Request for Payment (RFP)

What is Request for Payment?

Request for payment is a message that you could send via IBKR and its supporting bank to your bank to trigger a real-time credit transfer directly to your IBKR account. Your bank will prompt you via push notification or e-mail to review and approve the payment request. Upon receiving your approval, your bank will send a real-time credit transfer directly to IBKR's bank and IBKR will credit your account. Real-time payments are done on a new 24x7x365 payments platform managed by The Clearing House and available to all federally insured U.S. depository institutions.

Who is eligible to use Request For Payment?

Real-time payment eligibility depends on your bank's capability to accept the request. U.S. depository institutions are actively preparing to accept RFPs and most are expected to be able to accept requests in the coming months.

What is the transaction amount limit?

The request for payment limit is determined by your bank. Initially limits are expected to be modest (approximately $5,000 to $10,000), but are expected to increase in the future. The RTP network's current credit transfer limit is $1,000,000

How long does it take for the funds to be credited to my account?

Under normal circumstances you should receive the prompt to approve the request for payment and, upon approval, the funds would be credited to your account and available to trade within a few minutes or faster.

How to deposit HUF to Interactive Brokers

What are Giro/RTGS (Viber) transfers and International Bank Transfers (SWIFT) for HUF?

There are two different transfer methods available for transferring HUF depending of the location of your bank.

GIRO/ RTGS VIBER (domestic) transfers are available at banks located in Hungary for bank-to-bank transfers while banks located outside of Hungary will likely offer International Bank Transfers (SWIFT).

Giro /RTGS (Viber) payments

The Hungarian Internal Clearing System (ICS) operated by GIRO Zrt. is a payment system for the interbank clearing of domestic HUF transfers and direct debits. It is a "Real Time Gross Settlement" system called VIBER.

Banks that are connected to it will allow you to transfer HUF quickly and inexpensively between banks located in Hungary. It will be required to know the Bank Code, Branch Code and Account number of the receiving party.

You do not necessarily have to select GIRO or RTGS (VIBER) in your online banking. Your bank may call it "Bank-To-Bank transfer" or "domestic payment method" using the details mentioned above.

SWIFT payment

The Society for Worldwide Interbank Financial Telecommunication - SWIFT - is a network that allows banks to communicate financial information securely.

SWIFT payments are offered by most banks for international money transfers, and involve a series of banks which work together to make sure your money arrives at your account.

If you transfer HUF from a financial institution outside of Hungary, the payment would likely be routed via a correspondent bank located in Hungary before reaching your account. Such payments are known as cross-border payments and often take more time to complete because of the complexity associated with involving multiple banks.

Bank transfers can take time to complete, particularly when it comes to cross-border payments, because of the complexity associated with involving multiple bank in the payment chain.

Processing bank transfers involves a number of steps, particularly for cross-border payments. These are sent via the correspondent banking network and typically pass between several different banks along the way. After being initiated, a wire transfer is sent by the debtor agent to an intermediary bank before moving on to the creditor agent. Once these steps are complete, the recipient will receive their funds.

There are a number of reasons why cross-border payments may be delayed or held up. First, not all account balances can be updated outside of the operating hours of local settlement systems. Delays can also arise if compliance checks need to be carried out, especially when a payment passes through different countries and jurisdictions.

Difference between domestic and international bank transfers

Banks make a domestic transfer to send funds to financial institutions residing in the same country or financial zone. When sending funds to financial institutions in a foreign country or financial zone, banks have to make an international bank transfer. The differences between these two bank transfers affect the number of fees banks charge and the duration it takes to complete the transfer.

How long does it usually take for my funds to arrive?

|

Payment Type |

Timing |

Approximate Cost* |

|

Giro payment |

same day up to 1 business day |

free of cost or very low cost |

|

International bank transfer (SWIFT) |

from 1 to 4 business days |

vary by bank |

*Please consult with the sending institution about the costs to process your payment as this may vary by financial institution. IBKR does not charge fees for the deposit of funds.

IBKR credits funds real-time upon receipt. Please note that we do not have influence on the speed of transfer. Please consult with your bank regarding their processing times.

Payments that are subject to additional review may take longer to credit.

現金劃轉

背景

IB全能賬戶由兩個獨立的子賬戶或賬戶段組成,一個用于持有證券倉位和餘額,受美國證券交易委員會(SEC)客戶保護規則約束,另一個用于持有商品倉位和餘額,受美國商品期貨交易委員會(CFTC)客戶保護規則約束。這種全能賬戶的設計旨在盡可能地降低客戶維護兩個不同賬戶(例如,賬戶之間轉帳現金、兩個賬戶登錄和提交委托單、多份報表等)可能面臨的行政管理開銷,同時又維持法規要求的分隔措施。

該等法規還要求所有證券交易和相關保證金交易均在全能賬戶的證券賬戶段進行,而商品交易則在商品賬戶段進行。1 雖然法規允許將全額支付的證券持倉以保證金抵押品的形成存放在商品賬戶段進行托管,但IB幷不允許這種操作,從而對抵押權應用了更爲嚴格的SEC限制性規則。鑒于相關法規和政策已對持倉應歸于哪個賬戶段作出了規定,現金是唯一可由客戶自行决定在兩個賬戶段之間來回轉帳的資産。

下方爲現金劃轉選項、選擇步驟和注意事項相關的說明。

現金劃轉選項

客戶有三種劃轉選項,說明如下:

1. 不劃轉剩餘資金 – 根據這個選項,如非必要,剩餘現金不會在兩者之間進行轉移:

a. 解决/緩解另一賬戶段保證金不足的問題;

b. 盡可能地降低指定賬戶段的借方現金餘額,從而减少相關的利息費用。 請注意,對于只擁有證券或商品交易許可中一項許可的賬戶持有人來說,這是默認選項,也是唯一的選項。

2. 將剩餘資金劃轉至我的IB證券賬戶 – 只在商品賬戶段中留下能滿足當前商品保證金要求的現金餘額。 任何由于現金增加(例如,有利的變化和/或與交易相關)或保證金要求降低(例如,SPAN風險陣列和/或與交易相關的變化)而産生的超出保證金要求的現金,都將自動從商品賬戶段轉移到證券賬戶段。請注意,賬戶持有人必須具備證券交易許可才能選擇此選項。

3. 將剩餘資金劃轉至我的IB商品賬戶 – 只在證券賬戶段中留下能滿足當前證券保證金要求的現金餘額(加上含有貸款價值的其它證券倉位)。請注意,賬戶持有人必須具備商品交易許可才能選擇此選項。

其它注意事項:

- 由于全能賬戶允許以不同幣種持有現金餘額,因此存在一個層次結構,以决定當多種貨幣出現多頭餘額時,首先轉移哪種貨幣。在這類情况下,首先會轉移以基礎貨幣計價的餘額,然後是美元,然後剩下的多頭餘額再按金額從高到低的順序轉移。

- 爲了盡可能地降低一個賬戶段在把剩餘現金劃轉至另一個賬戶段後出現保證金不足的可能性,剩餘資金不會全部轉移,而是會留下相當于維持保證金要求5%的資金作爲緩衝。 同樣,爲了盡可能地降低轉移名義餘額的運營開銷,只有在扣除5%的保證金緩衝後,剩餘金額(如有)仍不低于賬戶淨資産的1%或200美元時,才會轉移餘額。

- 在執行交易前信用核查以確定賬戶是否擁有足够的淨資産來支持新的委托單時,一個賬戶段內進行的交易也會將另一個賬戶段內的剩餘現金納入考慮(但在交易執行之前不會進行劃轉,幷且也只有在爲了滿足保證金要求而有必要時才會進行劃轉)。 被標記爲典型日內交易者以及需要進行交易前信用核查(會考慮前一日和當日淨資産)的賬戶應特別留意下方選擇注意事項。

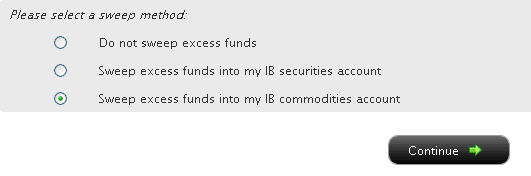

選擇劃轉的選項

如果您的賬戶管理版本在左側有一系列菜單選項,請選擇賬戶行政,然後選擇 剩餘資金劃轉菜單選項。 如果您的版本是頂部有菜單選項,請選擇管理賬戶/設置,然後選擇 配置賬戶/剩餘資金劃轉菜單選項。無論您的版本如何,您都將看到以下界面:

然後,您可點擊您想要的劃轉方式對應的單選按鈕,然後選擇〝繼續〞按鈕。您的選擇將從下一個工作日起生效,幷將一直有效,直到選擇其它選項爲止。請注意,只要滿足上文中提到的交易許可設置,您可隨時更改劃轉方式,沒有次數限制。

選擇注意事項

雖然選擇將剩餘現金存放在哪個賬戶段可能涉及每位客戶獨特的主觀决策和偏好(例如,客戶將大部份資産集中存放在其中一個賬戶段),但下述有幾個因素值得注意:

1. 典型日內交易淨資産 - 根據相關法規被標記爲典型日內交易者的賬戶(即在5個工作日內進行4次或以上日內交易),其證券購買力將被限制爲證券賬戶段當日或前一日收盤淨資産中的較低者。根據這個計算方式,如選擇將剩餘資金劃轉至商品賬戶段,則該筆資金將無法納入計算,從而可能對下達新委托單的造成一定限制。要最大程度地利用淨資産來擴大購買力下達證券委托單,客戶需選擇將剩餘資金劃轉至證券賬戶段。 請注意,選擇證券賬戶段幷不會限制下達商品委托單的能力,因爲典型日內交易規則不適用于此類賬戶。

2. 保險 – 美國證券投資者保護公司(SIPC)的保障範圍覆蓋證券賬戶段的資産,而商品賬戶段則沒有相應的保障計劃。不過,超過SIPC的$250,000現金分項給付限額(勞合社現金分項給付限額爲$900,000,如適用)的餘額不在承保範圍內。 IB加拿大和IB英國的客戶也分別受加拿大投資者保護基金(CIPF)和英國金融服務補償計劃(FSCS)規定的承保規則約束。

3.利息收入 – 在所有其它條件相同的情况下,從未將多頭現金餘額在證券和商品賬戶段中分開存放的客戶,可望獲得最高的利息收入,這是因爲兩者不會匯總以計算貸方利息(它們受不同的隔離池和再投資規則的約束)。 在選擇現金劃轉時,除了上述的因素外,也應該要考慮到貸款需要維持最低現金餘額,幷且餘額高一些,利率也會優惠一些。2

脚注:

1由于OneChicago個股期貨是由SEC和CFTC共同監管的混合産品,因此可在任何一種賬戶類型中進行買賣。不過,IB選擇在全能賬戶的證券賬戶段進行此類交易,因爲只有在這情况下,才能向單一股票期貨和任何合資格股票或期權持倉提供保證金减免。

2例如,某賬戶在證券和商品賬戶段各持有$9,000的多頭美元餘額。根據基準聯邦基金有效利率,如果兩個餘額存放在同一賬戶段,該賬戶有$8,000 ($18,000 - $10,000)可以獲得利息。但由于分別放在兩個賬戶段中的現金餘額均低于$10,000,都無法獲得利息,如不選擇現金劃轉,將無法賺取任何利息。同樣,如進行現金劃轉後,某賬戶段的多頭美元現金餘額超過$100,000,則賬戶持有人將能够賺取更高一檔的利息。有關利息計算的其它信息,包括當前基準利率的鏈接,請參閱KB39。

“信用限制期”內的存款是否可以獲得利息?

Overview:

答案取决于存款方式。 對于通過ACH進行的存款,利息從存款到達當日起便開始計算,資金記入賬戶前爲期四個工作日的信用限制期都會持續計息。對于銀行支票以外的支票存款,在信用限制期內不産生利息。銀行支票和電匯會在收到後立即記入賬戶,因此不受任何信用限制期的影響。

您收到的利息因市况而异。 有關當前向貸方餘額支付利息的信息,請參閱 www.interactivebrokers.com/interest

How to Deposit JPY to Interactive Brokers

Account holders depositing from a local Japanese bank should send funds via domestic fund transfer.

Please see below for more information regarding how to deposit funds into an IBSJ account.

Instructions for how to deposit JPY into your IBSJ account

A deposit notification will be required. It is recommended that you always enter a deposit notification before arranging a fund transfer with your bank.

Account holders can notify IBKR of an incoming fund transfer by entering a deposit notification in Client Portal by selecting Transfer & Pay followed by Transfer Funds and Make a Deposit.

Local bank transfers should use 'Domestic Bank Transfer.' Overseas accounts able to send JPY should use 'International Transfer.'

Banking instructions will be provided after submitting a deposit information. It is recommended that you always confirm that the banking instructions registered with your bank match those which are provided when creating a deposit notification.

Contact your bank and confirm how to complete a fund transfer using the provided bank instructions.

IMPORTANT: A deposit notification instructs your intent to send funds to your IBSJ account. Notifications DO NOT move any funds. Please arrange with your bank to send funds to your IBSJ account.

What methods can I use to fund my IBSJ account with JPY?

Local - Clients sending funds from a local Japanese domestic bank should send funds via domestic fund transfer.

International - Deposits from overseas bank accounts must use the 'International Transfer' method to send JPY to their IBSJ account. Confirm procedures with your sending institution on how to send an international wire using the provided banking instructions.

For both methods, account holders should confirm fees and procedures with their bank before sending funds. IBSJ is not responsible for fees charged by your bank.

What information does my bank need to transfer funds?

Local - Local Japanese banks will need the IBSJ bank, bank code/branch code, bank account title & address, and 7-digit destination bank account number/VAN*.

*A VAN (Virtual Account Number) is a bank account number assigned specifically to you for domestic fund transfers. It should be used exclusively for deposits initiated by yourself and should not be shared with anyone else. A VAN will not be used for international fund transfers

International - International transfers require IBSJ's bank information, SWIFT code, bank account title & address, and 10-digit bank account number. Be sure to include your name and U-account number in the memo/reference field of the transfer details. Failure to include this information may delay the arrival of funds to your account.

Contact Client Services should additional information or assistance be required.

What information does IBKR need to transfer funds?

Please create a deposit notification as instructed above.

If funds are sent without a deposit notification, proof of deposit may be requested to credit the funds to your account.

How long does it take for my funds to arrive into my IBSJ account?

Local - Your Japanese bank's daily cutoff times may affect the funds' arrival.

Should clients miss the daily deadline set by their bank, the funds should arrive the next business day. Please confirm this information with your Japanese bank.

International - The arrival of funds may take longer when sending JPY from an international bank via International Transfer (up to 3-4 business days in some cases).

Be sure to include your name and U-account number in the memo/reference field of the transfer details. Failure to include this information may delay the arrival of funds to your account.

Confirm that you have entered a matching deposit notification for your transfer. The arrival of funds may be delayed if funds are sent without a matching deposit notification.

| Payment Type | Timing | Approximate Cost | ||

| Domestic | Same day/following business day | Free to a few hundred Yen | ||

| International (SWIFT) | 1 to 4 business days | Varies by bank |

As costs vary by institution, please consult with the sending institution about the costs incurred to process your payment. IBKR does not charge fees for the deposit of funds.

IBKR credits funds to accounts in real-time upon receipt. Please note that we do not have any control over the speed/processing of your fund transfer. You may consider consulting your bank regarding processing times.

Payments that are subject to review may take longer to credit to the account.

Are third-party deposits into my IBSJ account permitted?

Funds must be sent from a bank account held in your name. Funds sent from an account using a different name will be considered third-party and will be rejected.

Does IBSJ charge for deposits?

IBSJ does not charge a handling fee for deposits.

Related fees (including, but not limited to: transfer fees, rejection fees, etc.) are to be paid by the account holder. IBSJ is not responsible for fees incurred due to rejected deposits.

Can I use a fund transfer service such as Wise or Revolut?

Fund transfer services, including Wise and Revolut, cannot be used for funding your IBSJ account. Please use a bank wire to send funds to an IBSJ account.

How to Deposit SGD to Interactive Brokers

How do I deposit SGD to Interactive Brokers?

IBKR's bank account for SGD is held in Singapore and is eligible to receive SGD transfers via domestic bank transfer (e.g. FAST) or international bank transfer (SWIFT). If your bank account is held with a local Singapore bank they will usually process SGD transfers as a domestic local transfer while clients with bank accounts outside of Singapore will use an international bank transfer (SWIFT).

We will provide you the SGD bank routing information upon completing the deposit notification in Client Portal. IBKR will provide you our bank account title and bank account number which are usually required for domestic SGD transfers from an account held in Singapore. SWIFT code will be provided for international bank transfers from a bank account held outside of Singapore. A SWIFT code is generally not required for domestic SGD transfers.

Please include your brokerage account number in the template you setup with your bank.

How long will it take for my SGD transfer to arrive?

The timing for SGD deposits varies based on the payment network your bank uses to transfer the funds.

|

Payment Type |

Timing |

Approximate Cost* |

|

Local SGD Transfer |

1 business day |

free of cost or very low cost |

|

SWIFT |

from 1 to 4 business days |

vary by bank |

*Please consult with the sending institution about the costs to process your payment as this may vary by financial institution. IBKR does not charge fees for the deposit of SGD.

Note

- IBKR credits funds real-time upon receipt under normal circumstances.

- We do not have influence on the speed of transfer. You may consult with the sending institution regarding their processing times and cut off times. Transfers that are subject to additional review may take longer to credit.

Request for Payment (RFP)

What is Request for Payment?

Request for Payment (RFP) is a message that you could send via IBKR and its supporting bank to your bank to trigger a real-time credit transfer directly to your IBKR account. Your bank will prompt you via push notification or e-mail to review and approve the payment request. Upon receiving your approval, your bank will send a real-time credit transfer directly to IBKR's bank and IBKR will credit your account. Real-time payments are done on a new 24x7x365 payments platform managed by The Clearing House and available to all federally insured U.S. depository institutions.

Who is eligible to use Request For Payment?

Real-Time Payment (RTP) eligibility depends on your bank's capability to accept the request. U.S. depository institutions are actively preparing to accept RFPs and most are expected to be able to accept requests in the coming months.

What is the transaction amount limit?

The Request for Payment limit is determined by your bank. Initially limits are expected to be modest (approximately $5,000 to $10,000), but are expected to increase in the future. The RTP network's current credit transfer limit is $1,000,000.

How long does it take for the funds to be credited to my account?

Under normal circumstances you should receive the prompt to approve the Request for Payment and upon approval, the funds would be credited to your account and available to trade within a few minutes or faster.

How to Deposit NOK to Interactive Brokers

What are SWIFT and RTGS transfer methods for NOK?

IBKR is able to receive NOK transferred via international bank wire (SWIFT) or RTGS (Real Time Gross Settlement payments system) to deposit NOK to your account, no matter if your bank is located within or outside of Norway.

Typically your bank may call those transfers just regular wire transfers, electronic bank transfers or bank-to-bank transfers and may not distinct between international bank wire versus RTGS. You may want to consult with your bank for further information

about the transfer system they use to facilitate your payment.

SWIFT payment

The Society for Worldwide Interbank Financial Telecommunication - understandably shortened to SWIFT - is a network that allows banks to communicate financial information securely.

SWIFT payments are offered by most banks, for international money transfers, and involve a series of banks which work together to make sure your money arrives at your account.

If you transfer NOK from a financial institution outside of Norway, they may require to use a so called intermediary or correspondent bank to route the payment through, before reaching your account and they are called cross-border payments.

Bank transfers can take time to complete, particularly when it comes to cross-border payments. Clients are increasingly accustomed to a payments experience that feels instant. But making a payment to another country can be much more complex and time-consuming.

Processing bank transfers involves a number of steps – particularly for cross-border payments. These are sent via the correspondent banking network and typically pass between several different banks along the way. After being initiated, a wire transfer is sent by the debtor agent to an intermediary bank before moving on to the creditor agent. Once these steps are complete, the recipient will receive their funds.

There are a number of reasons why cross-border payments may be delayed or held up. Firstly, not all account balances can be updated outside the operating hours of local settlement systems. Delays can also arise if compliance checks need to be carried out, especially when a payment passes through different countries and jurisdictions.

RTGS payment

RTGS stands for Real Time Gross Settlement and is the fastest way to sent money from one bank account to another within the country. Banks charges fees for this real time settlement, that vary by bank.

RTGS method is mostly used for transaction of high value. Its a system where there is continuous and real-time settlement of fund-transfers. You may not be able to select this transfer method in your online banking screen.

It is rather a system your bank will use in the background to transfer your funds upon your request if the funds are transferred within the country. You may consult with your bank which payment system they use to transfer funds.

How long does it usually take for my funds to arrive?

|

Payment Type |

Timing |

Approximate Cost* |

| RTGS | Same day to 1 business days | Low cost, vary by bank |

|

International bank transfer (SWIFT) |

from 1 to 4 business days |

vary by bank |

*Please consult with the sending institution about the costs to process your payment as this may vary by financial institution. IBKR does not charge fees for the deposit of funds.

Note! IBKR credit funds real time upon receipt under normal circumstances. Please note that we do not have influence on the speed of transfer. You may consult with the sending institution regarding their processing times and cut off times. Payments that are subject to additional review may take longer to credit.

通過Wise進行注資

什麽是Wise?

Wise(前稱TransferWise)是一項國際綫上資金轉帳服務,支持80個國家的55種貨幣,主要提供跨境資金轉帳和外匯服務。Wise比跨境銀行轉帳費用更低,也較跨境銀行轉帳更快到帳,同時其提供的外匯匯率也頗具競爭力。

通過與Wise進行合作,IBKR能够在您登錄IBKR平臺期間,爲您提供以下的服務:

通過與Wise進行合作,IBKR能够在您登錄IBKR平臺期間,爲您提供以下的服務:

- 把您的IBKR賬戶與WISE賬戶關聯進行注資

- 把IBKR不直接支持的貨幣(例如羅馬尼亞列伊(RON)、保加利亞列弗(BGN)、馬來西亞令吉(MYR)、印度尼西亞盧比(IDR))從您的本地銀行轉帳至Wise,然後在Wise將其兌換成IBKR支持的貨幣(例如歐元(EUR)、美元(USD)等)存入您的IBKR賬戶。

- 從現有的Wise餘額向您的IBKR賬戶轉帳以及從IBKR賬戶轉回Wise

IBKR是否允許通過Wise進行存款和取款?

是,客戶可通過Wise把資金存入IBKR賬戶,也可從IBKR賬戶提取資金回存至Wise賬戶。

誰可以使用Wise注資方式?

IBLLC、IB-英國、IB愛爾蘭、IB中歐、IB-香港、IB-新加坡的個人客戶可以使用Wise轉帳資金。

如您還沒有開立Wise賬戶,您將收到創建賬戶的提示。IBKR將使用您在IBKR賬戶內的信息(姓名、電郵等)爲您預填Wise賬戶的申請,而您需要登錄wise.com以完成申請過程,幷上傳Wise可能會要求您提交的文件。

Wise與IBKR賬戶只需要建立一次關聯。您只能與您名下的Wise賬戶進行關聯。

如何通過Wise進行存款?

要通過Wise進行存款,請登錄客戶端選擇轉帳與支付,然後選擇轉帳資金。點擊存款然後在下拉菜單中選擇您想存款的幣種。選取合適的貨幣後,選擇“通過Wise進行銀行轉帳”或“從Wise餘額轉帳”作爲注資方式。

如這是您首次使用Wise注資方式,您將會收到與Wise賬戶關聯的提示。

如這是您首次使用Wise注資方式,您將會收到與Wise賬戶關聯的提示。

通過Wise進行銀行轉帳:爲所存入的本地貨幣(例如羅馬尼亞列伊(RON)、保加利亞列弗(BGN)、馬來西亞令吉(MYR)、印度尼西亞盧比(IDR))提供直接整合。 您將把本地貨幣轉帳至Wise銀行賬戶,而Wise將進行兌換,然後把IBKR支持的幣種存入到您的IBKR賬戶。本地貨幣的列表將取决于您IBKR賬戶所在的IBKR實體。

您將看到一個報價界面。源幣種是您在上方選擇的本地貨幣,而您需要選擇要存入您IBKR賬戶的目標幣種(例如美元(USD)、歐元(EUR))。您可修改源幣種的數量以查看適用費用、兌換匯率、IBKR賬戶將收到的目標幣種到賬金額以及預期到賬的時間。確認後,您將收到Wise銀行賬戶的詳情和轉帳資金的指令。

所需時間方面,從您的本地銀行轉帳資金至Wise可能需要幾個小時至幾個工作日,然後需要最多一整個工作日把資金從Wise轉至您的IBKB賬戶,具體時間視乎不同貨幣而定。

從Wise餘額轉帳:您可以看到Wise多幣種賬戶中的餘額,幷向IBKR賬戶發起資金轉帳。如Wise賬戶中的資金是IBKR賬戶支持的幣種,則您可在無需兌換的情况下轉帳資金;如果不是,則您可以選擇在Wise價格資金兌換成IBKR支持的幣種(例如歐元(EUR)、美元(USD))再轉入IBKR賬戶。

資金從您的Wise賬戶轉出之後,需要幾個小時至一整個工作日才會到達您的IBKR賬戶,具體時間視乎幣種而定。

如何從Wise賬戶取款?

您可從IBKR賬戶提取支持的幣種(例如歐元(EUR)、美元(USD))轉帳至您的Wise賬戶。

您可從IBKR賬戶提取支持的幣種(例如歐元(EUR)、美元(USD))轉帳至您的Wise賬戶。

要通過Wise賬戶提取資金,請登錄客戶端選擇轉帳與支付,然後選擇 轉帳資金。

點擊取款然後在下拉菜單中選擇您想取款的幣種。選取合適的貨幣後,選擇“轉帳至Wise”作爲取款方式。

如果這是您首次使用“轉帳至Wise”作爲取款方式,您將會收到把Wise賬戶與IBKR賬戶關聯的指示。Wise賬戶完成關聯後,系統會提示您用預填的Wise賬戶信息創建取款目的地。創建完成後,頁面將顯示您已保存的目的地,您剛才創建的目的地信息將顯示爲“轉帳至Wise”。選取這個選項,鍵入金額,然後提交取款請求進行處理。

資金從您的IBKR賬戶轉出之後,需要幾個小時至一整個工作日才會到達您的Wise賬戶,具體時間視乎幣種而定。

通過Wise轉帳資金需要收費嗎?

通過Wise轉帳資金可能涉及費用。如果需要收費,有關費用將在您提交轉帳資金的請求前,在確認屏幕顯示出來。

我可以通過Wise取款到第三方嗎?

不能。您只能取款到您名下的Wise賬戶。

如果轉帳發生問題,我可以聯繫誰?

如關于在客戶端發起轉帳有任何疑問,或如果您的款項已從Wise賬戶轉出超過一個工作日但仍未到達IBKR賬戶,請與IBKR聯繫。

如果是關于款項狀態、或從銀行向Wise轉帳碰到的問題、或資金在Wise處于等待狀態的相關問題查詢,請直接登錄您的Wise賬戶聯繫客戶服務。

在哪裏可以瞭解更多關于Wise及其服務的信息?

請參考Wise支持中心的頁面>www.wise.com/help。

How to Deposit DKK to Interactive Brokers

What transfer method can I use to fund my account in DKK?

IBKRs bank account for DKK is held with our Danish Bank and is eligible to receive DKK via RTGS (Real Time Gross Settlement) or International Bank Transfer (SWIFT).

IBKR does currently not support domestic transfer methods (local bank to bank transfer).

What Information does my bank need to transfer funds?

IBKR will provide you with our IBAN (International Bank Account Number) and the SWIFT code of our bank account upon completing the deposit notification in Client Portal.

If your bank is located in Denmark, they may ask you to provide local bank account details. Please explain that our account is not eligible for local bank to bank transfers and let them advise you on how to transfer funds using our IBAN/SWIFT. IBKR is working to implement local bank transfers, however we cannot provide you a date at this time when it will be available.

If your bank is located outside of Denmark, your bank will typically process payments via international bank wire (SWIFT) or the RTGS payment method. Your online banking will likely show Wire, electronic bank transfer or bank-to-bank transfer as available methods.

Your bank will select the method to transfer your funds on your behalf.

SWIFT payment

The Society for Worldwide Interbank Financial Telecommunication - SWIFT - is a network that allows banks to communicate financial information securely.

SWIFT payments are offered by most banks for international money transfers, and involve a series of banks which work together to make sure your money arrives at your account.

If you transfer DKK from a financial institution outside of Denmark, they may require the use of a so called intermediary or correspondent bank to route the payment through before reaching your account. These are called cross-border payments.

Bank transfers can take time to complete, particularly when it comes to cross-border payments. Clients are increasingly accustomed to a payments experience that feels instant, but making a payment to another country can be much more complex and time-consuming.

Processing bank transfers involves a number of steps – particularly for cross-border payments. These are sent via the correspondent banking network and typically pass between several different banks along the way. After being initiated, a wire transfer is sent by the debtor agent to an intermediary bank before moving on to the creditor agent. Once these steps are complete, the recipient will receive their funds.

There are a number of reasons why cross-border payments may be delayed or held up. Not all account balances can be updated outside the operating hours of local settlement systems. Delays can also arise if compliance checks need to be carried out, especially when a payment passes through different countries and jurisdictions.

RTGS payment

Kronos2 is Denmark National Bank's RTGS (Real-Time-Gross-Settlement) system for payments in Danish Krona and it is primarily used for settlement of large-value, time-critical interbank payments. You may consult with your bank which system they use to facilitate your payment.

You will typically not be given a choice on which method your bank will use to transfer your funds, and it depends as well on the size of payments, the banks involved in the transfer and what service your bank offers.

Difference between domestic and international bank transfer

Banks make a domestic wire transfer to send funds to financial institutions residing in the same country or financial zone. When sending funds to financial institutions in a foreign country or financial zone, banks have to make an international bank transfer. The differences between these two bank transfers affect the number of fees banks charge and the duration it takes to complete the transfer.

How long does it usually take for my funds to arrive?

|

Payment Type |

Timing |

Approximate Cost* |

| RTGS | same to 1 business day | vary by bank |

|

International bank transfer (SWIFT) |

from 1 to 4 business days |

vary by bank |

*Please consult with the sending institution about the costs to process your payment as this may vary by financial institution. IBKR does not charge fees for the deposit of funds.

Please note: IBKR credits funds real-time upon receipt under normal circumstances. Please note that we do not have influence on the speed of transfer. You may consult with the sending institution regarding their processing times and cut off times. Payments that are subject to additional review may take longer to credit.