期權到期前被行權

美式期權賣方(沽出方)在期權到期前隨時可能會被行權。也就是說,期權賣方在賣出期權後到期權到期或通過買回期權將頭寸平倉這段時間隨時可能會被行權。看漲或看跌期權所有者在期權到期前調用其權利即為提早行權。作為期權賣方,您無法控制期權被行權,也無法知曉其會何時發生。通常,越臨近到期,被行權的風險越大,但即使這樣,美式期權交易仍然隨時會發生被行權。

空頭看跌期權

賣出看跌期權時,賣方有義務在指定時間窗口內(到期日)以約定價格(行使價)買入底層股票或資產。如果期權的行使價低於股票的當前市價,則期權持有者把股票賣給期權賣方並不會獲利,因為市場價格比行使價要高。反過來,如果期權的行使價高於股票的當前市價,則期權賣方就會有被行權的風險。

空頭看漲期權

賣出看漲期權後,看漲期權的所有者有權在給定時間範圍內以約定價格從期權賣方買入股票。如果股票的市價低於期權的行使價,則對看漲期權持有者來說,以高於市價的價格買入股票沒有任何好處。但如果股票的市價高於期權的行使價,則期權持有者可以低於市價的價格買入股票。如果期權處於價內或如果即將派息且空頭看漲期權的內在價值低於股息,則空頭看漲期權會有被行權風險。

期權會發生什麼?

如果空頭看漲期權被行權,則空頭看漲期權持有者將被分配空頭股票。例如,如果ABC公司的股價為$55,行使價為$50的空頭看漲期權被行權,則空頭看漲期權將會轉換成價格為$50的空頭股票。然後賬戶持有人可以決定以$55的價格買回股票平倉空頭頭寸。100股的淨損失會是$500,再減去最開始賣出看漲期權時收到的權利金。

如果空頭看跌期權被行權,則空頭看跌期權持有者相當於是以看跌期權行使價多頭持有股票。例如,XYZ的股價為$90,空頭看跌期權賣方按行使價$96被分配了股票,則看跌期權賣方有責任以$96(高於市價)的價格買入股票。假設賬戶持有人以$90的價格平倉了多頭股票頭寸,那麼100股的淨損失會是$600,再減去最開始賣出看跌期權時收到的權利金。

期權被行權導致保證金不足

如果被行權發生在期權到期之前並且產生的股票頭寸導致保證金不足,則根據我們的保證金政策,賬戶將面臨自動平倉清算以重新滿足保證金要求。平倉清算並不只限於期權被行權產生的股票頭寸。

此外,對於期權價差的空頭邊被行權的賬戶,IBKR不會將其持有的多頭期權行權。IBKR無法推測多頭期權持有者的意圖,並且在到期前行使多頭期權將導致放棄期權的時間價值(時間價值通過賣出期權實現)。

到期後風險敞口、公司行動和除息

盈透證券會根據到期時間或公司行動相關事件採取積極措施降低風險。有關我們到期政策的更多信息,請閱讀知識庫文章“到期&公司行動相關清算”。

賬戶持有人應參閱“標準期權的特徵與風險”披露文件,IBKR在賬戶申請時便向所有有期權交易資格的客戶提供了此文件,其中明確說明了被行權風險。此文件還可在期權清算公司(OCC)網站上查看。

Risk Based Margin Considerations

| LLC Risk Based (i.e. Portfolio Margin) | Non-LLC Risk Based Margin | |

| $110,000 initial value requirement | Yes | N/A |

| Minimum equity to operate on margin | USD 100,000 | IB-HK: USD 2,000 IB-AU: AUD 2,000 IB-LUX, IB-IE and IB-CE: EUR 2,000 IB-SG: SGD 2,000 |

| Full options trading approval | Yes | N/A |

| PDT | Yes | N/A |

| Stress testing | Yes | Yes |

| Dynamic House Scanning Charges (TOMS) ¹ | Yes | Yes |

| Shifts in option Implied Volatility (IV) | Yes | Yes |

| A $0.375 multiplied by the index per contract minimum is computed (Only applied to Portfolio Margin eligble products) | Yes | Yes |

| Initial margin will be 110% of Maintenance Margin (US securities only) | Yes | Yes |

| Initial margin will be 125% of Maintenance Margin (Non-US securities) | Yes | Yes |

| Extreme Price Scans | Yes | Yes |

| Large Position Charge (A position which is 1% or more of shares outstanding) | Yes | Yes |

| Days to Liquidate (A large position in relation to the average daily trading volume, which may result in higher initial margin requirements) | Yes | Yes |

| Global Concentration Charge (2 riskiest position stressed +/-30% remaining assets +/-5%) | Yes | Yes |

| Singleton Margin Method for Small Cap Stocks (Stress Test which simulates a price change reflective of a $500 million USD in market capitalization)² | Yes | Yes |

| Singleton Margin Method for stocks domiciled in China (Stress Test which simulates a price change reflective of a $1.5 billion USD in market capitalization)² | Yes | Yes |

| Default Singleton Margin Method (Stress Test which simulates a price change +30% and down -25%)² | Yes | Yes |

| Singleton Margin Method for HK Real Estate Stocks (Stress test +/-50%)² | Yes | Yes |

1 Dynamic House Scanning Charges are available only on select exchanges (Asian Exchanges and MEXDER)

2 IBKR will calculate the potential loss for each stock and its derivates by subjecting them to a stress test. The requirement for the stock (and its derivatives) which projects the greatest loss in the above scenario will be compared to what would otherwise be the aggregate portfolio margin requirement, and the greater of the two will be the margin requirement for the portfolio

風險漫遊:替代保證金計算器

Overview:

概述:

隨著市場條件的變化,IB 會經常評估保證金水平並根據需要在法定最低保證金要求的基礎

上提高保證金要求。為幫助客戶瞭解此類保證金變動對其投資組合的影響,我們在“風險漫

遊”應用中提供了一個被稱為“替代保證金計算器”的功能。下文列出了創建“假設情境”

投資組合的步驟,用以評估保證金調整帶來的影響。

第一步:打開全新的“假設情境”投資組合

在標準模式TWS交易平臺內,依次選擇“分析工具(Analytical Tools)”、“風險漫遊(Risk

Navigator)”和“打開新的假設情境(Open New What-If)”菜單選項(見圖1)。

圖1

.png)

在魔方模式TWS 交易平臺下,依次選擇“新窗口(New Window)”、“風險漫遊(Risk Navigator)”和“打開新的假設情境(Open New What-If)”菜單選項。

第二步:定義起始投資組合

跳出的彈出窗口(圖2)會詢問您是想用您當前的投資組合來創建假設投資組合還是重新創

建一個投資組合。點擊“是”將把已有的頭寸下載至新的“假設情境”投資組合。

圖2

點擊“否”將打開一個沒有頭寸的“假設情境”投資組合。

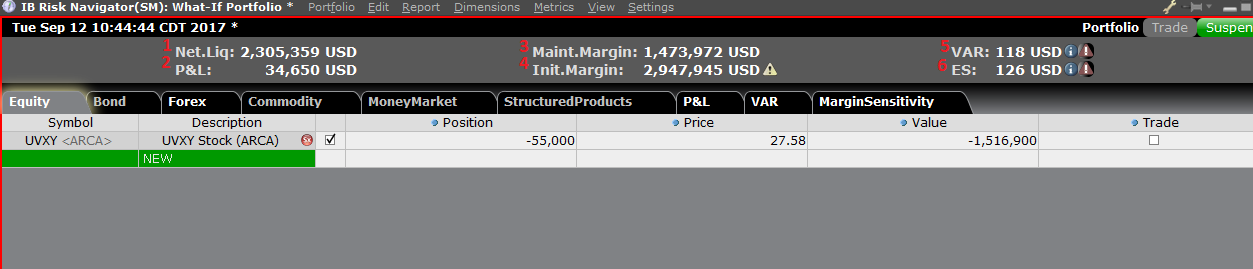

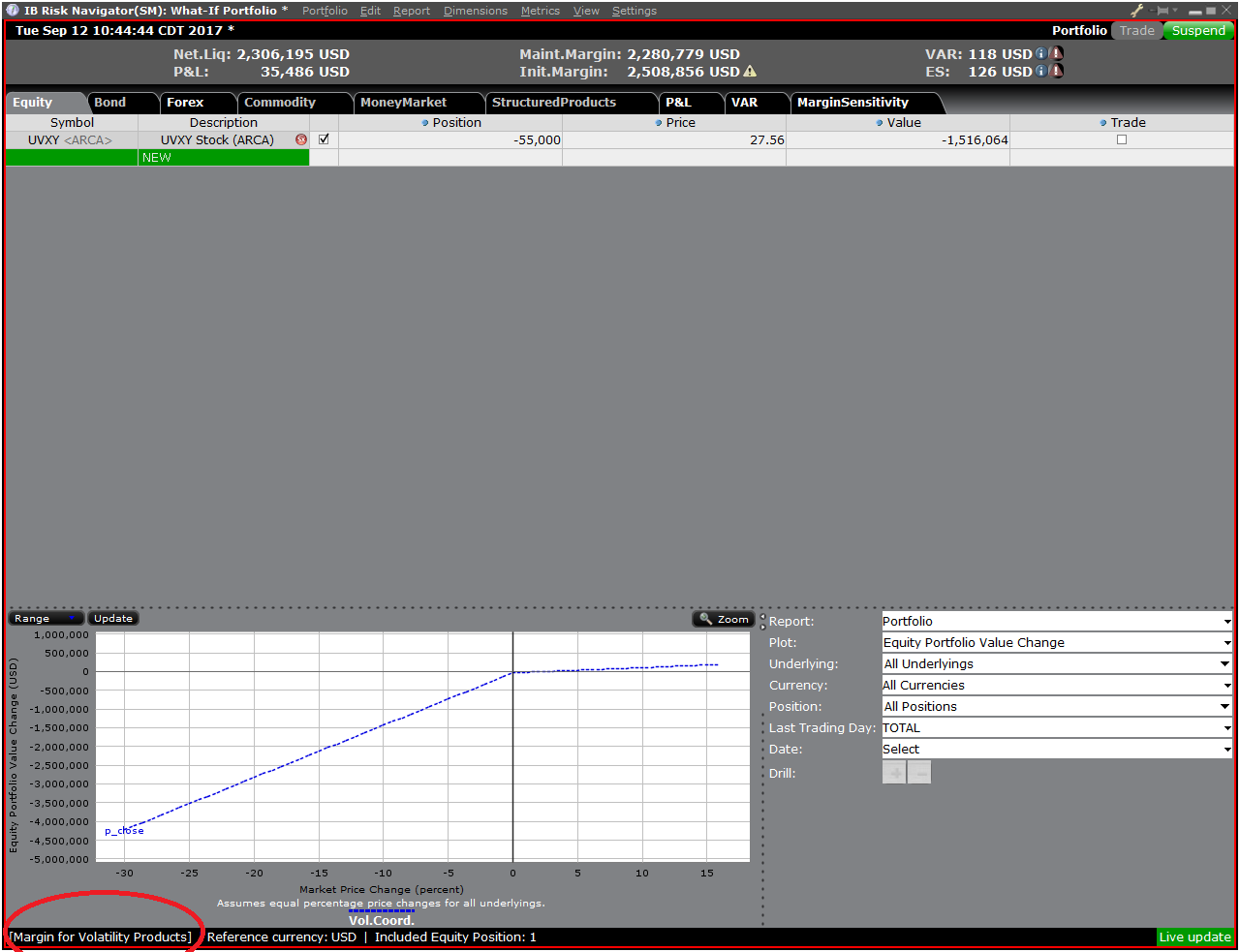

風險控制面板

“風險控制面板”位於產品標簽組的頂部,“假設情境”投資組合和真實活躍的投資組合均

可使用。“假設情境”投資組合可按需計算各類數值。用戶可通過該控制面板一目了然地查

看以下賬戶信息:

1) 淨清算價值:賬戶的總淨清算價值

2) 盈虧:整個投資組合的每日總盈虧

3) 維持保證金:當前總的維持保證金

4) 初始保證金:總的初始保證金要求

5) 風險價值(VAR):整個投資組合的風險價值

6) 預期虧損(ES):預期虧損(平均風險價值)是投資組合在最差的情境下的預期回報

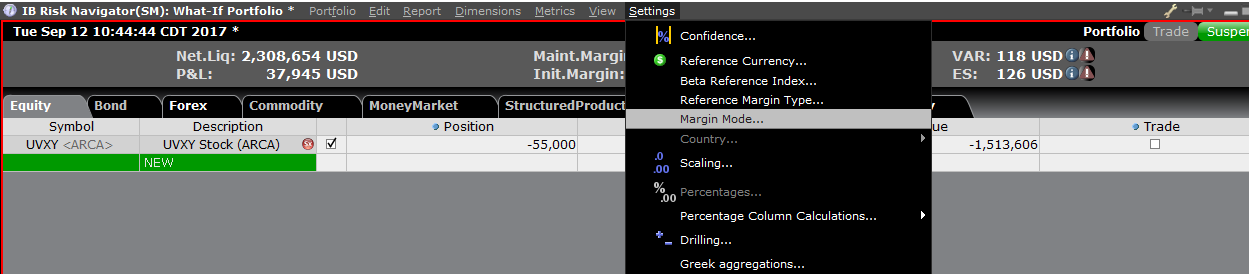

替代保證金計算器

在“設置(Setting)”菜單下點擊“保證金模式(Margin Mode)”(圖3)可打開替代保

證金計算器。該工具會顯示當保證金調整被完全實施後投資組合的保證金要求會發生什麼變

化。

圖3

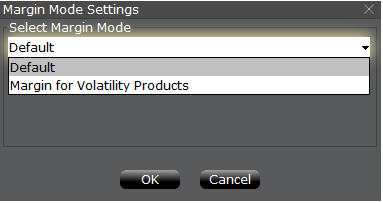

第三步:選擇保證金模式設置

出現一個名為“保證金模式設置”的彈出窗口(圖4)。您可使用該窗口中的下拉菜單將保

證金計算方式從“默認”(即當前政策)變更為新標題的保證金設置(即新的保證金政策)。

選擇完畢後點擊窗口中的“確定”按鈕。

圖4

設置好新的保證金模式後,風險漫遊控制面板會自動更新以反映您的選擇。您可在新舊保證

金模式設置中切換。注意,當前的保證金模式會在“風險漫遊”窗口的左下角顯示(圖5)。

圖5

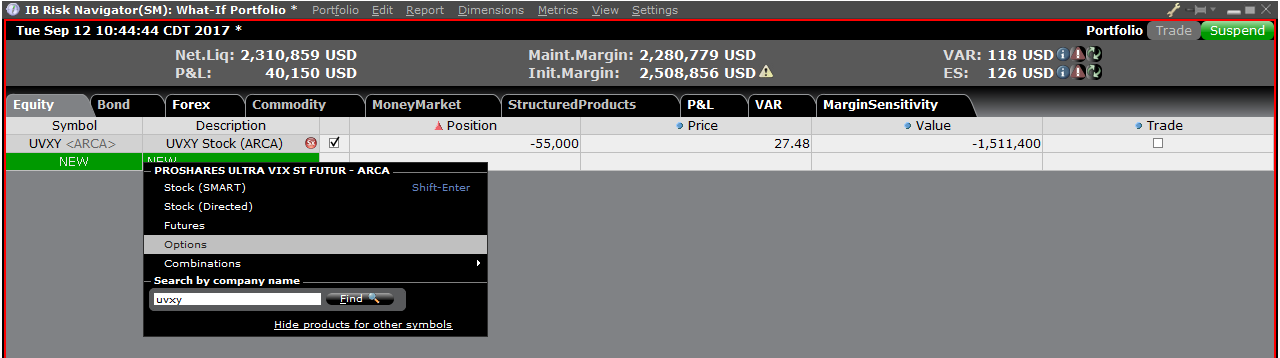

第四步:添加頭寸

要在“假設情境”投資組合中添加頭寸,點擊標題叫“新”的綠色行,然後依次輸入底層產

品的代碼(圖6)、選擇產品類型(圖7)及輸入頭寸數量(圖8)

圖6

圖7

圖8

您可修改頭寸以查看保證金會發生什麼變化。在您修改了頭寸後,您需要點擊保證金數字右

邊重新計算的圖標 (![]() ) 以更新數值。只要出現了該圖標就表明保證金數據沒有根據“假

) 以更新數值。只要出現了該圖標就表明保證金數據沒有根據“假

設情境”投資組合的內容更新至最新。

2020 年美國大選保證金增加

考慮到即將發生的美國總統選舉帶來的潛在市場波動,盈透證券將針對所有在美國交易的股

指期貨、衍生品及在大阪證券交易所(OSE.JPN)上市的道瓊斯期貨提高保證金要求。

客戶如持有美國股指期貨及其衍生品及/或在大阪證券交易所上市的道瓊斯期貨頭寸,請知

悉,保證金要求預計將在正常水準上提高35%左右。保證金要求將在20 個自然日內逐步提

高,其中維持保證金將從2020年10月5日起提高,直至2020年10月30日。

下表列舉了一些常見產品預計發生的保證金變動

| 期貨代碼 | 描述 | 上市交易所 | 交易類型 | 當前比例(價 格掃描範圍) * |

預計比例(價 格掃描範圍) |

| ES | E-mini S&P500 | GLOBEX | ES | 7.13 | 9.63 |

| YM | Mini DJIA | ECBOT | YM | 6.14 | 8.29 |

| RTY | Russel 200 | GLOBEX | RTY | 6.79 | 9.17 |

| NQ | NASDAQ E-mini | GLOBEX | NQ | 6.57 | 8.87 |

| DJIA | OSE 道瓊斯 工業平均 |

OSE.JPN | DJIA | 5.14 | 6.94 |

*截至2020年10月2日開市。

注:IBKR 的風險漫遊工具能幫助您評估最新的維持保證金要求對您現有的投資組合或您想

構建或測試的其它投資組合有何影響。有關“替代保證金計算器”的更多信息,請見知識庫

文章2957:風險漫遊:替代保證金計算器,並在風險漫遊的保證金模式設置下選擇“美國

大選保證金”。

U.S. 2020 Election Margin Increase

In light of the potential market volatility associated with the upcoming United States presidential election, Interactive Brokers will implement an increase in the margin requirement for all U.S. traded equity index futures and derivatives and Dow Jones Futures listed on the OSE.JPN exchange.

Clients holding a position in a U.S. equity index future and their derivatives and/or Down Jones Futures listed on the OSE.JPN exchange should expect the margin requirement to increase by approximately 35% above the normal margin requirement. The increase is scheduled to be implemented gradually over a 20-calendar day period with the maintenance margin increase starting on October 5, 2020 through October 30, 2020.

The table below provides examples of the margin increases projected for some of the more widely held products

| Future Symbol |

Description | Listing Exchange | Trading Class | Current Rate (Price scan range)* | Projected Rate (Price scan range) |

| ES | E-mini S&P 500 | CME | ES | 7.13 | 9.63 |

| YM | MINI DJIA | CBOT | YM | 6.14 | 8.29 |

| RTY | Russell 2000 | CME | RTY | 6.79 | 9.17 |

| NQ | NASDAQ E-MINI | CME | NQ | 6.57 | 8.87 |

| DJIA | OSE Dow Jones Industrial Average | OSE.JPN | DJIA | 5.14 | 6.94 |

*As of 10/2/20 open.

NOTE: IBKR's Risk Navigator can help you determine the impact the new maintenance margin requirements will have on your current portfolio or any other portfolio you would like to construct or test. For more information about the Alternative Margin Calculator feature, please see KB Article 2957: Risk Navigator: Alternative Margin Calculator and from the margin mode setting in Risk Navigator, select " US Election Margin".

Overview of Central Bank of Ireland CFD Rules Implementation for Retail Clients at IBIE

Overview:

|

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 61% of retail investor accounts lose money when trading CFDs with IBKR. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. |

The Central Bank of Ireland (CBI) enacted new rules applicable to retail clients trading CFDs, effective 1st August 2019. Professional clients are unaffected.

The rules consist of: 1) leverage limits; 2) a margin close out rule on a per account basis; 3) negative balance protection on a per account basis; 4) a restriction on the incentives offered to trade CFDs; and 5) a standardized risk warning.

Most clients (excepting regulated entities) are initially categorised as Retail Clients. IBKR may in certain circumstances agree to reclassify a Retail Client as a Professional Client, or a Professional Client as a Retail Client. Please see MiFID Categorisation for further detail.

The following sections detail how IBKR has implemented the CBI Decision.

1 Leverage Limits

1.1 Margins

Leverage limits were set by CBI at different levels depending on the underlying:

- 3.33% for major currency pairs; Major currency pairs are any combination of USD; CAD; EUR; GBP; CHF; JPY

- 5% for:

- Non-major currency pairs are any combination that includes a currency not listed above, e.g., USD.CNH

- Major indices are IBUS500; IBUS30; IBUST100; IBGB100; IBDE40; IBEU50; IBFR40; IBJP225; IBAU200

- Gold

- 10% for non-major equity indices; IBES35; IBCH20; IBNL25; IBHK50

- 20% for individual equities

1.2 Applied Margins - Standard Requirement

In addition to the CBI Margins, IBKR establishes its own margin requirements (IB Margins) based on the historical volatility of the underlying, and other factors. We will apply the IB Margins if they are higher than those prescribed by CBI .

Details of applicable IB and CBI margins can be found here.

1.2.1 Applied Margins - Concentration Minimum

A concentration charge is applied if your portfolio consists of a small number of CFD and/or Stock positions, or if the three largest positions have a dominant weight. We stress the portfolio by applying a 30% adverse move on the three largest positions and a 5% adverse move on the remaining positions. The total loss is applied as the maintenance margin requirement if it is greater than the standard requirement for the combined Stock and CFD positions. Note that the concentration charge is the only instance where CFD and Stock positions are margined together.

1.3 Funding of Initial Margin Requirements

You can only use cash to post initial margin to open a CFD position.

Initially all cash used to fund the account is available for CFD trading. Any initial margin requirements for other instruments and cash used to purchase cash stock reduce the available cash. If your cash stock purchases have created a margin loan, no funds are available for CFD trades even if your account has significant equity. We cannot increase a margin loan to fund CFD margin under the CBI rules.

Realized CFD profits are included in cash and are available immediately; the cash does not have to settle first. Unrealized profits however cannot be used to meet initial margin requirements.

2 Margin Close Out Rule

2.1 Maintenance Margin Calculations & Liquidations

The CBI requires IBKR to liquidate CFD positions latest when qualifying equity falls below 50% of the initial margin posted to open the positions. IBKR may close out positions sooner if our risk view is more conservative. Qualifying equity for this purpose includes CFD cash and unrealized CFD P&L (positive and negative). Note that CFD cash excludes cash supporting margin requirements for other instruments.

The basis for the calculation is the initial margin posted at the time of opening a CFD position. In other words, and unlike margin calculations applicable to non-CFD positions, the initial margin amount does not change when the value of the open position changes.

2.1.1 Example

You have EUR 2000 cash in your account and no open positions. You want to buy 100 CFDs of XYZ at a limit price of EUR 100. You are first filled 50 CFDs and then the remaining 50. Your available cash reduces as your trades are filled:

|

|

Cash |

Equity* |

Position |

Price |

Value |

Unrealized P&L |

IM |

MM |

Available Cash |

MM Violation |

|

Pre Trade |

2000 |

2000 |

|

|

|

|

|

|

2000 |

|

|

Post Trade 1 |

2000 |

2000 |

50 |

100 |

5000 |

0 |

1000 |

500 |

1000 |

No |

|

Post Trade 2 |

2000 |

2000 |

100 |

100 |

10000 |

0 |

2000 |

1000 |

0 |

No |

*Equity equals Cash plus Unrealized P&L

The price increases to 110. Your equity is now 3000, but you cannot open additional positions because your available cash is still 0, and under the CBI rules IM and MM remain unchanged:

|

|

Cash |

Equity |

Position |

Price |

Value |

Unrealized P&L |

IM |

MM |

Available Cash |

MM Violation |

|

Change |

2000 |

3000 |

100 |

110 |

11000 |

1000 |

2000 |

1000 |

0 |

No |

The price then drops to 95. Your equity declines to 1500 but there is no margin violation since it is still greater than the 1000 requirement:

|

|

Cash |

Equity |

Position |

Price |

Value |

Unrealized P&L |

IM |

MM |

Available Cash |

MM Violation |

|

Change |

2000 |

1500 |

100 |

95 |

9500 |

(500) |

2000 |

1000 |

0 |

No |

The price falls further to 85, causing a margin violation and triggering a liquidation:

|

|

Cash |

Equity |

Position |

Price |

Value |

Unrealized P&L |

IM |

MM |

Available Cash |

MM Violation |

|

Change |

2000 |

500 |

100 |

85 |

8500 |

(1500) |

2000 |

1000 |

0 |

Yes |

3 Negative Equity Protection

The CBI Decision limits your CFD-related liability to the funds dedicated to CFD-trading. Other financial instruments (e.g., shares or futures) cannot be liquidated to satisfy a CFD margin-deficit.*

Therefore, non-CFD assets are not part of your capital at risk for CFD trading.

Should you lose more than the cash dedicated to CFD trading, IB must write off the loss.

As Negative Equity Protection represents additional risk to IBKR, we will charge retail investors an additional financing spread of 1% for CFD positions held overnight. You can find detailed CFD financing rates here.

*Although we cannot liquidate non-CFD positions to cover a CFD deficit, we can liquidate CFD positions to cover a non-CFD deficit.

IB LLC大宗商品賬戶保證金要求

引言

作為一家在19個國家或地區提供期貨交易的全球性經紀商,IB受多種監管要求的約束,某些監管要求仍保留了在日末計算一次保證金的概念,而IB的保證金是連續、實時計算的。為滿足大宗商品監管要求并以務實的方式控制經濟風險,我們會在收槃時應用兩種保證金計算方式,兩種方式計算得出的保證金要求須同時滿足。兩種方式的概述如下。

概述

所有定單在執行前均須滿足初始保證金要求,執行后則須始終滿足維持保證金要求。由於某些產品的日中保證金可能會低於交易所要求的最低保證金比例,為確保日末能滿足保證金要求,IB通常會在休市前清算頭寸,而不是要求客戶追加保證金。然而,如果賬戶在休市時仍不滿足保證金要求,我們會通知客戶追加保證金,同時僅允許客戶做減少占用保證金的交易,如在之后的第三個工作日休時仍不能滿足最初的要求,則頭寸將被清算。

在確定是否需追加保證金時,IB會應用實時計算和監管計算這兩種方式,而某些情況下,這兩種方法得出的結果可能不同:

實時:在本方法下,初始保證金是用同一個時間點收集的頭寸和價格計算的,不考慮產品所在的交易所及正式的休市時間;鑒於大部分交易所的交易時間均接近連續,我們認為本方法有其適用性。

監管:在本方法下,初始保證金是用各家交易所常規交易時間終止時收集的頭寸和價格計算的。比如,對於交易香港交易所、EUREX和CME期貨產品的客戶,保證金要求將根據各家交易所休市時的信息計算。

影響

交易單一時段、單一國家或地區的期貨的客戶不受影響。在某個交易所的常規交易時段及槃后交易時段交易、或在不同國家或地區的交易所(這些交易所的休市時間不同)交易的客戶更可能受影響。比如,一個客戶在香港常規交易時段開倉期貨合約并在美國交易時段平倉,則保證金要求只取決於開倉時的頭寸。在新的計算方式下,這種交易將適用不同的保證金要求,甚至產生在當前方法下不存在的追加保證金。下表舉例說明了該情況。

舉例

本例試圖說明,如果一個同時在亞洲和美國兩個時區交易期貨的客戶在延長的交易時段(即在常規交易時段以外、該日已正式休市時)交易時會如何受影響。本例中,客戶在香港常規交易時段開倉,并在延長的交易時段內平倉,進而騰出資金在美國常規交易時段開倉。為說明起見,假設交易損失了1,000美元。本例說明,監管的日末保證金計算方法可能不能識別在正式休市后進行的會占用保證金的交易,因此產生了追加初始保證金的要求。

| 天數 | 時間(美東) | 事件 |

初始頭寸 |

結束頭寸 | IB保證金 | 監管保證金 | |||

| 含貸款的淨資產 | 維持 | 初始 | 隔夜 | 追加保證金 | |||||

| 1 | 22:00 | 買1份 HHI.HK | 無 | 1份HHI.HK多頭 | $10,000 | $3,594 | $4,493 | 不適用 | 不適用 |

| 2 | 04:30 | 香港交易所正式休市 | 1份HHI.HK多頭 | 1份HHI.HK多頭 | $10,000 | $7,942 | $9,927 | $4,493 | 不適用 |

| 2 | 08:00 | 賣1份HHI.HK | 1份HHI.HK多頭 | 無 | $9,000 | $0 | $0 | $0 | 不適用 |

| 2 | 10:00 | 買1份ES | 無 | 1份ES多頭 | $9,000 | $2,942 | $3,677 | 不適用 | 不適用 |

| 2 | 17:00 | 美國交易所正式休市 | 1份ES多頭 | 1份ES多頭 | $9,000 | $5,884 | $7,355 | $9,993 | 是 |

| 3 | 17:00 | 美國交易所正式休市 | 1份ES多頭 | 1份ES多頭 | $9,000 | $5,884 | $7,355 | $5,500 | 否 |

Margin Considerations for Intramarket Futures Spreads

Background

Clients who simultaneously hold both long and short positions of a given futures contract having different delivery months are often provided a spread margin rate that is less than the margin requirement for each position if considered separately. However, as the settlement prices of each contract may deviate significantly as the front month contract approaches its close out date, IBKR will reduce the benefit of the spread margin rate to reflect the risk of this price deviation.

Spread Margin Adjustment

This reduction is accomplished by effectively decoupling or breaking the spread in phases on each of the 3 business days preceding the close out date of the front contract month, as follows:

- On the 3rd business day prior to close out, the initial and maintenance margin requirements will be equal to 10% of their respective requirements on each contract month as if there was no spread, plus 90% of the spread requirement;

- On the 2nd business day prior to close out, the initial and maintenance margin requirements will be equal to 20% of their respective requirements on each contract month as if there was no spread, plus 80% of the spread requirement;

- On the business day prior to close out, the initial and maintenance margin requirements will be equal to 30% of their respective requirements on each contract month as if there was no spread, plus 70% of the spread requirement.

Working Example

Assume a hypothetical futures contract XYZ with the margin requirements as outlined in the table below:

| XYZ | Front Month - 1 Short Contract (Uncovered) | Back Month - 1 Long Contract (Uncovered) | Spread - 1 Short Front Month vs. 1 Long Back Month |

| Initial Margin | $1,250 | $1,500 | $500 |

| Maintenance Margin | $1,000 | $1,200 | $400 |

Further assume a position consisting of 1 short front month contract and 1 long back month contract with the front month contract close out date = T. using this hypothetical example, the initial margin requirement over the 3 business day period preceding close out date is outlined in the table below:

| Day | Initial Margin Requirement | Calculation Details |

| T-4 | $500 | Unadjusted |

| T-3 | $725 | .1($1,250 + $1,500) + .9($500) |

| T-2 | $950 | .2($1,250 + $1,500) + .8($500) |

| T-1 | $1,175 | .3($1,250 + $1,500) + .7($500) |

| T | $1,175 | Positions not in compliance with close out requirements are subject to liquidation. |

Concentrated Positions in Low Cap Stocks

The margin requirement for accounts holding concentrated positions in low cap stocks is as follows:

- An alternative stress test will be considered following the margin calculation currently in place. Here, each stock and its derivatives will be subject to a stress test which simulates a price change reflective of a $500 million decrease in capitalization (e.g., 25% in the case of a stock with a market capitalization of $2 billion; 30% for a stock with a market capitalization of $1.5 billion; etc.). Stocks with a market capitalization of $500 million or below will be subject to a stress test as if the price has fallen to $0.

- For the stock which projects the greatest loss assuming a $500 million decrease in capitalization, that loss will be compared to the initial margin as determined under the preceding calculation for the aggregate portfolio and, if greater, will become the initial margin requirement.

- If the initial margin requirement is increased, the maintenance margin for that same stock and its derivatives will increase to approximately 90% of the initial requirement for the aggregate portfolio.