Panoramica sulle metodologie relative al margine

Introduzione

La metodologia usata per calcolare il requisito di margine per una data posizione viene in larga parte stabilita attraverso i seguenti tre fattori:

1. Il tipo di prodotto;

2. Le regole della borsa presso il quale il prodotto è quotato e/o l’ente regolatore principale per il broker;

3. I requisiti fissati da IBKR.

In genere le varie metodologie esistenti possono essere classificate in due approcci: uno basato sulle regole e l’altro basato sul rischio. I metodi basati sul rischio di solito ipotizzano tassi di margine uniformi su prodotti simili, non offrono compensazioni intra-prodotto e infine considerano gli strumenti derivati in maniera simile a quella dei relativi sottostanti. In questo senso i metodi basati sul rischio offrono il vantaggio di una facilità di calcolo che si basa pero su ipotesi che, seppure facili da eseguire, potrebbero sovrastimare o sottostimare il rischio che di uno strumento rispetto alla sua performance passata. Un esempio comune di metodologia basata sulle regole è il requisito Reg. T applicato negli USA.

Per contro, attraverso le metodologie basate sul rischio si tenta spesso di applicare una copertura di margine che rifletta la performance passata di un prodotto. Vengono riconosciute alcune compensazioni intra-prodotto e si cerca di prevedere il rischio non lineare dei prodotti derivati attraverso l’utilizzo di modelli matematici sul prezzo. Sebbene siano intuitive, queste metodologie richiedono dei calcoli di non facile riproduzione da parte del cliente. Inoltre, dato che i loro imput dipendono da comportamenti di mercato osservati, questo potrebbe portare a dei requisiti soggetti ad una fluttuazione rapida e considerevole. Esempi di metodologie basate sul rischio includo TIMS e SPAN.

Indipendentemente dal tipo di metodologia usata, la maggior parte dei broker applicherà un margine “della casa” che serve ad aumentare il requisito previsto dalla normativa o quello di base in specifiche circostanze laddove l’esposizione del broker è più grande di quella che normalmente sarebbe soddisfatta dal semplice rispetto del requisito di base. Qui di seguito viene fornita una panoramica delle più comuni metodologie basate sulle regole e sul rischio.

Panoramica delle metodologie

In base al rischio

a. Margine di Portafoglio (TIMS) – Il TIMS (Theoretical Intermarket Margin System) è una metodologia basata sul rischio creata dalla Options Clearing Corporation (OCC) e calcola il valore di un portafoglio dati una serie di scenari di mercato ipotetici nei quali si immaginano variazioni di prezzo e le posizioni vengono rivalutate. Questa metodologia ricorre ad un modello di prezzo relativo alle opzioni per rivalutarle e agli scenari della OCC si aggiunge un certo numero di scenari ipotizzati dal broker che servono a catturare ulteriori rischi come movimenti di mercato estremi, concentrazione di posizioni e spostamenti in termini di volatilità implicita delle opzioni. Inoltre ci sono alcuni tipi di titoli (es. Pink Sheet, OTCBB e titoli a bassa capitalizzazione) per i quali il margine non può essere ampliato. Una volta stabilite le proiezioni relative ai valori del portafoglio per ciascuno scenario, verrà stabilito il requisito di margine in base allo scenario che in proiezione ha generato la perdita più grande.

Le posizioni per le quali si può applicare la metodologia TIMS includono titoli USA, ETF, opzioni, future su singole azioni, titoli che non appartengono al mercato statunitense e opzioni che rispettano il test ready market della SEC.

Dato che per questa metodologia di mercato si ricorre ad una serie di calcoli ancora più complessi di quelli presenti nella metodologia basata sulle regole, vi è una tendenza a prevedere in maniera più accurata il rischio e in genere viene offerta una leva maggiore. Considerata l’abilità di offrire una leva potenziata e visto che i requisiti fluttuano e potrebbero reagire rapidamente alle mutevoli condizioni del mercato, questa metodologia è indicata per investitori individuati molto esperti e richiede un capitale minimo di 110.000 USD per iniziare e 100.000 USD per il mantenimento. I requisiti per i titoli in questa metodologia vanno in genere dal 15 al 30%. Il requisito più favorevole viene applicato ai portafogli che contengono un gruppo di titoli altamente diversificato e che hanno storicamente mostrato una bassa volatilità e che tendono a impiegare opzioni hedge.

b. Lo SPAN (Standard Portfolio Analysis of Risk) è una metodologia basata sul rischio create dal Chicago Mercantile Exchange (CME) e progettata per future e opzioni future. In maniera simile al TIMS, lo SPAN stabilisce il requisito di margine attraverso calcolando il valore del portafoglio considerando una serie di scenari di mercato ipotetici nei quali il prezzo del sottostante cambia e si ipotizza la volatilità implicita delle opzioni. Anche in questo caso, IBKR includerà tra queste ipotesi anche alcuni scenari che tengono conto di movimenti di prezzo estremi oltre a l’impatto specifico queste variazioni potrebbero avere sulle opzioni “deep out-of-the-money”. In base allo scenario nel quale si prevede la perdita più grande verrà fissato il requisito di margine. Una panoramica dettagliata del sistema di marginazione con SPAN viene illustrato in questo articolo: KB563.

In base alle regole

a. Reg. T – La banca centrale americana, ossia la Federal Reserve Board, ha la responsabilità di mantenere la stabilità del sistema finanziario e contenere il rischio sistemico che potrebbe emergere nei mercati finanziari. A questo scopo la Fed opera regolando l’importo del credito che i broker dealer possono offrire ai clienti che prendono denaro in prestito per acquistare titoli a margine.

Per questo motivo viene usato la Regulation T, comunemente detta Reg. T, nella quale si dispone che venga stabilito un conto a margine e che fissa le regole relative al margine iniziale e al pagamento sulle transazioni per determinati tipi di titoli. Ad esempio, nel caso dell’acquisto di azioni, la Reg. T attualmente richiede il versamento di un margine iniziale da parte del cliente pari al 50% del valore dell’acquisto, consentendo al broker di estendere un credito o un finanziamento parti al restante 50%. Esempio: il titolare di un conto che decida di acquistare 1.000 USD di titoli avrà l’obbligo di versare 500 USD e gli sarà consentito di ottenere un prestito pari a 500 USD per detenere i titoli in questione.

La Reg. T stabilisce il requisito di margine iniziale e il margine di mantenimento, ossia l’importo necessario per continuare a detenere una posizione dopo l’apertura. Tale margine viene fissato in genere dalla borsa (25% per le azioni). La Reg. T inoltre non stabilisce i requisiti di margine per le opzioni in quanto queste rientrano nella competenza giurisdizionale delle regole delle differenti borse, a loro volta soggette all’approvazione della SEC. Le opzioni detenute in un conto Reg. T saranno inoltre soggette ad una metodologia fissata in base alle regole che stabilisce quanto segue: le posizioni short verranno trattate come equivalenti alle azioni e verrà fornita un’esenzione dalle regole per il margine in caso di transazioni spread. Infine le posizioni detenute nel portafoglio di un conto a margine ritenuto idoneo saranno esenti dai requisiti della Reg. T.

Per saperne di più

Definizioni chiave relative ai margini

Strumenti forniti per osservare e gestire il margine

Come stabilire il potere d'acquisto

Come stabilire se stai operando con fondi ottenuti in prestito tramite IBKR

Perché IBKR calcola e segnale il requisito di margine quando non ricevo fondi in prestito?

Anteprima ordine - Controllo impatto commissione di esposizione

IB permette ai titolari del conto di verificare l'eventuale impatto di un ordine sulla Commissione di esposizione attesa mediante una funzionalità pensata per un utilizzo prima dell'inoltro dell'ordine. Tale funzionalità fornisce un preavviso di commissione grazie al quale è possibile modificare l'ordine prima della sua trasmissione e diminuire o annullare la commissione stessa.

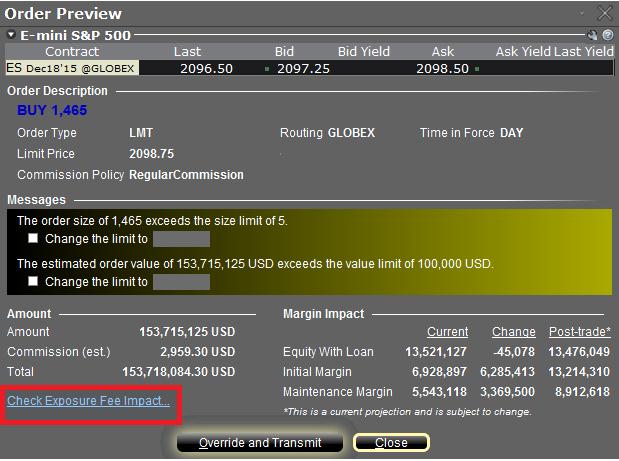

Per attivare questa funzionalità è necessario cliccare con il pulsante destro del mouse sulla riga dell'ordine, dopodiché si aprirà la finestra Anteprima ordine contenente un link denominato "Controllo impatto commissione di esposizione" (si veda il riquadro evidenziato in rosso nella Figura I qui di seguito).

Figura I

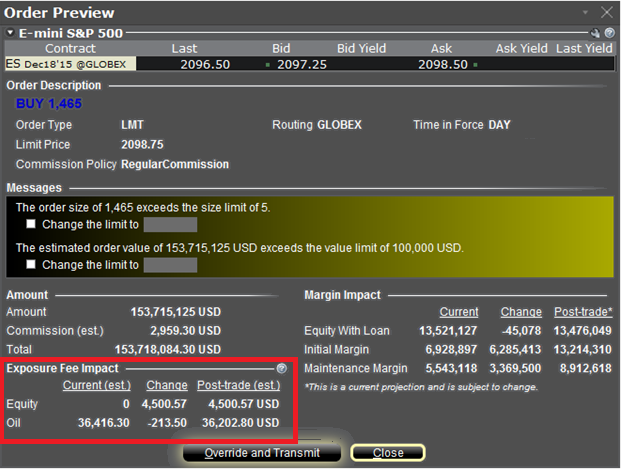

Cliccando sul link si aprirà una finestra raffigurante l'eventuale Commissione di esposizione associata alle posizioni esistenti, la variazione della commissione in caso di ordine processato e la commissione totale risultante una volta processato l'ordine (si veda il riquadro evidenziato in rosso nella Figura II qui di seguito). I saldi sono suddivisi ulteriormente per categoria di prodotto alla quale le commissioni si applicano (es. azioni, petrolio). I titolari del conto possono chiudere la finestra senza inoltrare l'ordine qualora ritengano l'impatto della commissione eccessivo.

Figura II

Si veda l'articolo KB2275 per informazioni sull'utilizzo di Risk Navigator relative alla gestione e alla stima della Commissione di esposizione e il KB2344 per il monitoraggio delle commissioni mediante la Finestra conto

Utilizzo di Risk Navigator per la stima delle commissioni di esposizione

Lo strumento Risk Navigator di IB prevede una funzionalità di scenario personalizzato per poter determinare l'eventuale effetto delle variazioni del proprio portafoglio sulla commissione di esposizione. Di seguito sono elencati i passaggi per creare un portafoglio “What–If”, o mediante variazioni ipotetiche a un portafoglio esistente o tramite un portafoglio completamente nuovo, e calcolarne la commissione. Si ricorda che questa funzionalità è disponibile tramite TWS 951 e versioni successive.

Punto 1: apertura di un nuovo portafoglio “What-if”

Dalla piattaforma di trading TWS classica selezionare le opzioni del menu Strumenti di analisi, Risk Navigator e Apri nuovo What-If (Figura 1).

Figura 1

.jpg)

Punto 2: scelta del portafoglio iniziale

Apparirà una finestra pop-up (Figura 2) che richiede di indicare se si desidera creare un portafoglio ipotetico a partire dal proprio portafoglio esistente oppure crearne uno nuovo. Cliccando sul pulsante "Sì" è possibile scaricare le posizioni esistenti nel nuovo portafoglio “What-If”.

Figura 2

.png)

Cliccando sul pulsante "No" si aprirà il portafoglio “What – If” privo di posizioni (Figura 3). Selezionare la voce associata alla categoria del prodotto per cui si desidera creare posizioni ipotetiche (es. Capitale proprio).

Exhibit 3

.jpg)

Punto 3: aggiunta di nuove posizioni

Per aggiungere posizioni al portafoglio "What - If" è necessario cliccare sulla cella verde denominata "Nuova" e premere il simbolo sottostante (Figura 4), scegliere la categoria di prodotto (Figura 5) e inserire la quantità della posizione (Figura 6)

Figura 4

.jpg)

Figura 5

.jpg)

Figura 6

.jpg)

Punto 4: calcolo della commissione di esposizione

Per visualizzare la commissione di esposizione attesa in base al proprio portafoglio “What-If” è necessario cliccare sulle opzioni del menu Report e Commissione di esposizione (Figura 7). Apparirà una finestra pop-up raffigurante la commissione di esposizione attesa suddivisa per categoria di prodotto (Figura 8).

Figura 7

.jpg)

Figura 8

.jpg)

Si veda l'articolo KB2344 per informazioni sul monitoraggio della commissione di esposizione mediante la Finestra conto e il KB2276 per verificare la commissione di esposizione attraverso la schermata Anteprima ordine.

Order Preview - Check Exposure Fee Impact

IB provides a feature which allows account holders to check what impact, if any, an order will have upon the projected Exposure Fee. The feature is intended to be used prior to submitting the order to provide advance notice as to the fee and allow for changes to be made to the order prior to submission in order to minimize or eliminate the fee.

The feature is enabled by right-clicking on the order line at which point the Order Preview window will open. This window will contain a link titled "Check Exposure Fee Impact" (see red highlighted box in Exhibit I below).

Exhibit I

Clicking the link will expand the window and display the Exposure fee, if any, associated with the current positions, the change in the fee were the order to be executed, and the total resultant fee upon order execution (see red highlighted box in Exhibit II below). These balances are further broken down by the product classification to which the fee applies (e.g. Equity, Oil). Account holders may simply close the window without transmitting the order if the fee impact is determined to be excessive.

Exhibit II

Please see KB2275 for information regarding the use of IB's Risk Navigator for managing and projecting the Exposure Fee and KB2344 for monitoring fees through the Account Window

Important Notes

1. The Estimated Next Exposure Fee is a projection based upon readily available information. As the fee calculation is based upon information (e.g., prices and implied volatility factors) available only after the close, the actual fee may differ from that of the projection.

2. The Check Exposure Fee Impact is only available for accounts that have been charged an exposure fee in the last 30 days

Using Risk Navigator to Project Exposure Fees

Overview:

IB's Risk Navigator provides a custom scenario feature which allows one to determine what effect, if any, changes to their portfolio will have to the Exposure fee. Outlined below are the steps for creating a “what-if” portfolio through assumed changes to an existing portfolio or through an entirely new proposed portfolio along with determining the resultant fee. Note that this feature is available through TWS build 971.0i and above.

Step 1: Open a new “What-if” portfolio

From the Classic TWS trading platform, select the Analytical Tools, Risk Navigator, and then Open New What-If menu options (Exhibit 1).

Exhibit 1

.png)

From the Mosaic TWS trading platform, select the New Window, Select Risk Navigator, and then Open New What-If menu options.

Step 2: Define starting portfolio

A pop-up window will appear (Exhibit 2) from which you will be prompted to define whether you would like to create a hypothetical portfolio starting from your current portfolio or a newly created portfolio. Clicking on the "yes" button will serve to download existing positions to the new “What-If” portfolio.

Exhibit 2

.png)

Clicking on the "No" button will open up the “What-If” Portfolio with no positions.

Step 3: Add Positions

To add a position to the “what-if” portfolio, click on the green row titled "New" and then enter the underlying symbol (Exhibit 3), define the product type (Exhibit 4) and enter position quantity (Exhibit 5).

Exhibit 3

.png)

Exhibit 4

.png)

Exhibit 5

.png)

You can modify the positions to see how that changes the margin. After you altered your positions you will need to click on the recalculate icon ( ) to the right of the margin numbers in order to have them update. Whenever that icon is present the margin numbers are not up-to-date with the content of the “what-if” Portfolio.

) to the right of the margin numbers in order to have them update. Whenever that icon is present the margin numbers are not up-to-date with the content of the “what-if” Portfolio.

Step 4: Determine Exposure Fee

To view the projected correlated exposure fee based upon your “what-if” portfolio, click on the Report and then Exposure Fee menu options (Exhibit 6). Once selected, a new Exposure Fee tab will be added, which will display the projected exposure fee broken down by primary risk factors (Exhibit 7).

Exhibit 6

.png)

Exhibit 7

.png)

You can modify the positions to see how that changes the Exposure Fee. After you altered your positions you will need to click on the refresh button to the right of the Last Calculation Time. Whenever the warning icon ( ) is present the Exposure Fee Calculations numbers are not up-to-date with the content of the “what-if” Portfolio.

) is present the Exposure Fee Calculations numbers are not up-to-date with the content of the “what-if” Portfolio.

Please see KB2344 for information on monitoring the Exposure fee through the Account Window and KB2276 for verifying exposure fee through the Order Preview screen.

Important Note

1. The on-demand Exposure Fee check represents a projection based upon readily available information. As the fee calculation is based upon information (e.g., prices and implied volatility factors) available only after the close, the actual fee may differ from that of the projection.

Overview of Margin Methodologies

Introduction

The methodology used to calculate the margin requirement for a given position is largely determined by the following three factors:

1. The product type;

2. The rules of the exchange on which the product is listed and/or the primary regulator of the carrying broker;

3. IBKR’s “house” requirements.

While a number of methodologies exist, they tend to be categorized into one of two approaches: rules based or risk based. Rules based methods generally assume uniform margin rates across like products, offer no inter-product offsets and consider derivative instruments in a manner similar to that of their underlying. In this sense, they offer ease of computation but oftentimes make assumptions which, while simple to execute, may overstate or understate the risk of an instrument relative to its historic performance. A common example of a rules based methodology is the U.S. based Reg. T requirement.

In contrast, risk based methodologies often seek to apply margin coverage reflective of the product’s past performance, recognize some inter-product offsets and seek to model the non-linear risk of derivative products using mathematical pricing models. These methodologies, while intuitive, involve computations which may not be easily replicable by the client. Moreover, to the extent that their inputs rely upon observed market behavior, may result in requirements that are subject to rapid and sizable fluctuation. Examples of risk based methodologies include TIMS and SPAN.

Regardless of whether the methodology is rules or risk based, most brokers will apply “house” margin requirements which serve to increase the statutory, or base, requirement in targeted instances where the broker’s view of exposure is greater than that which would satisfied solely by meeting that base requirement. An overview of the most common risk and rules based methodologies is provided below.

Methodology Overview

Risk Based

a. Portfolio Margin (TIMS) – The Theoretical Intermarket Margin System, or TIMS, is a risk based methodology created by the Options Clearing Corporation (OCC) which computes the value of the portfolio given a series of hypothetical market scenarios where price changes are assumed and positions revalued. The methodology uses an option pricing model to revalue options and the OCC scenarios are augmented by a number of house scenarios which serve to capture additional risks such as extreme market moves, concentrated positions and shifts in option implied volatilities. In addition, there are certain securities (e.g., Pink Sheet, OTCBB and low cap) for which margin may not be extended. Once the projected portfolio values are determined at each scenario, the one which projects the greatest loss is the margin requirement.

Positions to which the TIMS methodology is eligible to be applied include U.S. stocks, ETFs, options, single stock futures and Non U.S. stocks and options which meet the SEC’s ready market test.

As this methodology uses a much more complex set of computations than one that is rules based, it tends to more accurately model risk and generally offers greater leverage. Given its ability to offer enhanced leverage and that the requirements fluctuate and may react quickly to changing market conditions, it is intended for sophisticated individuals and requires minimum equity of $110,000 to initiate and $100,000 to maintain. Requirements for stocks under this methodology generally range from 15% to 30% with the more favorable requirement applied to portfolios which contain a highly diversified group of stocks which have historically exhibited low volatility and which tend to employ option hedges.

b. SPAN – Standard Portfolio Analysis of Risk, or SPAN, is a risk-based margin methodology created by the Chicago Mercantile Exchange (CME) that is designed for futures and future options. Similar to TIMS, SPAN determines a margin requirement by calculating the value of the portfolio given a set of hypothetical market scenarios where underlying price changes and option implied volatilities are assumed to change. Again, IBKR will include in these assumptions house scenarios which account for extreme price moves along with the particular impact such moves may have upon deep out-of-the-money options. The scenario which projects the greatest loss becomes the margin requirement. A detailed overview of the SPAN margining system is provided in KB563.

Rules Based

a. Reg. T – The U.S. central bank, the Federal Reserve Board, holds responsibility for maintaining the stability of the financial system and containing systemic risk that may arise in financial markets. It does this, in part, by governing the amount of credit that broker dealers may extend to customers who borrow money to buy securities on margin.

This is accomplished through Regulation T, or Reg. T as it is commonly referred, which provides for establishment of a margin account and which imposes the initial margin requirement and payment rules on certain securities transactions. For example, on stock purchases, Reg. T currently requires an initial margin deposit by the client equal to 50% of the purchase value, allowing the broker to extend credit or finance the remaining 50%. For example, an account holder purchasing $1,000 worth of securities is required to deposit $500 and allowed to borrow $500 to hold those securities.

Reg. T only establishes the initial margin requirement and the maintenance requirement, the amount necessary to continue holding the position once initiated, is set by exchange rule (25% for stocks). Reg. T also does not establish margin requirements for securities options as this falls under the jurisdiction of the listing exchange’s rules which are subject to SEC approval. Options held in a Reg.T account are also subject to a rules based methodology where short positions are treated like a stock equivalent and margin relief is provided for spread transactions. Finally, positions held in a qualifying portfolio margin account are exempt from the requirements of Reg. T.

Where to Learn More

Tools provided to monitor and manage margin

How to determine if you are borrowing funds from IBKR

Why does IBKR calculate and report a margin requirement when I am not borrowing funds?

Margin Requirement on Leveraged ETF Products

Leveraged Exchange Traded Funds (ETFs) are a subset of general ETFs and are intended to generate performance in multiples of that of the underlying index or benchmark (e.g. 200%, 300% or greater). In addition, some of these ETFs seek to generate performance which is not only a multiple of, but also the inverse of the underlying index or benchmark (e.g., a short ETF). To accomplish this, these leveraged funds typically include among their holdings derivative instruments such as options, futures or swaps which are intended to provide the desired leverage and/or inverse performance.

Exchange margin rules seek to recognize the additional leverage and risk associated with these instruments by establishing a margin rate which is commensurate with that level of leverage (but not to exceed 100% of the ETF value). Thus, for example, whereas the base strategy-based maintenance margin requirement for a non-leveraged long ETF is set at 25% and a short non-leveraged ETF at 30%, examples of the maintenance margin change for leveraged ETFs are as follows:

1. Long an ETF having a 200% leverage factor: 50% (= 2 x 25%)

2. Short an ETF having a 300% leverage factor: 90% (= 3 x 30%)

A similar scaling in margin is also in effect for options. For example, the Reg. T maintenance margin requirement for a non-leveraged, short broad based ETF index option is 100% of the option premium plus 15% of the ETF market value, less any out-of-the-money amount (to a minimum of 10% of ETF market value in the case of calls and 10% of the option strike price in the case of puts). In the case where the option underlying is a leveraged ETF, however, the 15% rate is increased by the leverage factor of the ETF.

In the case of portfolio margin accounts, the effect is similar, with the scan ranges by which the leveraged ETF positions are stress tested increasing by the ETF leverage factor. See NASD Rule 2520 and NYSE Rule 431 for further details.

What happens if the net liquidating equity in my Portfolio Margining account falls below USD 100,000?

Overview:

Portfolio Margining accounts reporting net liquidating equity below USD 100,000 are limited to entering trades which serve solely to reduce the margin requirement until such time as either: 1) the equity increases to above 100,000 or 2) the account holder requests a downgrade to Reg T style margining through Client Portal (select the Settings, Account Settings, Configure and Account Type menu options).

If a Portfolio Margining eligible account reporting net liquidating equity below USD 100,000 enters an order which, if executed, would serve to increase the margin requirement, the following TWS message will be displayed: "Your order is not accepted, margin requirement increase not allowed. Equity with loan value is less than 100,000.00 USD."

IMPORTANT NOTICE

Please note that requests to downgrade to Reg. T will become effective the following business day if submitted prior to 4:00 ET. Also note that as the Reg. T margining methodology generally affords less leverage than does Portfolio Margining, requesting a downgrade may lead to the automatic liquidation of positions in your account in order to comply with Reg. T. You will receive a warning message if that is the case at the time you request the downgrade.

-->

What positions are eligible for Portfolio Margining?

Overview:

Portfolio Margining is eligible for US securities positions including stocks, ETFs, stock and index options and single stock futures. It does not apply to US futures or futures options positions or non-US stocks, which may already be margined using an exchange approved risk based margining methodology.