现金划转

背景

IB全能账户由两个独立的子账户或账户段组成,一个用于持有证券仓位和余额,受美国证券交易委员会(SEC)客户保护规则约束,另一个用于持有商品仓位和余额,受美国商品期货交易委员会(CFTC)客户保护规则约束。这种全能账户的设计旨在尽可能地降低客户维护两个不同账户(例如,账户之间转账现金、两个账户登录和提交委托单、多份报表等)可能面临的行政管理开销,同时又维持法规要求的分隔措施。

该等法规还要求所有证券交易和相关保证金交易均在全能账户的证券账户段进行,而商品交易则在商品账户段进行。1 虽然法规允许将全额支付的证券持仓以保证金抵押品的形成存放在商品账户段进行托管,但IB并不允许这种操作,从而对抵押权应用了更为严格的SEC限制性规则。鉴于相关法规和政策已对持仓应归于哪个账户段作出了规定,现金是唯一可由客户自行决定在两个账户段之间来回转账的资产。

下方为现金划转选项、选择步骤和注意事项相关的说明。

现金划转选项

客户有三种划转选项,说明如下:

1. 不划转剩余资金 – 根据这个选项,如非必要,剩余现金不会在两者之间进行转移:

a. 解决/缓解另一账户段保证金不足的问题;

b. 尽可能地降低指定账户段的借方现金余额,从而减少相关的利息费用。 请注意,对于只拥有证券或商品交易许可中一项许可的账户持有人来说,这是默认选项,也是唯一的选项。

2. 将剩余资金划转至我的IB证券账户 – 只在商品账户段中留下能满足当前商品保证金要求的现金余额。 任何由于现金增加(例如,有利的变化和/或与交易相关)或保证金要求降低(例如,SPAN风险阵列和/或与交易相关的变化)而产生的超出保证金要求的现金,都将自动从商品账户段转移到证券账户段。请注意,账户持有人必须具备证券交易许可才能选择此选项。

3. 将剩余资金划转至我的IB商品账户 – 只在证券账户段中留下能满足当前证券保证金要求的现金余额(加上含有贷款价值的其它证券仓位)。请注意,账户持有人必须具备商品交易许可才能选择此选项。

其它注意事项:

- 由于全能账户允许以不同币种持有现金余额,因此存在一个层次结构,以决定当多种货币出现多头余额时,首先转移哪种货币。在这类情况下,首先会转移以基础货币计价的余额,然后是美元,然后剩下的多头余额再按金额从高到低的顺序转移。

- 为了尽可能地降低一个账户段在把剩余现金划转至另一个账户段后出现保证金不足的可能性,剩余资金不会全部转移,而是会留下相当于维持保证金要求5%的资金作为缓冲。 同样,为了尽可能地降低转移名义余额的运营开销,只有在扣除5%的保证金缓冲后,剩余金额(如有)仍不低于账户净资产的1%或200美元时,才会转移余额。

- 在执行交易前信用核查以确定账户是否拥有足够的净资产来支持新的委托单时,一个账户段内进行的交易也会将另一个账户段内的剩余现金纳入考虑(但在交易执行之前不会进行划转,并且也只有在为了满足保证金要求而有必要时才会进行划转)。 被标记为典型日内交易者以及需要进行交易前信用核查(会考虑前一日和当日净资产)的账户应特别留意下方选择注意事项。

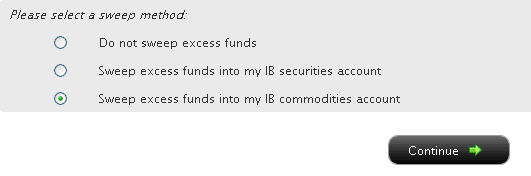

选择划转的选项

如果您的账户管理版本在左侧有一系列菜单选项,请选择账户行政,然后选择 剩余资金划转菜单选项。 如果您的版本是顶部有菜单选项,请选择管理账户/设置,然后选择 配置账户/剩余资金划转菜单选项。无论您的版本如何,您都将看到以下界面:

然后,您可点击您想要的划转方式对应的单选按钮,然后选择〝继续〞按钮。您的选择将从下一个工作日起生效,并将一直有效,直到选择其它选项为止。请注意,只要满足上文中提到的交易许可设置,您可随时更改划转方式,没有次数限制。

选择注意事项

虽然选择将剩余现金存放在哪个账户段可能涉及每位客户独特的主观决策和偏好(例如,客户将大部份资产集中存放在其中一个账户段),但下述有几个因素值得注意:

1. 典型日内交易净资产 - 根据相关法规被标记为典型日内交易者的账户(即在5个工作日内进行4次或以上日內交易),其证券购买力将被限制为证券账户段当日或前一日收盘净资产中的较低者。根据这个计算方式,如选择将剩余资金划转至商品账户段,则该笔资金将无法纳入计算,从而可能对下达新委托单的造成一定限制。要最大程度地利用净资产来扩大购买力下达证券委托单,客户需选择将剩余资金划转至证券账户段。 请注意,选择证券账户段并不会限制下达商品委托单的能力,因为典型日内交易规则不适用于此类账户。

2. 保险 – 美国证券投资者保护公司(SIPC)的保障范围覆盖证券账户段的资产,而商品账户段则没有相应的保障计划。不过,超过SIPC的$250,000现金分项给付限额(劳合社现金分项给付限额为$900,000,如适用)的余额不在承保范围内。 IB加拿大和IB英国的客户也分别受加拿大投资者保护基金(CIPF)和英国金融服务补偿计划(FSCS)规定的承保规则约束。

3.利息收入 – 在所有其它条件相同的情况下,从未将多头现金余额在证券和商品账户段中分开存放的客户,可望获得最高的利息收入,这是因为两者不会汇总以计算贷方利息(它们受不同的隔离池和再投资规则的约束)。 在选择现金划转时,除了上述的因素外,也应该要考虑到贷款需要维持最低现金余额,并且余额高一些,利率也会优惠一些。2

脚注:

1由于OneChicago个股期货是由SEC和CFTC共同监管的混合产品,因此可在任何一种账户类型中进行买卖。不过,IB选择在全能账户的证券账户段进行此类交易,因为只有在这情况下,才能向单一股票期货和任何合资格股票或期权持仓提供保证金减免。

2例如,某账户在证券和商品账户段各持有$9,000的多头美元余额。根据基准联邦基金有效利率,如果两个余额存放在同一账户段,该账户有$8,000 ($18,000 - $10,000)可以获得利息。但由于分别放在两个账户段中的现金余额均低于$10,000,都无法获得利息,如不选择现金划转,将无法赚取任何利息。同样,如进行现金划转后,某账户段的多头美元现金余额超过$100,000,则账户持有人将能够赚取更高一档的利息。有关利息计算的其它信息,包括当前基准利率的链接,请参阅KB39。

通过Wise进行注资

什么是Wise?

Wise(前称TransferWise)是一项国际线上资金转帐服务,支持80个国家的55种货币,主要提供跨境资金转帐和外汇服务。Wise比跨境银行转帐费用更低,也较跨境银行转帐更快到帐,同时其提供的外汇汇率也颇具竞争力。

通过与Wise进行合作,IBKR能够在您登录IBKR平台期间,为您提供以下的服务:

通过与Wise进行合作,IBKR能够在您登录IBKR平台期间,为您提供以下的服务:

- 把您的IBKR账户与WISE账户关联进行注资

- 把IBKR不直接支持的货币(例如罗马尼亚列伊(RON)、保加利亚列弗(BGN)、马来西亚令吉(MYR)、印度尼西亚卢比(IDR))从您的本地银行转帐至Wise,然后在Wise将其兑换成IBKR支持的货币(例如欧元(EUR)、美元(USD)等)存入您的IBKR账户。

- 从现有的Wise余额向您的IBKR账户转账以及从IBKR账户转回Wise

IBKR是否允许通过Wise进行存款和取款?

是,客户可通过Wise把资金存入IBKR账户,也可从IBKR账户提取资金回存至Wise账户。

谁可以使用Wise注资方式?

IBLLC、IB-英国、IB爱尔兰、IB中欧、IB-香港、IB-新加坡的个人客户可以使用Wise转帐资金。

如您还没有开立Wise账户,您将收到创建账户的提示。IBKR将使用您在IBKR账户内的信息(姓名、电邮等)为您预填Wise账户的申请,而您需要登录wise.com以完成申请过程,并上传Wise可能会要求您提交的文件。

Wise与IBKR账户只需要建立一次关联。您只能与您名下的Wise账户进行关联。

如何通过Wise进行存款?

要通过Wise进行存款,请登录客户端选择转帐与支付,然后选择转帐资金。点击存款然后在下拉菜单中选择您想存款的币种。选取合适的货币后,选择“通过Wise进行银行转帐”或“从Wise余额转帐”作为注资方式。

如这是您首次使用Wise注资方式,您将会收到与Wise账户关联的提示。

如这是您首次使用Wise注资方式,您将会收到与Wise账户关联的提示。

通过Wise进行银行转帐:为所存入的本地货币(例如罗马尼亚列伊(RON)、保加利亚列弗(BGN)、马来西亚令吉(MYR)、印度尼西亚卢比(IDR))提供直接整合。 您将把本地货币转帐至Wise银行账户,而Wise将进行兑换,然后把IBKR支持的币种存入到您的IBKR账户。本地货币的列表将取决于您IBKR账户所在的IBKR实体。

您将看到一个报价界面。源币种是您在上方选择的本地货币,而您需要选择要存入您IBKR账户的目标币种(例如美元(USD)、欧元(EUR))。您可修改源币种的数量以查看适用费用、兑换汇率、IBKR账户将收到的目标币种到账金额以及预期到账的时间。确认后,您将收到Wise银行账户的详情和转帐资金的指令。

所需时间方面,从您的本地银行转帐资金至Wise可能需要几个小时至几个工作日,然后需要最多一整个工作日把资金从Wise转至您的IBKB账户,具体时间视乎不同货币而定。

从Wise余额转帐:您可以看到Wise多币种账户中的余额,并向IBKR账户发起资金转账。如Wise账户中的资金是IBKR账户支持的币种,则您可在无需兑换的情况下转帐资金;如果不是,则您可以选择在Wise价格资金兑换成IBKR支持的币种(例如欧元(EUR)、美元(USD))再转入IBKR账户。

资金从您的Wise账户转出之后,需要几个小时至一整个工作日才会到达您的IBKR账户,具体时间视乎币种而定。

如何从Wise账户取款?

您可从IBKR账户提取支持的币种(例如欧元(EUR)、美元(USD))转账至您的Wise账户。

您可从IBKR账户提取支持的币种(例如欧元(EUR)、美元(USD))转账至您的Wise账户。

要通过Wise账户提取资金,请登录客户端选择转帐与支付,然后选择 转帐资金。

点击取款然后在下拉菜单中选择您想取款的币种。选取合适的货币后,选择“转帐至Wise”作为取款方式。

如果这是您首次使用“转帐至Wise”作为取款方式,您将会收到把Wise账户与IBKR账户关联的指示。Wise账户完成关联后,系统会提示您用预填的Wise账户信息创建取款目的地。创建完成后,页面将显示您已保存的目的地,您刚才创建的目的地信息将显示为“转帐至Wise”。选取这个选项,键入金额,然后提交取款请求进行处理。

资金从您的IBKR账户转出之后,需要几个小时至一整个工作日才会到达您的Wise账户,具体时间视乎币种而定。

通过Wise转帐资金需要收费吗?

通过Wise转帐资金可能涉及费用。如果需要收费,有关费用将在您提交转帐资金的请求前,在确认屏幕显示出来。

我可以通过Wise取款到第三方吗?

不能。您只能取款到您名下的Wise账户。

如果转帐发生问题,我可以联系谁?

如关于在客户端发起转帐有任何疑问,或如果您的款项已从Wise账户转出超过一个工作日但仍未到达IBKR账户,请与IBKR联系。

如果是关于款项状态、或从银行向Wise转账碰到的问题、或资金在Wise处于等待状态的相关问题查询,请直接登录您的Wise账户联系客户服务。

在哪里可以了解更多关于Wise及其服务的信息?

请参考Wise支持中心的页面>www.wise.com/help。

How To Transfer an Existing IRA from Interactive Brokers

If the other broker participates in the Automated Customer Account Transfer Service (ACATS) program, then contact your other broker to submit the transfer out electronically.

If the other broker is not ACAT eligible, they must provide outgoing trustee to trustee transfer paperwork or outgoing Direct Rollover paperwork. They can give you the completed documents which can be uploaded online. Please note this is only for cash transfers, and information submitted is only instructions, not the actual withdrawal. After paperwork is reviewed and approved, you’ll be advised when to submit the withdrawal of funds.

To submit a withdrawal request:

- Log into Client Portal

- Select Transfer & Pay followed by Transfer Funds

- Click Make a Withdrawal

- Select Use a new withdrawal method and next to Bank Wire, click Use this Method

- Select Financial Institution when asked “Where will funds be deposited?”

- Answer the prompts that follow, then click in the box when asked if you’ll be sending a trustee-to-trustee transfer or Direct Rollover to this destination

- Confirm in the pop up box you have the signed custodian transfer paperwork

- Complete remaining banking prompts and click Save Bank Information

- Confirm the instructions on the next page and click Continue

- Click on Upload your form

- Click Reply to upload the document and add a comment.

- Click Submit and close the window

You will be provided updates of your transfer request through the Message Center.

If a wire transfer is not accepted by your new custodian, you may submit a check withdrawal request. Please note check requests require review by Compliance and will take longer to process if approved.

- Log into Client Portal

- Select Transfer & Pay followed by Transfer Funds

- Click Make a Withdrawal

- Select Use a new withdrawal method and next to Check, click Use this Method

- Select “Send to another person/entity” from the first drop down box

- Answer the prompts that follow and click Save Destination

- Complete remaining banking prompts and click Save Bank Information

- Confirm the information and click Continue

- Read the instructions and click Finish

- Finally, click on Help on the top right and select Secure Message Center to create a new ticket

- Click Compose and then New Ticket>Funds & Banking>Cash Withdrawals

- Complete the prompts and upload the completed paperwork from your broker/custodian

You will be provided updates via this ticket.

Contra firms and Custodians (only) may forward paperwork to the following:

Interactive Brokers LLC

Attn: IRA Services, Transfers

209 South LaSalle Street, 10th Floor

Chicago, IL 60604

- Email — iraservices@ibkr.com

- Fax — 312-542-7345

Additional Information

- IRA Transfer Methods in the Client Portal Users' Guide

从已关的账户中提取资金

简介

客户如选择关户,则应在关户前取走或转走账户中的全部现金及证券余额。账户一旦被关闭,就无法再进行交易。然而,在少数情况下,可能会有资产被存入已关的账户。正如在关户时向客户披露的,鉴于已关账户不再能使用交易平台兑换货币,被存入已关账户的现金余额不论金额大小,都将自动被兑换为基础货币。

下文将介绍前述情况发生的背景以及客户应如何提取相关资产。

关户后产生余额

尽管关户后通常不会再有资产存入,但在以下情况下仍可能导致账户产生余额:

- 关户时选择通过支票提取账户余额,而客户未在90天内兑现该支票,进而导致支票交易被IBKR取消;或者,由于支票遗失、被盗或未送达,客户要求止付。

- 关户时选择通过电子渠道(如电汇、ACH、EFT)提取账户余额,但资产后被接收银行退回了IBKR。这可能是由于客户在接收银行处的账户已关闭或IBKR的账户名称和银行的账户名称不一致(如第三方转账的情况),导致接收银行拒收并退回资金。

- 账户被关后收到了之前多扣的股息税退还的税款。

- 开户人在账户未成功开立前向账户存入了资金,而该账户一直未被IBKR批准或被开户人遗弃。

- 关户时选择将资产转至其它经纪商,但资产在关户后被经纪商退回。

提取资产

要提取现金,请登录客户端,依次选择转账与支付和转账资金菜单,然后系统会显示可用的取款方式及您在账户开立状态时创建的银行存取款指令列表。选择一个适用于要提取的币种的可用存取款指令。

如您的账户内有持仓,请联系退回持仓的经纪商,请求将该笔持仓重新转回。请注意,您无法通过已关闭的账户提交委托单平仓。

常见问题解答

问:如果我不记得我的登录验证信息、无法登录客户端怎么办?

答:如您需要登录账户方面的帮助,请致电您当地的客服中心。为防止无授权的用户登录您的账户,此类请求需要口头验证您的身份。联系信息请见我们的网站。

问:我如何确定我账户中的余额?

答:您可通过账户活动报表了解账户余额及其组成。每日、每月及年度报表可通过客户端的报告/税务报告菜单在线查看。

问:我可否重开已关闭的账户?

答:已关闭很长时间且只是为了提取资产而申请重开的账户通常不能重开。如您希望重开账户并长期使用我们的经纪服务,请联系您当地的客服中心获取帮助。

问:如果我希望通过支票提取资金而我的地址变了会怎么样?

答:如果您的账户可通过支票提取资金(只支持美元取款且要求客户有美国的邮寄地址)而您记录在我们这里的地址不再准确,则您将无法在线更改您的地址。在这种情况下,请联系客服告知我们您的最新地址,客服人员将指导您如何上传驾照或其它可被接受的文件副本。

问:如果我想通过电子渠道取款而我的账户没有有效的银行存取款指令,这种情况下怎么办?

答:如果您目前没有可用的银行存取款指令,请登录客户端并使用“转账与支付”菜单添加新的指令。请注意,IBKR有权通过口头验证及/或要求客户提交文件的方式来验证新的存取款指令。该验证步骤旨在防止客户因无授权的第三方转账而蒙受损失。

问:开户实体的银行账户被注销了或实体不再存在了。这种情况下如何取款?

答:如果无法以关户时的账户持有人的名义取款,则IBKR将尝试按实体所有人的所有权比例来向所有人分配资金。请注意,这通常要求所有人提交文件来证明其身份及其所有权权益,并提交有所有人签字的保证和补偿书,承诺其提供的信息是准确的,且除他们以外,没有其它所有人或债权人对账户资金有索取权。IBKR也有权要求由律师提供独立意见,证明所有人提供的信息的准确性。

问:如果我不采取行动来提取已关账户内的资产会怎么样?

答:IBKR会尝试通过客户留在我司处的邮箱来通知已关账户的持有人账户内有余额。如果账户持有人在通知发出后30天内不采取行动取款,则将被收取20美元/月的已关账户费用。另外,还请注意,根据法规要求,IBKR有义务将“被遗弃账户”内的资产上交给客户居住的州政府(如果客户居住在美国以外,则上交给康涅狄格州)。对于账户多久无活动会被归为“不活跃”,各州的规定不同,但最短可为3年。关于如何从州政府出取回无主财产的详细信息,请见知识库文章2599。

费用概览

我们鼓励客户和潜在客户访问我们的网站了解详细费用信息。

最常见的几项费用有:

1. 佣金——取决于产品类型和挂牌交易所,以及您选择的是打包式(一价全含)还是非打包式收费。例如,美国股票佣金为每股0.005美元,每笔交易最低佣金为1.00美元。

2. 利息——保证金贷款需缴纳利息,IBKR采用国际公认的隔夜存款基准利率作为基础来确定自己的利率。然后我们将分等级在基准利率基础上应用一个浮动值(这样余额越大对应的利率就越有利)来确定实际利率。例如,对于美元计价的贷款,基准利率是联邦基金利率,而10万美元以内的余额利率会在基准利率的基础上加1.5%。此外,卖空股票的个人应注意,借用“难以借到”的股票还会有一笔特殊费用,以日息表示。

3. 交易所费用——取决于产品类型和交易所。例如,对于美国证券期权,某些交易所会对消耗流动性的委托单(市价委托单或适销的限价委托单)收取费用、对添加流动性的委托单(限价委托单)给与补贴。此外,许多交易所还会对取消或修改的委托单收取费用。

4. 市场数据——您并非一定要订阅市场数据,但是如果不订阅市场数据,您可以会产生月费用,具体取决于供应交易所及其订阅服务。我们提供市场数据助手工具,可根据您想交易的产品帮助您选择适当的市场数据订阅服务。要访问该工具,请登录客户端,点击支持然后打开市场数据助手链接。

5. 最低月活动费用——为迎合活跃客户的需求,我们规定如果账户产生的月佣金能达到最低月佣金要求,则可免交月活动费用;而如果产生的月佣金未能达到最低月佣金要求,则需缴纳差额作为活动费用。最低月佣金要求为10美元。

6. 杂费 - IBKR允许每月一次免费取款,后续取款将收取费用。此外,还会代收交易取消请求费用、期权和期货行权&被行权费用以及ADR保管费用。

更多信息,请访问我们的网站,从定价菜单中选择查看。

资金转账限制

简介

作为反洗钱工作的一部分,IBKR会对某些客户存款和取款实施限制。该等限制针对的是具有较高反洗钱风险之国家相关的转账,同时会考虑客户的居住地、取款目的地和转账资金的计价币种等因素。1下方对该等限制进行了简要介绍。

限制概述

- 在被认定为具有较高反洗钱风险之国家居住或拥有联系地址的客户不得将资金取到位于另一具有较高反洗钱风险之国家的账户,除非其在该国也有联系地址。

- 在被认定为具有较高反洗钱风险之国家居住或拥有联系地址的客户不得从位于另一具有较高反洗钱风险之国家的账户发起存款,除非其在该国也有联系地址。

- 在被认定为具有较高反洗钱风险之国家居住或拥有联系地址的客户只能将资金取到其曾从中收到过存款的自己名下的账户。

- 客户只能以基础货币、其本国货币或通用货币(如USD、EUR、HKD、AUD、GBP、CHF、CAD、JPY和SGD)取款。

- IBSG的客户只能以SGD、USD、CNH、HKD和GBP取款。

- IBKR会对客户取款的目标银行数目进行限制,不论客户或银行的所在国家或地区。

请注意,客户如果要创建被限制的在线银行指令或发起被限制的存款或取款,系统会阻止其操作并报错。

1在决定一个国家是否存在较高反洗钱风险时,我们会参考金融行动特别工作组(FATF)提供的信息,金融行动特别工作组是为打击洗钱、恐怖主义融资和其它威胁国际金融体系及其它反洗钱指数完整的行为而成立的政府间组织。

Notification Regarding Third-Party Wire Withdrawals

Certain Interactive Brokers (“IBKR”) accounts are eligible to request withdrawal of funds to third parties by bank wire. These requests are subject to review and approval at IBKR’s sole discretion. This program is described on the IBKR website here.

After a due diligence review, IBKR may allow withdrawals to a third party for purposes like:

• Withdrawal for purchase of a home or mortgage payoff

• Withdrawal to a spouse, parent, sibling, or child of source account holder

• Withdrawal to an account held by one of the accountholders of a joint account or vice versa.

• Withdrawal from trust account to a beneficiary

• Payment of certain account expenses

• Tax payments

• IRA qualified charitable distributions

IBKR will generally not approve the following types of third-party withdrawals:

• Private investments

• Repayment of loans

• Withdrawals to companies owned by the accountholder

• Payment for purchase of goods or services

• Withdrawals to individuals other than spouse, parent, sibling or child of account holder

Withdrawing Funds from a Closed Account

Introduction

Clients who elect to close their account must first ensure that all balances (e.g., cash and positions) have been withdrawn or transferred before the account can be closed. Once closed, the account is then restricted from further transactions, however, there are situations where assets may be credited to the account despite it being closed. As disclosed at the point of account closing, cash balances credited to an account after it has been closed are automatically converted to the base currency, regardless of amount, since the trading platform is no longer available to facilitate conversions.

The following article provides background as to how such situations may occur and the steps clients can take to withdraw the assets.

Post-Closure Balances

While it is uncommon for credits to be applied to an account once closed, the events which cause this to happen generally arise from the following:

- The account was closed via disbursement issued in in the form of a check which the client does not present for payment for 90 days and is therefore cancelled by IBKR; or, where the client requests a stop payment due to loss, theft or non-delivery of the check.

- The account was closed via an electronic disbursement (e.g., wire, ACH, EFT) later returned to IBKR by the receiving bank. This can occur if the receiving bank decides to reject and return the funds because the client’s bank account is closed or if the title of the account at IBKR differs from the bank account to which it is being deposited (i.e., a 3rd party transfer).

- A credit adjustment is applied to the account after it has closed to correct an over-withholding of taxes on a prior period dividend.

- An applicant deposited funds prior to the account being opened and the application was never approved by IBKR or was abandoned by the applicant.

- The account was closed via transfer to another broker who later returns the assets after the account has closed.

Withdrawing Assets

To withdraw cash, log into the Client Portal, select the Transfer & Pay and then Transfer Funds menu options and you will be presented with the option to make a withdrawal and a list of available banking instructions which you created while the account was open. Select an instruction that is active and applicable to the denomination of the currency to be withdrawn.

If your account has positions, please contact the broker who returned the positions to request that they be transferred back. Note that you will not be able to submit orders to close positions in a closed account.

FAQs

Q. What do I do if I don't recall my login credentials and am unable to log into the Client Portal?

A. If you require assistance logging into your account, you will need to contact your local Client Service Center via telephone. Such requests require verbal verification of your identity as a protection from unauthorized users. Contact information is available on our website.

Q. How do I determine the credit balance in my account?

A. The account balance and its composition can be found in your activity statement. Daily, monthly and annual statements are available online via the Client Portal through the Reports/Tax Reports menu option.

Q. Am I able to reopen an account that has been closed?

A. Accounts that have been closed for an extended period or are attempting to reopen solely for the purpose of withdrawing assets are generally not eligible to be reopened. If you intend to reopen the account to establish an ongoing brokerage relationship, please contact your local Client Service Center for assistance.

Q. What happens if I want to withdraw the funds via check and my address has changed?

A. If your account is eligible to withdraw funds via check (only available for US currency withdrawals by customers with a US mailing address) and your mailing address on record is no longer accurate, you will not be able to change your address online. In this instance, please contact Client Services to inform us of your new address and receive instructions on how to upload a copy of a driver's license or other acceptable document.

Q. What happens if I want to withdraw the funds electronically and my account does not already have a valid banking instruction on file?

A. If you currently do not have an active banking instruction on file, please log into the Client Portal and add a new instruction using the Transfer & Pay menu option. Note that IBKR reserves the right to verify new instructions via verbal confirmation and/or submission of qualifying documentation. This verification step is intended to protect against unauthorized transfers to a 3rd party.

Q. The entity which owned the account no longer has a bank account or is no longer in existence. How can the funds be withdrawn?

A. In the event the funds are unable to be withdrawn and distributed in the name of account holder at the point of account closure, IBKR will seek to distribute the funds to the entity owners based on their pro rata share of ownership. Note that this will generally require submission of documentation evidencing the owners and their ownership interests as well as a warranty and indemnification letter executed by the owners that the information they provide is accurate and there aren’t any other owners or creditors to whom the funds are owned. IBKR also reserves the right to request an independent opinion of counsel verifying the accuracy of the information provided.

Q. What happens if I do not act to withdraw assets in a closed account?

A. IBKR will attempt to notify closed accounts of a credit balance using the email address of record. Account holders who do not act to withdraw balances within 30 days after notice has been sent are subject to a monthly closed account fee of $20. Also note that IBKR is subject to statutes which require that assets in accounts deemed "abandoned" be turned over to the state in which the client resides (or Connecticut if the client resides outside the U.S.). The period of inactivity by which an account is considered "inactive" varies by state, but can be as low as 3 years. See Knowledge Base Article 2599 for details regarding retrieving unclaimed property from the state.

IB LLC大宗商品账户保证金要求

引言

作为一家在19个国家或地区提供期货交易的全球性经纪商,IB受多种监管要求的约束,某些监管要求仍保留了在日末计算一次保证金的概念,而IB的保证金是连续、实时计算的。为满足大宗商品监管要求并以务实的方式控制经济风险,我们会在收盘时应用两种保证金计算方式,两种方式计算得出的保证金要求须同时满足。两种方式的概述如下。

概述

所有定单在执行前均须满足初始保证金要求,执行后则须始终满足维持保证金要求。由于某些产品的日中保证金可能会低于交易所要求的最低保证金比例,为确保日末能满足保证金要求,IB通常会在休市前清算头寸,而不是要求客户追加保证金。然而,如果账户在休市时仍不满足保证金要求,我们会通知客户追加保证金,同时仅允许客户做减少占用保证金的交易,如在之后的第三个工作日休时仍不能满足最初的要求,则头寸将被清算。

在确定是否需追加保证金时,IB会应用实时计算和监管计算这两种方式,而某些情况下,这两种方法得出的结果可能不同:

实时:在本方法下,初始保证金是用同一个时间点收集的头寸和价格计算的,不考虑产品所在的交易所及正式的休市时间;鉴于大部分交易所的交易时间均接近连续,我们认为本方法有其适用性。

监管:在本方法下,初始保证金是用各家交易所常规交易时间终止时收集的头寸和价格计算的。比如,对于交易香港交易所、EUREX和CME期货产品的客户,保证金要求将根据各家交易所休市时的信息计算。

影响

交易单一时段、单一国家或地区的期货的客户不受影响。在某个交易所的常规交易时段及盘后交易时段交易、或在不同国家或地区的交易所(这些交易所的休市时间不同)交易的客户更可能受影响。比如,一个客户在香港常规交易时段开仓期货合约并在美国交易时段平仓,则保证金要求只取决于开仓时的头寸。在新的计算方式下,这种交易将适用不同的保证金要求,甚至产生在当前方法下不存在的追加保证金。下表举例说明了该情况。

举例

本例试图说明,如果一个同时在亚洲和美国两个时区交易期货的客户在延长的交易时段(即在常规交易时段以外、该日已正式休市时)交易时会如何受影响。本例中,客户在香港常规交易时段开仓,并在延长的交易时段内平仓,进而腾出资金在美国常规交易时段开仓。为说明起见,假设交易损失了1,000美元。本例说明,监管的日末保证金计算方法可能不能识别在正式休市后进行的会占用保证金的交易,因此产生了追加初始保证金的要求。

| 天数 | 时间(美东) | 事件 |

初始头寸 |

结束头寸 | IB保证金 | 监管保证金 | |||

| 含贷款的净资产 | 维持 | 初始 | 隔夜 | 追加保证金 | |||||

| 1 | 22:00 | 买1份 HHI.HK | 无 | 1份HHI.HK多头 | $10,000 | $3,594 | $4,493 | 不适用 | 不适用 |

| 2 | 04:30 | 香港交易所正式休市 | 1份HHI.HK多头 | 1份HHI.HK多头 | $10,000 | $7,942 | $9,927 | $4,493 | 不适用 |

| 2 | 08:00 | 卖1份HHI.HK | 1份HHI.HK多头 | 无 | $9,000 | $0 | $0 | $0 | 不适用 |

| 2 | 10:00 | 买1份ES | 无 | 1份ES多头 | $9,000 | $2,942 | $3,677 | 不适用 | 不适用 |

| 2 | 17:00 | 美国交易所正式休市 | 1份ES多头 | 1份ES多头 | $9,000 | $5,884 | $7,355 | $9,993 | 是 |

| 3 | 17:00 | 美国交易所正式休市 | 1份ES多头 | 1份ES多头 | $9,000 | $5,884 | $7,355 | $5,500 | 否 |

Funds Transfer Restrictions

INTRODUCTION

As part of its anti-money laundering efforts, IBKR implements restrictions on certain client deposits and withdrawals. These restrictions apply to transfers associated with countries considered to have elevated AML risk and consider factors such as the client’s residency, the withdrawal destination and the denomination of the currency being transferred.1 An outline of these restrictions is provided below.

OVERVIEW OF RESTRICTIONS

- Clients residing or maintaining an address in a country designated as having elevated AML risk may not withdraw funds to an account located in another country that has elevated AML risk unless they also maintain an address in that country.

- Clients residing or maintaining an address in a country designated as having elevated AML risk may not deposit funds from an account located in another country having elevated AML risk unless they also maintain an address in that country.

- Clients residing or maintaining an address in a country designated as having elevated AML risk may only withdraw funds to an account from which that client received a first-party deposit.

- Clients may only withdraw funds in their base currency, their home country’s currency or common currencies (e.g. USD, EUR, HKD, AUD, GBP, CHF, CAD, JPY and SGD).

- IBSG clients may only withdraw in SGD, USD, CNH, EUR, GBP and HKD.

- IBKR may restrict the number of banks that a client may send money to, regardless of the domicile of the client or the bank.

- A change to your base currency requires a minimum of 5 days before withdrawal instructions can be entered and a withdrawal request can be processed.

Note that clients who attempt to create an online banking instruction or initiate a deposit or withdrawal which is restricted will be blocked from creating that instruction or initiating that transaction and will be presented with an online error message.

1In determining whether a country is associated with elevated AML risk, consideration is given to information provided by the Financial Action Task Force (FATF), an intergovernmental organization which promotes measures for combating money laundering, terrorist financing and other related threats to the integrity of the international financial system and other public AML indices.