Devo finanziare il mio conto prima che venga approvato?

Coloro che abbiano fatto richiesta di aprire un conto dovranno fornire a IBKR una notifica nella quale si specifica l’importo e la maniera con la quale intendono finanziare il proprio conto con l’obiettivo di vedere approvata la richiesta. Non vi è tuttavia un requisito circa l’obbligo di finanziare il fondo prima dell’approvazione.

Ciononostante i richiedenti potranno inviare fondi tramite bonifico, assegno o con un trasferimento di fondi elettronico (es. ACH, EFT) prima di aver ricevuto la conferma di approvazione del loro conto. In questo modo sarà possibile accelerare l’inizio di qualsiasi periodo di detenzione del credito. Va ricordato tuttavia che i versamenti ricevuti prima dell’approvazione del conto saranno tenuti in sospeso e non verranno accreditati sul conto né saranno idonei per la maturazione di interessi fino a quando il conto non sarà stato approvato. Nel caso in cui il richiedente abbia autorizzato IBKR a finanziare il conto tramite il trasferimento di asset (es. ACAT, ATON) provenienti da un altro broker, IBKR non avvierà il trasferimento fino a quando la richiesta non sarà stata approvata.

È possibile avere un conto cointestato con più di due persone fisiche?

IB offre tre tipi di conti cointestati: “Comunione con diritto di reversibilità”, “Comunione pro indiviso” e infine “Comunione dei beni”. Ciascuno di questi tipi di conto cointestato è disponibile solamente per due titolari di conto.

I richiedenti interessati ad aprire un conto con più titolari (ovvero più di due) potranno prendere in considerazione l’ipotesi di forme quali la società, la partnership, la LLC (limited liability company) o anche altre strutture legali diverse dalla società costituite disponibili presso IB. Ti ricordiamo che in genere la documentazione per dimostrare la costituzione di una società viene richiesta nel momento in cui si compila la richiesta di apertura di un conto.

Come posso fare per sapere a che punto è la mia richiesta di apertura del conto?

Vai su IBKR.com/app-status per accedere e controllare lo status della tua richiesta di apertura del conto.

Per velocizzare la procedura di verifica, ti invitiamo a seguire le seguenti raccomandazioni:

- Finanzia la tua richiesta di applicazione in modo da rendere prioritaria la verifica. Se per qualunque motivo la tua richiesta non verrà approvata, i fondi saranno tempestivamente restituiti.

- Accedi e verifica di aver inviato tutta la documentazione necessaria. Spesso il motivo più comune di possibili ritardi è proprio la mancanza di uno o più documenti richiesti.

- Per verificare eventuali aggiornamenti dal nostro team di Compliance, controlla regolarmente i messaggi dell’indirizzo di posta elettronica che hai fornito nella tua richiesta. Il team potrà contattarti tramite email nel caso in cui sia necessario inviare ulteriori documenti e/o ulteriori chiarimenti una volta che la parte online della tua richiesta sia stata completata.

- Una volta che tutta la documentazione sarà stata inviata e accettata, ti preghiamo di far trascorrere del tempo in modo che vengano completate le verifiche di due diligence e si concluda la procedura di controllo della tua richiesta di apertura del conto.

Quale entità di IBKR gestisce il mio conto?

I titolari dei conti potranno confermare l’entità di IBKR presso la quale viene gestito il loro conto dopo aver controllato con cura le informazioni riportate in testa al loro Resoconto delle attività.

Interactive Brokers Group Inc. opera attraverso una serie di broker sussidiari come descritto qui in basso. L’entità di IBKR attraverso la quale viene gestito un conto dipende dal paese presso la quale il titolare ha la residenza legale; oppure, nel caso in cui si tratti di una società, l'entità verrà stabilita in base al paese nel quale è stata costituita la società. Ti ricordiamo che alcune entità mantengono relazioni con le altre allo scopo di fornire servizi quali ad esempio la compensazione e l’esecuzione. Tali informazioni sono contenute nel Contratto Clienti.

- Interactive Brokers LLC (IB LLC)

- Interactive Brokers Canada Inc (IBC)

- Interactive Brokers (U.K.) Limited (IBUK)

- Interactive Brokers Ireland Limited (IBIE)

- Interactive Brokers Central Europe Zrt. (IBCE)

- Interactive Brokers Luxembourg SARL (IBLUX)

- Interactive Brokers Australia Pty. Ltd. (IBA)

- Interactive Brokers Hong Kong Limited (IBHK)

- Interactive Brokers (India) Pvt. Ltd. (IBI)

- Interactive Brokers Securities Japan, Inc. (IBSJ)

- Interactive Brokers Singapore Pte. Ltd. (IBSG)

Perché mi viene chiesto di dichiarare il mio rapporto di lavoro con un'istituzione finanziaria?

La regola FINRA 3210 stabilisce che i soggetti richiedenti associate con una società membro del FINRA (i cosiddetti “Membri datori di lavoro”) ottengano il consenso scritto del “Membro datore di lavoro” prima di aprire un conto presso IBKR (“Membro esecutore”). La regola richiede inoltre che le persone interessate diano notifica a IBKR circa il loro legame con il “Membro datore di lavoro”. IBKR potrebbe essere soggetta a regole simili anche al di fuori degli Stati Uniti.

Ai soggetti richiedenti che risultano essere dipendenti o affiliati con un altro broker o un’istituzione finanziaria potrà venir chiesto di inviare documentazione contenente i contatti del loro datore di lavoro. In questo modo IBKR sarà in grado di fornire informazioni relative alle transazioni qualora il datore di lavoro ne faccia richiesta. Nel caso in cui il soggetto richiedente sia dipendente di un’istituzione finanziaria e non abbia inviato alcun documento, IBKR avrà la facoltà di contattare il richiedente per confermare che la Regola FINRA 3210 non si applica al suo caso.

Come inviare documenti a IBKR grazie al tuo smartphone

Overview:

Interactive Brokers ti consente di inviarci una copia di un documento anche se non hai al momento uno scanner. Puoi scattare una foto del documento richiesto semplicemente utilizzando il tuo smartphone.

Qui di seguito troverai le istruzioni su come scattare una foto e inviarla tramite e-mail a Interactive Brokers per i seguenti sistemi operativi su smartphone:

Se sai già come scattare e inviare foto tramite e-mail con il tuo smartphone, ti invitiamo a cliccare QUI – Dove inviare l’e-mail e cosa inserire nel campo oggetto.

iOS

1. Dal fondo dello schermo del tuo smartphone scorri verso l’alto e seleziona l’icona della fotocamera.

Se non hai l’icona della Fotocamera, tocca l’icona dell’app Fotocamera presente sulla schermata Home del tuo iPhone.

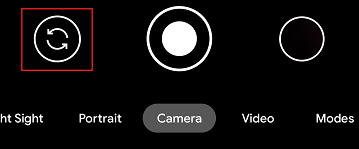

In genere il tuo telefono dovrebbe attivare la fotocamera posteriore. Se si attiva quella anteriore, ti basterà toccare il pulsante cerchiato in rosso nell’immagine qui sotto.

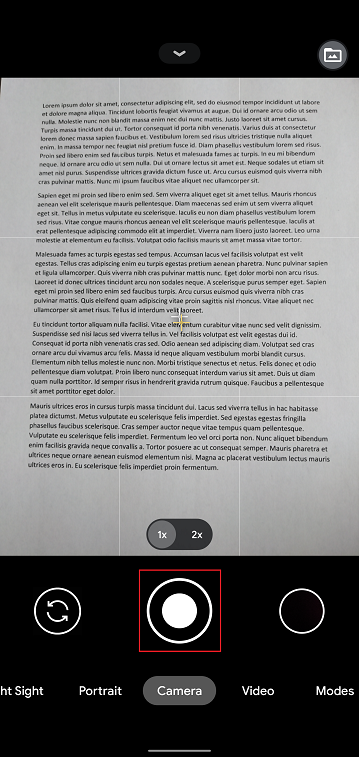

2. Disponi l’iPhone sopra il documento e inquadra una porzione o una pagina intera.

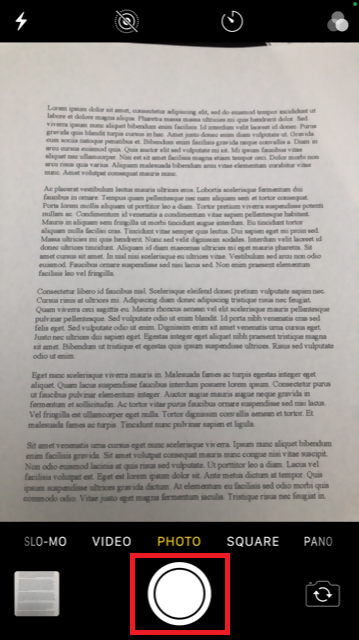

3. Assicurati che la luce sia uniforme e basti a illuminare il testo. Fai in modo che non ci siano ombre sul documento per via della tua posizione. Reggi lo smartphone in maniera decisa evitando scosse o tremolii. Tocca il pulsante dell’otturatore per scattare la foto.

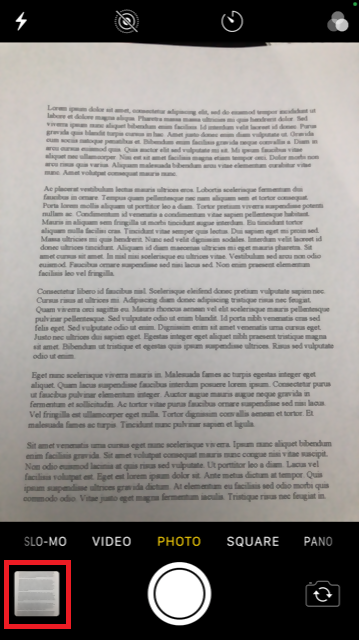

4. Tocca la miniatura della foto nell’angolo in basso a sinistra per visualizzare a schermo intero la foto che hai appena scattato.

5. Assicurati che la foto sia chiara e che il documento sia leggibile. Puoi ingrandire la foto e vedere nel dettaglio l’immagine facendo scorrere le due dita come mostrato nell’immagine qui sotto.

Se la foto non è di buona qualità oppure non c'è abbastanza luce, ripeti i passaggi precedenti per scattare una foto migliore.

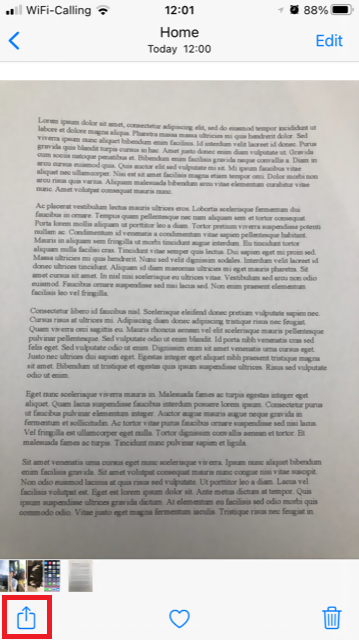

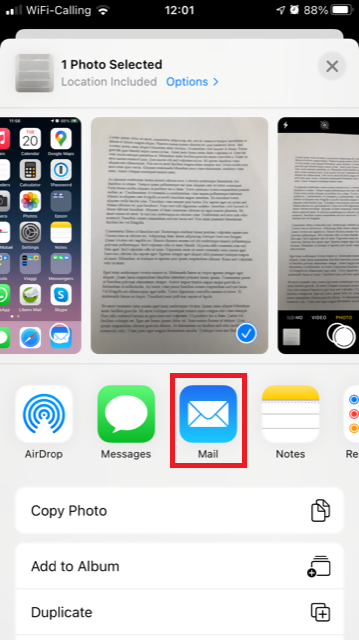

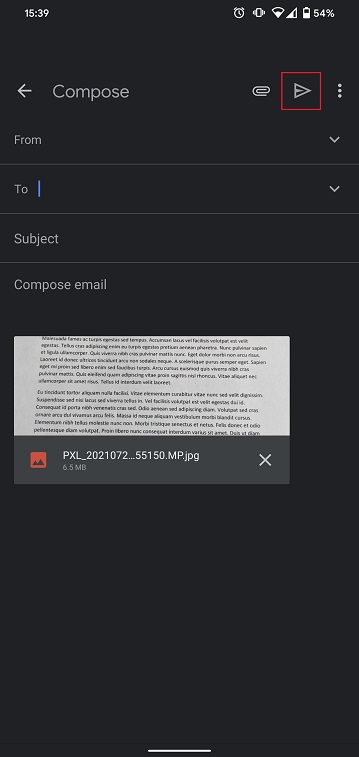

6. Tocca l’icona di condivisione nell’angolo in basso a sinistra dello schermo.

7. Tocca l’icona della posta elettronica.

Nota bene: per inviare e-mail il tuo telefono deve essere configurato per questo scopo. Ti invitiamo a contattare il tuo e-mail provider se non hai familiarità con questa procedura.

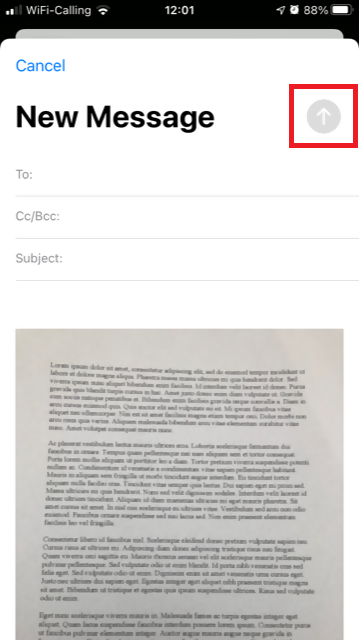

8. Ti invitiamo a leggere QUI per vedere come compilare i campi A: e Oggetto: della tua e-mail. Una volta completata l’e-mail, tocca l’icona della freccia in alto a destra per l’invio.

Android

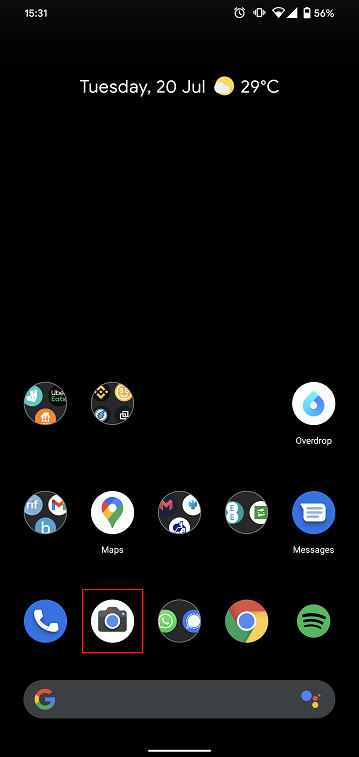

1. Apri la lista delle applicazioni e avvia l’app Fotocamera. In alternativa puoi accedervi dalla tua schermata Home. L’applicazione potrebbe avere un nome diverso a seconda del modello di telefono, della marca o delle impostazioni.

In genere il tuo telefono dovrebbe attivare la fotocamera posteriore. Se si attiva quella anteriore, ti basterà toccare il pulsante cerchiato in rosso nell’immagine qui sotto.

2. Disponi il tuo dispositivo Android sopra il documento e inquadra una porzione o una pagina intera.

3. Assicurati che la luce sia uniforme e basti a illuminare il testo. Fai in modo che non ci siano ombre sul documento per via della tua posizione. Reggi lo smartphone in maniera decisa evitando scosse o tremolii. Tocca il pulsante dell’otturatore per scattare la foto.

4. Assicurati che la foto sia chiara e che il documento sia leggibile. Puoi ingrandire la foto e vedere nel dettaglio l’immagine facendo scorrere le due dita come mostrato nell’immagine qui sotto.

Se la foto non è di buona qualità oppure la luce non basta, ripeti i passaggi precedenti per scattare una foto migliore.

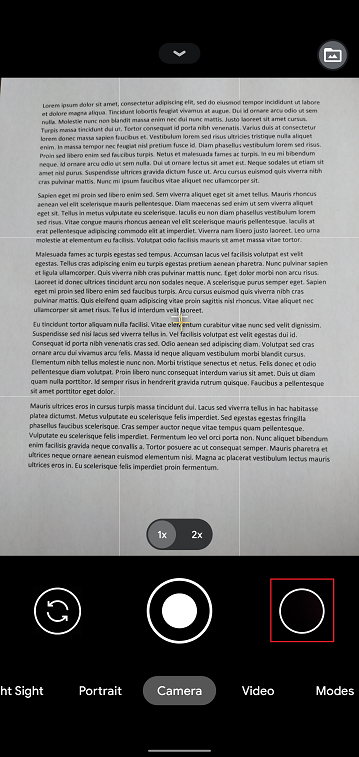

5. Tocca l’icona del cerchio vuoto nell’angolo in basso a destra dello schermo.

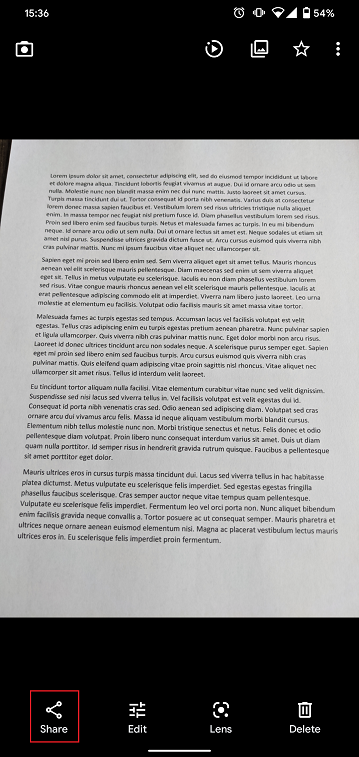

6. Tocca l’icona di condivisione nell’angolo in basso a sinistra dello schermo.

7. Nel menu di condivisione tocca l’icona del servizio e-mail impostato sul tuo telefono. Nell’esempio qui in basso viene selezionata Gmail, ma il nome potrebbe variare in base alle impostazioni del tuo smartphone.

.png)

Nota bene: per inviare e-mail il tuo telefono deve essere configurato per questo scopo. Ti invitiamo a contattare il tuo e-mail provider se non hai familiarità con questa procedura.

8. Ti invitiamo a leggere QUI per vedere come compilare i campi "A" e "Oggetto" della tua e-mail. Una volta completata l'e-mail, tocca l’icona della freccia in alto a destra per l’invio.

DOVE INVIARE L’E-MAIL E COSA INSERIRE NEL CAMPO OGGETTO

L’e-mail deve essere scritta rispettando le seguenti istruzioni:

1. Nel campo "A:" bisogna inserire quanto segue:

- newaccounts@interactivebrokers.com se hai la residenza in un Paese al di fuori del continente europeo

- newaccounts.uk@interactivebrokers.co.uk se hai la residenza in un Paese europeo

2. Il campo dell' Oggetto:deve contenere tutte le seguenti informazioni:

- Il tuo numero di conto (in genere nel formato Uxxxxxxx, dove a ogni x corrisponde un numero) oppure il tuo nome utente.

- Il motivo per il quale hai inviato il documento. Ti invitiamo a utilizzare i seguenti acronimi a seconda dei casi:

- PoRes per un documento comprovante il tuo indirizzo di residenza

- PID per un documento comprovante l’identità

Panoramica su oneri e commissioni

I clienti e i potenziali clienti sono invitati a visitare il nostro sito web dove troveranno descrizioni dettagliate riguardo oneri e commissioni.

In questa pagina vengono illustrati gli oneri e le commissioni più comuni:

1. Commissioni - Le commissioni variano a seconda del tipo di prodotto, della borsa valori e dipendono anche dal tipo di piano tariffario scelto (tutto incluso oppure no). Nel caso dei titoli statunitensi, applichiamo una commissione pari a 0.0005 USD per azione con un trading minimo di 1.00 USD.

2. Interessi - Gli interessi vengono applicati sui saldi di debito relativo ai margini e IBKR utilizza dei benchmark riconosciuti a livello internazionale per i versamenti overnight come base per stabilire i tassi d’interesse. Successivamente applichiamo un differenziale per il tasso d’interesse benchmark (“BM”) in scaglioni degressivi; in questo modo i saldi relativi a grandi quantità di liquidi riceveranno – in maniera proporzionale – tassi migliori e sarà possibile stabilire un tasso effettivo. Per esempio: nel caso di prestiti denominati in USD, il tasso di riferimento (benchmark) sarà quello della Fed Funds e si applicherà uno spread del 1.5% per i saldi fino a 100,000 USD. Inoltre i soggetti che vogliono vendere titoli short devono essere al corrente dell’esistenza di oneri speciali in termini di interessi nel caso in cui i titoli presi in prestito per coprire la vendita di titoli short siano considerati “difficili da ottenere in prestito”.

3. Oneri di cambio - Anche questa tipologia varia in base al tipo di prodotto e alla borsa valori. Per esempio: nel caso di opzioni su titoli USA, alcune borse valori applicano un onere nel caso di rimozione della liquidità (ordine al meglio oppure un ordine con limite di prezzo marketable) e forniscono pagamenti per ordini che aggiungono liquidità (ordine con limite). Inoltre diverse borse applicano degli oneri su ordini che vengono cancellati o modificati.

4. Dati di mercato - L’iscrizione ai dati di mercato non è obbligatoria, tuttavia nel caso in cui tu abbia chiesto questo servizio, potrai vedere applicato un onere mensile in base al tipo di borsa valori scelto e alla loro offerta di abbonamento. Tramite il nostro strumento, l’Assistente per i Dati di mercato, ti offriamo assistenza nel selezionare gli abbonamenti ai dati di mercato sulla base dei prodotti che vuoi usare per la tua attività di trading. Per accedere a questo strumento ti basterà entrare nel Portale Clienti, cliccare nella sezione Assistenza e selezionare il link per l’Assistente per i Dati di mercato.

5. Onere sull’attività minima mensile - Dato che offriamo servizi per trader attivi, richiediamo a nostri clienti di avere dei conti che generino un minimo di commissioni ogni mese altrimenti verrà applicato un onere sulla differenza tra commissioni generate e il minimo stabilito. Il minimo è di 10 USD mensili.

6. Varie - IBKR consente un prelievo mensile gratuito e applica un onere per ogni prelievo successivo. Inoltre ci sono alcuni oneri relativi alle richieste di trade bust, per l’esercizio di opzioni e/o future & assegnazioni e infine commissioni di custodia sugli ADR (American Depositary Receipt).

Per maggiori informazioni, ti consigliamo di visitare il nostro sito web e selezionare una delle opzioni disponibili nel menu dedicato ai Prezzi.

Verifica del numero di telefono cellulare durante la procedura di apertura del conto

Introduzione

IB richiede ai clienti di verificare il loro numero di telefono cellulare in modo da poter ricevere in maniera diretta – tramite SMS – comunicazioni relative al loro conto e alle attività di trading. I clienti che non avranno modo di verificare il proprio telefono saranno soggetti a delle limitazioni per quanto riguarda il trading per tutta la durata di questa procedura. La verifica viene eseguita online e i passaggi per completarla sono illustrati in questo articolo.

Nel caso in cui il tuo conto sia già stato aperto ma il tuo numero di telefono non è stato verificato, vai direttamente all’articolo KB2552 per completare la procedura di verifica.

Verifica del telefono

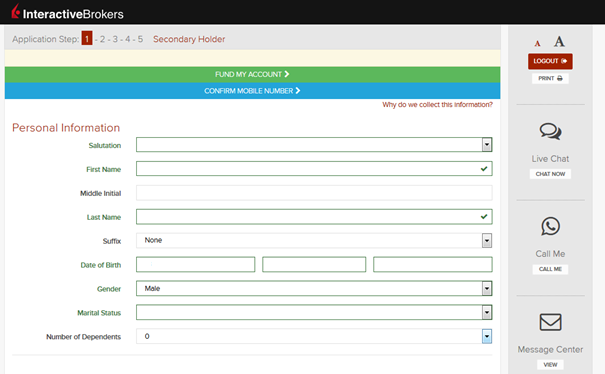

Quando stai completando la tua Richiesta di Apertura di conto presso Interactive Brokers, vedrai una barra blu nella parte alta della pagina che riporta la seguente dicitura "CONFERMA IL NUMERO DI CELLULARE".

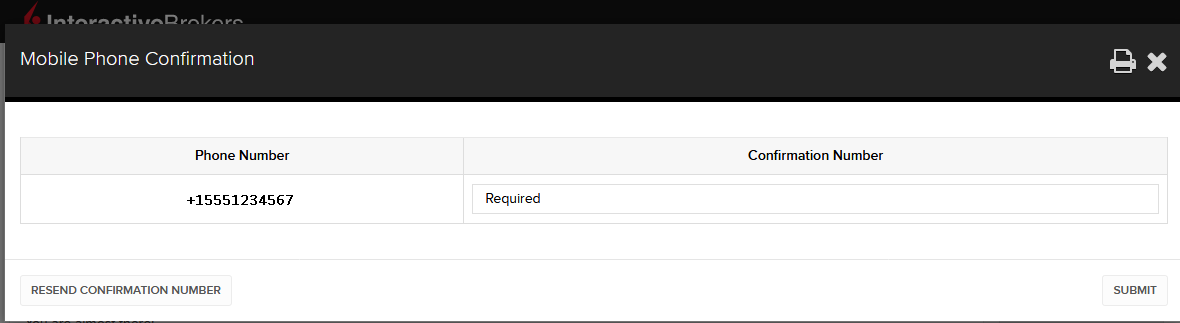

In qualunque momento puoi cliccare su quella barra durante i passaggi 1-4. Dopo aver cliccato vedrai comparire questa finestra:

Una volta che avrai inserito il tuo numero per intero, questo verrà riconosciuto dal sistema e ti verrà inviato subito un messaggio di conferma. Convalida il tuo numero di telefono inserendo il Codice SMS che hai ricevuto nel campo del Codice di Conferma, quindi clicca su Invio.

Nel caso in cui non ti sia possibile fare questo durante la procedura di apertura del conto, potrai sempre confermare il numero attraverso la pagina di Stato della Richiesta.

.png)

Ti ricordiamo che alcune delle seguenti restrizioni potrebbero essere attive:

- I messaggi SMS potrebbero essere bloccati se nel tuo Paese partecipi al registro nazionale per non ricevere chiamate indesiderate come quelle fatte per indagini di mercato o telemarketing (acronimo inglese NDNC).

- Mittenti che inviano numeri/codici potrebbero essere bloccati in modo da prevenire potenziali frodi.

- Alcuni gestori di telefonia mobile potrebbero limitare gli orari di ricezione dei messaggi SMS.

Non ricevo i messaggi di testo (SMS) inviati da IBKR sul mio telefono cellulare

Background:

Una volta che il numero del tuo telefono cellulare sarà stato verificato nel Portale Clienti, dovresti essere subito in grado di ricevere messaggi di testo (SMS) inviati da IBKR direttamente sul tuo telefono. Questo articolo fornisce alcuni passi semplici per rilevare possibili errori nel caso in cui non sia possibile ricevere questi messaggi.

1. Attiva l’Autenticazione di IBKR Mobile (IB-KEY) tramite il dispositivo di sicurezza a 2 livelli.

Per evitare di avere problemi legati al telefono oppure agli operatori di rete mobile e allo scopo di ricevere messaggi da IBKR in maniera regolare, ti consigliamo di attivare il sistema di Autenticazione di IBKR Mobile (IB Key) sul tuo smartphone.

L’autenticazione dello smartphone tramite la IB Key fornita dalla nostra app IBKR Mobile funziona come dispositivo di sicurezza a 2 livelli, eliminando quindi il bisogno di ricevere codici di autenticazione tramite SMS quando accedi al tuo conto IBKR.

La nostra app IBKR Mobile è attualmente supportata dagli smartphone che hanno i sistemi operativi Android e iOS L’installazione, l’attivazione e le istruzioni per il funzionamento sono disponibili qui:

2. Riavvia il tuo telefono:

Spegni completamente il tuo telefono portatile per poi accenderlo nuovamente. Di solito questo basterà per iniziare a ricevere i messaggi di testo.

Ti segnaliamo che in alcuni casi, ad esempio nel caso in cui la copertura dell’operatore di telefonia mobile non sia quella tradizionale (quando si è all’estero), potresti non ricevere tutti i messaggi.

3. Usa l’opzione Chiamata vocale

Se non hai ricevuto il codice di accesso per l’autenticazione dopo aver riavviato il tuo telefono, potrai selezionare l’opzione “Voce”. Quindi riceverai il codice di autenticazione per l'accesso attraverso una chiamata automatica. Per maggiori istruzioni su come usare l’opzione Chiamata vocale sono contenute nel seguente articolo: IBKB 3396.

4. Verifica che il tuo operatore di telefonia mobile non stia bloccando la ricezione di SMS inviati da IBKR

Alcuni gestori di telefonia mobile bloccano automaticamente i messaggi di testo di IBKR in quanto li considerano erroneamente come messaggi spam o contenuti non richiesti. In base alla tua area geografica, in questa sezione troverai i servizi ai quali potrai rivolgerti per verificare se è stato applicato un filtro SMS al tuo numero di telefono:

Negli Stati Uniti:

- Tutti i gestori: Federal Trade Commission Registry

- T-Mobile: Le impostazioni per il blocco dei messaggi sono disponibili sul sito web di T-Mobile oppure direttamente sull’app T-Mobile.

In India:

- Tutti i gestori: Telecom Regulatory Authority of India

In China:

- Chiama direttamente il tuo gestore di telefonia mobile per sapere se utilizzano dei filtri per bloccare i messaggi di IBKR.

Riferimenti:

- Come accedere utilizzando l'autenticazione tramite SMS

- Panoramica del Sistema di Accesso Sicuro

- Informazioni e procedure relative ai dispositivi di sicurezza

- Autenticazione con IBKR Mobile

Requisiti di sistema per i colloqui tramite FaceKom

In base a quanto stabilito dalle normative del settore, Interactive Brokers Central Europe ZRt ("IBCE") ha l’obbligo di confermare l’identità di coloro che abbiano effettuato una richiesta di apertura conto. Tale verifica avviene tramite un colloquio realizzato tramite video. Nello specifico i colloqui vengono svolti grazie ad un sistema remoto di identificazione del cliente offerto da FaceKom. I requisiti minimi di sistema necessari per partecipare ad un colloquio video con IBCE sono i seguenti:

- PC, laptop oppure dispositivi mobili: Android OS versione 4 e successive con il browser Chrome, oppure Android 5 e versioni successive con Chrome come browser ufficiale, iOS Safari versione 11 e successive.

- Browser supportati per PC e laptop: Google Chrome v44 o successive, Mozilla Firefox v39 e successive, Opera (dal 2018), Microsoft Edge 15+ Safari 11.

- Requisiti hardware: processore Intel Core i3, i5, oppure i7 (AMD o equivalente); RAM: minimo 2GB. Si raccomanda una videocamera HD (720p).