Document Certification for Australian Residents

OVERVIEW

IB is required by regulation to verify the identity and address of each applicant and, where copies of physical documents are required, is often subject to local rules as to the type and form of documents which may be accepted. In the case of Australian residents, documents can only be accepted if certified as a true copy of the original by an approved individual. A list of such individuals along with other requirements and document submission instructions is outlined below.

LIST OF APPROVED CERTIFIERS

- Authorized/licensed/registered notary public

- Justice of the Peace with a registration number1

- A person who is enrolled on the roll of the Supreme Court of a State or Territory, or the High Court of Australia, as a legal practitioner (however described) (e.g. a solicitor or barrister)

- Manager of an Australian bank or credit union1

- A member of the Institute of Chartered Accountants in Australia, CPA Australia or the National Institute of Accountants with two or more years of continuous membership (e.g. an accountant)

- Officer of a company which holds an Australian financial services license or authorized representative of an Australian financial services licensee, having two or more continuous years of service with one or more licensees

- Dentist1

- Judges or masters of an Australian Federal, State or Territory court

- Medical Practitioners1

- Police officer in charge of police stations or of the rank of Sergeant or above1

- Agent of the Australian Postal Corporation who is in charge of an office supplying postal services to the public1

- Australian consular officer or an Australian diplomatic officer (within the meaning of the Consular Fees Act 1955) in Australia or overseas

1Person must be authorized/licensed/registered under Australian law.

OTHER REQUIREMENTS

Each page of the document being certified must contain the certifiers signature plus the following statement: "I certify this document to be a true and accurate copy of the original as sighted by me". Have the certifying party complete the Certified Copy Certificate Form for fastest processing. If you do not use the above form, ensure to include the following information on the first page of the document being certified:

- Full name of the certifier

- Signature of the certifier

- Date of certification

- Capacity of the certifier (e.g., Practicing solicitor, Justice of Peace, etc.)

- Registration number (if any) of the certifier's profession

- Number of pages if more than one

DOCUMENT SUBMISSION

Documents cannot be sent electronically and must be delivered to IB by mail or courier.

New Accounts Department

Interactive Brokers Australia Pty Ltd

P.O. Box R229

Royal Exchange, NSW 1225

Australia

Courier

New Accounts Department

Interactive Brokers Australia Pty Ltd

Level 40 Grosvenor Place

225 George Street, Sydney, NSW 2000

Australia

FATCA Procedures - Grantor Trust Tax Information Submission

Overview:

Interactive Brokers is required to collect certain documentation from clients to comply with U.S. Foreign Account Tax Compliance Act (“FATCA”) and other international exchange of information agreements.

This guide contains instructions for a Trust to complete the online tax information and to electronically submit a W-9 or W-8BEN.

U.S. Tax Classification

Your U.S. income tax classification determines the tax form(s) required to document the account.

You must login to Account Management with the trust's primary username to access the Tax Form Collection page.

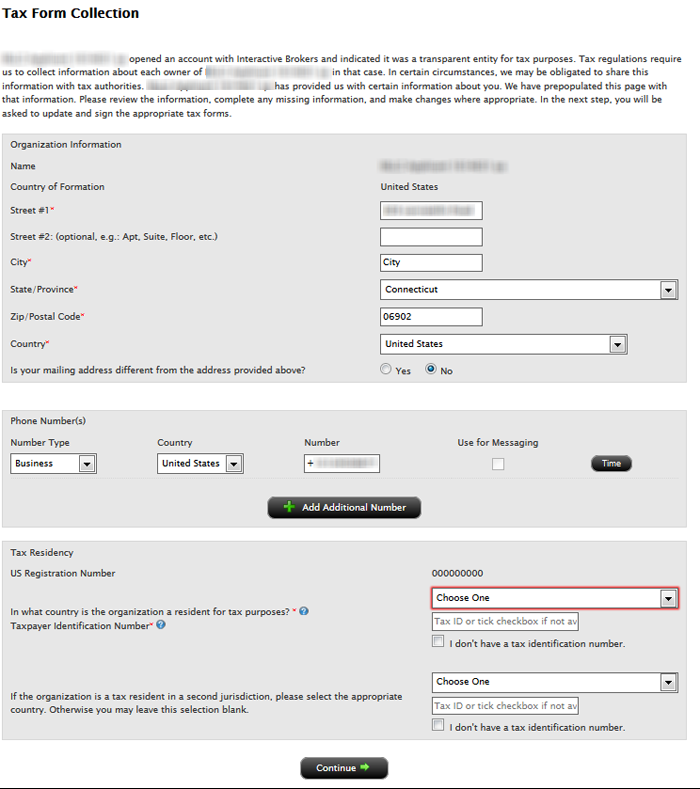

1. Tax Form Collection

The Tax Form Collection page lets account holders review and update important tax-related information and lets account holders electronically fill out an IRS Form W-9 (U.S. taxpayers) and IRS Form W-8 (non-U.S. taxpayers).

Accessing the Tax Form Collection Page

a. Click Manage Account > Account Information > Tax Information > Tax Forms.

b. Click the Update Tax Forms button to access the Collection page.

The Tax Form Collection page opens, displaying a form with tax-related information that should already be completed. (Advisors and brokers can check the status of client updates to this page on the Dashboard Pending Items tab.

c. Review the Trust’s information and update as required.

Confirm the primary tax residency of the trust beside the Tax Residency question, "In what country is the trust a resident for tax purposes?" Select the appropriate country in the drop down menu.

Select in the Tax Residency drop down menu the applicable country.

d. Click Continue.

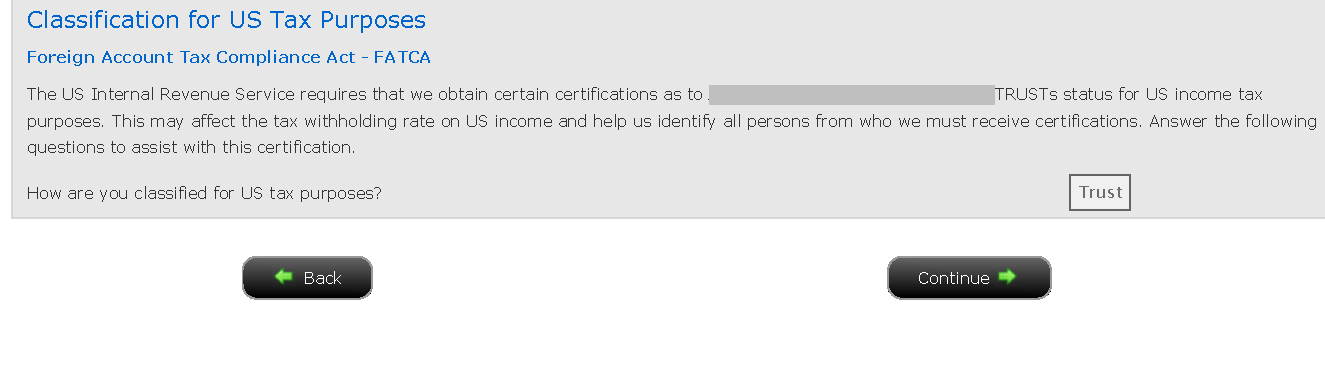

2. Classification for US Tax Purposes

Confirming the Trust’s classification for U.S. purposes

a. Review the Trust’s status by confirming the question, “How are you classified for US tax purposes?” The answer is pre-filled based upon your information completed during the account application process.

b. Click the Continue button to confirm the trust classification and complete the Form W-8 or W-9 for the entity.

c. Click the Continue button to identify each Grantor.

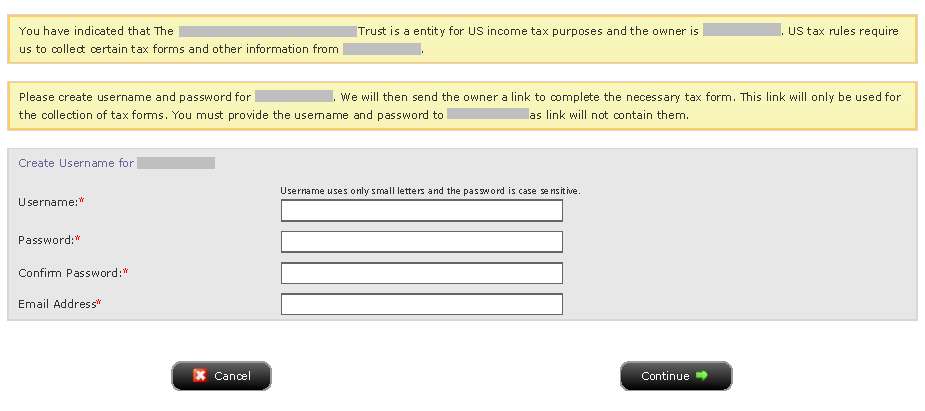

3. Identify Grantors

a. Click Manage Account > Account Information > Tax Information > Tax Forms.

b. Click the Create button beside each grantor to send each user the applicable tax questionnaire and to submit the tax certification form (W-8 or W-9).

Also, update the "Percentage of Ownership" to add up to 100%, if necessary.

.png)

c. Enter the required fields for the username and password for specified grantor and click the Continue button to complete the email delivery of the link.

We will then send the owner a link to complete the necessary tax form. This link will only be used for the collection of tax forms. You must provide the username and password to the Grantor as link will not contain them.

Each Grantor must login with the username/password created and complete the pending tasks by going to Manage Account > Account Information > Tax Information > Tax Forms > Update Tax Forms.

d. Click the Continue button upon creating and sending usernames to each Grantor.

Disclaimer

This guide does not constitute tax or legal advice and Interactive Brokers cannot advise you on how to complete an IRS Forms W-8 or W-9. Instructions are for information purposes only and do not address all possible scenarios. Please consult your tax professional if you are unsure how to complete.

Can I have more than two individuals on a joint account?

IBKR offers three types of joint accounts: Tenants with Rights of Survivorship, Tenancy in Common and Community Property. Each of these joint account types is limited to two account holders.

Applicants interested in opening an account with multiple owners in excess of two may consider the corporate, partnership, limited liability company or unincorporated legal structure account types offered by IBKR. Note that documentation establishing proof of formation and address are generally required at the point of application.

Converting From a Single to Joint Account

The process of adding a second owner to an existing single account for purposes of converting to a joint account is outlined below:

1. As the joint account structure differs from that of the individual in terms of account holder information required, legal agreements and, in certain cases, taxpayer status, direct conversion is not supported and a new joint account application must be completed online.

The joint application may be initiated online from the single account by logging into Client Portal and clicking the User menu (head and shoulders icon in the top right corner) followed by Manage Account. Click the Configure (gear) icon next to the words Open an Additional Account. This process will allow you to retain your existing user name, password and security device for purposes of operating the joint account. Be sure to request trading permissions and, if necessary, margin status, sufficient to maintain the positions currently carried in your individual account. Note that if your account is managed by a financial advisor or you are a client of an introducing broker, please contact your advisor or broker to initiate the new application (you may need to make arrangements with your advisor or broker for fees that have accrued but not yet paid if the individual account closes).

The joint account application requires Compliance review and approval and documentation evidencing the identity and address of the second account holder may be required. If this is the case, notice as to the required documents and how to submit will be provided at the conclusion of the online application.

2. Once you have received an email confirming approval of the joint account application, send a request from your Message Center authorizing IBKR to manually transfer positions from your single to joint account. Prior to submitting the request you should make sure to close all open orders in the individual account to ensure that no executions take place following the transfer.

Due to the manual steps and scheduling required, you should allow a minimum of one week after joint account approval and submitting your request for the transfer to take effect.

IMPORTANT NOTES

1. Note that exchange regulations preclude ownership transfer of derivative contracts such as futures and options. If you are holding such positions you would either need to close them prior to the transfer taking place or request that they remain in your individual account.

2. Prior to processing the transfer, you should make sure to close all open orders in the individual account to ensure that no executions take place following the transfer.

3. The SMA (Special Memorandum Account) balance in your individual account will not transfer to the joint account. In certain cases this may impact your ability to open new positions in the joint account on the first day after the transfer is completed.

4. Elective options such as participation in IBKR's Stock Yield Enhancement Program will not be carried over to the joint account and must be re-initiated to continue.

5. The cost basis of transferred positions as reported in the activity statements will remain unchanged for tax purposes.

6. Once the transfer has been completed and assuming all positions have been transferred your individual account will be designated for automatic closure. Note that certain balances such as dividend accruals can’t be transferred until paid, after which they will then be transferred and your individual account closed.

7. You'll receive any applicable tax forms for the reportable activity transacted in each of your individual and joint accounts at year end. Access to Client Portal for your individual account will remain after it has been closed for the purpose of reviewing and printing activity statements and tax forms.

8. IBKR does not provide tax advice or investment guidance and recommends that account holder consult with qualified professionals to determine any legal, tax or estate planning consequences associated with single to joint transfer requests.

Market Data Non-Professional Questionnaire

Overview:

Insight into completing the new Non-Professional Questionnaire.

Background:

The NYSE and most US exchanges require vendors to positively confirm the market data status of each customer before allowing them to receive market data. Going forward, the Non-Professional Questionnaire will be used to identify and positively confirm the market data status of all customer subscribers. As per exchange requirements, without positively identifying customers as non-professional, the default market data status will be professional. The process will protect and maintain the correct market data status for all new subscribers. For a short guide on non-professional definitions, please see https://ibkr.info/article/2369.

Each question on the questionnaire must be answered in order to have a non-professional designation. As exchanges require positive confirmations of proof for non-professional designations, an incomplete or unclear Non-Professional Questionnaire will result in a Professional designation until the status can be confirmed.

If the status should change, please contact the helpdesk.

Explanation of questions:

1) Commercial & Business purposes

a) Do you receive financial information (including news or price data concerning securities, commodities and other financial instruments) for your business or any other commercial entity?

Explanation: Are you receiving and using the market data for use on behalf of a company or other organization aside from using the data on this account for personal use?

b) Are you conducting trading of any securities, commodities or forex for the benefit of a corporation, partnership, professional trust, professional investment club or other entity?

Explanation: Are you trading for yourself only or are you trading on behalf of an organization (Ltd, LLC, GmbH, Co., LLP, Corp.)?

c) Have you entered into any agreement to (a) share the profit of your trading activities or (b) receive compensation for your trading activities?

Explanation: Are you being compensated to trade or are you sharing profits from your trading activities with a third party entity or individual?

d) Are you receiving office space, and equipment or other benefits in exchange for your trading or work as a financial consultant to any person, firm or business entity?

Explanation: Are you being compensated in any way for your trading activity by a third party, not necessarily by being paid in currency.

2) Act in a capacity

a) Are you currently acting in any capacity as an investment adviser or broker dealer?

Explanation: Are you being compensated to manage third party assets or compensated to advise others on how to manage their assets?

b) Are you engaged as an asset manager for securities, commodities or forex?

Explanation: Are you being compensated to manage securities, commodities, or forex?

c) Are you currently using this financial information in a business capacity or for managing your employer’s or company’s assets?

Explanation: Are you using data at all for a commercial purposes specifically to manage your employer and/or company assets?

d) Are you using the capital of any other individual or entity in the conduct of your trading?

Explanation: Are there assets of any other entity in your account other than your own?

3) Distribute, republish or provide data to any other party

a) Are you distributing, redistributing, publishing, making available or otherwise providing any financial information from the service to any third party in any manner?

Explanation: Are you sending any data you receive from us to another party in any way, shape, or form?

4) Qualified professional securities / futures trader

a) Are you currently registered or qualified as a professional securities trader with any security agency, or with any commodities or futures contract market or investment adviser with any national or state exchange, regulatory authority, professional association or recognized professional body? i, ii

YES☐ NO☐

i) Examples of Regulatory bodies include, but are not limited to,

- US Securities and Exchange Commission (SEC)

- US Commodities Futures Trading Commission (CFTC)

- UK Financial Service Authority (FSA)

- Japanese Financial Service Agency (JFSA)

ii) Examples of Self-Regulatory Organization (SROs) include, but are not limited to:

- US NYSE

- US FINRA

- Swiss VQF

CFTC Ownership and Control Reporting

The Commodities Futures Trading Commission (CFTC) has historically maintained rules which require FCMs to report information relating to clients holding positions equal to or exceeding defined thresholds (e.g., Large Trader Reporting). In November 2013, the CFTC adopted a new rule which expands the prior reporting rules and which requires the collection and reporting of more comprehensive information on owners and controllers of accounts trading U.S. commodity futures products. This new rule is referred to as Ownership and Control Reporting (OCR) and outlined below are a series of FAQs relating to this rule.

1. Who must provide CFTC OCR information?

In order to comply with the requirement that any account meeting the position or volume thresholds be reported to the CFTC by 09:00 ET on the day following the day in which the account becomes reportable, IB requires that all accounts trading U.S. commodity futures products provide the requested information.

In order to comply with the requirement that any account meeting the position or volume thresholds be reported to the CFTC by 09:00 ET on the day following the day in which the account becomes reportable, IB requires that all accounts trading U.S. commodity futures products provide the requested information.

2. What information must be provided?

The following information is required of all Owners and Controllers of an account:

• Name

• Street Address

• Email Address

• Direct Phone Number, Including Country Code

The following information is required of all Owners and Controllers of an account:

• Name

• Street Address

• Email Address

• Direct Phone Number, Including Country Code

The following details are also required for owners and controllers that are legal entities:

• Legal Entity Identifier (LEI), If Applicable

• Contact Person Details:

o Name

o Job Title

o Relationship to Legal Entity

o Direct Phone Number, Including Country Code

• Legal Entity Identifier (LEI), If Applicable

• Contact Person Details:

o Name

o Job Title

o Relationship to Legal Entity

o Direct Phone Number, Including Country Code

The following details are also required for all individuals who are “Account Controllers”:

• Individual’s Relationship to Account Owner

• Individual’s Job Title

• Name of Individual’s Employer

• Employer’s Legal Entity Identifier (LEI), If Applicable

• Individual’s Relationship to Account Owner

• Individual’s Job Title

• Name of Individual’s Employer

• Employer’s Legal Entity Identifier (LEI), If Applicable

3. Who is an "Account Owner" for the purposes of OCR?

An "Account Owner" includes any individual or legal entity who holds a direct ownership interest in the trading account.

4. Who is an "Account Controller" for the purposes of OCR?

The CFTC defines an “Account Controller” as “a natural person who by power of attorney or otherwise actually directs the trading of an account. A trading account may have more than one controller.”

This definition can be found at 17 C.F.R. § 15.00(bb).

An "Account Owner" includes any individual or legal entity who holds a direct ownership interest in the trading account.

4. Who is an "Account Controller" for the purposes of OCR?

The CFTC defines an “Account Controller” as “a natural person who by power of attorney or otherwise actually directs the trading of an account. A trading account may have more than one controller.”

This definition can be found at 17 C.F.R. § 15.00(bb).

5. What is the "Head of Desk" option?

As noted above, you must provide full OCR information for all Owners and Controllers of your account. Unless you indicate otherwise, IB presumes that every active TWS user on your account is an Account Controller for CFTC OCR purposes.

Your institution may have a "Head of Desk" who directs the trading of your institution's trading account, with the other traders simply acting under this individual's direction. If this is the case, you can identify the "head of desk" using the Account Management OCR interface, in which case "Account Controller" information will only be required for that individual.

6. What is a Legal Entity Identifier (LEI)?

An LEI is a unique 20 -digit alphanumeric code associated with a single organization and which is intended to be recognized universally across regulatory agencies and jurisdictions.

-If any of the Account Owners or Controllers of your account have LEIs, you must provide the LEIs;

-If an Account Owner or Controller of your account does not have an LEI, you can select "non applicable".

DTC, in collaboration with SWIFT, operate as the local (U.S.) source provider of LEIs and maintains a website (www.gmeiutility.org) for the assignment of new and search of existing LEIs.

7. What is a National Futures Association (NFA) ID?

A number which the National Futures Organization assigns to each registrant (e.g., firms and individuals such as Commodity Trading Advisors and Commodity Pool Operators). The NFA maintains an Online Registration System (ORS) through which registration and assignment of the ID is provided. See www.nfa.futures.org

A number which the National Futures Organization assigns to each registrant (e.g., firms and individuals such as Commodity Trading Advisors and Commodity Pool Operators). The NFA maintains an Online Registration System (ORS) through which registration and assignment of the ID is provided. See www.nfa.futures.org

8. How do I know if my employer has an LEI or NFA ID?

You may ask your employer to provide you with this information or search one of the following websies:

You may ask your employer to provide you with this information or search one of the following websies:

LEI searches may be performed via the following DTC website: www.gmeiutility.org. Searches may be conducted by the entity's registered legal name or address.

NFA ID searches may be performed via the following NFA webpage: www.nfa.futures.org/basicnet/welcome.aspx . Searches may be conducted by entering a firm name, individual name or pool name.

9. Why must I provide this information?

U.S. federal regulations require all FCMs, including IB, to obtain this information from its clients. The requirement is universal and applies to any individual or entity regardless of their broker.

U.S. federal regulations require all FCMs, including IB, to obtain this information from its clients. The requirement is universal and applies to any individual or entity regardless of their broker.

10. Does OCR apply to non-U.S. persons?

Yes, if you wish to trade U.S. commodity futures products, we must collect this information from you.

Yes, if you wish to trade U.S. commodity futures products, we must collect this information from you.

11. How will Interactive Brokers treat this information?

This data will be kept confidential in accordance with the Interactive Brokers Group Privacy Statement. See link for details: https://individuals.interactivebrokers.com/en/index.php?f=ibgStrength&p=priv

This data will be kept confidential in accordance with the Interactive Brokers Group Privacy Statement. See link for details: https://individuals.interactivebrokers.com/en/index.php?f=ibgStrength&p=priv

12. Can I enter the OCR information in multiple sessions?

Unfortunately, all data must be entered within a single session and partial entry and a save option is not available. If you do not enter all required OCR information in a single session, you will need to start all over and reenter it in your next session.

13. Are foreign brokers subject to OCR?

Yes. As a foreign broker you must either:

a) Ensure that IB has OCR information for all of your customers that trade U.S. commodity futures products; or

b) Perform your own OCR submissions on their behalf.

14. Where can I learn more?

The full text of this rule change is available on the CFTC website

The full text of this rule change is available on the CFTC website

Hong Kong - China Stock Connect

Hong Kong – China Stock Connect (“China Connect”) is a mutual market access program through which Hong Kong and international investors can trade shares listed on the Shanghai Stock Exchange (SSE) and Shenzhen Stock Exchange (SZSE) via the Stock Exchange of Hong Kong (SEHK) and their existing clearinghouse. As a member of SEHK, IBKR provides you with direct access to trade with eligible listed products on the Shanghai and Shenzhen Stock Exchange. IBKR clients with China Connect trading permissions will be eligible to trade SSE/SZSE securities through Shanghai and Shenzhen - Stock Connect.

Among the different types of SSE/SZSE-listed securities, only A shares (shares in mainland China-based companies that trade on Chinese stock exchange) are included in the Shanghai and Shenzhen Stock Connect.

Shanghai Connect includes all the constituent stocks of the SSE 180 Index, SSE 380 Index and all the SSE-listed A shares that have corresponding H shares listed on the SEHK.

Product List and Stock Codes for SSE

Shenzhen Connect includes all the constituent stocks of the SZSE Component Index, the SZSE Small/Mid Cap Innovation Index that have a market capitalization of not less than RMB 6 billion and all the SZSE-listed A shares that have corresponding H shares listed on SEHK.

Product List and Stock Codes for SZSE

IBKR Commission for Trading SSE/SZSE Securities

Same as trading Hong Kong stocks, IBKR charges only 0.08% of trade value as a commission with a minimum CNH 15 per order. Detailed fee rates can be found in the Hong Kong – China Stock Connect Northbound fee table.

Daily Quota

Trading under Shanghai Connect and Shenzhen Connect is subject to a Daily Quota. The Daily Quota is applied on a “net buy” basis. The Daily Quota limits the maximum net buy value of cross-boundary trades under Shanghai Connect and Shenzhen Connect each day.

If the Northbound Daily Quota Balance drops to zero or the Daily Quota is exceeded during the opening call auction session, new buy orders will be rejected. Or if it happens during a continuous auction session or closing call auction session, no further buy orders will be accepted for the remainder of the day. SEHK will resume the Northbound buying service on the following trading day.

SEHK will also publish the remaining balance of the Aggregate Quota and Daily Quota.

For details, please refer to HKEX Stock Connect FAQ or HKEX Stock Connect Rule 1407

Trading Information of Shanghai and Shenzhen Connect

|

Trading currency |

RMB |

|

Order Type |

IBKR offers various order types but will stimulate the order into limit order for execution. More information can be referred to our website.

|

|

Tick Size / Spread |

Uniform at RMB 0.01 |

|

Board Lot |

100 shares (applicable for buyers only) |

|

Odd Lot |

Sell orders only (odd lot should be made in one single order) |

|

Max Order Size |

1 million shares |

|

Price Limit |

±10% on previous closing price (±5% for stocks under special treatment under risk alert, i.e. ST and *ST stocks) |

|

Day (Turnaround) Trading |

Not allowed |

|

Block Trade |

Not available |

|

Manual Trade |

Not available |

|

Order Modification |

IBKR will cancel and replace the order for any order modification |

|

Settlement cycle |

Securities: Settlement on T day Cash from China Connect trades: Settlement on T+1 day Forex*: Settlement on T+2 day |

*Due to the unsynchronized settlement cycle, clients who exchange CNH themselves should execute the Forex trade one day prior to the stock trade (T-1) to avoid the extra day’s interest payment (considering normal settlement without involving holidays).

Trading Hours

|

SSE/SZSE Trading Sessions |

SSE/SZSE Trading Hours |

|

Opening Call Auction |

09:15 - 09:25 |

|

Continuous Auction (Morning) |

09:30 – 11:30 |

|

Continuous Auction (Afternoon) |

13:00 – 14:57 |

|

Closing Call Auction |

14:57 – 15:00 |

Half-day Trading

If a Northbound trading day is a half-trading day in the Hong Kong market, it will continue until respective Connect Market is closed. Refer to the exchange website for holiday trading arrangements and additional information.

Disclosure Obligation

If client holds or controls up to 5% of the issued shares of China Connect, the client is required to report in writing to the China Securities Regulatory Commission (“CSRC”) and the relevant exchange, and inform the Mainland listed company within three working days of reaching 5%.

The client is not allowed to continue purchasing or selling shares in that Mainland listed company during the three days notification period. Visit the IBKR Knowledge Base for more information.

Shareholding Restriction

A single foreign investor’s shareholding in a Mainland listed company is not allowed to exceed 10% of the company’s total issued shares, while all foreign investors’ shareholding in the A shares of the listed company is not allowed to exceed 30% of its total issued shares. Visit the IBKR Knowledge Base for more information.

Forced-sale Arrangement

Each IBKR client is not allowed to hold more than a specific percentage of the China Connect listing company's total issued shares. HKEX requires the client to follow the forced-sell requirements if the shares exceed the limit:

|

Situation |

Shareholding (in a listed company) |

|

A single foreign investor |

> = 10% of the company’s total issued shares |

|

All foreign investors |

> = 30% of the company’s total issued shares |

Margin Financing

Margin trading in China Connect securities will subject to restrictions and only certain A shares will be eligible for margin trading. Eligible Securities, as determined by SSE and SZSE from time to time, are listed on the HKEX website.

According to the relevant rules of SSE and SZSE, either market may suspend margin trading activities in specific A shares when the volume of margin trading activities for a specific A share exceeds the prescribed threshold. The market will resume margin trading activities in the affected A share when its volume drops below a prescribed threshold.

Stock Borrowing and Lending (SBL)

SBL in China Stock Connect Securities is subject to restrictions set by the SSE or SZSE and stated in the Rules of the Exchange.

IBHK does not offer this service at the moment.

Eligible Short Selling Securities

SBL for the purpose of short selling will be limited to those China Stock Connect Securities that are eligible for both buy orders and sell orders through Shanghai and Shenzhen Connect (i.e., excluding Connect Securities that are only eligible for sell orders).

IBHK does not offer this service at the moment.

Trading Shenzhen ChiNext and Shanghai Star shares

Trading Shenzhen ChiNext and Shanghai Star shares are limited to institutional professional investors.

Holidays

Clients will only be allowed to trade China Connect on days where Hong Kong and Mainland markets are both open for trading and banking services are available in both Hong Kong and Mainland markets on the corresponding settlement days. This arrangement is essential in ensuring that investors and brokers will have the necessary banking support on the relevant settlement days when they will be required to make payments.

The following table illustrates the holiday arrangement of Northbound trading of SSE/SZSE Securities:

|

|

Mainland |

Hong Kong |

Open for Northbound Trading |

|

Day 1 |

Business Day |

Business Day |

Yes |

|

Day 2 |

Business Day |

Business Day |

No, HK market closes on money settlement day |

|

Day 3 |

Business Day |

Public Holiday |

No, HK market closes on trading day |

|

Day 4 |

Public Holiday |

Business Day |

No, Mainland market closes |

Severe Weather Conditions

Information on the trading arrangement available under severe weather conditions can found on the HKEx website.

Where to Learn More?

Please refer to the following exchange website links for additional information regarding Hong Kong China Stock Connect:

If you have any questions regarding Hong Kong-China Stock Connect, please contact IBKR Client Services for further information.

Foreign Acount Tax Compliance Act (FATCA)

What is FATCA?

The Foreign Account Tax Compliance Act (FATCA) represents the United States efforts to combat tax evasion and abuse by US persons holding investments outside of the United States. The Act establishes a new set of tax information reporting and withholding procedures. While not expressly aimed at non-US persons, the regulations do impose withholding taxes on certain non-US entities that decline to disclose their US investors or account holders.

Under FATCA, US persons must report to the US tax authority, Internal Revenue Service (IRS), their assets held in offshore accounts. In addition, the regulations seek to require non-US financial institutions to report to the US tax authority certain information about financial accounts of US or US-owned investors and account holders.

How does this impact US Brokers, including Interactive Brokers?

As a broker based in the United States, Interactive Brokers is required to report information and make payment of withholding taxes to the IRS, for all of our customers. FATCA simply creates additional practices and withholdings to the current requirements for all US brokers.

Interactive Brokers will comply with the new rules. This may require additional disclosures by investors during the account application process, as well as expanded tax reporting. For all US institutions, FATCA becomes effective January 1, 2013. Any FATCA tax withholding requirements begin on January 1, 2014.

Additional aspects of the regulations will be phased-in over the next few years, including an expansion of US brokers reporting on US source income to non-US accounts through Form 1042-S.

What action is required for US persons?

No additional action is required for US persons holding Interactive Brokers accounts. US persons, who include US citizens, Green Card holders and other legal residents, need only to complete Form W-9 during the account application process to certify their tax status.

Does FATCA affect non-US accounts?

Yes. FATCA requires foreign financial institutions (FFIs) to furnish certain data directly to the IRS about any of their US taxpayer accounts or foreign entity accounts in which US taxpayers hold a certain level of ownership. FFI compliance with the new regulations becomes effective July 1, 2013 with the submission of electronic FFI applications to the IRS. The application forms are scheduled to be available through the IRS in January 2013.

All non-US persons and entities applying for and maintaining Interactive Broker accounts will continue to be required to fully disclose and indentify the identity of their account's beneficial owner(s). Through the IRS Form W-8, our account holders certify the beneficial owner's country of tax residence. If you fail to provide a Form W-8, or do not resubmit a new W-8 when prompted upon the three-year expiration, additional withholding will apply.

Some entities not ordinarily considered to be financial institutions may be categorized under FATCA as an FFI. Therefore, it is important to review the details outlined by the IRS.

Is there a summary of FFI requirements?

While the regulations and compliance are far more complex than a brief FAQ can describe, the following offers a short summary of actions required by those defined foreign financial institutions.

- Identify US taxpayers. If US taxpayers refuse to waive your non-US country's privacy or secrecy rules, then the US taxpayer account must be closed.

- Report to the IRS on the related US taxpayer activity within defined financial accounts.

- Withhold 30% US tax on US source income against any US taxpayer or foreign entity failing to disclose information or comply with the FATCA regulations.

Additional Information & Resources

The IRS remains the most comprehensive and up-to-date resource about FATCA compliance, implementation, and document filing. The IRS continues to issue news releases and forms. Please feel free to visit the IRS FATCA Website for details.

IRS Circular 230 Notice: These statements are provided for information purposes only, are not intended to constitute tax advice which may be relied upon to avoid penalties under any federal, state, local or other tax statutes or regulations, and do not resolve any tax issues in your favor.

IRA: Retirement Account Resource Center

IMPORTANT NOTE: This article has been customized for use by self-directed Individual Retirement Account (IRA) owners for information purposes only. Persons are encouraged to consult a qualified tax professional with the investments and elections within the IRA. IB does not provide tax advice. For detailed information regarding IRAs, you may consult the IRS Publication 590-A about IRA contributions and the IRS Publication 590-B about IRA distributions.

This resource center provides a central reference point for information concerning the various IRA account types offered by IB.

Important Notice - Select IRA Tax Reporting for key information with transaction and tax reporting in your IRA.

Account Management IRA Reference

Beneficiary Options

Recharacterizations from a Roth IRA

Required Minimum Distributions

IRS Circular 230 Notice: These statements are provided for information purposes only, are not intended to constitute tax advice which may be relied upon to avoid penalties under any federal, state, local or other tax statutes or regulations, and do not resolve any tax issues in your favor.

How to send documents to IBKR using your smartphone

Overview:

Interactive Brokers allows you to send us a copy of a document even if you do not currently have access to a scanner. You can take a picture of the requested document with your smartphone.

Below you will find the instructions on how to take a picture and send it per email to Interactive Brokers with the following smartphone operating systems:

If you already know how to take and send pictures per email using your smartphone, please click HERE - Where to send the email to and what to include in the subject.

iOS

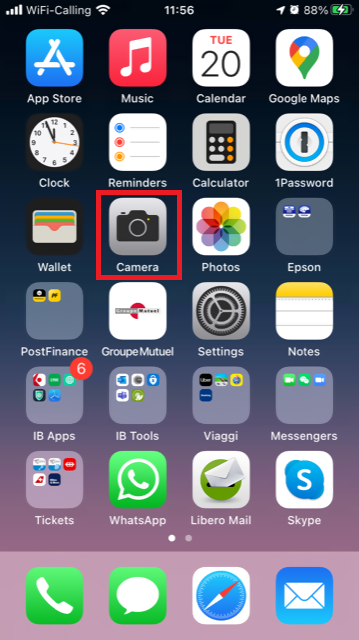

1. Swipe up from the bottom of your smartphone screen and tap the camera icon.

If you do not have the Camera icon, you can tap the Camera app icon from the home screen of your iPhone.

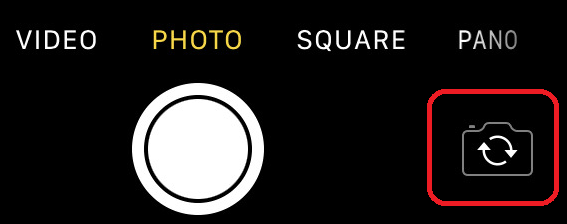

Normally your phone should now activate the rear camera. If it activates the front one, tap the camera switch button.

2. Place your iPhone above the document and frame the desired portion or page of the document.

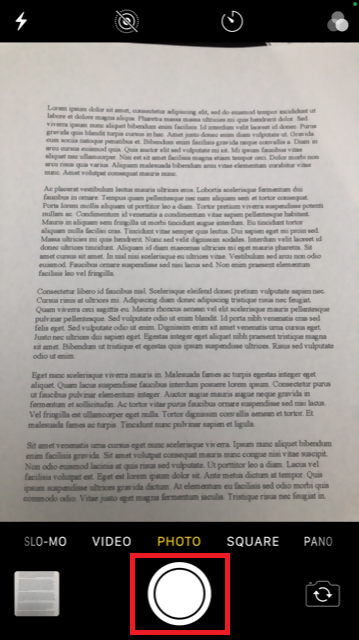

3. Make sure to have uniform, sufficient lighting and not to cast any shadow on the document due to your position. Hold the smartphone firmly with your hand/s and avoid shaking. Tap on the shutter button to take the photo.

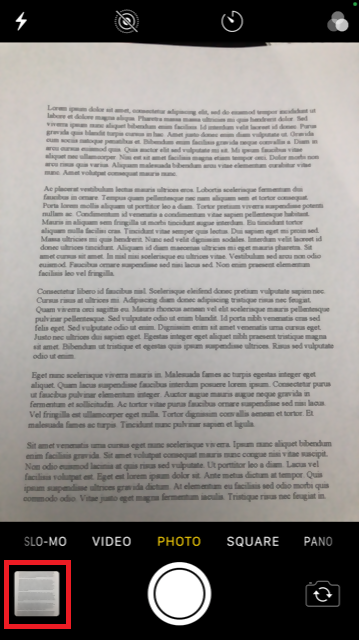

4. Tap the thumbnail image in the lower left-hand corner to access the picture you have just taken.

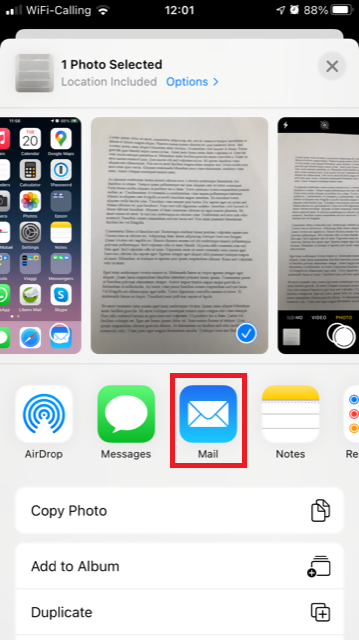

5. Make sure that the picture is clear and the document is well legible. You can enlarge the picture and see it in detail by swiping apart two fingers on the picture itself.

If the picture does not present a good quality or lighting, please repeat the previous steps in order to take a sharper one.

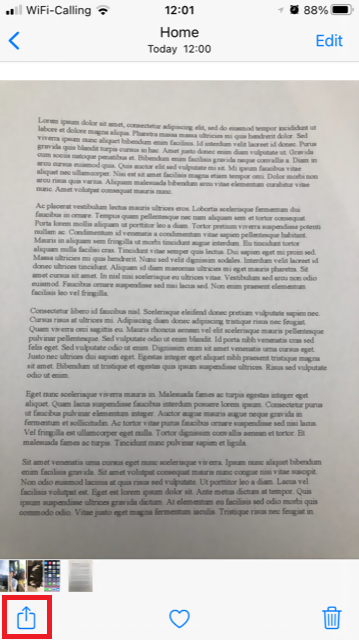

6. Tap the share icon in the lower left-hand corner of the screen.

7. Tap the Mail icon.

Note: to send emails your phone has to be configured for that. Please contact your email provider if you are not familiar with this procedure.

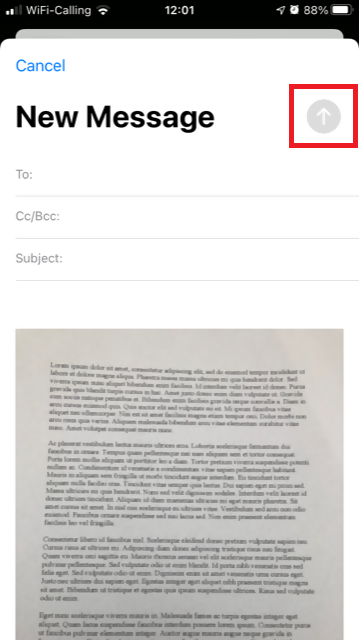

8. Please see HERE how to populate the To: and Subject: fields of your email. Once the email is ready, tap the up arrow icon on the top right to send it.

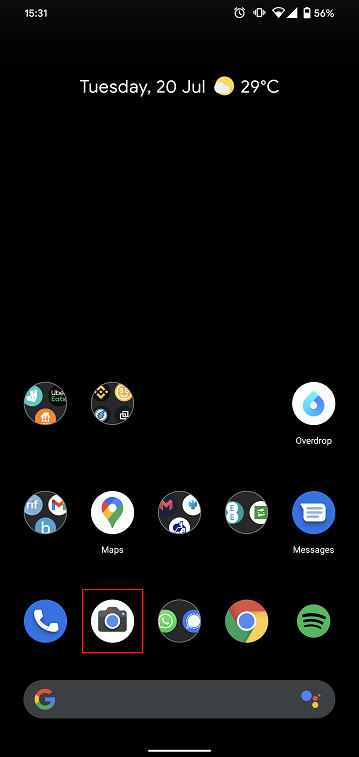

Android

1. Open your applications list and start the Camera app. Alternatively start it from your Home screen. Depending on your phone model, maker or setup, the app might be called differently.

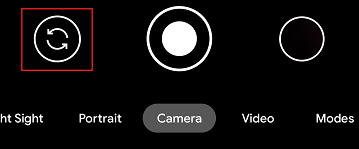

Normally your phone should now activate the rear camera. If it activates the front one, tap the camera switch button.

2. Place your Android above the document and frame the desired portion or page of the document.

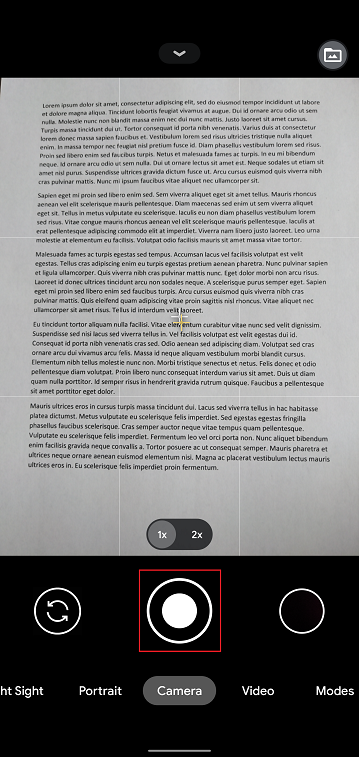

3. Make sure to have uniform, sufficient lighting and not to cast any shadow on the document due to your position. Hold the smartphone firmly with your hand/s and avoid shaking. Tap on the shutter button to take the photo.

4. Make sure that the picture is clear and the document is well legible. You can enlarge the picture and see it in detail by swiping apart two fingers on the picture itself.

If the picture does not present a good quality or lighting, please repeat the previous steps in order to take a sharper one.

5. Tap the empty circle icon in the lower right-hand corner of the screen.

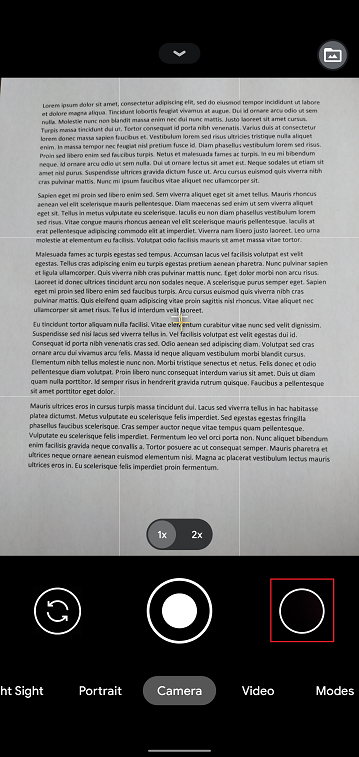

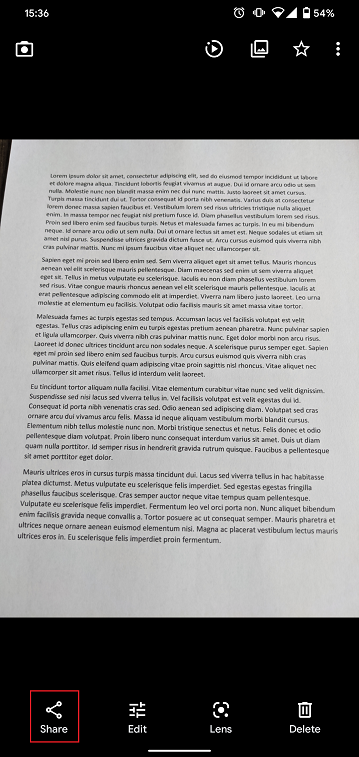

6. Tap the share icon in the lower left-hand corner of the screen.

7. In the sharing menu that will be displayed now tap the icon of the email client set up on your phone. In the example picture below, it is called Gmail but the name may vary according to your specific setup.

.png)

Note: to send emails your phone has to be configured for that. Please contact your email provider if you are not familiar with this procedure.

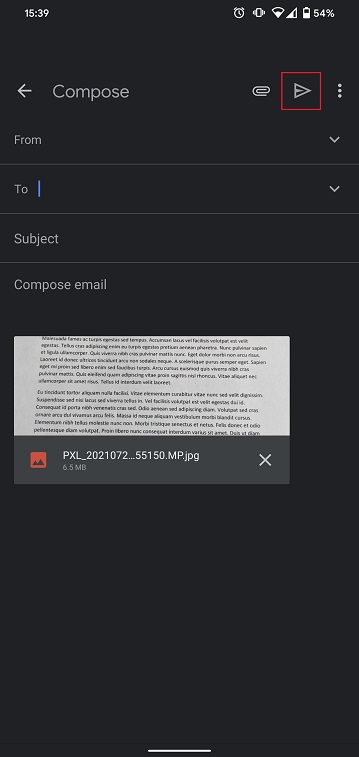

8. Please see HERE how to populate the To and Subject fields of your email. Once the email is ready, tap the airplane icon on the top right to send it.

WHERE TO SEND THE EMAIL AND WHAT TO INCLUDE IN THE SUBJECT

The email has to be created observing the below instructions:

1. In the field To: type:

- newaccounts@interactivebrokers.com if you are a resident of a non-European country

- newaccounts.uk@interactivebrokers.co.uk if you are a European resident

2. The Subject: field must contain all of the below:

- Your account number (it usually has the format Uxxxxxxx, where x are numbers) or your username

- The purpose of sending the document. Please use the below convention:

- PoRes for a proof of residential address

- PID for a proof of identity