Information regarding high precision forex quotes

Overview:

Clients wishing to see forex (IDEALPRO) market data in a more detailed way can now control the order book display mode via the Global Configuration. In order to access this feature you must use TWS release 944.2b or higher. The display mode selection allows the order book to be viewed either as:

- Rounded prices (default): market data is rounded out to the next 0.5 pip. This is identical to the current display functionality for the IB trading platforms. This setting provides a more stable visible quote and a larger ‘top-of-book’ size since it includes the available size at multiple price levels up to the rounded price.

- Unrounded prices: market data is visible in 0.1 pip increments. This allows you to see prices in a more granular fashion, but the displayed values will change more rapidly and the sizes for the top-of-book may appear to be smaller.

It is important to understand that either display mode accesses the same IDEALPRO order book. Order submission will still be in 0.5 pip increments and orders submitted in either display mode will execute in exactly the same way. As in the past (and currently), in cases where the order book has prices at better than your order’s limit price, you will receive the full price improvement.

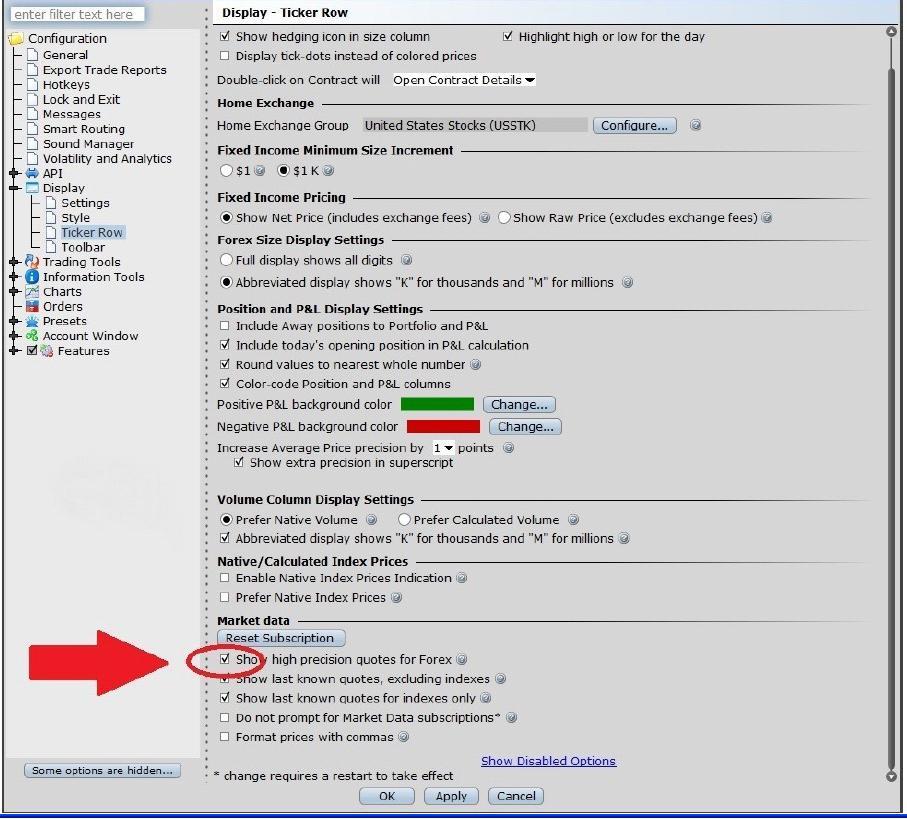

Instructions on how to display high precision forex quotes

In Global Configuration go to Display, choose Ticker Row and then at the bottom of the window in the Market Data section tick Show high precision quotes for Forex. Then press apply or ok to enable the new setting.

"EMIR": Reporting to Trade Repository Obligations and Interactive Brokers Delegated Service to help meet your obligations

1. Background: In 2009 the G20 pledged to undertake reforms aimed at increasing transparency and reducing counterparty risk in the OTC derivatives market post the financial crisis of 2008. The European market infrastructure regulation (“EMIR”) implements most of these pledges in the EU. EMIR is a EU regulation and entered into force on 16 August 2012.

2. Financial instruments and asset classes reportable under EMIR: OTC and Exchange Traded derivatives for the following asset classes: credit, interest, equity, commodity and foreign exchange derivatives Reporting obligation does not apply to exchange traded warrants.

3. Who do EMIR reporting obligations apply to: Reporting obligations normally apply to all counterparties established in the EU with the exception of natural persons. They apply to:

* Financial Counterparties (“FC”)

* Non-financial counterparties above the clearing threshold (“NFC+”)

* Non-financial counterparties below the clearing threshold (“NFC-“)

* Third country Entities outside the EU (“TCE”) in some limited circumstances

The reporting obligations essentially apply to any entity established in the EU that has entered into a derivatives contract.

4. Financial counterparties (“FC”): include banks, investment firms, credit institutions, insurers, UCITS and pension schemes and Alternative Investment Fund managed by an AIFM. The Alternative Investment Fund (“AIF”) will only become an FC if the manager of that AIF is authorised under the Alternative Investment Fund Managers Directive (“AIFMD”), so a fund outside the EU may be subject to EMIR reporting requirements.

5. Non-Financial Counterparty (“NFC”): A NFC is defined as an undertaking established in the EU other than those defined as a FC or a Central Counterparty (“CCP”), like the Clearing Houses. NFCs have lesser obligations than FCs. But when an NFC breaches a “clearing threshold” it becomes an NFC+, when it is subject to almost the same obligations as FCs (including collateral and valuation reporting). NFCs below the clearing threshold are known as NFC-s. In practice anyone other than a natural individual person (i.e. an individual or individuals operating a joint

account) is defined as an NFC- and subject to reporting obligations.

INTERACTIVE BROKERS DELEGATED REPORTING SERVICE TO HELP MEET YOUR REPORTING OBLIGATIONS

6. What service will Interactive Brokers offer to its customers to facilitate them fulfill their reporting obligations i.e. will it offer a delegated service for trade reporting as well as facilitating issuance of LEI: As noted above, both FCs and NFCs must report details of their transactions (both OTC and ETD) to authorized Trade Repositories. This obligation can be discharged directly through a Trade Repository, or by delegating the operational aspects of reporting to the counterparty or a third party (who submits reports on their behalf).

Interactive Brokers intends to facilitate the issuance of LEIs and offer delegated reporting to customers for whom it executes and clear trades, subject to customer consent, to the extent it is possible to do so from an operational, legal and regulatory perspective.

If you are subject to EMIR Reporting you will shortly be able to log into the IB Account Management system and apply for an LEI and delegate your reporting to Interactive Brokers.

We intend to include valuation reporting but only if and to the extent and for so long as it is permissible for Interactive brokers to do so from a legal and regulatory perspective and where the counterparty is required to do so (i.e. in cases where it is a FC or NFC+).

However, this would be subject to condition that Interactive Brokers uses its own trade valuation for reporting purposes.

7. Can EMIR reporting be delegated: EMIR allows either counterparty to delegate reporting to a third-party. If a counterparty or CCP delegates reporting to a third party, it remains ultimately responsible for complying with the reporting obligation. Likewise, the counterparty or CCP must ensure that the third party to whom it has delegated reports correctly. Brokers and dealers do not have a reporting obligation when acting purely in an agency capacity. If a block trade gives rise to multiple transactions, each transaction would have to be reported.

FUNDS AND SUB-FUNDS - The obligations under EMIR are on the counterparty which may be the fund or sub-fund. The fund or sub-fund that is the principal to transactions will have to provide details of their classification (FC, NFC+ or NFC-), authorization for delegated reporting and Legal Entity Identifier (“LEI”) application.

8. Exemptions under Article 1(4) and 1(5) of EMIR: Articles 1(4) and 1(5) of EMIR exempt certain entities from some or all of the obligations set out in EMIR, depending on their classification. Specifically, exempt entities under Article 1(4) are exempt from all obligations set out in EMIR, while exempt entities under Article 1(5) are exempt from all obligations except the reporting obligation, which continues to apply.

9. Entities qualifying under Article 1(4) and 1(5) of EMIR: Article 1(4) initially applied only to EU central banks, Union public bodies involved in the management of public debt and the Bank for International Settlements. Subsequently the

application of the Article 1(4) exemption was extended to include the central banks and debt management offices of the United States and Japan. The Commission has indicated that further foreign central banks and debt management offices may be added in the future if they are satisfied that equivalent regulation is put in place in those jurisdictions. Article 1(5) broadly exempts the following categories of entities:

- Multilateral development banks;

- Non-commercial public sector entities owned and guaranteed by central government; and

- The European Financial Stability Facility and the European Stability Mechanism.

10. OTC and Exchange Traded Derivatives: There is no distinction between reporting of exchange traded derivatives (“ETDs”) and OTC contracts within the level 1 regulations, implementing technical standards, or regulatory technical standards of ESMA.

The contract is to be identified by using a unique product identifier. In addition, a unique trade identifier will be required for transactions. In the event that a globally agreed system of product identifiers does not materialise, it has been suggested that International Securities Identification numbers (“ISIN”), Alternative Instruments Identifiers (“AII”), or Classification of Financial Instruments Codes (“CFI”) may serve as alternatives.

11. Trade repository Interactive Brokers use: Interactive Brokers (U.K.) Limited will use the services of CME ETR, which is part of the CME Group.

12. Issuance of Legal Entity Identifiers (“LEI”)

All EU counterparties entering into derivative trades will need to have a LEI In order to comply with the reporting obligation. The LEI will be used for the purpose of reporting counterparty data.

A LEI is a unique identifier or code attached to a legal person or structure, that will allow for the unambiguous identification of parties to financial transactions.

“EMIR”: Further Information on Reporting to Trade Repository Obligations

13. Thresholds which determine whether an NFC is an NFC+ or NFC-: Breaching any of the following clearing threshold values will mean classification as an NFC+. Positions must be calculated on a notional, 30-day rolling average basis:

• EUR 1 billion in gross notional value for OTC credit derivative contracts;

• EUR 1 billion in gross notional value for OTC equity derivative contracts;

• EUR 3 billion in gross notional value for OTC interest rate derivative contracts;

• EUR 3 billion in gross notional value for OTC FX derivative contracts; and

• EUR 3 billion in gross notional value for OTC commodity derivative contracts and other OTC derivative contracts not covered above.

For the purpose of calculating whether a clearing threshold has been breached, an NFC must aggregate the transactions of all non-financial entities in its group (and determine whether or not those entities are inside or outside the EU) but discount transactions entered into for hedging or treasury purposes. The term “hedging transactions” in this context means transactions objectively measureable as reducing risks directly relating to the commercial activity or treasuring financing activity of the NFC or its group.

14. Reporting Of Exposures: FCs and NFC+s must report on:

* Mark-to-market or mark-to-model valuations of each contract

* Details of all collateral posted, either on a transaction or portfolio basis (i.e. where collateral is calculated on the basis of net positions resulting from a set of contracts rather than being posted on a transaction by transaction basis)

15. Timetable to report to Trade repositories: The reporting start date is 12 February 2014:

* New contracts they enter into on or after February 12th, on a trade date +1;

* Positions open from contracts entered into on or after 16 August 2012 and still open on February 12th, 2014 must be reported to a trade repository by February 12th 2014;

* Positions open from contracts entered into before 16th August and still open on February 12th, 2014 must be reported to a trade repository by 13th May 2014;

* Reporting of valuation and collateral must be reported to a trade repository by 12th August 2014;

* Contracts that were either entered before, on or after 16 August 2012 but not open on 12th February 2014 must be reported to a trade repository by February 12th, 2017.

16. What must be reported and when: Information must be reported on the counterparties to each trade (counterparty data) and the contracts themselves (common data).

There are 26 items that must be reported with regard to counterparty data, and 59 items that must be reported with regard to common data. These items are set out within tables 1 and 2 of the Annex to the ESMA’s Regulatory technical standards on minimum details to be reported to trade repositories.

Counterparties and CCPs have to make a report:

* when a contract is entered into

* when a contract is modified

* when a contract is terminated

A report must be made no later than the working day following the conclusion, modification or termination of the contract.

17. What has to be reported and who is responsible for reporting: Reporting applies to both OTC derivatives and exchange traded derivatives. The reporting obligation applies to counterparties to a trade, irrespective of their classification. Please note:

* Reporting of valuation and collateral is only required for FCs and NFC+s

* Every trade must be normally be reported by both counterparties.

THIS INFORMATION IS GUIDANCE FOR INTERACTIVE BROKERS CLEARED CUSTOMERS ONLY

NOTE: THE INFORMATION ABOVE IS NOT INTENDED TO BE A COMPREHENSIVE, EXHAUSTIVE NOR A DEFINITIVE INTERPRETATION OF THE REGULATION, BUT A SUMMARY OF ESMA’S EMIR REGULATION AND RESULTING TRADE REPOSITORY REPORTING OBLIGATIONS.

Determining Tick Value

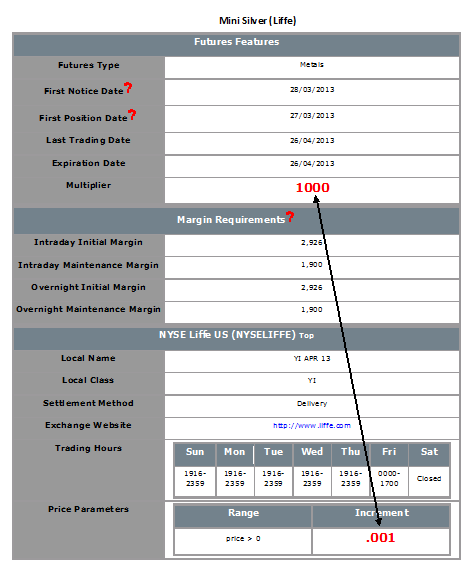

Financial instruments are subject to minimum price changes or increments which are commonly referred to as ticks. Tick values vary by instrument and are determined by the listing exchange. IB provides this information directly from the Contract Search tool on the website or via the Trader Workstation (TWS). To access from TWS, enter a symbol on the quote line, right click and from the drop-down window select the Contract Info and then Details menu options. The contract specifications window for the instrument will then be displayed (Exhibit 1).

To determine the notional value of a tick, multiple the tick increment by the contract trade unit or multiplier. As illustrated in the example below, the LIFFE Mini Silver futures contact has a tick value or minimum increment of .001 which, when multiplied by the contract multiplier of 1,000 ounces, results in a minimum tick value of $1.00 per contract. Accordingly, every tick change up or down results in a profit or loss of $1.00 per LIFFE Mini Silver futures contract.

Exhibit 1

Converting Currency Balances

Account holders may find themselves holding balances in currencies other than their designated Base Currency as a result of trades in products denominated in a different currency or from profits/losses directly associated with Forex trading. In these cases, IB does not act to automatically convert balances back to the Base Currency as this action would require assumptions as to the account holder's desired currency exposure as well as the trade price at which they would be willing to close the position.1 IB does, however, provide those account holders who are not active Forex traders an expedited 3 step process for converting such positions at an individual or aggregate currency level. These steps are outlined below.

Please note the feature below is specific to Trader Workstation. If you are using WebTrader, you must place an order to convert currency. Please see the following link for more information on WebTrader Order Entry: WebTrader Order Entry

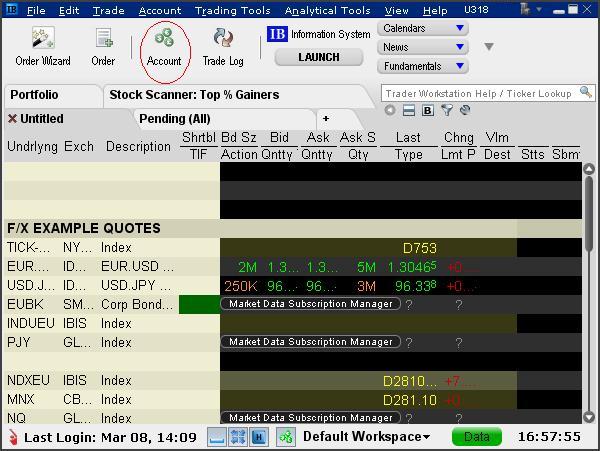

Step 1 – View Currency Balances

Select the Account icon from the TWS header.

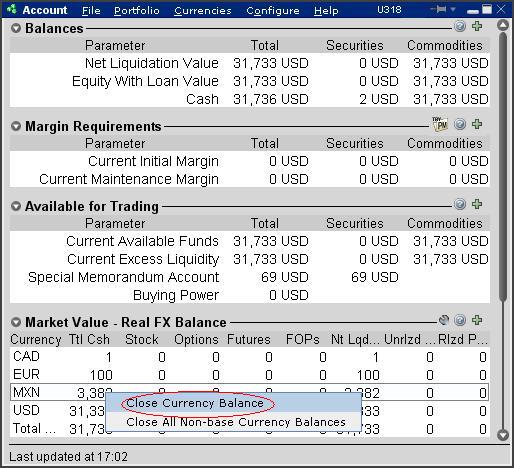

Step 2 - Select the Position(s) to Close

From the Account window, scroll down to the section titled "Market Value - Real FX Balance", place your cursor on a currency you wish to convert and right-click on the mouse to display the Close Currency menu option. You will be provided with two options, Close Currency Balance which will close the single currency you've selected and Close All Non-base Currency Balances which will close all.

Depending upon the currency quantity you are converting and the market rate, a residual balance may remain as conversions can only be performed in whole currency amounts (e.g. no cents). The following message will appear advising of this situation and the automated conversion which will take place thereafter.

.jpg)

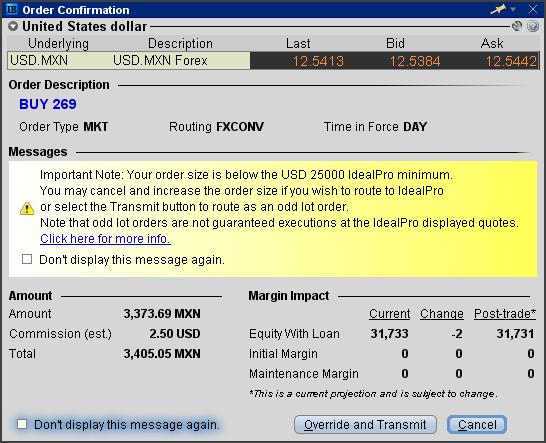

Step 3 - Review & Transmit Order

Next, an order line for the conversion trade will be populated on the TWS. The order will be set up with default conditions of a market order (“MKT”), good for that day and for the current position quantity2. Select "T" to generate the Order Confirmation window using the default conditions or set the price and time conditions as desired.

Note: At times the use of a market order when performing a currency conversion may result in an order rejection due to margin requirements. In order to avoid this, traders may wish to update the order type to a limit order (“LMT”) and set up a limit price. The limit price is the worst price you are willing to trade at; if a better price is available your order will be executed at a better price.

Preview the order from the Order Confirmation window. Note that if your order size is below the IdealPro USD 25,000 equivalent minimum, it will be routed to the odd lot order book. Select the Transmit button when your desired order has been set up.

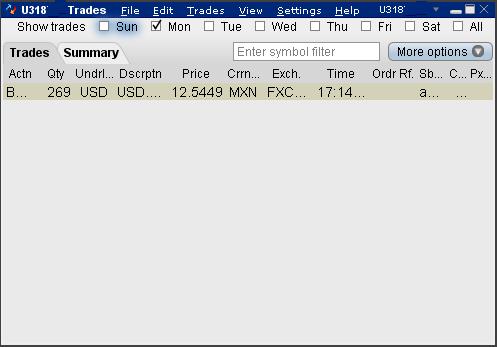

Once your order has been executed, it may be reviewed through the Trade Log icon from the TWS header.

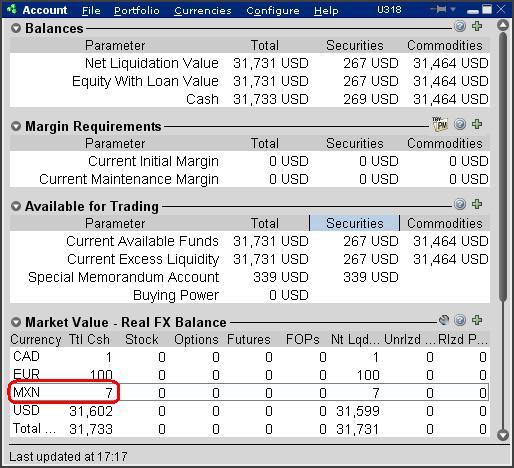

In the event a residual balance remains, it will be displayed within the Account window (e.g. MXN 7 equals approximately USD 0.56) until the following business day at which point it will be automatically converted to the Base Currency.

For additional information on IB Forex, please see: An Introduction to Forex (FX)

1 IB will act to automatically convert non-Base Currency balances only where the balance is nominal (i.e., below USD 5 equivalent and assuming no subsequent trade activity through settlement) and when the customer requests to close the account (where the balances are below USD 1,000 equivalent)

2 Note that the position quantity created by this default will not include balances which are in an accrual state (e.g. interest, dividends).

Compatibility between MetaTrader and Interactive Brokers

Overview:

Interactive Brokers (IBKR) provides to its account holders a variety of proprietary trading platforms at no cost and therefore does not actively promote or offer the platforms or add-on software of other vendors. Nonetheless, as IBKR's principal trading platform, the TraderWorkstation (TWS), operates with an open API, there are numerous third-party vendors who create order entry, charting and various other analytical programs which operate in conjunction with the TWS for purposes of executing orders through IBKR. As these API specifications are made public, we are not necessarily aware of all vendors who create applications to integrate with the TWS but do offer a program referred to as the Investors Marketplace which operates as a self-service community bringing together third party vendors who have products and services to offer with IBKR customers seeking to fill a specific need.

While MetaQuotes Software is not a participant of IBKR's Investors Marketplace, they offer to Introducing Brokers the oneZero Hub Gateway so that MetaTrader 5 can be used to trade IBKR Accounts[1]. Clients interested would need to contact oneZero directly for additional assistance. Please refer to the Contact section from the following URL.

Note: Besides oneZero Hub Gateway, different vendors such as Trade-Commander, jTWSdata and PrimeXM also offer a software which they represent, acts as a bridge between MetaTrader 4/5 and the TWS. As is the case with other third-party software applications, IBKR is not in a position to provide information or recommendations as to the compatibility or operation of such software.

1: oneZero is not available for Individual Accounts, please click here for more information on Introducing Brokers.

Considerations for Optimizing Order Efficiency

Account holders are encouraged to routinely monitor their order submissions with the objective of optimizing efficiency and minimizing 'wasted' or non-executed orders. As inefficient orders have the potential to consume a disproportionate amount of system resources. IB measures the effectiveness of client orders through the Order Efficiency Ratio (OER). This ratio compares aggregate daily order activity relative to that portion of activity which results in an execution and is determined as follows:

OER = (Order Submissions + Order Revisions + Order Cancellations) / (Executed Orders + 1)

Outlined below is a list of considerations which can assist with optimizing (reducing) one's OER:

1. Cancellation of Day Orders - strategies which use 'Day' as the Time in Force setting and are restricted to Regular Trading Hours should not initiate order cancellations after 16:00 ET, but rather rely upon IB processes which automatically act to cancel such orders. While the client initiated cancellation request which serve to increase the OER, IB's cancellation will not.

2. Modification vs. Cancellation - logic which acts to cancel and subsequently replace orders should be substituted with logic which simply modifies the existing orders. This will serve to reduce the process from two order actions to a single order action, thereby improving the OER.

3. Conditional Orders - when utilizing strategies which involve the pricing of one product relative to another, consideration should be given to minimizing unnecessary price and quantity order modifications. As an example, an order modification based upon a price change should only be triggered if the prior price is no longer competitive and the new suggested price is competitive.

4. Meaningful Revisions – logic which serves to modify existing orders without substantially increasing the likelihood of the modified order interacting with the NBBO should be avoided. An example of this would be the modification of a buy order from $30.50 to $30.55 on a stock having a bid-ask of $31.25 - $31.26.

5. RTH Orders – logic which modifies orders set to execute solely during Regular Trading Hours based upon price changes taking place outside those hours should be optimized to only make such modifications during or just prior to the time at which the orders are activated.

6. Order Stacking - Any strategy that incorporates and transmits the stacking of orders on the same side of a particular underlying should minimize transmitting those that are not immediately marketable until the orders which have a greater likelihood of interacting with the NBBO have executed.

7. Use of IB Order Types - as the revision logic embedded within IB-supported order types is not considered an order action for the purposes of the OER, consideration should be given to using IB order types, whenever practical, as opposed to replicating such logic within the client order management logic. Logic which is commonly initiated by clients and whose behavior can be readily replicated by IB order types include: the dynamic management of orders expressed in terms of an options implied volatility (Volatility Orders), orders to set a stop price at a fixed amount relative to the market price (Trailing Stop Orders), and orders designed to automatically maintain a limit price relative to the NBBO (Pegged-to-Market Orders).

The above is not intended to be an exhaustive list of steps for optimizing one's orders but rather those which address the most frequently observed inefficiencies in client order management logic, are relatively simple to implement and which provide the opportunity for substantive and enduring improvements. For further information or questions, please contact the Customer Service Technical Assistance Center.

IdealPro - Large-Size Order Facility

Overview:

The IdealPro Forex market center provides a Large-Size Order facility specifically intended for accounts which regularly submit orders in quantities greater than standard order maximums and are willing to trade outside the NBBO associated with the standard order minimum/maximum bands in an attempt to obtain faster fills.

Background:

Standard orders submitted through IdealPro are subject to minimum and maximum size restrictions which, when expressed in USD equivalents, generally range from $25,000 to $7,000,000 but vary by currency (see Forex Min/Max Order Sizes Chart). These size restrictions serve to provide for the most optimal combination of liquidity and spreads, minimize the impact of erroneous or “fat finger” entries, and are intended to minimize any distortion which the submission of a large-size order may have upon supply or demand.

Orders submitted at a quantity below the standard order minimums are considered odd lot orders and are subject to special handling and price quoting considerations (see Odd Lot FX Transactions). Account holders who wish to submit orders at quantities above the standard order maximum must first request to be qualified for the Large-Size Order facility. Unlike standard orders for which the quote covers any quantity within the stated minimum and maximum size restrictions, the quote associated with a Large-Sized Order is specific to the order quantity entered. In an effort to obtain the best execution possible and also to limit any market impact, Large-Sized Order quotes are

generated based upon an aggregation of quotes provided by interbank dealers along with

and internalized orders of other IB clients.

Outlined below are a series of FAQs addressing the features and considerations of the Large-Size Order

facility.

How do I become eligible to submit Large-Size Orders?

In order to become eligible to submit large-size orders through the Large-Size Order facility, you would need to first submit a request to Customer Service. Requests will be reviewed and considered based upon a number of factors including the applicant's prior trade history and account equity. Please allow up to 7 business days for completion of this review to take place.

What spreads are expected for Large-Size Orders?

In general, spreads for Large-Size Orders on IdealPro are expected to be greater than those for standard orders, however, other factors such as liquidity of the currency pair, time of the day and release of economic numbers or other data can also influence bid ask spreads and should also be taken into consideration.

What is the maximum available order size?

In general sizes up to 50 million of the base currency are available. As with bid-ask spreads, this may vary depending on a number of factors. The Large-Size Order facility will return the lower of the size requested and size available at the time of the request.

What order types are supported?

Account holders are strongly encouraged to use limit order types with the Large Size Order facility as market orders are susceptible to being filled at prices far lower/higher than the current displayed bid/ask particularly under volatile market conditions or where the order involves illiquid products. In addition, to protect from losses associated with significant and rapidly changing prices, IB will simulate client market orders as market with protection orders, establishing an execution cap seven basis points (0.07%) beyond the quoted bid/ask. While this cap is set at a level that is intended to balance the objectives of execution certainty and minimizing price risk, there exists a remote possibility that the execution of a market order will be delayed or may not take place.

How will prices be displayed?

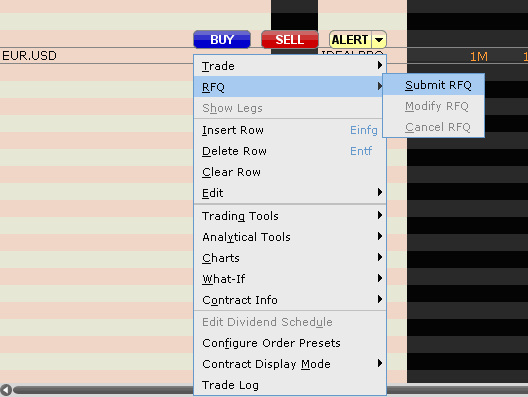

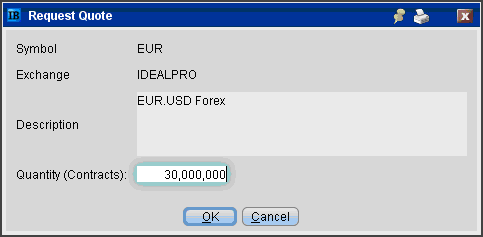

The TWS quote line will display dealable prices for a predefined amount once access to the Large-Size Order facility has been provided. To display prices, right-click on a given currency pair and then select the Choose RFQ and Submit RFQ menu options (Exhibit 1). You will then be prompted to provide the currency amount and then hit enter (Exhibit 2). The prices displayed (Exhibit 3) will time out after a certain time and you would have to repeat the request process to get another price again. We do not publish prices through other channels at the moment. The handling of the orders remains the same, regardless whether sent using the Large-Size Order facility, the quote screen, FX Trader or sent using an API.

Exhibit 1

Exhibit 2

Exhibit 3

.bmp)

Forex Basics

A Forex trade represents an exchange of one asset for another, similar in many respects to a stock trade. However, while in the case of the stock trade the assets being exchanged are cash for stock, in the Forex transaction the assets being exchanged are both cash, one denominated in a given currency and the other a different currency. Similar to the convention in which stocks are quoted, for example, in quantity of USD per share unit, in a currency pair the quote reflects the quantity of one currency unit which is required to buy (or which will be received if selling) another unit.

Take, for example the currency pair of EUR/USD quoted at 1.40. In accordance with industry quoting conventions, the first currency listed, the EUR, is the transaction currency or that which the trader wishes to buy or sell (also referred to as the base currency). The second currency listed, the USD, is the currency in which the transaction will be settled (referred to as either the settlement or quote currency). A trader seeking to buy 1 EUR given this quote would pay 1.40 USD and if seeking to sell 1 EUR would receive 1.40 USD.

Other items of note regarding Forex transactions are as follows:

IdealPro

IB’s venue for executing Forex trades, referred to as IdealPro, operates as an exchange-style order book, assembling quotes from the largest international Forex banks as well as other IB clients and market makers. IB imposes no markup to the quoted spreads but rather charges an explicit commission ranging from 0.2 to 0.10 basis points of the trade value depending upon your monthly trade amount, subject to a per order minimum of USD 2.00.

Quoting Conventions

In Forex markets the USD is generally considered the transaction currency for quoting purposes, that is the quotes are expressed as a unit of USD $1 per the other currency quoted in the pair (e.g., USD.CAD, USD.JPY, USD.CHF). The primary exceptions to this rule are the GBP, the EUR and the AUD which are quoted as GBP.USD, EUR.USD and AUD.USD, respectively. These quoting conventions are industry standard and orders cannot be submitted to IB’s IdealPro venue in an inverted format (e.g. USD.EUR).

These quoting conventions introduce special considerations when one is attempting to close out a specific cash balance denominated in a settlement currency which, based upon the current quote, may not be able to be closed out in its entirety. Please refer to the following article for additional details: Closing FX Positions Denominated in a Settlement Currency

Odd Lots

For purposes of maintaining adequate scale and competitive spreads, a minimum size of USD 25,000, or equivalent, is imposed on all IdealPro orders. Orders below this size are considered odd lots and their limit prices are not disclosed through IdealPro. While odd lot marketable orders are not likely to be executed at the inter-bank spreads afforded to IdealPro orders, they will generally be executed at prices only slightly inferior (1-3 ticks).

Trading Multi-Currency Products

When trading products which are denominated in a currency which you do not hold in your account, special attention must be paid to the Forex implications of such trades. Namely, if you do not hold or acquire the particular currency in the necessary amount and denomination prior to the trade, IB will automatically create a loan for those funds (assuming margin compliance). In addition, once you close out a non-base currency stock, option or futures position you are likely to be left with a residual Forex balance which IB will not automatically convert. Please refer to the following article for additional details: What happens if I trade a product denominated in a currency which I do not hold in my account?

Odd Lot FX Transactions

IB’s venue for executing Forex trades, referred to as IdealPro, operates as an exchange-style order book, assembling quotes from the largest global Forex banks and dealers as well as other IB clients and market makers. For purposes of maintaining competitive bid-ask spreads and optimal liquidity, a minimum size of USD 25,000, or equivalent, is imposed on all IdealPro orders. Orders below this size are considered odd lots and their limit prices are not disclosed through IdealPro even if inside the IdealPro bid-ask spread. As such, odd lot marketable limit orders are not guaranteed execution at the inter-bank spreads afforded to IdealPro orders, and will generally be executed at slightly inferior prices ranging from 1- 2 basis points* outside the IdealPro quote.

*Basis points are a unit of measure that describes the percentage change in value of a financial instrument. One basis point = 0.01% or 0.0001 in decimal form.

Closing FX Positions Denominated in a Settlement Currency

Price quoting for Forex pairs on IdealPro is subject to an industry convention whereby the relationship between the first pair (transaction currency) and second pair (settlement currency) is fixed and cannot be inverted. Considering, for example, pairs involving the USD, the following are examples where the USD is listed as the transaction currency: USD.CAD, USD.JPY and USD.CHF. Similarly, the GBP.USD, EUR.USD and AUD.USD are examples where the USD is listed as the settlement currency (a complete listing of quoting conventions for pairs executable via IdealPro can be found by typing IdealPro into the IB website search engine).

These quoting conventions introduce special considerations when one is attempting to close out a specific cash balance denominated in a settlement currency which, based upon the current quote, may not be able to be closed out in its entirety. To illustrate, assume the following transactions:

Day 1: Account holder maintaining USD 300,000 in a USD base currency account buys 10,000 shares of stock XYZ which is denominated in CAD at a price of 50.00. Also assume that the account holder does not convert USD into CAD prior to the stock purchase and therefore borrows the CAD necessary to settle the trade from IB. The USD.CAD closes at 1.0526 and XYZ at CAD 50.00 (no unrealized gain or loss). The end of day account balance is as follows:

| Position |

Position in Local Currency |

Position Translated into Base Currency |

| Cash - USD | 300,000.00 | $300,000.00 |

| Cash - CAD | (500,000.00) | ($475,014.25) |

| Stock - XYZ | 500,000.00 | $475,014.25 |

| NLV (in Base) | $300,000.00 |

Day 2: Assume no trade activity, the USD.CAD closes that day at 1.0309 and XYZ closes at CAD 52.00. (unrealized gain of USD 19,400.52). The end of day account balance is as follows:

| Position |

Position in Local Currency |

Position Translated into Base Currency |

| Cash - USD | 300,000.00 | $300,000.00 |

| Cash - CAD | (500,000.00) | ($485,013.10) |

| Stock - XYZ | 520,000.00 | $504,413.62 |

| NLV (in Base) | $319,400.52 |

Day 3: Account holder sells the 10,000 shares of XYZ at CAD 53.00 and the USD.CAD closes unchanged at 1.0309 (unrealized gain of USD 29,100.79). The end of day account balance is as follows:

| Position |

Position in Local Currency |

Position Translated into Base Currency |

| Cash - USD | 300,000.00 | $300,000.00 |

| Cash - CAD | 30,000.00 | $29,100.79 |

| Stock - XYZ | 0.00 | $0.00 |

| NLV (in Base) | $329,100.79 |

Day 4: Account holder seeks to close out the CAD 30,000.00 cash balance through the sale of CAD vs. the purchase of USD. Due to the quoting convention of this pair in which the order must be specified in a quantity of USD, the account holder is required to determine the USD equivalent of CAD 30,000.00 at the desired trade price. Assuming the account holder seeks to close the position at the market price of 1.0253 an order to buy 29,259 USD.CAD would be entered which, if executed, will result in a residual long CAD balance of 0.75. The end of day account balance is displayed below:

| Position |

Position in Local Currency |

Position Translated into Base Currency |

| Cash - USD | 329,259.00 | $329,259.00 |

| Cash - CAD | 0.75 | $0.73 |

| Stock - XYZ | 0.00 | $0.00 |

| NLV (in Base) | $329,259.73 |

Note, however, that in accordance with IB's policies regarding nominal Forex balances, residual balances of less than USD 5.00 equivalent will automatically be converted into the account holder's base currency upon settlement assuming no subsequent trade activity in that non-base currency has taken place in the interim. This is intended to minimize the actions required of the account holder to convert nominal non-base currency balances back into the designated base currency and also to convert fractional balances which could otherwise not be converted. IB does not charge a commission for these automated conversions.