Методологии расчета маржи

Введение

Методология расчета маржинального требования для той или иной позиции во многом зависит от следующих трех факторов:

1. Тип продукта;

2. Правила биржи, на которой он котируется, и/или надзорного органа, регулирующего брокера;

3. Внутренние правила IBKR.

Хотя существуют разные методологии, всех их можно разделить на две категории: основанные на правилах и основанные на риске. Основанные на правилах методологии устанавливают единые ставки маржи для похожих продуктов, не учитывают при расчете маржи другие продукты и расценивают деривативные инструменты на условиях, схожих с маржей для их андерлаингов. Такие методологии используют упрощенный расчет, но зачастую делают допущения, которые могут преуменьшать или преувеличивать риск инструмента в сравнении с его показателями в прошлом. Типичным примером такой методологии является правило Reg. T свода федеральных законов США.

Методологии, основанные на риске, стремятся при расчете маржи учесть доходность продукта в прошлом и другие продукты в портфеле и смоделировать нелинейную динамику рисков деривативных продуктов, используя математические модели ценообразования. Данный тип методологий, хотя является наглядным, требует сложных расчетов, которые трудно воспроизвести самостоятельно. Кроме того, поскольку вводные данные зависят от наблюдаемого поведения рынка, рассчитываемые требования могут быстро и значительно меняться. К этому типу методологий можно отнести TIMS и SPAN.

Независимо от типа методологии, большинство брокеров устанавливают собственные внутренние требования маржи, часто превышающие биржевые, особенно в случаях повышенных рисков для брокера, для защиты от которых недостаточно базовых требований. Ниже приведено краткое описание наиболее распространенных методологий, основанных на риске и правилах.

Методологии

Основанные на риске

a. Маржевый портфель (TIMS) – от англ. Theoretical Intermarket Margin System, методология, разработанная Опционной клиринговой корпорацией США (OCC). Включает расчет стоимости портфеля при разных гипотетических условиях на рынке, включая изменение цены и переоценку позиций. Методология использует модель расчета цены опционов для переоценки их стоимости и, помимо гипотетических сценариев OCC, применяет дополнительные сценарии для учета большего числа рисков, например, резкого движения рынка, концентрированных позиций и изменений подразумеваемой волатильности опционов. Кроме того, маржа недоступна для некоторых ценных бумаг (например, внебиржевых ценных бумаг и бумаг с низкой капитализацией). После расчета предполагаемых значений для портфеля при каждом сценарии в качестве маржи устанавливается требование, рассчитанное для сценария с максимальным потенциальным убытком.

Методология TIMS может применяться к позициям по акциям, ETF, опционам, фьючерсам на одиночные акции США и акциям и опционам других стран, отвечающим условиям свободного рынка SEC.

Поскольку данная методология использует более сложные расчеты, чем основанные на правилах, она позволяет более точно моделировать риск и, как правило, предлагает больший леверидж. Из-за увеличенного левериджа и быстро меняющихся маржинальных требований в ответ на изменение условий на рынке, эта методология больше подходит опытным инвесторам. Начальное требование капитала на счете для ее использования составляет $110 000, а минимальное – $100 000. Маржинальные требования для акций по этой методологии составляют от 15% до 30%, при этом более выгодные условия применяются к портфелям, которые хорошо диверсифицированы, содержат акции с низкой волатильностью и хеджированы при помощи опционов.

b. SPAN (от англ. Standard Portfolio Analysis of Risk) – методология расчета маржи на основе риска, созданная Чикагской товарной биржей (CME) для фьючерсов и фьючерсных опционов. Как и TIMS, SPAN определяет маржинальные требования, рассчитывая стоимость портфеля на основе гипотетических условий на рынке и изменении цены андерлаинга и подразумеваемой волатильности опционов. В этом случае IBKR также задает собственные условия, включающие максимальные изменения цен и влияние таких изменений на опционы "вне денег". В качестве необходимой маржи устанавливается требование, рассчитанное для сценария с максимальным потенциальным убытком. Подробное описание системы SPAN приведено в статье KB563.

Основанные на правилах

a. Reg. T – ответственность по обеспечению стабильной финансовой системы и ограничению риска на финансовом рынке несет центральный банк США – Федеральная резервная система. ФРС достигает эти цели, в том числе, устанавливая максимальный размер кредита, который брокеры-дилеры могут предоставлять клиентам, желающим одолжить средства для покупки ценных бумаг с маржей.

Этот лимит указан в правиле Т, или Reg. T (англ. Regulation T), которое устанавливает критерии для открытия маржинального счета, а также начальные маржинальные требования и порядок оплаты определенных транзакций с ценными бумагами. Например, в настоящее время, согласно Reg. T, для покупки ценных бумаг клиент должен обеспечить начальную маржу в размере 50% от стоимости транзакции, и брокер может предоставить заем на оставшиеся 50%. Так, если клиент хочет купить ценные бумаги на сумму $1 000, он должен внести на счет $500 и может занять $500.

Reg. T определяет только начальные и минимальные маржинальные требования, правила для сохранения позиции устанавливает биржа (для акций составляет 25%). Reg. T также не оговаривает требования для опционов на ценные бумаги, т.к. они подчиняются правилам котирующей биржи согласно руководству SEC. Для опционов на счете, подпадающем под действие Reg.T, также действует методология расчета маржи, основанная на правилах, и в этом случае короткие позиции приравниваются к акциям, а для спредовых транзакций действуют облегченные требования маржи. Наконец, требования Reg. T не распространяются на позиции на определенных счетах маржевого портфеля.

Другая справочная информация

Основные понятия, связанные с маржей

Инструменты для управления и наблюдения за маржей

Определение покупательной способности

Как определить, заимствовали ли Вы средства у IB

Почему IBKR рассчитывает и создает отчет о маржинальных требованиях, когда я не занимаю средства?

Проверка влияния на плату за риск при предпросмотре ордера

IB дает владельцам счетов возможность проверить, какое влияние ордер окажет на прогнозируемую плату за риск. Эту функцию следует использовать перед отправкой ордера для определения изменений, необходимых, чтобы снизить или избежать такую плату.

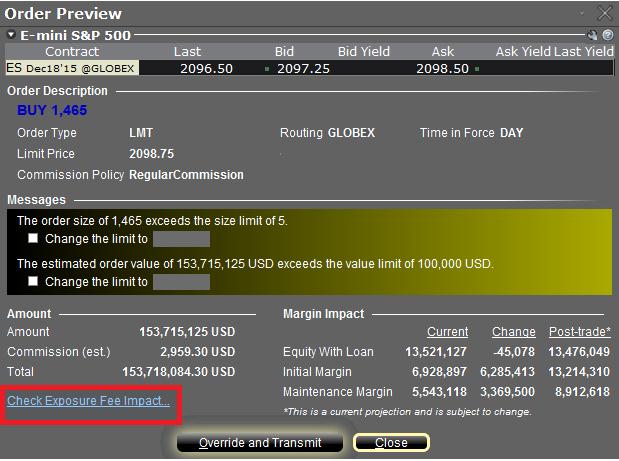

Для доступа к инструменту нужно открыть окно предварительного просмотра, щелкнув правой кнопкой мыши по строке ордера. В нем можно будет увидеть ссылку "Проверка влияния на плату за риск" (см. отмеченную красным область на Изображении 1).

Изображение 1

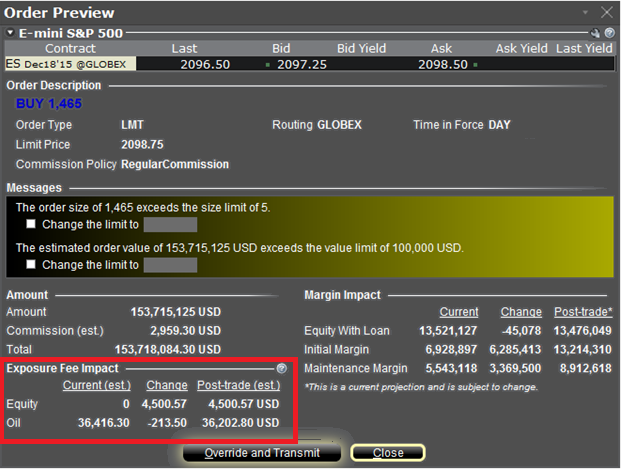

Щелкнув по ссылке, можно расширить окно и увидеть плату за риск (если она требуется), связанную с текущими позициями, ее изменение при исполнении данного ордера, а также конечную плату после исполнения (см. отмеченную красным область на Изображении 2). Дальнейшие показатели делятся по классам инструментов, подвергающимся упомянутой плате (напр. акции, нефть). Владелец счета может просто закрыть окно, не отправив ордер, если рост итоговой платы за риск покажется ему избыточным.

Изображение 2

Узнайте больше об управлении платой за риск и ее прогнозировании при помощи "Навигатора риска" IB в статье KB2275, а также об ее отслеживании в статье KB2344.

Использование "Навигатора риска" для прогноза платы за риск

В "Навигаторе риска" от IB имеется возможность создания пользовательских сценариев для определения того, как изменения в портфеле повлияют на Вашу плату за риск. Ниже описаны шаги по созданию портфеля “Что, если” путем внесения предполагаемых изменений в существующий портфель или создания нового гипотетического портфеля и определения итоговой платы. Данная функция доступна в TWS версии 951 и новее.

Шаг 1: Создайте новый портфель "Что, если"

Используя классическую раскладку торговой платформы TWS, в меню Аналитические инструменты выберите Навигатор риска и Открыть новый "Что, если" (Изображение 1).

Изображение 1

.jpg)

Шаг 2: Выберите тип портфеля

Вы увидите всплывающее окно (Изображение 2), где Вам потребуется уточнить, желаете ли Вы создать гипотетический портфель на основе своего текущего или же новый портфель. Если Вы нажмете "Да", в Ваш портфель "Что, если" будут загружены уже имеющиеся позиции.

Изображение 2

.png)

Ответ "Нет" приведет к открытию портфеля “Что, если” без позиций (Изображение 3). Выберите вкладку инструмента, по которому желаете создать гипотетические позиции (напр., "Капитал").

Изображение 3

.jpg)

Шаг 3: Добавьте позиции

Чтобы добавить позицию в портфель "Что, если" , щелкните по зеленой строке под названием "Новый" и введите символ андерлаинга (Изображение 4), укажите тип инструмента (Изображение 5) и количество (Изображение 6).

Изображение 4

.jpg)

Изображение 5

.jpg)

Изображение 6

.jpg)

Шаг 4: Определите плату за риск

Для просмотра платы за риск, прогнозируемой на основе вашего портфеля "Что, если", откройте меню Отчет и выберите Плата за риск (Изображение 7). Перед Вами откроется окно с прогнозируемой платой за риски, разделенной по классам инструментов (Изображение 8).

Изображение 7

.jpg)

Изображение 8

.jpg)

Отслеживание платы за риск в окне "Счет" описано в статье KB2344, а проверка ее суммы при помощи функции предпросмотра ордера - в статье KB2276.

Order Preview - Check Exposure Fee Impact

IB provides a feature which allows account holders to check what impact, if any, an order will have upon the projected Exposure Fee. The feature is intended to be used prior to submitting the order to provide advance notice as to the fee and allow for changes to be made to the order prior to submission in order to minimize or eliminate the fee.

The feature is enabled by right-clicking on the order line at which point the Order Preview window will open. This window will contain a link titled "Check Exposure Fee Impact" (see red highlighted box in Exhibit I below).

Exhibit I

Clicking the link will expand the window and display the Exposure fee, if any, associated with the current positions, the change in the fee were the order to be executed, and the total resultant fee upon order execution (see red highlighted box in Exhibit II below). These balances are further broken down by the product classification to which the fee applies (e.g. Equity, Oil). Account holders may simply close the window without transmitting the order if the fee impact is determined to be excessive.

Exhibit II

Please see KB2275 for information regarding the use of IB's Risk Navigator for managing and projecting the Exposure Fee and KB2344 for monitoring fees through the Account Window

Important Notes

1. The Estimated Next Exposure Fee is a projection based upon readily available information. As the fee calculation is based upon information (e.g., prices and implied volatility factors) available only after the close, the actual fee may differ from that of the projection.

2. The Check Exposure Fee Impact is only available for accounts that have been charged an exposure fee in the last 30 days

Using Risk Navigator to Project Exposure Fees

Overview:

IB's Risk Navigator provides a custom scenario feature which allows one to determine what effect, if any, changes to their portfolio will have to the Exposure fee. Outlined below are the steps for creating a “what-if” portfolio through assumed changes to an existing portfolio or through an entirely new proposed portfolio along with determining the resultant fee. Note that this feature is available through TWS build 971.0i and above.

Step 1: Open a new “What-if” portfolio

From the Classic TWS trading platform, select the Analytical Tools, Risk Navigator, and then Open New What-If menu options (Exhibit 1).

Exhibit 1

.png)

From the Mosaic TWS trading platform, select the New Window, Select Risk Navigator, and then Open New What-If menu options.

Step 2: Define starting portfolio

A pop-up window will appear (Exhibit 2) from which you will be prompted to define whether you would like to create a hypothetical portfolio starting from your current portfolio or a newly created portfolio. Clicking on the "yes" button will serve to download existing positions to the new “What-If” portfolio.

Exhibit 2

.png)

Clicking on the "No" button will open up the “What-If” Portfolio with no positions.

Step 3: Add Positions

To add a position to the “what-if” portfolio, click on the green row titled "New" and then enter the underlying symbol (Exhibit 3), define the product type (Exhibit 4) and enter position quantity (Exhibit 5).

Exhibit 3

.png)

Exhibit 4

.png)

Exhibit 5

.png)

You can modify the positions to see how that changes the margin. After you altered your positions you will need to click on the recalculate icon ( ) to the right of the margin numbers in order to have them update. Whenever that icon is present the margin numbers are not up-to-date with the content of the “what-if” Portfolio.

) to the right of the margin numbers in order to have them update. Whenever that icon is present the margin numbers are not up-to-date with the content of the “what-if” Portfolio.

Step 4: Determine Exposure Fee

To view the projected correlated exposure fee based upon your “what-if” portfolio, click on the Report and then Exposure Fee menu options (Exhibit 6). Once selected, a new Exposure Fee tab will be added, which will display the projected exposure fee broken down by primary risk factors (Exhibit 7).

Exhibit 6

.png)

Exhibit 7

.png)

You can modify the positions to see how that changes the Exposure Fee. After you altered your positions you will need to click on the refresh button to the right of the Last Calculation Time. Whenever the warning icon ( ) is present the Exposure Fee Calculations numbers are not up-to-date with the content of the “what-if” Portfolio.

) is present the Exposure Fee Calculations numbers are not up-to-date with the content of the “what-if” Portfolio.

Please see KB2344 for information on monitoring the Exposure fee through the Account Window and KB2276 for verifying exposure fee through the Order Preview screen.

Important Note

1. The on-demand Exposure Fee check represents a projection based upon readily available information. As the fee calculation is based upon information (e.g., prices and implied volatility factors) available only after the close, the actual fee may differ from that of the projection.

Overview of Margin Methodologies

Introduction

The methodology used to calculate the margin requirement for a given position is largely determined by the following three factors:

1. The product type;

2. The rules of the exchange on which the product is listed and/or the primary regulator of the carrying broker;

3. IBKR’s “house” requirements.

While a number of methodologies exist, they tend to be categorized into one of two approaches: rules based or risk based. Rules based methods generally assume uniform margin rates across like products, offer no inter-product offsets and consider derivative instruments in a manner similar to that of their underlying. In this sense, they offer ease of computation but oftentimes make assumptions which, while simple to execute, may overstate or understate the risk of an instrument relative to its historic performance. A common example of a rules based methodology is the U.S. based Reg. T requirement.

In contrast, risk based methodologies often seek to apply margin coverage reflective of the product’s past performance, recognize some inter-product offsets and seek to model the non-linear risk of derivative products using mathematical pricing models. These methodologies, while intuitive, involve computations which may not be easily replicable by the client. Moreover, to the extent that their inputs rely upon observed market behavior, may result in requirements that are subject to rapid and sizable fluctuation. Examples of risk based methodologies include TIMS and SPAN.

Regardless of whether the methodology is rules or risk based, most brokers will apply “house” margin requirements which serve to increase the statutory, or base, requirement in targeted instances where the broker’s view of exposure is greater than that which would satisfied solely by meeting that base requirement. An overview of the most common risk and rules based methodologies is provided below.

Methodology Overview

Risk Based

a. Portfolio Margin (TIMS) – The Theoretical Intermarket Margin System, or TIMS, is a risk based methodology created by the Options Clearing Corporation (OCC) which computes the value of the portfolio given a series of hypothetical market scenarios where price changes are assumed and positions revalued. The methodology uses an option pricing model to revalue options and the OCC scenarios are augmented by a number of house scenarios which serve to capture additional risks such as extreme market moves, concentrated positions and shifts in option implied volatilities. In addition, there are certain securities (e.g., Pink Sheet, OTCBB and low cap) for which margin may not be extended. Once the projected portfolio values are determined at each scenario, the one which projects the greatest loss is the margin requirement.

Positions to which the TIMS methodology is eligible to be applied include U.S. stocks, ETFs, options, single stock futures and Non U.S. stocks and options which meet the SEC’s ready market test.

As this methodology uses a much more complex set of computations than one that is rules based, it tends to more accurately model risk and generally offers greater leverage. Given its ability to offer enhanced leverage and that the requirements fluctuate and may react quickly to changing market conditions, it is intended for sophisticated individuals and requires minimum equity of $110,000 to initiate and $100,000 to maintain. Requirements for stocks under this methodology generally range from 15% to 30% with the more favorable requirement applied to portfolios which contain a highly diversified group of stocks which have historically exhibited low volatility and which tend to employ option hedges.

b. SPAN – Standard Portfolio Analysis of Risk, or SPAN, is a risk-based margin methodology created by the Chicago Mercantile Exchange (CME) that is designed for futures and future options. Similar to TIMS, SPAN determines a margin requirement by calculating the value of the portfolio given a set of hypothetical market scenarios where underlying price changes and option implied volatilities are assumed to change. Again, IBKR will include in these assumptions house scenarios which account for extreme price moves along with the particular impact such moves may have upon deep out-of-the-money options. The scenario which projects the greatest loss becomes the margin requirement. A detailed overview of the SPAN margining system is provided in KB563.

Rules Based

a. Reg. T – The U.S. central bank, the Federal Reserve Board, holds responsibility for maintaining the stability of the financial system and containing systemic risk that may arise in financial markets. It does this, in part, by governing the amount of credit that broker dealers may extend to customers who borrow money to buy securities on margin.

This is accomplished through Regulation T, or Reg. T as it is commonly referred, which provides for establishment of a margin account and which imposes the initial margin requirement and payment rules on certain securities transactions. For example, on stock purchases, Reg. T currently requires an initial margin deposit by the client equal to 50% of the purchase value, allowing the broker to extend credit or finance the remaining 50%. For example, an account holder purchasing $1,000 worth of securities is required to deposit $500 and allowed to borrow $500 to hold those securities.

Reg. T only establishes the initial margin requirement and the maintenance requirement, the amount necessary to continue holding the position once initiated, is set by exchange rule (25% for stocks). Reg. T also does not establish margin requirements for securities options as this falls under the jurisdiction of the listing exchange’s rules which are subject to SEC approval. Options held in a Reg.T account are also subject to a rules based methodology where short positions are treated like a stock equivalent and margin relief is provided for spread transactions. Finally, positions held in a qualifying portfolio margin account are exempt from the requirements of Reg. T.

Where to Learn More

Tools provided to monitor and manage margin

How to determine if you are borrowing funds from IBKR

Why does IBKR calculate and report a margin requirement when I am not borrowing funds?

Margin Requirement on Leveraged ETF Products

Leveraged Exchange Traded Funds (ETFs) are a subset of general ETFs and are intended to generate performance in multiples of that of the underlying index or benchmark (e.g. 200%, 300% or greater). In addition, some of these ETFs seek to generate performance which is not only a multiple of, but also the inverse of the underlying index or benchmark (e.g., a short ETF). To accomplish this, these leveraged funds typically include among their holdings derivative instruments such as options, futures or swaps which are intended to provide the desired leverage and/or inverse performance.

Exchange margin rules seek to recognize the additional leverage and risk associated with these instruments by establishing a margin rate which is commensurate with that level of leverage (but not to exceed 100% of the ETF value). Thus, for example, whereas the base strategy-based maintenance margin requirement for a non-leveraged long ETF is set at 25% and a short non-leveraged ETF at 30%, examples of the maintenance margin change for leveraged ETFs are as follows:

1. Long an ETF having a 200% leverage factor: 50% (= 2 x 25%)

2. Short an ETF having a 300% leverage factor: 90% (= 3 x 30%)

A similar scaling in margin is also in effect for options. For example, the Reg. T maintenance margin requirement for a non-leveraged, short broad based ETF index option is 100% of the option premium plus 15% of the ETF market value, less any out-of-the-money amount (to a minimum of 10% of ETF market value in the case of calls and 10% of the option strike price in the case of puts). In the case where the option underlying is a leveraged ETF, however, the 15% rate is increased by the leverage factor of the ETF.

In the case of portfolio margin accounts, the effect is similar, with the scan ranges by which the leveraged ETF positions are stress tested increasing by the ETF leverage factor. See NASD Rule 2520 and NYSE Rule 431 for further details.

What happens if the net liquidating equity in my Portfolio Margining account falls below USD 100,000?

Overview:

Portfolio Margining accounts reporting net liquidating equity below USD 100,000 are limited to entering trades which serve solely to reduce the margin requirement until such time as either: 1) the equity increases to above 100,000 or 2) the account holder requests a downgrade to Reg T style margining through Client Portal (select the Settings, Account Settings, Configure and Account Type menu options).

If a Portfolio Margining eligible account reporting net liquidating equity below USD 100,000 enters an order which, if executed, would serve to increase the margin requirement, the following TWS message will be displayed: "Your order is not accepted, margin requirement increase not allowed. Equity with loan value is less than 100,000.00 USD."

IMPORTANT NOTICE

Please note that requests to downgrade to Reg. T will become effective the following business day if submitted prior to 4:00 ET. Also note that as the Reg. T margining methodology generally affords less leverage than does Portfolio Margining, requesting a downgrade may lead to the automatic liquidation of positions in your account in order to comply with Reg. T. You will receive a warning message if that is the case at the time you request the downgrade.

-->

What positions are eligible for Portfolio Margining?

Overview:

Portfolio Margining is eligible for US securities positions including stocks, ETFs, stock and index options and single stock futures. It does not apply to US futures or futures options positions or non-US stocks, which may already be margined using an exchange approved risk based margining methodology.