Key Information Documents (KID)

概観:

IBKR is required to provide EEA and UK retail customers with Key Information Documents (KID) for certain financial instruments.

Relevant products include ETFs, Futures, Options, Warrants, Structured Products, CFDs and other OTC products. Funds include both UCITS and non-UCITS funds available to retail investors.

Generally KIDs must be provided in an official language of the country in which a client is resident.

However, clients of IBKR have agreed to receive communications in English, and therefore if a KID is available in English all EEA and UK clients can trade the product regardless of their country of residence.

In cases where a KID is not available in English, IBKR additionally supports other languages as follows:

| Language | Can be traded by residents or citizens* of |

| German | Germany, Austria, Belgium, Luxembourg and Liechtenstein |

| French | France, Belgium and Luxembourg |

| Dutch | the Netherlands and Belgium |

| Italian | Italy |

| Spanish | Spain |

*regardless of country of residence

IBKR(UK)におけるESMAルール導入の概要 - 個人投資家のみ対象

概観:

|

CFDはレバレッジによる損失のリスクが高い複雑な商品です。

63.7%の個人投資家口座に、IBKRとのCFD取引による損失が発生しています。

お取引を開始される前にCFDの機能、また損失の際のリスクをご理解ください。 |

欧州証券市場監督局(ESMA)は、CFDを取引する個人投資家に対し、2018年8月1日より適用となるルールを実施しました。特定投資家のお客様への影響はありません。

ルールの構成は以下のようになります: 1) レバレッジの上限、 2) 口座単位のマージン・クローズアウト、 3) 口座単位のマイナス残高の保護、 4) CFD取引に対するインセンティブの制限、 5) リスク警告の標準化。

ほとんどのお客様は(規制対象となる事業体以外)まず個人投資家に分類されます。IBKRでは、場合によっては個人投資家のお客様を特定投資家に、または特定投資家のお客様を個人投資家に再分類することがあります。詳細は、MiFID分類基準をご覧ください。

下記の項目では、IBKR(UK)におけるESMAルールの導入に関してご説明しています。

1 レバレッジの上限

1.1 ESMA証拠金

レバレッジの上限は、原資産によって違うレベルにESMAが設定しています:

- 主要な通貨ペアには3.33%。USD、CAD、EUR、GBP、CHF、JPYの組み合わせは、すべて主要な通貨ペアとなります。

- 主要ではない通貨ペアおよび主要な指数には5%。

- 主要ではない通貨ペアはUSD.CNHなどの、上に記載されない通貨を組み合わせたペアとなります。

- 主要な指数は、IBUS500、IBUS30、IBUST100、IBGB100、IBDE40、IBEU50、IBFR40、IBJP225、IBAU200になります。

- 主要ではない株式指数には10%。IBES35、IBCH20、IBNL25、IBHK50

- 個別株式には20%。

1.2適用となる証拠金 - 標準要件

IBKR(UK)ではESMA証拠金に加え、原資産の過去の変動やその他の要因に基づいて、自社の証拠金(IB証拠金)を設定しています。 IB証拠金はESMAの設定によるものを上回る場合に適用されます。

適用となるIBおよびESMAの証拠金に関する詳細は、こちらよりご確認下さい。

1.2.1適用となる証拠金 - 最低コンセントレーション

ポートフォリオが少量のCFDからなる場合、または最も大きいポジションふたつのウェイトが優勢な場合には、コンセントレーション・チャージが適用されます。弊社では、最も大きなポジションふたつには30%の不利な動き、残りのポジションに5%の不利な動きを適用してストレステストにかけます。損失の合計が標準証拠金を上回った場合には、これが維持証拠金として適用されます。

1.3委託証拠金として利用可能な資金

CFDのポジションを建てる場合の委託証拠金は、現金のみご利用可能です。CFDの実現利益は現金に含まれすぐに利用可能になります。現金が先に決済される必要はありません。未実現利益の場合は異なり、委託証拠金として利用することはできません。

1.4委託証拠金の自動資金調達(Fセグメント)

IBKR(UK)では、CFD用の委託証拠金の供給として、お客様のメイン口座から口座内のFセグメントに資金を自動的に移動します。

CFDの維持証拠金のために資金が移動されることはありませんのでご注意ください。このため、メイン口座に十分なご資金があっても、適格株式(以下に定義)が必要証拠金を満たすことができなくなる場合には強制決済されます。強制決済を避けるにはアカウント・マネジメントより、Fセグメントに追加の資金を入れて下さい。

2 マージン・クローズアウトに関するルール

2.1維持証拠金の計算と清算

対象となる資本がポジションを建てるために利用された委託証拠金の50%を下回った場合、IBKRではESMAの規制により、CFDのポジションを最後に清算するよう義務付けられています。IBKRでは、弊社のリスクに対する見解がより保守的な場合には早めにポジションを決済することがあります。 対象となる資本には、Fセグメント内の現金(口座の他のセグメントの現金は含まず)および未実現のCFD損益(プラスおよびマイナス)が含まれます。

この計算は、CFDのポジションを建てる時点での委託証拠金に基づいて行われます。 CFD以外のポジションに適用される証拠金計算とは異なり、オープンポジションの価値が変わっても委託証拠金の金額は変わりません。

2.1.1取引例

お客様はCFD口座にEUR 2000お持ちです。XYZのCFDを100枚、EUR 100の指値価格で購入を希望されています。CFDの初めの50枚が約定し、そのあと残りの50枚が約定します。ご利用可能な現金額が取引の約定と共に減っていきます:

| 現金 | 資本* | ポジション | 価格 | 価値 | 未実現損益 | IM | MM | 利用可能な現金 | MM違反 | |

| 取引前 | 2000 | 2000 | 2000 | |||||||

| 取引後 1 | 2000 | 2000 | 50 | 100 | 5000 | 0 | 1000 | 500 | 1000 | 不可 |

| 取引後 2 | 2000 | 2000 | 100 | 100 | 10000 | 0 | 2000 | 1000 | 0 | 不可 |

*資本は現金と評価損益の合計と同等です。

価格が110に上がります。現在の資本は3000ですが、利用可能な現金がまだ0のため新しいポジションを追加で建てることはできません。また、ESMAの規制により、IMおよびMMには変化はありません:

| 現金 | 資本 | ポジション | 価格 | 価値 | 未実現損益 | IM | MM | 利用可能な現金 | MM違反n | |

| 変化 | 2000 | 3000 | 100 | 110 | 11000 | 1000 | 2000 | 1000 | 0 | 不可 |

価格がこのあと95に下がります。資本は1500に減りますが、必要となる1000以上なため、証拠金不足にはなりません:

| 現金 | 資本 | ポジション | 価格 | 価値 | 未実現損益 | IM | MM | 利用可能な現金 | MM違反 | |

| 変化 | 2000 | 1500 | 100 | 95 | 9500 | (500) | 2000 | 1000 | 0 | 不可 |

価格がさらに85に下がり、証拠金不足が発生するため清算となります:

| 現金 | 資本 | ポジション | 価格 | 価値 | 未実現損益 | IM | MM | 利用可能な現金 | MM違反 | |

| 変化 | 2000 | 500 | 100 | 85 | 8500 | (1500) | 2000 | 1000 | 0 | 可能 |

3 ネガティブ・エクイティ・プロテクション

ESMAの規制により、CFDに関連するお客様のご責任はCFD取引専用の資金に限定されます。株式や先物などその他の銘柄は、CFDの証拠金不足を解消するために清算することはできません。*

このため、メイン口座の有価証券およびコモディティセグメントに含まれる資産、またFセグメント内のCFDとは関連のない資産は、CFD取引に伴うキャピタル・アット・リスクには含まれませんが、Fセグメント内の現金はすべて、CFD取引から生じる損失のカバーに利用することができます。

ネガティブ・エクイティ・プロテクションはIBKRにとって追加的なリスクとなるため、個人投資家のお客様にはオーバーナイトで保有されるCFDポジションに対し、追加で1%スプレッドをご請求させていただきます。CFD借入金利の詳細は、こちらよりご確認下さい。

*CFDの不足分の補填としてCFD以外のポジションを清算することはできませんが、CFD以外の不足分を補填するためにCFDのポジションを清算することは可能です。

4 CFD取引のためのインセンティブ

ESMAの規制により、CFD取引に関連する金銭的利益、また特定のタイプの非金銭的利益は禁止となっています。IBKRでは、CFD取引に対していかなるボーナスやその他のインセンティブも提供しておりません。

「EMIR」: 取引情報蓄積機関への報告義務およびお客様の義務達成をサポートするインタラクティブ・ブローカーズの代行サービス

1. 背景: 2009年、G20は、2008年の金融危機以降、店頭デリバティブ市場の透明性を高め、 取引当事者リスクを低減することを目的とした改革に取り組むことを 約束しました。欧州内でこの約束のほとんどをまとめる欧州市場インフラ規則(「EMIR」)はEUの規則であり、 2012年8月16日に発効となりました。

2. EMIRによる報告義務の対象となる金融銘柄および資産クラス: 次のクラスの店頭および取引所取引のデリバティブ: クレジット、利息、株式、 コモディティ、ならびに外国為替デリバティブ。取引所で取引されるワラントには適用されません。

3. EMIRによる報告義務の対象となる方: 報告義務は通常、自然人を除き、EUで設立されたすべての取引当事者に対して適用されます。適用対象:

* 金融取引先(「FC」)

* 決済基準を超える非金融取引先(「NFC+」)

* 決済基準以下の非金融取引先(「NFC-」)

* 一部の限られた状況においてEU圏外の第三国の事業体(「TCE」)

報告義務は基本的にEUで設立され、デリバティブコントラクトを取引した事業体すべてに適用となります。

4. 金融取引当事者(「FC」): 銀行、投資会社、クレジット機関、保険会社、AIFM管理のUCITS、年金制度、代替投資ファンドが含まれます。代替投資ファンド(「AIF」)はAIFのマネージャーが、「Alternative Investment FundManagers Directive(「AIFMD」)」の下で認可された場合のみ金融機関となるため、EU圏外のファンドがEMIRの報告義務の対象となる可能性があります。

5. 非金融取引当事者(「NFC」): NFCとは、EU 圏内で設立されたFCやクリアリング機関のような清算機関(「CCP」) として定義されるもの以外の事業を指します。NFCはFCに比べ義務が少なくなっていますが、 NFCは「清算基準」を超えた時点でNFC+になり、 FCとほぼ同等の義務の対象となります(担保および評価報告を含め)。 清算基準に満たないNFCはNFC-とみなされます。実際には、自然人以外の人物 (個人またはジョイント口座を持つ1人または1人以上の個人)はNFC-と定義され、

報告義務の対象となります。

インタラクティブ・ブローカーズによるお客様の報告義務の達成をサポートする報告サービスの代行

6. お客様が報告義務を果たすサポートとしてLEIの発行に加え、取引報告に関連して弊社で提供している代行サービス: 上に記載されるよう、FCおよびNFCは両方とも、公認の取引情報蓄積機関に取引(店頭およびETD)を報告する必要があります。この義務は、取引情報蓄積機関を通じて直接行うか、報告管理の部分を取引所やサードパーティ(代理として報告を行う)に委託することによって果たすことができます。

インタラクティブ・ブローカーズでは、業務上、法律上そして規制上の観点から可能な限りLEIの発行を促進し、お客様の同意に基づいて弊社が取引の約定および決済を行うお客様に対し、代理報告を行う意向です。

EMIR報告の対象となるお客様は、今後間もなく弊社のアカウント・マネジメントシステムよりLEIの申請および報告を、インタラクティブ・ブローカーズに委託できるようになります。

弊社では、法律上および規制上の観点から弊社にて評価報告を行うことが許容され、また取引当事者が評価報告を行うよう求められる場合(FCまたはNFC+に該当する場合)に限り、評価報告を行う予定です。

これは、報告用に弊社独自の取引評価を使用することが条件となります。

7EMIR報告の委託は可能なのか: EMIRでは、どちらの取引当事者にもサードパーティへの報告の委託を許可しています。取引当事者または清算機関がサードパーティに報告を委託した場合、報告義務を遵守する最終的な責任はサードパーティにあります。取引当事者または清算機関は、業務を委託するサードパーティが、正しい報告を行っていることを確認する必要があります。ブローカーやディーラーは、純粋に代理人として機能している場合には、報告義務を負いません。ブロック取引が複数の取引になった場合には、それぞれの取引を報告する必要があります。

ファンドおよびサブファンド - EMIRによる義務は取引当事者にありますが、これがファンドおよびサブファンドのことがあります。取引の主体であるファンドまたはサブファンドは、区分(FC、NFC+ またはNFC-)、委任報告の許可、ならびに取引主体識別コード(「LEI」)申請の詳細を提出する必要があります。

8. EMIR 条項 1(4) および 1(5) による免除: EMIR 条項 1(4) および 1(5) により、区分によって特定の事業体がEMIRにの設定する義務から免除される場合があります。条項 1(4)の下に免除を受ける事業体は、EMIRの設定するすべての義務を免除され、また条項 1(5) の下に免除を受ける事業体は、継続して適用となる報告義務以外の義務を免除されます。

9. EMIR 条項 1(4) および 1(5)による免除対象となる事業体: 条項 1(4) は当初、EUの中央銀行、公的債務の管理に関わる公的機関、ならびに国際決済銀行のみに適用されました。

その後、条項 1(4) の適用除外は、米国と日本の中央銀行および債権管理機構に拡大されました。委員会は、外国の中央銀行や債権管理機構に関しても、それらの管轄区において同等の規制が実施されていることの確認ができれば、今後追加される可能性があることを示唆しています。条項 1(5) は大まかに以下の事業体を免除対象としています:

- 国際開発金融機関

- 中央政府が所有し、また保証する非商業的な公共セクターの事業体、ならびに

- 欧州金融安定ファシリティおよび欧州安定メカニズム。

10. 店頭および上場投資デリバティブ: ESMAのレベル1既定、実施技術基準、ならびに規制技術基準において、上場投資デリバティブ(「ETD」)と店頭コントラクトの報告には、なんの違いもありません 。

コントラクトは、それぞれの商品個別の識別子で特定されます。また、それぞれの取引には個別の識別子が必要となります。世界的に同意されている商品識別子がない場合には、ISINコード、Alternative Instruments Identifiers(AII)、またはClassification of FinancialInstruments Codes(CFI)が代替として機能することもあります。

11. インタラクティブ・ブローカーズで使用している取引情報蓄積機関: Interactive Brokers (U.K.) Limited では、CMEグループの一部である、CME ETRのサービスを使用しています。

12. 取引主体識別(「LEI」)の発行

デリバティブの取引を行うすべてのEUの取引当事者は、報告義務の遵守のため、LEIの保有が必要となります。LEIは取引当事者データの報告目的で使用されます。

LEIとは、法人格のある個人や組織に付随し、金融取引の当事者の明確な識別を可能にするユニークな識別子、またはコードです。

「EMIR」: 取引情報蓄積機関の報告義務に関する詳細

13. NFCがNFC+、またはNFC-のどちらであるかを決定する際の基準: 以下の清算基準値のいずれかに違反する場合、これはNFC+の区分を意味します。ポジションは、想定される、30日の移動平均ベースでの計算となります:

• 店頭クレジット・デリバティブコントラクトの想定元本が10億ユーロ

• 店頭株式デリバティブコントラクトの想定元本が10億ユーロ

• 店頭金利デリバティブコントラクトの想定元本が30億ユーロ

• 店頭FXデリバティブコントラクトの想定元本が30億ユーロ

• 店頭コモディティ・デリバティブコントラクトの想定元本が30億ユーロ、ならびに 上に明記されない店頭デリバティブコントラクト

清算基準額に達したかどうかを計算するため、NFCはそのグループ内のすべての非金融事業体(また、これら事業体がEU圏内か圏外かを決定します)の取引を集計する必要がありますが、ヘッジや資金目的のために行われた取引は考慮に入れません。 ここでの「ヘッジ取引」とは、NFCまたはそのグループの商業活動や資金調達活動に直接関連するリスクを軽減するものとして、客観的に測定可能な取引を指します。

14. エクスポージャーの報告: FCおよびNFC+は以下の報告を行う義務があります:

* 各コントラクトの時価評価またはモデル評価価値

* 取引ベースまたはポートフォリベースで計上された、すべての担保の詳細(担保が取引ごとに計上されるのではなく、一連のコントラクトから生じるネットポジションに基づいて計算される場合)

15. 取引情報蓄積機関に報告するスケジュール: 報告開始日は、2014年2月12日になります:

* 2月12日以降に行われるコントラクト取引は取引日 +1

* 2012年8月16日以降のコントラクト取引において建てられたポジションが 2014年2月12日の時点でまだある場合には、 2014年2月14日までに取引情報蓄積機関に報告が必要になります

* 2012年8月16日以前のコントラクト取引において建てられたポジションが 2014年2月12日の時点でまだある場合には、2014年5月13日までに取引情報蓄積機関に報告が必要になります

* 評価および担保は、 2014年8月12日までに取引情報蓄積機関に報告が必要になります

* 2012年8月16日以前、当日またはこれ以降に行われたコントラクト取引において建てられたポジションが 2014年2月12日の時点でない場合には、 2017年2月12日までに取引情報蓄積機関に報告が必要になります。

16. 報告が必要となる内容および時期: 各取引の取引当事者(取引当事者データ)およびコントラクトそのもの(共通データ)に関する情報の報告が必要になります。

取引当事者データに関連しては26項目、また共通データに関連しては59項目の報告が必要となります。これらの項目は、取引情報蓄積機関に報告が必要となる最小限の内容に関するESMAの規制技術基準付属書の表1および表2に記載されています。

取引当事者および清算機関は、以下の場合に報告が必要となります:

* コントラクトが締結した時

* コントラクトが変更された時

* コントラクトが終了した時

締結、変更、終了の翌営業日内に報告する必要があります。

17. 報告が必要となる内容および報告責任者: 報告は、店頭デリバティブおよび取引所で取引されるデリバティブの両方に必要となります。報告義務は、区分には関係なく取引当事者に適用されます。以下にご注意下さい:

* 評価および担保の報告が必要となるのは、FCおよびNFC+のみです。

* 両タイプの取引先は通常、すべての取引を報告する必要があります。

この情報はインタラクティブ・ブローカーズで清算されるお客様のみを対象とします

留意点: 上記の情報は規制に対する包括的、完全、または確定的な解釈をであることを意図するものではなく、ESMAによるEMIR規制とそれに伴う取引レポジトリの報告義務のサマリーとなります。

IBIEおよびIBCEにおける個人投資家向けESMAルール導入の概要

概観:

|

CFDはレバレッジによる損失のリスクが高い複雑な商品です。 68.7%の個人投資家口座に、IBKRとのCFD取引による損失が発生しています。 お取引を開始される前にCFDの機能、また損失の際のリスクをご理解ください。 |

欧州証券市場監督局(ESMA)は、CFDを取引する個人投資家に対し、2018年8月1日より適用となるルールを実施しました。特定投資家のお客様への影響はありません。

国内の規制当局はESMAによるルールを永久的に採択しました。

ルールの構成は以下のようになります: 1) レバレッジの上限、 2) 口座単位のマージン・クローズアウト、 3) 口座単位のマイナス残高の保護、 4) CFD取引に対するインセンティブの制限、 5) リスク警告の標準化。

ほとんどのお客様は(規制対象となる事業体以外)まず個人投資家に分類されます。IBKRでは、場合によっては個人投資家のお客様を特定投資家に、または特定投資家のお客様を個人投資家に再分類することがあります。詳細は、MiFID分類基準をご覧ください。

下記の項目では、IBKRにおけるESMAルールの導入に関してご説明しています。

1 レバレッジの上限

1.1 ESMA証拠金

レバレッジの上限は、原資産によって違うレベルにESMAが設定しています:

- 主要な通貨ペアには3.33%。USD、CAD、EUR、GBP、CHF、JPYの組み合わせは、すべて主要な通貨ペアとなります。

- 主要ではない通貨ペアおよび主要な指数には5%。

- 主要ではない通貨ペアはUSD.CNHなどの、上に記載されない通貨を組み合わせたペアとなります。

- 主要な指数は、IBUS500、IBUS30、IBUST100、IBGB100、IBDE40、IBEU50、IBFR40、IBJP225、IBAU200になります。

- 主要ではない株式指数には10%。IBES35、IBCH20、IBNL25、IBHK50

- 個別株式には20%。

1.2適用となる証拠金 - 標準要件

IBKRではESMA証拠金に加え、原資産の過去の変動やその他の要因に基づいて、自社の証拠金(IB証拠金)を設定しています。 IB証拠金はESMAの設定によるものを上回る場合に適用されます。

適用となるIBおよびESMAの証拠金に関する詳細は、こちらよりご確認下さい。

1.2.1適用となる証拠金 - 最低コンセントレーション

ポートフォリオが少量のCFDおよび/または株式のポジションからなる場合、または最も大きいポジションふたつのウェイトが優勢な場合には、コンセントレーション・チャージが適用されます。弊社では、最も大きなポジションふたつには30%の不利な動き、残りのポジションに5%の不利な動きを適用してストレステストにかけます。損失の合計が、株式とCFDのポジションの組み合わせに必要となる標準証拠金を上回った場合には、これが維持証拠金として適用されます。CFDと株式の証拠金が組み合わされた場合のみ、コンセントレーション・チャージが発生します。

1.3委託証拠金の資金調達

CFDのポジションを建てる場合の委託証拠金は、現金のみご利用可能です。

初めに口座に入金された資金はCFD取引に利用できます。その他の銘柄の委託証拠金や株式の購入に現金を利用することにより、利用可能な現金が減っていきます。株式の購入によって証拠金の借入れが発生した場合、口座に十分な資金があってもCFD取引には利用できません。ESMAの規制により、CFDのための証拠金として証拠金の借入れを増やすことはできません。

CFDの実現利益は現金に含まれすぐに利用可能になります。現金が先に決済される必要はありません。未実現利益の場合は異なり、委託証拠金として利用することはできません。

2 マージン・クローズアウトに関するルール

2.1維持証拠金の計算と清算

対象となる資本がポジションを建てるために利用された委託証拠金の50%を下回った場合、IBKRではESMAの規制により、CFDのポジションを最後に清算するよう義務付けられています。IBKRでは、弊社のリスクに対する見解がより保守的な場合には早めにポジションを決済することがあります。 対象となる資本には、CFDの現金および未実現のCFD損益(プラスおよびマイナス)が含まれます。CFD現金にはその他の銘柄用の必要証拠金は含まれませんのでご注意下さい。

この計算は、CFDのポジションを建てる時点での委託証拠金に基づいて行われます。 CFD以外のポジションに適用される証拠金計算とは異なり、オープンポジションの価値が変わっても委託証拠金の金額は変わりません。

2.1.1取引例

口座に現金でEUR 2000があり、オープンポジションはありません。XYZのCFDを100枚、EUR 100の指値価格で購入を希望されています。CFDの初めの50枚が約定し、そのあと残りの50枚が約定します。ご利用可能な現金額が取引の約定と共に減っていきます:

|

|

現金 |

資本* |

ポジション |

価格 |

価値 |

未実現損益 |

IM |

MM |

利用可能な現金 |

MM違反 |

|

取引前 |

2000 |

2000 |

|

|

|

|

|

|

2000 |

|

|

取引後 1 |

2000 |

2000 |

50 |

100 |

5000 |

0 |

1000 |

500 |

1000 |

不可 |

|

取引後 2 |

2000 |

2000 |

100 |

100 |

10000 |

0 |

2000 |

1000 |

0 |

不可 |

*資本は現金と評価損益の合計と同等です。

価格が110に上がります。現在の資本は3000ですが、利用可能な現金がまだ0のため新しいポジションを追加で建てることはできません。また、ESMAの規制により、IMおよびMMには変化はありません:

|

|

現金 |

資本 |

ポジション |

価格 |

価値 |

未実現損益 |

IM |

MM |

利用可能な現金 |

MM違反 |

|

変化 |

2000 |

3000 |

100 |

110 |

11000 |

1000 |

2000 |

1000 |

0 |

不可 |

価格がこのあと95に下がります。資本は1500に減りますが、必要となる1000以上なため、証拠金不足にはなりません:

|

|

現金 |

資本 |

ポジション |

価格 |

価値 |

未実現損益 |

IM |

MM |

利用可能な現金 |

MM違反 |

|

変化 |

2000 |

1500 |

100 |

95 |

9500 |

(500) |

2000 |

1000 |

0 |

不可 |

価格がさらに85に下がり、証拠金不足が発生するため清算となります:

|

|

現金 |

資本 |

ポジション |

価格 |

価値 |

未実現損益 |

IM |

MM |

利用可能な現金 |

MM違反 |

|

変化 |

2000 |

500 |

100 |

85 |

8500 |

(1500) |

2000 |

1000 |

0 |

可能 |

3 ネガティブ・エクイティ・プロテクション

ESMAの規制により、CFDに関連するお客様のご責任はCFD取引専用の資金に限定されます。株式や先物などその他の銘柄は、CFDの証拠金不足を解消するために清算することはできません。*

このためCFDとは関連のない資産は、CFD取引に伴うキャピタル・アット・リスクには含まれません。

お客様がCFD取引にあてた現金以上の損害が発生した場合、弊社ではこの損失を切捨てします

ネガティブ・エクイティ・プロテクションはIBKRにとって追加的なリスクとなるため、個人投資家のお客様にはオーバーナイトで保有されるCFDポジションに対し、追加で1%スプレッドをご請求させていただきます。CFD借入金利の詳細は、こちらよりご確認下さい。

*CFDの不足分の補填としてCFD以外のポジションを清算することはできませんが、CFD以外の不足分を補填するためにCFDのポジションを清算することは可能です。

IBKRアイルランドおよび中央ヨーロッパにおけるリテールクライアント用TWS口座ウィンドウ

概観:

こちらのページでは、EUにおけるIBKR事業体のTWS口座ウィンドウに表示される情報についてご説明します。

|

CFDはレバレッジによる損失のリスクが高い複雑な商品です。 63.7%の個人投資家口座に、IBKRとのCFD取引による損失が発生しています。 お取引を開始される前に、CFDがどのように機能するものか、また損失の際のリスクをご理解ください。 |

Background:

EEAに居住し、このためヨーロッパのIBKR事業体であるIBIEまたはIBCEに口座をお持ちのリテールクライアントのお客様は、CFD取引に適用されるレバレッジおよびその他のEU規制の対象となります。

特に、CFDの必要証拠金にかかる要件を満たすためのフリーキャッシュの使用が規制によって必要となります。リテールクライアントのお客様は、CFDのポジションを建てるまたは維持するために資金を借入れする場合、口座内の有価証券を担保として使用することが禁止されています。詳細は、IBIEおよびIBCEにおけるリテールクライアントに適用となるESMA CFDルール概要をご確認下さい。

IBKRのEU事業体における口座は、弊社のプラットフォームで利用可能なすべての資産クラスを利用できるユニバーサル口座ですが、弊社の米国や英国の事業体とは異なり、個別に資金の入金ができるセグメントはありません。

この規制が適用される例および、CFD取引に利用可能なフリーキャッシュをモニターする方法は、以下のようになります。

口座ウィンドウ

CFDの委託証拠金および維持証拠金をカバーするために利用可能なフリーキャッシュが不十分な場合、弊社ではフリーキャッシュに関する制限を適用します。これは、CFD取引に利用可能な資金のリアルタイム・ベースの計算、新しい注文の拒否、既存のポジションの強制決済によって行われます。

CFD取引に利用可能なフリーキャッシュのモニター機能は、口座のフリーキャッシュ・レベルを表示するように強化された、TWSの口座ウィンドウよりご提供しています。CFD取引に利用可能な資金が別のセグメントに保有されているものかどうかは表示されません。この機能は口座の残高合計のうち、どれだけがCFD取引に利用可能かを表示します。

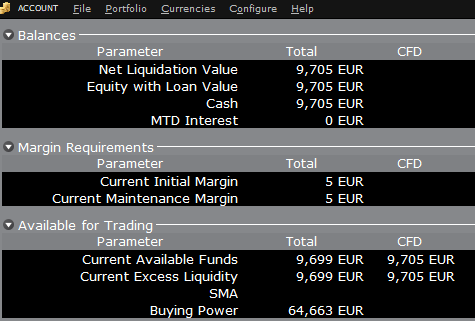

例として、口座にEUR 9,705の現金が保有され、ポジションはないものと仮定します。CFDのポジション、またはどの資産クラスのポジションを建てるにしても現金をすべて利用することができます:

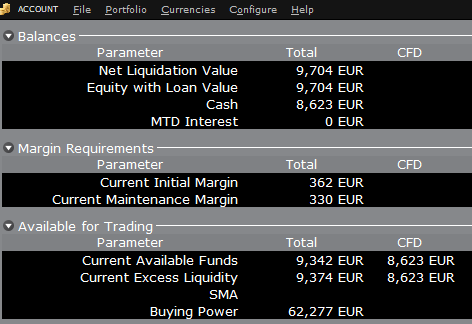

この状態でAAPLの株式を10株、合計USD 1,383分購入する場合、口座の現金はこれに相当するEURの金額分減り、

CFD取引に利用可能な資金がこれと同じ分減ります:

利用可能な資金の合計は株式の必要証拠金に対応する金額分減り、これは若干少ない金額になります。

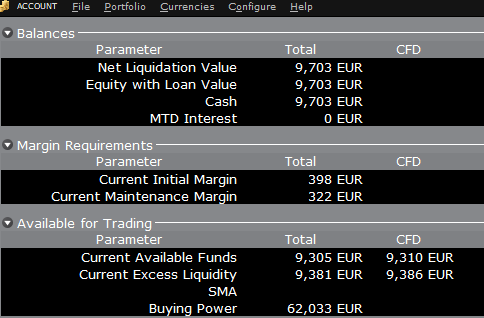

AAPL株式の代わりにAAPL CFDを10株購入する場合、状況は少し異なります。原資産の購入ではなく、デリバティブ・コントラクトの取引となるために現金は減りませんが、コントラクトのパフォーマンスを保証するためCFDに利用可能な資金がCFDの必要証拠金分減ります:

この場合の利用可能な資金の合計とCFDに利用可能な資金は、CFDの必要証拠金である同額になります。

資金

上に記載されるように、EUベースの口座には個別のセグメントがありません。このため口座間の送金は必要ではありません。資金は口座ウィンドウに表示される金額ですべての資産クラスに利用できます。移動や送金の必要はありません。

口座にマイナスの現金残高となる証拠金の借入れがある場合、CFDのポジションを建てることはできません。これはCFDの必要証拠金が、プラスの現金残高であるフリーキャッシュでないとならないためです。証拠金の借入れがある上でCFD取引をご希望の場合には、借入れをなくすべく先ず証拠金のポジションを決済するか、借入れをカバーする現金を口座に入金してCFD証拠金のためのバッファーを設けて下さい。

TWS Account Window for Retail Clients of IBKR Ireland and Central Europe

概観:

This article describes the information provided in the TWS account window for IBKRs EU based entities.

|

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 61% of retail investor accounts lose money when trading CFDs with IBKR. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. |

Background:

Retail clients who are residents of the EEA and therefore maintain an account with one of IBKR’s European brokers, IBIE or IBCE, are subject to EU regulations which introduce leverage and other restrictions applicable to CFD transactions.

Notably the regulations require the use of free cash to satisfy CFD margin requirements and prohibit retail clients from using securities in the account as collateral to borrow funds to initiate or maintain a CFD position. Please see Overview of ESMA CFD Rules Implementation for Retail Clients at IBIE and IBCE for full details.

The accounts of IBKRs EU entities are universal accounts in which clients can trade all asset classes available on IBKRs platform, but unlike IBKRs US and UK entities, there are no separately funded segments.

Working examples of how this restriction is applied, along with details as to how clients can monitor free cash available for CFD transactions, are outlined below.

Account Window

IBKR enforces the restriction relating to free cash by calculating the funds available for CFD trading on a real-time basis, rejecting new orders and liquidating existing positions when the available free cash is insufficient to cover CFD initial and maintenance margin requirements.

IBKR offers clients the ability to monitor free cash available for CFD transactions via an enhancement to the TWS Account Window which displays the level of free cash in the account. Importantly, the funds shown as available for CFD trading do not imply that cash is held in a separate segment. It simply indicates what proportion of total account balances is available for CFD trading.

For example, assume that an account has EUR 9,705 in cash and no positions. All the cash is available to open CFD positions, or positions in any other asset class:

If the account now purchases 10 shares of AAPL stock for an aggregate value of USD 1,383 the cash in the account is reduced by a corresponding amount in EUR, and the funds available for CFD trading are reduced by the

same amount:

Note that Total available funds are reduced by a smaller amount, corresponding to the stock margin requirement.

If, instead of buying AAPL stock, the account buys 10 AAPL CFDs the impact will be different. As the transaction involves a derivative contract rather than the purchase of the underlying asset itself, there’s no reduction in cash but the funds available for CFDs are reduced by the CFD margin requirement to secure performance on the contract:

In this case Total available funds and CFD available funds are reduced by an equal amount; the CFD margin requirement.

Funding

As noted above, EU-based accounts do not have segments and therefore there is no need for internal transfers. Funds are available for trades in all asset classes in the amounts indicated in the account window, without the need for sweeps or transfers.

Note also that should an account have a margin loan, i.e. negative cash, it will not be possible to open CFD positions since the CFD margin requirement must be satisfied by free, positive cash. Should you have a margin loan and wish to trade CFDs you must first either close margin positions to eliminate the loan, or add cash to the account in an amount that covers the margin loan and creates a cash buffer sufficient for the necessary CFD margin.

IBKR Metals CFDs – Facts and Q&A

概観:

The following article is intended to provide a general introduction to London Gold and Silver Contracts for Differences (CFDs) issued by IBKR.

Please follow these links for information on IBKR Share CFDs, Index CFDs and Forex CFDs.

Risk Warning

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage.

61% of retail investor accounts lose money when trading CFDs with IBKR.

You should consider whether you understand how CFDs work and whether you can afford to take the

high risk of losing your money.

ESMA Rules for CFDs (Retail Clients only)

The European Securities and Markets Authority (ESMA) has enacted new CFD rules effective 1st August

2018.

The rules include: 1) leverage limits on the opening of a CFD position; 2) a margin close out rule on a per

account basis; and 3) negative balance protection on a per account basis.

The ESMA Decision is only applicable to retail clients. Professional clients are unaffected.

Please refer to the following articles for more detail:

ESMA CFD Rules Implementation at IBKR (UK) and IBKR LLC

ESMA CFD Rules Implementation at IBIE and IBCE

Introduction

A London Gold CFD enables you to have exposure to price movements of physical Gold without actually owning it. A London Gold CFD is an agreement between you and IBKR to exchange the difference in price of the underlying over a period of time. The difference to be exchanged is determined by the change in the reference price of the underlying. Thus, if the price of physical Gold traded on the London bullion market rises and you are long the CFD, you receive cash from IBKR and vice versa. A London Gold CFD can be bought long or sold short to suit your view of market direction in the future.

Contract Specifications

| Contract | IBKR Symbol | Per Trade Fee | Minimum per Order | Multiplier |

| London Gold | XAUUSD | 0.015% | USD 2.00 | 1 |

| London Silver | XAGUSD | 0.03% | USD 2.00 | 1 |

Price Determination

The IBKR London Gold and Silver CFDs reference physical Gold and Silver traded on the London bullion market. The London bullion market is a wholesale over-the-counter market for the trading of precious metals. Trading is conducted among members of the London Bullion Market Association (LBMA). Most of the members are major international banks.

IBKR receives quote streams from approximately 10 such major banks, in much the same way it does for cash forex. IBKR Smart routes between the banks, and the best available price at any given time becomes the reference price for the CFDs. IBKR does not add a spread to the banks’ quotes.

Low Commissions and Financing Rates: Unlike other CFD providers IBKR charges a transparent

commission, rather than widening the spread. Commission rates are only 0.015% for London Gold and 0.03% for London Silver. Overnight financing rates are just benchmark +/- 1.5% (an additional 1% surcharge is added for retail accounts).

Transparent Quotes: Because IBKR does not widen the spread, the Metals CFD quotes accurately

represent the spreads and price movements of the related cash metal, as described above.

Margin Efficiency: IBKR establishes house-margin requirements based on historic volatility of the

underlying and other factors. Retail clients are subject to regulatory minimum initial margins of 5% for

London Gold or 10% for London Silver.

Trading Permissions: Same as for Share and Index CFDs.

Market Data Permissions: Metals CFD market data is free, but a permission is required for system

reasons.

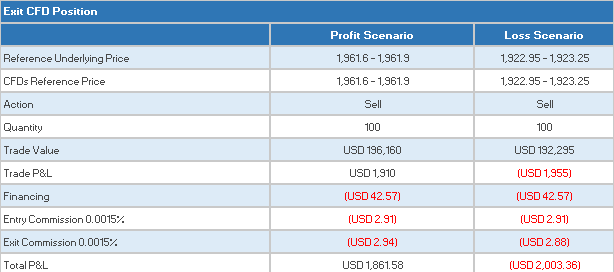

Worked Trade Example (Professional Clients):

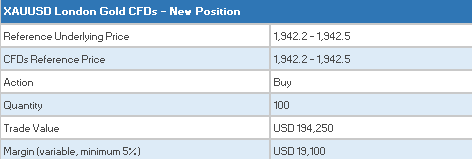

You purchase 100 XAUUSD CFDs at $1,942.5 for USD 194,250 which you then hold for 5 days.

![]()

Closing the Position

CFD Resources

Below are some useful links with more detailed information on IB’s CFD offering:

Frequently asked Questions

Are short Metals CFDs subject to forced buy-in?

No.

Can I take delivery of the underlying metal?

No, IBKR does not support physical delivery for Metals CFDs.

Are there any market data requirements?

The market data for Metal CFDs is free, and is included the market data for Index CFDs. However, you need to subscribe to the permission for system reasons. To do this, log into Account Management, and click through the following tabs: Settings/User Settings/Trading Platform/Market Data Subscriptions. Alternatively you can set up an Index or Metals CFD in your TWS quote monitor and click the “Market Data Subscription Manager” button that appears on the quote line.

How are my CFD trades and positions reflected in my statements?

If you are a client of IBKR (U.K.) or IBKR LLC, your CFD positions are held in a separate account segment identified by your primary account number with the suffix “F”. You can choose to view Activity Statements for the F-segment either separately or consolidated with your main account. You can make the choice in the statement window in Account Management.

If you are a client of other IBKR entities, there is no separate segment. You can view your positions normally alongside your non-CFD positions.

In what type of IB accounts can I trade CFDs e.g., Individual, Friends and Family,

Institutional, etc.?

All margin and cash accounts are eligible for CFD trading.

Can I trade CFDs over the phone?

No. In exceptional cases we may agree to process closing orders over the phone, but never opening

orders.

Can anyone trade IB CFDs?

All clients can trade IB CFDs, except residents of the USA, Canada, Hong Kong, New Zealand and

Israel. There are no exemptions based on investor type to the residency-based exclusions.

Bonus Certificates Tutorial

Introduction

Bonus certificates are designed to provide a predictable return in sideways markets, and market returns in rising markets.

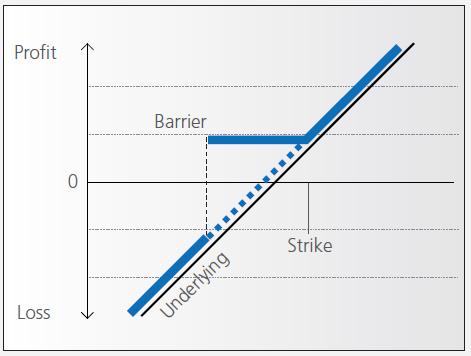

At the time they’re issued, bonus certificates normally have a term to maturity of two to four years. You will receive a specified cash pay-out (“bonus level” or “Strike”) if at maturity the price of the underlying is below or at the strike, as long as the underlying instrument has not touched or fallen below an established price level (“safety threshold” or “barrier”) during the term of the certificate.

Unless the certificate has a cap, you continue to participate in the price gains if the underlying instrument rises above the bonus level. In this case you either receive the corresponding number of shares or a cash settlement reflecting the value of the underlying instrument on the maturity date.

However, if the barrier is breached, you will no longer be entitled to the bonus payment. The value of the certificate then corresponds to the value of the underlying (times the ratio). In other words, once the barrier has been touched the certificate effectively converts to an index certificate. You will receive either the corresponding number of shares or a cash settlement reflecting the value of the underlying instrument on the maturity date.

Although there is no structured leverage, the presence of the barrier creates effective leverage. When the price of the underlying instrument approaches the barrier the probability of a breach increases, affecting the price of the certificate disproportionately.

Pay-out Profile

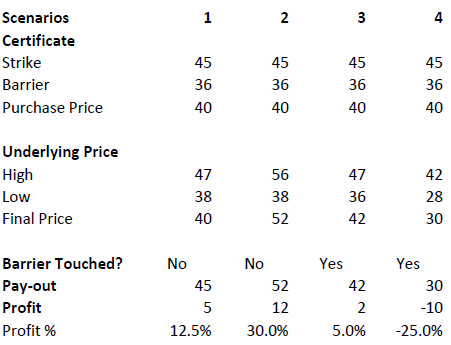

Example

Assume a bonus certificate on ABC share. The certificate has a strike of EUR 45.00 and a barrier set at EUR 36.00. The table below shows scenarios depending on the trading range of the underlying, the final price of the underlying and whether the barrier has been touched or not.

Warrant Tutorial

Introduction

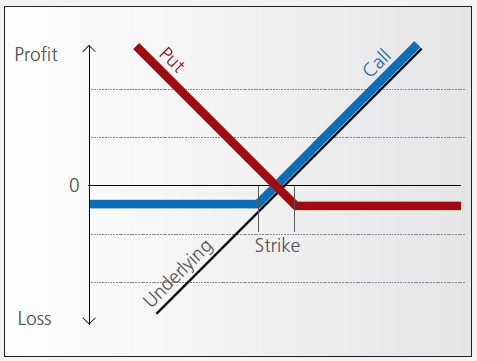

A warrant confers the right to buy (call-warrant) or sell (put-warrant) a specific quantity of a specific underlying instrument at a specific price over a specific period of time.

Pay-out Profile

With some warrants, the option right can only be exercised on the expiration date. These are referred to as “European-style” warrants. With “American-style” warrants, the option right can be exercised at any time prior to expiration. The vast majority of listed warrants are cash-exercised, meaning that you cannot exercise the warrant to obtain the underlying physical share. The exception to this rule is Switzerland, where physically settled warrants are widely available.

IBKR does allow for US and Canadian warrant exercise. Customers wishing to do so should submit a Customer Service ticket stating the name/symbol of the warrant, the quantity of shares and the intended action (i.e. exercise). The broker will pass through all associated exercise costs to the customer upon completion of the request. US or Canadian warrants are not eligible for auto-exercise at expiration. Warrants remaining in an account at expiration will be removed as worthless.

Factors that influence pricing

Not only do changes in the price of the underlying instrument influence the value of a warrant, a number of other factors are also involved. Of particular importance to investors in this regard are changes in volatility, i.e. the degree to which the price of the underlying instrument fluctuates. In addition, changes in interest rates and the anticipated dividend payments on the underlying instrument also play a role.

However, changes in implied volatility - as well as interest rates and dividends - only affect the time value of a warrant. The primary driver - intrinsic value - is solely determined by the difference between the price of the underlying instrument and the specified exercise price.

Historical and implied volatility

In addressing this topic, a differentiation has to be made between historical and implied volatility. Implied volatility reflects the volatility market participants expect to see in the financial instrument in the days and months ahead. If implied volatility for the underlying instrument increases, so does the price of the warrant.

This is because the probability of profiting from a warrant during a particular time-frame increases if the price of the underlying instrument is highly volatile. The warrant is therefore more valuable.

Conversely, if implied volatility decreases, that leads to a decline in the value of warrants and hence occasionally to nasty surprises for warrant investors who aren’t familiar with the concept and influence of volatility.

Interest rates and dividends

Issuers hedge themselves against price changes in the warrant through purchases and sales of the underlying instrument. Due to the leverage afforded by warrants, the issuer needs considerably more capital to hedge its exposure than you require to buy the warrants. The issuer’s interest expense associated with that capital is included in the price of the warrant. The amount of embedded interest reduces over time and at expiration is zero.

In the case of puts, the situation is exactly the opposite. Here, the issuer sells the underlying instrument

short to establish the necessary hedge, and in so doing receives capital that can earn interest. Thus interest reduces the price of the warrant by an amount that decreases over time.

As the issuer owns shares as a part of its hedging operations, it is entitled to receive the related dividend

payments. That additional income reduces the price of call warrants and increases the price for puts. But if the dividend expectations change, that will have an influence on the price of the warrants. Unanticipated special dividends on the underlying instrument can lead to a price decline in the related warrants.

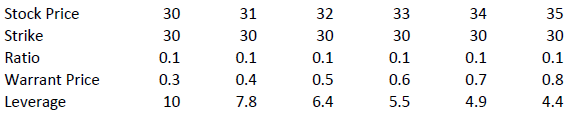

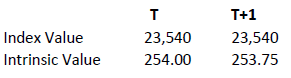

Key valuation factors

Let’s assume the following warrant:

Warrant Type: Call

Term to expiration: 2 years

Underlying : ABC Share

Share price: EUR 30.00

Strike: EUR 30.00

Exercise ratio: 0.1

Warrant’s price: EUR 0.30

Intrinsic value

Intrinsic value represents the amount you could receive if you exercised the warrant immediately and then bought (in the case of a call) or sold (put) the underlying instrument in the open market.

It’s very easy to calculate the intrinsic value of a warrant. In our example the intrinsic value is EUR 00.00

and is calculated as follows:

(price of underlying instrument – strike price) x exercise ratio

= (EUR 30.00 – EUR 30.00) x 0.1

= EUR 00.00

If the price of the ABC share increases by EUR 1, the intrinsic value becomes

= (EUR 31.00 – EUR 30.00) x 0.1

= EUR 00.10

The intrinsic value of a put warrant is calculated with this formula:

(strike price – price of underlying instrument) x exercise ratio

It’s important to note that the intrinsic value of a warrant can never be negative. By way of explanation:

if the price of the underlying instrument is at or below the exercise price, the intrinsic value of a call equals zero. In this instance, the price of the warrant consists only of “time value”. On the flipside, the intrinsic value of a put is equal to zero if the price of the underlying instrument is at or above the exercise price.

Time value

Once you’ve calculated the intrinsic value of a warrant, it’s also easy to figure out what the time value of that warrant is. You simply deduct the intrinsic value from the current market price of the warrant. In our example, the time value is equal to EUR 1.30 as you can see from the following calculation:

(warrant price – intrinsic value)

= (EUR 0.30 EUR – EUR 0.00)

= EUR 0.30

Time value gradually erodes during the term of a warrant and ultimately ends up at zero upon expiration. At that point, warrants with no intrinsic value expire worthless. Otherwise you can expect to receive payment of the intrinsic value. Take note, though: a warrant’s loss of time value accelerates during the final months of its term.

Premium

The premium indicates how much more expensive a purchase/sale of the underlying instrument would be via the purchase of a warrant and the immediate exercise of the option right as opposed to simply buying/selling the underlying instrument in the open market.

Hence the premium is a measure of how expensive a warrant actually is. It follows that, when given a choice between warrants with similar features, you should always buy the one with the lowest premium. By calculating the premium as an annualized percentage, warrants with different terms to expiry can be compared with each other.

The percentage premium for the call warrant in our example can be calculated as follows:

(strike price + warrant price / exercise ratio – share price) / share price * 100

= (EUR 30.00 + EUR 0.30 / 0.1 – EUR 30.00) / EUR 30.00 x 100

= 10 percent

Leverage

The amount of leverage is the price of the share * ratio divided by the price of the warrant. In our example 30.00*0.1/0.3 = 10. So when the price of ABC increases by 1% the value of the warrant increases by 10%.

The amount of leverage is not constant however; it varies as intrinsic and time value changes, and is particularly sensitive to changes in intrinsic value. As a rule of thumb, the higher the intrinsic value of the warrant, the lower the leverage. For example (assuming constant time value):

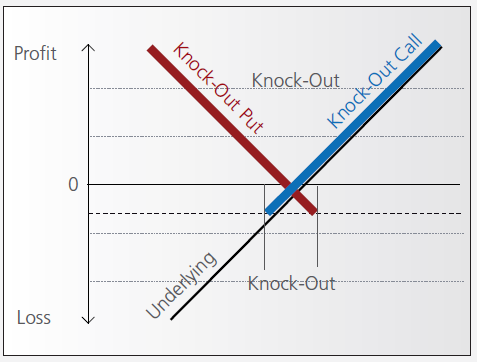

Knock-out (Turbo) Tutorial

Introduction

Knock-out warrants (turbos), like vanilla warrants, derive their value from the difference between the price of the underlying and the strike. They differ significantly however from vanilla warrants in many important respects:

- They can expire (knock-out) prematurely if the price of the underlying instrument touches or falls below (in the case of knock-out calls) or exceeds (in the case of knockout puts) a predetermined barrier-level. It expires worthless if the barrier equals the strike, or it may have a residual stop-loss value if the barrier is set higher than the strike (in the case of a call).

- Changes in implied volatility have little or no impact on knock-out products, therefore their pricing is easier for investors to comprehend than that of warrants.

- They have little or no time value (because of the presence of the knock-out barrier), and therefore have a higher degree of leverage than a warrant with the same strike. This is because the absence of time value makes the instrument “cheaper”.

Pay-out Profile

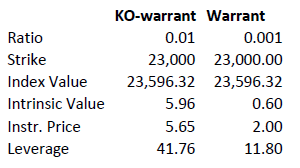

Leverage

As discussed above, knock-out warrants exhibit high degrees of leverage, particularly as the price of the underlying nears the strike/barrier. Consider the following example of a long turbo on the Dow Jones Index, compared to a vanilla warrant:

Intrinsic value = (index value – strike) x ratio

Leverage = Index Value x Ratio / Instrument Price

A vanilla warrant retains significant time value even as the underlying price approaches the strike, sharply reducing its leverage compared to a knock-out warrant.

Product types

As discussed above, the barrier may either equal the strike, or be set above (calls) or below (puts). In the latter cases a small residual value remains after knock-out, corresponding to the difference between the barrier (the stop-loss level) and the strike.

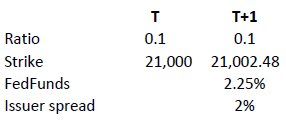

Moreover, knock-out products may either have an expiration date or may be open-ended. This makes a difference in the way interest is accounted for. If the contract has an expiration date interest is included in the premium, the amount of which reduces over time and is zero on expiration. This is analogous to a standard vanilla warrant.

in relation to an expiration date. The price of the contract therefore corresponds exactly to its intrinsic value. Interest however must be accounted for. This is done by a daily adjustment of the barrier and strike. The following example shows the daily adjustment for a long open-end turbo on the Dow Jones Index:

The adjustment = Strike T x (1+ FedFunds/360 + Issuer Spread/360).

The intrinsic value of the instrument is correspondingly reduced as follows, assuming no change in the value of the DJ Index):

Intrinsic value = (index value – strike) x ratio