Determining Buying Power

Buying power serves as a measurement of the dollar value of securities that one may purchase in a securities account without depositing additional funds. In the case of a cash account where, by definition, securities may not be purchased using funds borrowed from the broker and must be paid for in full, buying power is equal to the amount of settled cash on hand. Here, for example, an account holding $10,000 in cash may purchase up to $10,000 in stock.

In a margin account, buying power is increased through the use of leverage provided by the broker using cash as well as the value of stocks already held in the account as collateral. The amount of leverage depends upon whether the account is approved for Reg. T margin or Portfolio Margin. Here, a Reg. T account holding $10,000 in cash may purchase and hold overnight $20,000 in securities as Reg. T imposes an initial margin requirement of 50%, which translates to buying power of 2:1 (i.e., 1/.50). Similarly, a Reg. T account holding $10,000 in cash may purchase and hold on an intra-day basis $40,000 in securities given IB’s default intra-day maintenance margin requirement of 25%, which translates to buying power of 4:1 (i.e., 1/.25).

In the case of a Portfolio Margin account, greater leverage is available although, as the name suggests, the amount is highly dependent upon the make-up of the portfolio. Here, the requirement on individual stocks (initial = maintenance) generally ranges from 15% - 30%, translating to buying power of between 6.67 – 3.33:1. As the margin rate under this methodology can change daily as it considers risk factors such as the observed volatility of each stock and concentration, portfolios comprised of low-volatility stocks and which are diversified in nature tend to receive the most favorable margin treatment (e.g., higher buying power).

In addition to the cash examples above, buying power may be provided to securities held in the margin account, with the leverage dependent upon the loan value of the securities and the amount of funds, if any, borrowed to purchase them. Take, for example, an account which holds $10,000 in securities which are fully paid (i.e., no margin loan). Using the Reg. T initial margin requirement of 50%, these securities would have a loan value of $5,000 (= $10,000 * (1 - 0.50)) which, using that same initial requirement providing buying power of 2:1, could be applied to purchase and hold overnight an additional $10,000 of securities. Similarly, an account holding $10,000 in securities and a $1,000 margin loan (i.e., net liquidating equity of $9,000), has a remaining equity loan value of $4,000 which could be applied to purchase and hold overnight an additional $8,000 of securities. The same principles would hold true in a Portfolio Margin account, albeit with a potentially different level of buying power.

Finally, while the concept of buying power applies to the purchase of assets such as stocks, bonds, funds and forex, it does not translate in the same manner to derivatives. Most securities derivatives (e.g., short options and single stock futures) are not assets but rather contingent liabilities and long options, while an asset, are short-term in nature, considered a wasting asset and therefore generally have no loan value. The margin requirement on short options, therefore, is not based upon a percentage of the option premium value, but rather determined on the underlying stock as if the option were assigned (under Reg. T) or by estimating the cost to repurchase the option given adverse market changes (under Portfolio Margining).

Determining Tick Value

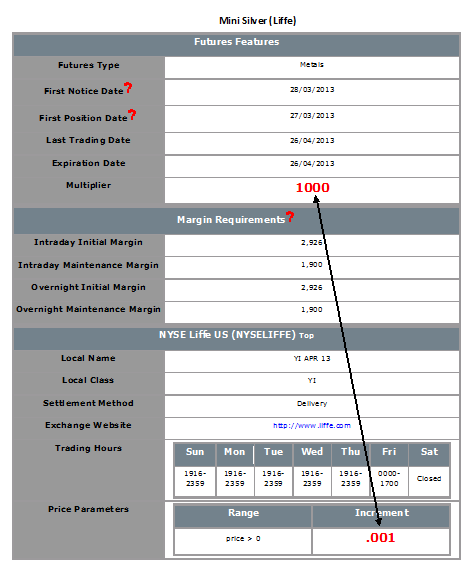

Financial instruments are subject to minimum price changes or increments which are commonly referred to as ticks. Tick values vary by instrument and are determined by the listing exchange. IB provides this information directly from the Contract Search tool on the website or via the Trader Workstation (TWS). To access from TWS, enter a symbol on the quote line, right click and from the drop-down window select the Contract Info and then Details menu options. The contract specifications window for the instrument will then be displayed (Exhibit 1).

To determine the notional value of a tick, multiple the tick increment by the contract trade unit or multiplier. As illustrated in the example below, the LIFFE Mini Silver futures contact has a tick value or minimum increment of .001 which, when multiplied by the contract multiplier of 1,000 ounces, results in a minimum tick value of $1.00 per contract. Accordingly, every tick change up or down results in a profit or loss of $1.00 per LIFFE Mini Silver futures contract.

Exhibit 1

SPY - Dividend Recognition

Unlike the case of a stock, in which a dividend is taxable in the year in which it is paid, the SPDR S&P 500 ETF Trust (Symbol: SPY) represents itself as a Regulated Investment Company and its dividend is deemed taxable in the year in which the record date is determined. As such, SPY dividends declared in either October, November or December and payable to shareholders of record on a specified date in one of those months will be considered taxable income income in that year despite the fact that such dividend will generally be paid in January of the following year.

Circular 230 Notice: These statements are provided for information purposes only, are not intended to constitute tax advice which may be relied upon to avoid penalties under any federal, state, local or other tax statutes or regulations, and do not resolve any tax issues in your favor.

Margin Treatment for Foreign Stocks Carried by a U.S. Broker

As a U.S. broker-dealer registered with the Securities & Exchange Commission (SEC) for the purpose of facilitating customer securities transactions, IB LLC is subject to various regulations relating to the extension of credit and margining of those transactions. In the case of foreign equity securities (i.e., non-U.S. issuer), Reg T. allows a U.S. broker to extend margin credit to those which either appear on the Federal Reserve Board's periodically published List of Foreign Margin Stocks, or are deemed to have a have a "ready market" under SEC Rule 15c3-1 or SEC no-action letter.

Prior to November 2012, "ready market" was deemed to include equity securities of a foreign issuer that are listed on what is now known as the FTSE World Index. This definition was based upon a 1993 SEC no-action letter and was premised upon the fact that, while there may not have been a ready market for such securities within the U.S., the securities could be readily resold in the applicable foreign market. In November of 2012, the SEC issued a follow-up no-action letter (www.sec.gov/divisions/marketreg/mr-noaction/2012/finra-112812.pdf) which expanded the population of foreign equity securities deemed to have a ready market to also include those not listed on the FTSE World Index provided that the following four conditions are met:

1. The security is listed on a foreign exchange located within a FTSE World Index recognized country, where the security has been trading on the exchange for at least 90 days;

2. Daily bid, ask and last quotations for the security as provided by the foreign listing exchange are made continuously available to the U.S. broker through an electronic quote system;

3. The median daily trading volume calculated over the preceding 20 business day period of the security on its listing exchange is either at least 100,000 shares or $500,000 (excluding shares purchased by the computing broker);

4. The aggregate unrestricted market capitalization in shares of the security exceed $500 million over each of the preceding 10 business days.

Note: if a security previously meeting the above conditions no longer does so, the broker is provided with a 5 business day window after which time the security will no longer be deemed readily marketable and must be treated as non-marginable.

Foreign equity securities which do not meet the above conditions, will be treated as non-marginable and will therefore have no loan value. Note that for purposes of this no-action letter foreign equity securities do not include options.

Aperçu des CFD sur actions émis par IB

L’article qui suit constitue une introduction générale aux CFD (contrat sur différence) sur actions émis par IBKR.

Pour des informations concernant les CFD sur indices IBKR, cliquez ici. Pour les CFD sur Forex, cliquez ici.

Table des matières :

I. Définition d'un CFD

II. Comparaison entre les CFD et les actions sous-jacentes

III. Coûts et marge

IV. Exemples

V. Ressources

VI. Foire aux questions

Avertissement concernant les risques

Les CFD sont des instruments complexes associés à un risque élevé de perte financière rapide en raison de l'effet de levier.

67% des comptes d'investisseurs de détail perdent de l'argent lorsqu'ils tradent des CFD avec IBKR (UK).

Vous devez vous assurer que vous comprenez la manière dont fonctionnent les CFD et que vous pouvez vous permettre de courir un risque élevé de perdre de l'argent.

Règles ESMA relatives aux CFD (Pour les clients de détail uniquement)

L'Autorité européenne des marchés financiers (ESMA) a édicté de nouvelles règles relatives aux CFD qui entreront en vigueur à compter du 1er août 2018.

Les règles consistent en: 1) des limites sur les effets de levier à l'ouverture de positions de CFD; 2) une règle de clôture des positions ouvertes par compte basée sur la marge 3) une protection contre les soldes négatifs par compte.

Les mesures de l'ESMA s'appliquent aux clients de détail. Les clients professionnels ne sont pas affectés.

Veuillez vous référer au document Application des règles de l'ESMA sur les CFD à IBKR pour plus d'informations.

I. Définition d'un CFD sur actions

Les CFD IBKR sont des contrats de gré à gré (OTC) qui offrent le rendement de l’action sous-jacente, y compris les dividendes et les opérations sur titres (en savoir plus sur les Opérations sur titres pour les CFD).

En d’autres termes, il s’agit d’un accord entre l’acheteur (vous) et IBKR visant à échanger la différence entre la valeur actuelle d’une action et sa valeur à une date ultérieure. Si vous détenez une position longue et que la différence est positive, IBKR vous paie. Si la différence est négative, vous payez IBKR.

Les CFD sur actions IBKRsont négociés sur votre compte de marge; vous pouvez donc trader aussi bien des positions longues que courtes avec effet de levier. Le prix des CFD correspond au prix coté sur la Bourse de l’action sous-jacente. Les prix des CFD IBKR sont en fait identiques aux prix "Smart-routed" pour les actions, comme vous pouvez l'observer sur la Trader Workstation. Par ailleurs, IB offre un accès direct au marché (DMA). Comme pour les actions, vos ordres non négociables (par ex. les ordres à cours limité) voient le hedge du sous-jacent directement inscrit dans la profondeur du carnet d’ordres des Bourses où il est négocié. Cela signifie également que vous pouvez acheter le CFD au cours acheteur du sous-jacent et le vendre au cours vendeur.

Pour comparer le modèle transparent d’IBKR à d’autres modèles disponibles sur le marché, consultez notre Aperçu des modèles du marché CFD.

IBKRoffre actuellement environ 7100 CFD sur actions couvrant les marchés principaux des États-Unis, de l'Europe et d' Asie. Les constituants des indices majeurs mentionnés ci-dessous sont actuellement disponibles sous forme de CFD sur actions IBKR. Dans de nombreux pays, IBKR offre également le trading d’actions liquides de faible capitalisation. Il s’agit d’actions dont la capitalisation boursière ajustée du flottant est de 500 millions d'USD minimum pour une valeur de trading médiane journalière de 600,000 USD minimum. Pour en savoir plus, consultez notre liste de produits CFD . D’autres pays seront bientôt ajoutés.

| États-Unis | S&P 500, DJA, Nasdaq 100, S&P 400 (Moy. Cap), Small cap liquides |

| Royaume-Uni | FTSE 350 + Small cap liquides (y compris. IOB) |

| Allemagne | Dax, MDax, TecDax + Small cap liquides |

| Suisse | Portion suisse du STOXX Europe 600 (48 actions) + Small cap liquides |

| France | CAC Large Caps, CAC Mid Caps + Small Cap liquides |

| Pays-Bas | AEX, AMS Mid Cap + Small Cap liquides |

| Belgique | BEL 20, BEL Mid Cap + Small Cap liquides |

| Espagne | IBEX 35 + Small Cap liquides |

| Portugal | PSI 20 |

| Suède | OMX Stockholm 30 + Small Cap liquides |

| Finlande | OMX Helsinki 25 + Small Cap liquides |

| Danemark | OMX Copenhagen 30 + Small Cap liquides |

| Norvège | OBX |

| République Tchèque | PX |

| Japon | Nikkei 225 + Small Cap liquides |

| Hong Kong | HSI + Small Cap liquides |

| Australie | ASX 200 + Small Cap liquides |

| Singapour* | STI + Small Cap liquides |

| Afrique du sud | Top 40 + Small Cap liquides |

*non disponible pour les résidents de Singapour

II. Comparaison entre les CFD et les actions sous-jacentes

Selon vos objectifs et votre style de trading, les CFD offrent un certain nombre d'avantages par rapport aux actions, mais également quelques inconvénients:

| AVANTAGES des CFD IBKR | INCONVÉNIENTS DES CFD IBKR |

|---|---|

| Pas de droit de timbre ou taxe sur les transactions financières (Royaume-Uni, Belgique, France) | Pas de droit de propriété |

| En général, les commissions et taux de marge sont moins élevés que pour les actions | Les opérations sur titres complexes ne peuvent pas toujours être reproduites |

| Taux de convention fiscale sans la nécessité de récupération | L'imposition des gains peut différer des actions (veuillez consulter votre conseiller fiscal) |

| Exemption des règles de day trading |

III. Coûts et marge

Les CFD IBKR peuvent être un moyen encore plus efficace de négocier sur les marchés boursiers européens plutôt que d’utiliser l’offre déjà très compétitive d'actions proposée par IB.

Tout d’abord, les CFD IBKR sont soumis à des commissions moins élevées que les actions, tout en offrant les mêmes spreads à faible financement:

| EUROPE | CFD | ACTION | |

|---|---|---|---|

| Commission | GBP | 0.05% | 6.00 + 0.05% GBP* |

| EUR | 0.05% | 0.10% | |

| Financement** | Benchmark +/- | 1.50% | 1.50% |

*par ordre + 0.05% plus franchise au delà de 50,000 GBP

**Financement CFD sur valeur totale de position, financement action sur montant emprunté

Plus vous négociez et plus les commissions des CFD baissent, jusqu'à 0,02%. Pour les positions portant sur des volumes importants, les frais de financement sont réduits et peuvent être de 0.5% seulement. Pour en savoir plus, consultez nos commissions CFD et Taux de financement CFD.

De plus, les CFD ont des exigences de marge moindre par rapport aux actions. Les clients de détail sont soumis à des exigences de marge supplémentaires comme l'impose l'ESMA, l'organisme régulateur européen. Veuillez consulter le document Application des règles de l'ESMA sur les CFD à IBKR pour plus d'informations.

| CFD | ACTION | ||

|---|---|---|---|

| Tous | Standard | Portfolio margin | |

| Exigence de marge de maintien* |

10% |

25% - 50% | 15% |

*Marge type pour les blue-chips. Les clients de détail sont soumis à une marge initiale minimum de 20%. Marge de maintien standard intraday de 25% pour les actions, 50% overnight. La marge de portefeuille (Portfolio Margin) indiquée est la marge de maintien (y compris overnight). Les émissions plus volatiles sont soumises à des exigences de marge plus importantes

Veuillez vous référer aux Exigences de marge pour les CFD pour plus d'informations.

IV. Exemple (Client professionnel)

Examinons l'exemple ci-dessous. Le listing d’Unilever Amsterdam a augmenté de 3.2% au cours du dernier mois (20 jours de trading au 14 mai 2012) et vous pensez que sa performance va se maintenir. , Vous souhaitez créer une exposition de 200,000 EUR et la conserver pendant 5 jours. Vous passez 10 ordres pour développer et 10 ordres pour déboucler. Vos coûts directs seraient comme suit:

ACTION

| CFD | ACTION | ||

|---|---|---|---|

| Position 200,000 EUR | Standard | Portfolio margin | |

| Exigence de marge | 20,000 | 100,000 | 30,000 |

| Commission (Aller Retour) | 200.00 | 400.00 | 400.00 |

| Taux d'intérêt (Simplifié) | 1.50% | 1.50% | 1.50% |

| Montant financé | 200,000 | 100,000 | 170,000 |

| Jours financés | 5 | 5 | 5 |

| Dépense en intérêts (1.5% Taux simplifié) | 41.67 | 20.83 | 35.42 |

| Coût total direct (Commission + Intérêt) | 241.67 | 420.83 | 435.42 |

| Différence de coût | 74% plus élevé | 80% plus élevé | |

Remarque: les intérêts des CFD sont calculés sur la position totale tandis que les intérêts des actions sont calculés sur le montant emprunté. Les taux appliqués sont les mêmes pour les CFD et les actions. Les intérêts applicables sont les mêmes pour les actions et pour les CFD

Mais supposons que vous n'ayez que 20,000 EUR de disponible pour financer la marge. Si Unilever maintient le même niveau de performance qu'au cours du mois passé, votre gain potentiel serait aux alentours de:

| GAIN EFFET DE LEVIER | CFD | ACTION | |

|---|---|---|---|

| Marge disponible | 20,000 | 20,000 | 20,000 |

| Total investi | 200,000 | 40,000 | 133,333 |

| Rendement brut (5 Days) | 1,600 | 320 | 1,066.66 |

| Commission | 200.00 | 80.00 | 266.67 |

| Dépense en intérêts (1.5% Taux simplifié) | 41.67 | 4.17 | 23.61 |

| Coût total direct (Commission + Interest) | 241.67 | 84.17 | 290.28 |

| Rendement net (Rendement brut moins coût direct) | 1,358.33 | 235.83 | 776.39 |

| Montant d'investissement du rendement sur marge | 0.07 | 0.01 | 0.04 |

| Différence | 83% moins Gain | 43% moins Gain | |

| RISQUE EFFET DE LEVIER | CFD | ACTION | |

|---|---|---|---|

| Marge disponible | 20,000 | 20,000 | 20,000 |

| Total investi | 200,000 | 40,000 | 133,333 |

| Rendement brut (5 Days) | -1,600 | -320 | -1,066.66 |

| Commission | 200.00 | 80.00 | 266.67 |

| Dépense en intérêts (1.5% Taux simplifié) | 41.67 | 4.17 | 23.61 |

| Coût total direct (Commission + Interest) | 241.67 | 84.17 | 290.28 |

| Rendement net (Rendement brut moins coût direct) | -1,841.67 | -404.17 | -1,356.94 |

| Différence | 78% Moins Perte | 26% Moins Perte | |

V. Ressources CFD

Vous trouverez ci-dessous des liens utiles contenant des informations plus détaillées sur l’offre des CFD IBKR:

Le tutoriel suivant est également disponible:

Comment passer un ordre de CFD sur la Trader Workstation

VI. Foire aux questions

Quelles actions sont disponibles en tant que CFD?

Les actions de forte et moyenne capitalisation aux États-Unis, en Europe de l'ouest, dans les pays nordiques et au Japon. Les actions de faible capitalisation liquides sont également disponibles sur de nombreux marchés. Veuillez consulter la page Liste de produits CFD pour plus d'informations. D'autres pays seront ajoutés très prochainement.

Avez-vous des CFD pour des indices sur actions et Forex?

Oui. Veuillez consulter la page CFD sur indices IBKR - Informations et questions et CFD sur Forex - Informations et questions.

Comment sont déterminées les cotations des CFD sur actions?

Le prix des CFD IBKR correspond à la cotation via Smartrouting de l’action sous-jacente. IBKR n'élargit pas le spread ni ne détient de positions en votre défaveur. Pour en savoir plus, veuillez consulter l'aperçu des modèles du marché CFD.

Puis-je voir mes ordres à cours limité sur la Bourse?

Oui. IBKRoffre un accès direct au marché (DMA). Comme les actions, les ordres qui ne sont pas négociables (par ex. les ordres à cours limité) bénéficient de la protection du sous-jacent qui est directement inscrit sur le carnet d’ordres des bourses où il est négocié. Cela signifie également que vous pouvez acheter le CFD au cours acheteur du sous-jacent et le vendre au cours vendeur. De plus, vous recevrez peut-être une amélioration de prix si l'ordre d'un autre client peut être croisé au vôtre à un meilleur prix que celui disponible sur les marchés.

Comment déterminez-vous les marges des CFD sur actions?

IBKR établit des exigences de marge sur la base de la volatilité historique de chaque action sous-jacente. La marge minimum est de 10% Ce taux de marge est généralement appliqué à la plupart des CFD IBKR, ce qui rend le trading de CFD plus attractif en termes de marge que le trading du sous-jacent. Les investisseurs de détail sont soumis à des exigences de marge supplémentaires imposées par ESMA, l'organisme

régulateur européen. Veuillez consulter le document Application des règles de l'ESMA sur les CFD à IBKR pour plus d'informations. Il n'y a pas de compensation de portefeuille entre des positions CFD individuelles ou entre des positions CFD et l'exposition à l’action sous-jacente. Les positions concentrées et portant sur de gros volumes peuvent être soumises à des marges supplémentaires. Pour en savoir plus, veuillez consulter les exigences de marge des CFD.

Les CFD sur action courts sont-ils soumis à des rachats forcés ?

Oui. Si l’action sous-jacente devient difficile ou impossible à emprunter, le détenteur de la position sera soumis à un rachat.

Comment traitez-vous les dividendes et opérations sur titre?

En règle générale, IBKR reflète l'effet économique de l’opération sur titre pour les détenteurs de CFD comme s'ils détenaient les titres sous-jacent*. Les dividendes sont comptabilisés sous forme d'ajustement de liquidité, tandis que d'autres actions peuvent être comptabilisées sous forme d'ajustement de liquidité, d'ajustement de position ou une combinaison des deux. Par exemple, si les actions d'entreprise se traduisent par un changement du nombre d’actions (par ex. dans le cas de fractionnement d'actions ou fractionnement d'actions inversé), le nombre de CFD est ajusté en conséquence. Lorsque l’action devient une nouvelle entité et qu'IBKR décide de la proposer comme CFD, de nouvelles positions courtes et longues sont créées dans la quantité appropriée. Pour en savoir plus, consultez la page CFD - Opérations sur titre.

*Dans certains cas, il ne sera pas possible d'ajuster de manière exacte le CFD, comme pour une opération sur titres complexe telle qu'une fusion par exemple. Dans ce cas, IBKR pourra clôturer la position de CFD avant la date de détachement.

Tout le monde peut-il trader des CFD IBKR?

Tous les clients peuvent trader des CFD IBKR à l'exception des résidents des États-Unis, du Canada et de Hong Kong. Les résidents de Singapour peuvent trader des CFD IBKR à l'exception de ceux basés sur des actions cotées à Singapour. Il n'existe pas d'exemption aux exclusions sur la base de la résidence en fonction du type d'investisseur.

Que dois-je faire pour commencer à trader des CFD avec IBKR?

Vous devez mettre en place les autorisations de trading pour les CFD dans la Gestion de compte et accepter les déclarations adéquates. Si vous détenez un compte auprès d'IB LLC, IBKR créera un nouveau segment de compte (identifié avec votre numéro de compte existant par le suffixe “F”). Une fois le segment confirmé, vous pourrez commencer à trader. Vous n'avez pas besoin d'approvisionner le compte "F" séparément, les fonds seront automatiquement transférés en fonction des exigences de marge de votre compte principal.

Existe t-il des conditions en termes de données de marché?

Les données de marché pour les CFD sur actions IBKR sont les mêmes que les données de marché des actions sous-jacentes. Il est par conséquent nécessaire d'obtenir les autorisations de données de marché pour les Bourses correspondantes. Si vous avez déjà mis en place des autorisations de données de marché pour une Bourse afin de pouvoir trader des actions, aucune autre action n'est requise. Si vous souhaitez trader des CFD sur une Bourse pour laquelle vous n'avez pas actuellement d'autorisation de données de marché, vous pouvez mettre en place des autorisations de trading de la même manière que si vous envisagiez de trader les actions sous-jacentes.

Mes transactions de CFD apparaissent-elles dans mes relevés de compte?

Si vous détenez un compte auprès d'IBLLC, vos positions de CFD sont détenues dans un segment de compte distinct identifié par le suffixe "F" et votre numéro de compte principal. Vous pouvez choisir de visualiser les relevés de compte pour ce segment "F" soit séparément, soit de manière consolidée avec votre compte principal. Vous pouvez sélectionner l'option de votre choix dans la fenêtre des relevés de la Gestion de compte. Pour les autres comptes, les CFD sont affichés normalement dans le relevé de compte comme les autres produits de trading.

Puis-je transférer mes positions CFD depuis un autre courtier?

IBKR ne permet pas le transfert de positions de CFD à l'heure actuelle.

Des graphiques sont-ils disponibles pour les CFD?

Oui.

Quelles protections de compte s’appliquent au trading de CFD émis pas IBKR?

Les CFD sont des contrats émis par IB UK qui agit en tant que contrepartie. Ils ne sont donc pas négociés sur un marché réglementé et ne sont pas compensés par une chambre de compensation centrale. Étant donné qu’IB UK est votre contrepartie pour les CFD, vous êtes exposé à des risques financiers et commerciaux, y compris le risque de crédit associé à la réalisation de transactions avec IB Royaume-Uni. Veuillez noter cependant que tous les fonds des clients sont toujours totalement ségrégés, y compris ceux des clients institutionnels. IB UK est membre du programme UK Financial Services Compensation Scheme (FSCS). IB UK n'est pas un membre de la U.S. Securities Investor Protection Corporation (“SIPC”). Veuillez consulter la déclaration des risques liés aux CFD IB UK pour davantage d'informations sur les risques liés au trading de CFD.

Avec quel type de compte IBKR puis-je négocier des CFD (par ex. compte individuel, institutionnel, Amis et famille, etc.)?

Tous les comptes de marge sont éligibles au trading de CFD. Les comptes au comptant et SIPP ne sont pas éligibles.

Combien de positions maximum puis-je avoir pour un CFD spécifique?

Pas de limite pré-établie. Cependant, rappelez-vous que les positions très importantes peuvent être soumises à une augmentation des exigences de marge. Pour en savoir plus, veuillez consulter les exigences de marge des CFD.

Puis-je trader des CFD par téléphone?

Non. Cependant, dans certains cas exceptionnels, nous pouvons accepter de traiter des ordres de fermeture par téléphone mais jamais des ordres d'ouverture.

Excess Margin Securities

The term "excess margin securities" refers to margin securities carried for the account of a customer having a market value in excess of 140 percent of the total debit balance in the customer's account. These securities are in excess of the securities held in a customer's margin account that are pledged by the customer as collateral for the margin loan and can be used to support the purchase of additional securities on margin

Example:

A customer whose account equity consists solely of a cash balance of USD 10,000 on Day 1 purchases 400 shares of stock ABC at USD 50 per share on Day 2.

| Account Balance | Day 1 | Day 2 |

| Cash | $10,000 | ($10,000) |

| Stock | $0 | $20,000 |

| Total | $10,000 | $10,000 |

On Day 2, the customer's excess margin securities total USD 6,000. This is calculated by subtracting 140% of the margin debit or loan balance from the market value of the stock position ($6,000 = $20,000 - {1.4 * $10,000}).

The term is relevant from a regulatory perspective as the SEC requires that U.S. broker dealers segregate and maintain in a good control location (e.g., DTC or bank) all customer securities which are deemed excess margin securities. Such securities cannot be pledged or loaned to finance the activities of the firm or other customers without specific written permission from the customer. The portion of the securities classified as margin securities ($20,000 - $6,000 or $14,000 in this example) are subject to a lien and may be pledged or loaned by the broker to others to assist in financing the loan made to the customer.

Note that securities which were excess margin at the date of acquisition may later be reclassified as margin securities based upon the customer's subsequent trade and/or margin borrowing activity. For example, if the loan value of excess margin securities is subsequently used to acquire additional securities on margin, a portion of securities will then be reclassified as margin securities and subject to a lien. If the customer subsequently deposits cash or sells securities to reduce or eliminate the margin loan, the securities will be reclassified as excess margin or fully paid and are required to be segregated.

See also "fully paid securities".

Fully Paid Securities

The term "fully paid securities" refers to securities held in a customer's margin or cash account that have been completely paid for and are not being pledged as collateral to support the purchase of other securities on margin. The term is relevant from a regulatory perspective as the SEC requires that U.S. broker dealers segregate and maintain in a good control location (e.g., DTC or bank) all customer securities which are fully paid. Such securities cannot be pledged or loaned to finance the activities of the firm or other customers.

Note that securities which were fully paid at the date of acquisition may later be reclassified as margin or excess margin securities based upon the customer's subsequent trade and/or borrowing activity. For example, if the loan value of fully paid securities is subsequently used to acquire additional securities on credit, a portion of securities will then be classified as margin securities and subject to a lien and potential pledge or hypothecation by the broker.

See also "excess margin securities".

Overview of IBKR issued Share CFDs

The following article is intended to provide a general introduction to share-based Contracts for Differences (CFDs) issued by IBKR.

For Information on IBKR Index CFDs click here. For Forex CFDs click here. For Precious Metals click here.

Topics covered are as follows:

I. CFD Definition

II. Comparison Between CFDs and Underlying Shares

III. CFD Tax and Margin Advantage

IV. US ETFs

V. CFD Resources

VI. Frequently Asked Questions

Risk Warning

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage.

61% of retail investor accounts lose money when trading CFDs with IBKR.

You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

ESMA Rules for CFDs (Retail Clients only)

The European Securities and Markets Authority (ESMA) has enacted new CFD rules effective 1st August 2018.

The rules include: 1) leverage limits on the opening of a CFD position; 2) a margin close out rule on a per account basis; and 3) negative balance protection on a per account basis.

The ESMA Decision is only applicable to retail clients. Professional clients are unaffected.

Please refer to the following articles for more detail:

ESMA CFD Rules Implementation at IBKR (UK) and IBKR LLC

ESMA CFD Rules Implementation at IBIE and IBCE

I. Share CFD Definition

IBKR CFDs are OTC contracts which deliver the return of the underlying stock, including dividends and corporate actions (read more about CFD corporate actions).

Said differently, it is an agreement between the buyer (you) and IBKR to exchange the difference in the current value of a share, and its value at a future time. If you hold a long position and the difference is positive, IBKR pays you. If it is negative, you pay IBKR.

IBKR Share CFDs are traded through your cash or margin account, and you can enter long as well as short leveraged positions. The price of the CFD is the exchange-quoted price of the underlying share. In fact, IBKR CFD quotes are identical to the Smart-routed quotes for shares that you can observe in the Trader Workstation and IBKR offers Direct Market Access (DMA). Similar to shares, your non-marketable (i.e. limit) orders have the underlying hedge directly represented on the deep book of those exchanges at which it trades. This also means that you can place orders to buy the CFD at the underlying bid and sell at the offer.

To compare IBKR’s transparent CFD model to others available in the market please see our Overview of CFD Market Models.

IBKR currently offers approximately 8000 Share CFDs covering the principal markets in the US, Europe and Asia. The constituents of the major indexes listed below are currently available as IBKR Share CFDs. In many countries IBKR also offers trading in liquid small cap shares. These are shares with free float adjusted market capitalization of at least USD 500 million and median daily trading value of at least USD 600 thousand. Please see CFD Product Listings for more detail. More countries will be added in the near future.

| United States | S&P 500, DJA, Nasdaq 100, S&P 400 (Mid Cap), Liquid Small Cap |

| United Kingdom | FTSE 350 + Liquid Small Cap (incl. IOB) |

| Germany | Dax, MDax, TecDax + Liquid Small Cap |

| Switzerland | Swiss portion of STOXX Europe 600 (48 shares) + Liquid Small Cap |

| France | CAC Large Cap, CAC Mid Cap + Liquid Small Cap |

| Netherlands | AEX, AMS Mid Cap + Liquid Small Cap |

| Belgium | BEL 20, BEL Mid Cap + Liquid Small Cap |

| Spain | IBEX 35 + Liquid Small Cap |

| Portugal | PSI 20 |

| Sweden | OMX Stockholm 30 + Liquid Small Cap |

| Finland | OMX Helsinki 25 + Liquid Small Cap |

| Denmark | OMX Copenhagen 30 + Liquid Small Cap |

| Norway | OBX |

| Czech | PX |

| Japan | Nikkei 225 + Liquid Small Cap |

| Hong Kong | HSI + Liquid Small Cap |

| Australia | ASX 200 + Liquid Small Cap |

| Singapore | STI + Liquid Small Cap |

| South Africa | Top 40 + Liquid Small Cap |

| Brazil | Bovespa |

| Russia | MOEX |

II. Comparison Between CFDs and Underlying Shares

Depending on your trading objectives and trading style, CFDs offer a number of advantages compared to stocks, but also some disadvantages:

| BENEFITS of IBKR CFDs | DRAWBACKS of IBKR CFDs |

|---|---|

| No stamp duty or financial transaction tax (UK, France, Belgium, Spain) | No ownership rights |

| Generally lower margin rates than shares* | Complex corporate actions may not always be exactly replicable |

| Tax treaty rates for dividends without need for reclaim | Taxation of gains may differ from shares (please consult your tax advisor) |

| Exemption from day trading rules | |

| US ETFs tradable as CFDs** |

*IB LLC and IB-UK accounts.

**EEA area clients cannot trade US ETFs directly, as they do not publish KIDs.

III. CFD Tax and Margin Advantage

Where stamp duty or financial transaction tax is applied, currently in the UK (0.5%), France (0.3%), Belgium (0.35%) and Spain (0.2%), it has a substantially detrimental impact on returns, particular in an active trading strategy. The taxes are levied on buy-trades, so each time you open a long, or close a short position, you will incur tax at the rates described above.

The amount of available leverage also significantly impacts returns. For European IBKR entities, margin requirements are risk-based for both stocks and CFDs, and therefore generally the same. IB-UK and IB LLC accounts however are subject to Reg T requirements, which limit available leverage to 2:1 for positions held overnight.

To illustrate, let's assume that you have 20,000 to invest and wish to leverage your investment fully. Let's also assume that you hold your positions overnight and that you trade in and out of positions 5 times in a month.

Let's finally assume that your strategy is successful and that you have earned a 5% return on your gross (fully leveraged) investment.

The table below shows the calculation in detail for a UK security. The calculations for France, Belgium and Spain are identical, except for the tax rates applied.

| UK CFD | UK Stock | UK Stock | |

|---|---|---|---|

| All Entities |

EU Account

|

IB LLC or IBUK Acct

|

|

| Tax Rate | 0% | 0.50% | 0.50% |

| Tax Basis | N/A | Buy Orders | Buy Orders |

| # of Round trips | 5 | 5 | 5 |

| Commission rate | 0.05% | 0.05% | 0.05% |

| Overnight Margin | 20% | 20% | 50% |

| Financing Rate | 1.508% | 1.508% | 1.508% |

| Days Held | 30 | 30 | 30 |

| Gross Rate of Return | 5% | 5% | 5% |

| Investment | 100,000 | 100,000 | 40,000 |

| Amount Financed | 100,000 | 80,000 | 20,000 |

| Own Capital | 20,000 | 20,000 | 20,000 |

| Tax on Purchase | 0.00 | 2,500.00 | 1,000.00 |

| Round-trip Commissions | 500.00 | 500.00 | 200.00 |

| Financing | 123.95 | 99.16 | 24.79 |

| Total Costs | 623.95 | 3099.16 | 1224.79 |

| Gross Return | 5,000 | 5,000 | 2,000 |

| Return after Costs | 4,376.05 | 1,900.84 | 775.21 |

| Difference | -57% | -82% |

The following table summarizes the reduction in return for a stock investment, by country where tax is applied, compared to a CFD investment, given the above assumptions.

| Stock Return vs cfD | Tax Rate | EU Account | IB LLC or IBUK Acct |

|---|---|---|---|

| UK | 0.50% | -57% | -82% |

| France | 0.30% | -34% | -73% |

| Belgium | 0.35% | -39% | -75% |

| Spain | 0.20% | -22% | -69% |

IV. US ETFs

EEA area residents who are retail investors must be provided with a key information document (KID) for all investment products. US ETF issuers do not generally provide KIDs, and US ETFs are therefore not available to EEA retail investors.

CFDs on such ETFs are permitted however, as they are derivatives for which KIDs are available.

Like for all share CFDs, the reference price for CFDs on ETFs is the exchange-quoted, SMART-routed price of the underlying ETF, ensuring economics that are identical to trading the underlying ETF.

V. CFD Resources

Below are some useful links with more detailed information on IBKR’s CFD offering:

The following video tutorial is also available:

How to Place a CFD Trade on the Trader Workstation

VI. Frequently Asked Questions

What Stocks are available as CFDs?

Large and Mid-Cap stocks in the US, Western Europe, Nordic and Japan. Liquid Small Cap stocks are also available in many markets. Please see CFD Product Listings for more detail. More countries will be added in the near future.

Do you have CFDs on other asset classes?

Yes. Please see IBKR Index CFDs - Facts and Q&A, Forex CFDs - Facts and Q&A and Metals CFDs - Facts and Q&A.

How do you determine your Share CFD quotes?

IBKR CFD quotes are identical to the Smart routed quotes for the underlying share. IBKR does not widen the spread or hold positions against you. To learn more please go to Overview of CFD Market Models.

Can I see my limit orders reflected on the exchange?

Yes. IBKR offers Direct market Access (DMA) whereby your non-marketable (i.e. limit) orders have the underlying hedges directly represented on the deep books of the exchanges on which they trade. This also means that you can place orders to buy the CFD at the underlying bid and sell at the offer. In addition, you may also receive price improvement if another client's order crosses yours at a better price than is available on public markets.

How do you determine margins for Share CFDs?

IBKR establishes risk-based margin requirements based on the historical volatility of each underlying share. The minimum margin is 10%, making CFDs more margin-efficient than trading the underlying share in many cases. Retail investors are subject to additional margin requirements mandated by the European regulators. There are no portfolio off-sets between individual CFD positions or between CFDs and exposures to the underlying share. Concentrated positions and very large positions may be subject to additional margin. Please refer to CFD Margin Requirements for more detail.

Are short Share CFDs subject to forced buy-in?

Yes. In the event the underlying stock becomes difficult or impossible to borrow, the holder of the short CFD position may become subject to buy-in.

How do you handle dividends and corporate actions?

IBKR will generally reflect the economic effect of the corporate action for CFD holders as if they had been holding the underlying security. Dividends are reflected as cash adjustments, while other actions may be reflected through either cash or position adjustments, or both. For example, where the corporate action results in a change of the number of shares (e.g. stock-split, reverse stock split), the number of CFDs will be adjusted accordingly. Where the action results in a new entity with listed shares, and IBKR decides to offer these as CFDs, then new long or short positions will be created in the appropriate amount. For an overview please CFD Corporate Actions.

*Please note that in some cases it may not be possible to accurately adjust the CFD for a complex corporate action such as some mergers. In these cases IBKR may terminate the CFD prior to the ex-date.

Can anyone trade IBKR CFDs?

All clients can trade IBKR CFDs, except residents of the USA, Canada, Hong Kong, New Zealand and Israel. There are no exemptions based on investor type to the residency based exclusions.

What do I need to do to start trading CFDs with IBKR?

You need to set up trading permission for CFDs in Client Portal, and agree to the relevant disclosures. If your account is with IBKR (UK) or with IBKR LLC, IBKR will then set up a new account segment (identified with your existing account number plus the suffix “F”). Once the set-up is confirmed you can begin to trade. You do not need to fund the F-account separately, funds will be automatically transferred to meet CFD initial margin requirements from your main account.

If your account is with another IBKR entity, only the permission is required; an additional account segment is not necessary.

Are there any market data requirements?

The market data for IBKR Share CFDs is the market data for the underlying shares. It is therefore necessary to have market data permissions for the relevant exchanges. If you already have market data permissions for an exchange for trading the shares, you do not need to do anything. If you want to trade CFDs on an exchange for which you do not currently have market data permissions, you can set up the permissions in the same way as you would if you planned to trade the underlying shares.

How are my CFD trades and positions reflected in my statements?

If you are a client of IBKR (U.K.) or IBKR LLC, your CFD positions are held in a separate account segment identified by your primary account number with the suffix “F”. You can choose to view Activity Statements for the F-segment either separately or consolidated with your main account. You can make the choice in the statement window in Client Portal.

If you are a client of other IBKR entities, there is no separate segment. You can view your positions normally alongside your non-CFD positions.

Can I transfer in CFD positions from another broker?

IBKR does not facilitate the transfer of CFD positions at this time.

Are charts available for Share CFDs?

Yes.

In what type of IBKR accounts can I trade CFDs e.g., Individual, Friends and Family, Institutional, etc.?

All margin and cash accounts are eligible for CFD trading.

What are the maximum a positions I can have in a specific CFD?

There is no pre-set limit. Bear in mind however that very large positions may be subject to increased margin requirements. Please refer to CFD Margin Requirements for more detail.

Can I trade CFDs over the phone?

No. In exceptional cases we may agree to process closing orders over the phone, but never opening orders.

IBKR Stock Yield Enhancement Program

PROGRAM OVERVIEW

The Stock Yield Enhancement Program provides the opportunity to earn extra income on the fully-paid shares of stock held in your account by allowing IBKR to borrow shares from you in exchange for collateral (either U.S. Treasuries or cash), and then lend the shares to traders who want to sell them short and are willing to pay interest to borrow them. For additional information on the Stock Yield Enhancement Program please see here or review the Frequently Asked Questions page.

HOW TO ENROLL IN THE STOCK YIELD ENHANCEMENT PROGRAM

To enroll, please login to the Client Portal. Once logged in, click the User menu (head and shoulders icon in the top right corner) followed by Settings.

In the Trading section of the Settings page, click the link for the Stock Yield Enhancement Program. Select the checkbox on the next screen and click Continue. You will then be presented with the requisite forms and disclosures needed to enroll in the program. Once you have reviewed and signed the forms, your request will be submitted for processing. Please allow 24-48 hours for enrollment to become active.

.png)

.png)

Considerations for Optimizing Order Efficiency

Account holders are encouraged to routinely monitor their order submissions with the objective of optimizing efficiency and minimizing 'wasted' or non-executed orders. As inefficient orders have the potential to consume a disproportionate amount of system resources. IB measures the effectiveness of client orders through the Order Efficiency Ratio (OER). This ratio compares aggregate daily order activity relative to that portion of activity which results in an execution and is determined as follows:

OER = (Order Submissions + Order Revisions + Order Cancellations) / (Executed Orders + 1)

Outlined below is a list of considerations which can assist with optimizing (reducing) one's OER:

1. Cancellation of Day Orders - strategies which use 'Day' as the Time in Force setting and are restricted to Regular Trading Hours should not initiate order cancellations after 16:00 ET, but rather rely upon IB processes which automatically act to cancel such orders. While the client initiated cancellation request which serve to increase the OER, IB's cancellation will not.

2. Modification vs. Cancellation - logic which acts to cancel and subsequently replace orders should be substituted with logic which simply modifies the existing orders. This will serve to reduce the process from two order actions to a single order action, thereby improving the OER.

3. Conditional Orders - when utilizing strategies which involve the pricing of one product relative to another, consideration should be given to minimizing unnecessary price and quantity order modifications. As an example, an order modification based upon a price change should only be triggered if the prior price is no longer competitive and the new suggested price is competitive.

4. Meaningful Revisions – logic which serves to modify existing orders without substantially increasing the likelihood of the modified order interacting with the NBBO should be avoided. An example of this would be the modification of a buy order from $30.50 to $30.55 on a stock having a bid-ask of $31.25 - $31.26.

5. RTH Orders – logic which modifies orders set to execute solely during Regular Trading Hours based upon price changes taking place outside those hours should be optimized to only make such modifications during or just prior to the time at which the orders are activated.

6. Order Stacking - Any strategy that incorporates and transmits the stacking of orders on the same side of a particular underlying should minimize transmitting those that are not immediately marketable until the orders which have a greater likelihood of interacting with the NBBO have executed.

7. Use of IB Order Types - as the revision logic embedded within IB-supported order types is not considered an order action for the purposes of the OER, consideration should be given to using IB order types, whenever practical, as opposed to replicating such logic within the client order management logic. Logic which is commonly initiated by clients and whose behavior can be readily replicated by IB order types include: the dynamic management of orders expressed in terms of an options implied volatility (Volatility Orders), orders to set a stop price at a fixed amount relative to the market price (Trailing Stop Orders), and orders designed to automatically maintain a limit price relative to the NBBO (Pegged-to-Market Orders).

The above is not intended to be an exhaustive list of steps for optimizing one's orders but rather those which address the most frequently observed inefficiencies in client order management logic, are relatively simple to implement and which provide the opportunity for substantive and enduring improvements. For further information or questions, please contact the Customer Service Technical Assistance Center.