when or how often you may change your sweep method.

Selection Considerations

While the decision to elect one segment vs. the other for the purposes of maintaining excess cash may involve subjective decisions and preferences unique to each customer (e.g. customer maintains assets which are significant and concentrated in one segment vs. the other), outlined below are several factors warranting consideration:

1. Pattern Day Trading Equity - The securities buying power of accounts designated by regulation as Pattern Day Traders (i.e., 4 or more day trades within a 5 business day period) is limited by the lesser of the current or prior day’s closing equity in the securities segment. As such, an election to sweep excess funds to the commodities segment will prevent the inclusion of such funds in this calculation, thereby potentially limiting the capacity to enter new orders. To maximize the use of equity for purposes of entering securities orders, one would need to elect to sweep excess fund to the securities segment. Note that an election to the securities segment will not impair the ability to enter commodities orders as the pattern day trading rules do not apply to such accounts.

2. Insurance – SIPC protection is afforded to assets in the securities segment and there is no commensurate insurance scheme in place for the commodities segment. That being said, balances in excess of the SIPC $250,000 cash sub-limit ($900,000 Lloyd’s cash sub-limit, where applicable) are not afforded coverage. Customers of IB Canada and IB UK are also subject coverage rules as specified by CIPF and the FSCS, respectively.

3. Interest Income – all other things being equal, customers are likely to receive the most optimal interest income on long cash balances that have not been partitioned between the securities and commodities segments as they are not aggregated for interest credit purposes (since they are subject to distinct segregation pools and reinvestment rules). This, along with the fact that credits require maintenance of a minimum cash balance and that higher balances are afforded preferential rates are factors to be considered when making a sweep election.2

Other Relevant Knowledge Base Articles:

A Comparison of U.S. Segregation Models

A Comparison of U.S. Segregation Models

Footnotes:

1As OneChicago single stock futures are a hybrid product jointly regulated by the SEC and CFTC, they can be purchased and sold in either account type. IB, however, conducts such transactions in the securities segment of the Universal account as this is necessary to provide margin relief between the single stock future and any qualifying stock or option position.

2Consider, for example, an account which maintains a long USD balance of $9,000 in each of the securities and commodities segments. Depending upon the benchmark Fed Funds Effective rate, the account would be eligible to earn interest on $8,000 ($18,000 - $10,000) if the two balances were held in a single segment, but since balances below $10,000 in either of the two segments are not eligible for interest, could not earn anything without electing a sweep option. Similarly, one would be eligible to earn interest at a higher tier if as a result of a sweep election the account holder was then able to achieve a long USD cash balance above $100,000 in a given segment. For additional information regarding interest calculations including a link to current benchmark interest rates, refer to KB39.

Why does the "price" on hard to borrow stocks not agree to the closing price of the stock?

In determining the cash deposit required to collateralize a stock borrow position, the general industry convention is for the lender to require a deposit equal to 102% of the prior business day's** settlement price, rounded up to the nearest whole dollar and then multiplied by the number of shares borrowed. As borrow rates are determined based upon the value of the loan collateral, this convention impacts the cost of maintaining the short position, with the impact being most significant in the case of low-priced and hard-to-borrow shares. Note, for shares not denominated in USD the calculation will differ. Find below a table summarizing the calculations per currency:

| Currency | Calculation Method |

| USD | 102%; rounded up to the nearest dollar |

| CAD | 102%; rounded up to the nearest dollar |

| EUR | 105%; rounded up to the nearest cent |

| CHF | 105%; rounded up to the nearest rappen |

| GBP | 105%; rounded up to the nearest pence |

| HKD | 105%; rounded up to the nearest cent |

For US Treasuries and corporate bonds, the collateral amount on which the borrow fee is charged will include the accrued interest.

Account holders may view this adjusted price for a given transaction in the "Borrow Fee Details" section of the daily account statement. Two examples of this collateral calculation and its impact upon borrow fees are provided below.

Example 1

Sell short 100,000 shares of ABC at a price of $1.50

Short sale proceeds received = $150,000.00

Assume the price of ABC falls to $0.25 and the stock has a borrow fee rate of 50%

Short stock collateral value calculation

Price = 0.25 x 102% = 0.255; round up to $1.00

Value = 100,000 shares x $1.00 = $100,000.00

Borrow fee = $100,000 x 50% / 360 days in year = $138.89 per day

Assuming the account holder's cash balance does not include proceeds from any other short sale transaction then this borrow fee will not be offset by any credit interest on the short sale proceeds as the balance does not exceed the minimum $100,000 Tier 1 threshold necessary to accrue interest.

Example 2 (EUR denominated stock)

Sell short 100,000 shares of ABC at a price of EUR 1.50

Assume a prior business day's close price of EUR 1.55 and a borrow fee rate of 50%

Short stock collateral value calculation

Price = EUR 1.55 x 105% = 1.6275; round up to EUR 1.63

Value = 100,000 shares x 1.63 = $163,000.00

Borrow fee = EUR 163,000 x 50% / 360 days in year = EUR 226.38 per day

** Please note, Saturdays and Sundays are treated as a Friday and will use Thursday's settlement price to calculate the required deposit.

Interest Benchmark Definitions

Fed Funds Effective (USD only) is the volume weighted average of the transactions processed through the Federal Reserve between member banks. It is intended to reflect the best estimate of interbank financing activity for Reserve Bank members and is the reference for many short term money market transactions in the broader market.

EONIA (EUR only) is the global standard for overnight Euro deposits and is determined by a weighted average of the actual transactions between major continental European banks mediated through the European Central Bank.

HIBOR (CNY and HKD) is a daily fixing based on a group of large Hong Kong banks.

KORIBOR (KRW only) is an average of the leading interest rates for KRW as determined by a group of large Korean banks. The benchmark utilizes the KORIBOR with 1 week maturity.

STIBOR (SEK only) is a daily fixing based on a group of large Swedish banks.

TIIE (MXN only) is the interbank "equilibrium" rate based on the quotes provided by money center banks as calculated by the Mexican Central Bank. The benchmark TIIE is based on 28-day deposits so is atypical as a measure for short term funds (most currencies have an overnight or similar short term benchmark).

Overnight (O/N - CZK, HUF, ILS and SGD) rate is the most widely used short term benchmark and represents the rate for balances held from today until the next business day.

Spot-Next (S/N - DKK only) refers to the rate on balances from the next business day to the business day thereafter. Due to time zone and other criteria, Spot-Next rates are sometimes used as the short-term reference.

Day-Count conventions: it is beyond the scope of this document to describe day-count conventions and their use in interest calculations. IBKR conforms to the international standards for day-counting wherein deposits rates for most currencies are expressed in terms of a 360 day year, while for exceptional currencies (ex: GBP) the convention is a 365 day year.

Understanding interest charges when the net cash balance is a credit

An account will be subject to interest charges despite maintaining an overall net long or credit cash balance under the following circumstances:

1. The account maintains a short or debit balance in a given currency.

For example, an account maintaining a net cash credit balance equivalent to USD 5,000 comprised of a long USD balance of 8,000 and a short EUR balance equivalent to USD 3,000 would be subject to an interest debit based upon the short EUR balance. There would be no offsetting credit on the long USD balance as it is less than the USD 10,000 Tier I level above which interest is earned.

Account holders should note that in the event they purchase a security which is denominated in a currency that they do not hold in their account, IBKR will create a loan in that currency in order to settle the trade with the clearinghouse. If one wishes to avoid such loans and their associated interest charges, they would need to either deposit funds denominated in that particular currency or convert existing cash balances via the Ideal Pro (for balances of USD 25,000 or above) or odd lot (for balances less than USD 25,000) venue prior to entering into your trade.

2. The credit balance is comprised principally of proceeds from the short sale of securities.

For example, an account maintaining a net cash credit balance of USD 12,000 which is comprised of a USD debit of 6,000 in the security sub-account (less the market value of any short stock positions) and a short stock market value credit of USD 18,000 would be charged interest on the Tier 1 debit of USD 6,000 and would earn no interest on the short stock credit as it falls below the USD 100,000 Tier I level.

3. The credit balance includes unsettled funds.

IBKR determines interest debits and credits solely based upon settled funds. Just as an account holder is not assessed interest charges on funds borrowed to purchase a security until such time that purchase transaction settles, the account holder will not receive an interest credit, or offset against a debit balance, on funds originating from the sale of a security until such time the transaction has settled (and IBKR has been credited funds by the clearinghouse).

Are there any particular risks that one should be aware of when using SSFs to either invest excess funds or borrow funds at available synthetic rates?

Overview:

While the High and Low Synthetic strategies are both hedged positions, the futures leg is subject to a daily cash variation of the mark-to-market gain or loss whereas the stock leg is not (mark-to-market gain or loss is reflected in account equity but there is no cash impact until the position is closed). If, for example, an account holds a High Synthetic position and the stock prices increases significantly, the resultant variation pay on the short futures leg may erode the account’s cash balance resulting in a debit balance which is subject to interest payments. The net effect in this example would be to reduce and potentially erase the earnings on the High Synthetic position

Does a deposit subject to a "Credit Hold” accrue credit interest during the hold period?

Overview:

The answer depends upon the method of deposit. In the case of deposits made via ACH, any interest accrues from the date the deposit arrives through the four-business day credit hold period after which it is credited to the account. In the case of check deposits other than Bank Checks, no interest is accrued during the credit hold period. Bank Checks and wire transfers are credited to the account effective upon receipt and are therefore not subject to any credit hold.

Interest paid to you varies with market conditions. For information regarding the amount of interest currently paid on credit balances see www.interactivebrokers.com/interest

Glossary terms:

What does the Interest Accrual Reversal line item on the Activity Statement represent?

Overview:

Each day, IBKR calculates and reports in the Interest Accruals section of the Activity Statement a forecast or accrual of interest earned or to be paid for the statement period. Around the first week of each month the interest which has been accrued during the prior month is "backed-out" or reversed and actual interest for the month is posted in the Cash Report section. These reversals, which occur once a month, should be close to the actual interest, although they may not always be exactly equal since accruals are a forecast of actual interest.

Account holders should also note that accrued interest is only posted for any given reporting period when the amount exceeds $1, either positive or negative. Balances below $1 are retained and posted once, when aggregated with future accruals, the amount exceeds $1.